10 things that happened in 2014

I had planned to write about five nice things and five nasty ones, but it hasn’t been that kind of year. Instead I have chosen three nice things and seven nasty ones. These ten events can be grouped into four themes: taxes, costs, diversification and valuation.

Three nice things

Here are my three nice things from 2014:

- Pension reforms – tax

- ISA reforms – tax

- Biotech out performance – valuation

Seven nasty things

And here are seven nasty ones:

- Stamp Duty changes – tax

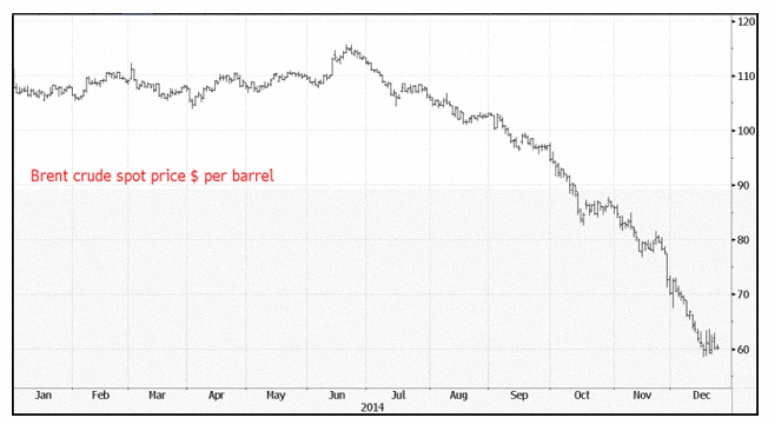

- Oil Price crash – valuation

- Tesco crash and the supermarket wars – diversification

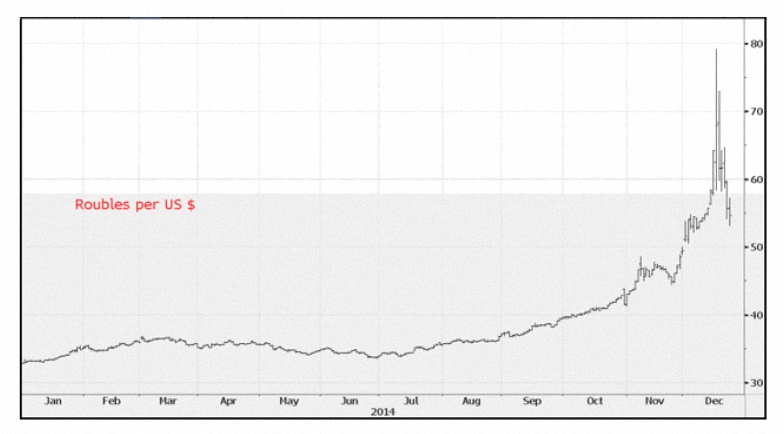

- Russian crisis: market and rouble crash – valuation

- Bonds got even more expensive – valuation

- Interest rates stayed low – valuation

- Woodford fund launch – costs

Taxes

The pension reforms are very welcome. Those people ((Disclosure #1 – I am one of them)) who have diligently funded their SIPPs since Gordon Brown raised the contribution limits ten years ago have at last been rewarded.

From April 2015 they are free to withdraw as much cash as they wish subject to normal taxation. How many really will pay 40% and 45% to get early access remains to be seen, but at least people have the choice. I will be sticking below the £42K higher-rate threshold.

The removal of the annuity requirement and the relaxation of tax penalties when passing pensions on to descendent are also welcome. Similarly, passing on of ISAs between spouses is a good thing, as is the raising of the annual contribution limit to £15K. Added to the pension limit of £40K, the ability to shelter £55K per year is more than adequate for long-term thinkers.

On the debit side we have the stamp duty changes, which were welcomed by most observers. While replacing the slab duty system with a gradual tax is easy to support, marginal rates of 12% can have only one effect – to slow the market. I can’t see why reduced liquidity is ever a good idea. High-end prices in London duly cooled, and more importantly, market activity dwindled.

It’s easy to understand why a Tory Chancellor might introduce the measure in an election year, but here at 7C we need to favour the long-term view, and I don’t see how this has fixed the UK property market. It’s a nice idea to think that the top-end of the market is distinct from the bottom, but property doesn’t work like that, particularly in a crowded island that has only one region capable of driving economic growth.

Costs

Neil Woodford’s move from Invesco to set up his own fund led to £4bn of retail funds being shifted around and a vast advertising spend. Though Woodford is a good example of a true active manager, it highlights the problems with open-ended active funds – they are essentially part of an enormous marketing machine which slowly erodes investor’s funds (mainly through ongoing charges rather than marketing and management costs).

In the long run, a mixture of direct investment (in easily accessible markets like the UK and the US) and listed passive and/or closed-end funds (ETFs and investment trusts) elsewhere will better serve most people than the closet trackers pushed by most platforms and advisors.

Diversification

The real lesson from the Tesco crash is that you must diversify. Relying on big names and safe sectors will find you out in the end, since nothing lasts forever. ((Disclosure #2 – I hold Tesco, along with most of the UK supermarkets)) Terry Smith had been avoiding Tesco for years because of its falling return on capital, despite steadily rising earnings per share. More and more capital was being deployed at lower rates of return. The US and China operations never worked.

Valuations

We had every flavour of price change this year, and not too much mean reversion.

- Oil fell suddenly, and further that most people predicted.

- “Cheap” things got cheaper. The Russian market has had a low PE for years (it began 2014 at 5 vs 15 for the UK market) and many stocks were priced below book value. But still the market went down in reaction to the oil price crash, the rouble crisis and geo-political tensions.

- The same thing applies in reverse. Just because bond yields were at record lows didn’t mean that bond prices would fall in 2014 (or that they will in 2015). They duly rose once again.

- Interest rates remained at record lows.

- Biotech had another good year, despite recent outperformance.

Oil was a surprise to me. I expected some impact from US shale production, but not this much, and I wasn’t expecting OPEC to sit back as the price slid below $60 a barrel. The potential impacts of the low oil price are complicated, and I will return to this in another post.

The key to interpreting all of this price “strangeness” is to consider your time horizon: if you want to pick the winning market for next year, looking for the cheapest one at the start of the year is not the way to go. If you want to invest for 25 years, it might well be.

Similarly, while bond rates didn’t fall this year, if you are investing for the long-term, you must fear that they will fall eventually, and that this may not be the best time to buy. With the low yields on offer in comparison to stocks they don’t look a good long-term bet.

As for interest rates, back in 2008, few would have predicted six years of record low interest rates, but now it’s hard to see how the global economy will ever recover sufficiently to allow them to be raised. Deflation seems more of a threat than inflation. Low rates are hard on investors, but deflation would be worse, and the the 7C philosophy is not very reliant on fixed-income.

With biotech, though it’s tempting to hang on for the ride, the sensible thing is to take some profits and look at re-balancing your portfolio. At the very least, think about adding new money elsewhere. The same goes for any other areas that have out performed.

Sources

- Seven lessons I learned from the financial events of 2014, Richard Dyson – Daily Telegraph 21/12/14

- The five charts that sum up 2014, John Stepek – MoneyWeek.com

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London.

He has been managing his own money for 40 years, with some success.