Weekly Roundup, 22nd November 2016

We begin today’s Weekly Roundup as usual in the FT, with the Chart That Tells A Story. This week it was about property shares.

Contents

After Trump, all eyes are now on this week’s Autumn Statement, so it was another thin week for general news.

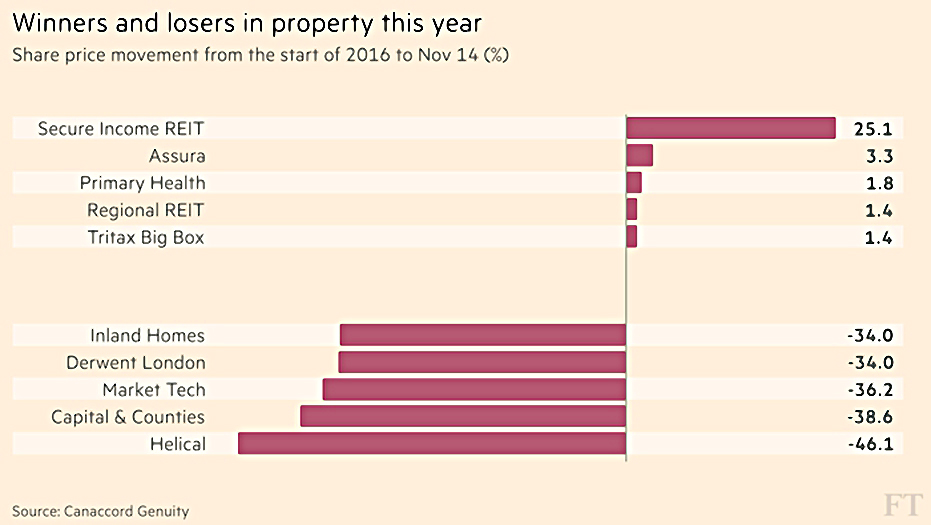

In the FT, Judith Evans looked at the performance of property stocks in 2016, and in particular at the effect of the Brexit vote.

- In general, the asset class fell, but as you can see from the chart below, Secure Income REIT was the exception.

Secure Income owns theme parks like Thorpe Park and Alton Towers, and lets them on long leases of around 20 years.

- This means that its income is secure and investors feel safe.

- Secure aims to yield 6.5% pa.

The big losers this year have been:

- companies exposed to London, which might suffer from post-Brexit flight, and

- those with lots of developments underway – these might not be successfully let

Helical Bar is down 46% on the back of its large London holdings (almost 50%).

Other modest winners like Assura and Primary Health specialise in healthcare properties, let on long leases to public-sector clients.

- Regional and Tritax Big Box have no London exposure.

In general, property firms hold less debt than 10 years ago, and with yields far above those on bonds, they should be well-supported from here.

- A Brexit calamity could hit the London-based stocks once again, though.

Infrastructure

Aime Williams and Naomi Rovnick looked at how Trump’s plans for infrastructure investment – and similar plans in the UK – might affect private investors.

There are four ways to play this opportunity (assuming that you believe the investment will materialise):

- investment trusts (many of which we covered a few weeks ago)

- ETFs

- funds, and

- companies directly involved in infrastructure

The seven UK-listed investment trusts include:

- HICL Infrastructure

- 3i Infrastructure (described as “expensive”, at 1.36% pa)

The main problem with these trusts – for the purposes of the Trumpian analysis – is that they don’t have much US exposure (though this could conceivably change if Trump triggers a lot of new projects).

ETFs include those from Deutsche (x-trackers), BlackRock (iShares) and State Street (SPDR).

- These track indices from S&P, MSCI, FTSE, Morningstar and Macquarie.

- S&P’s index is mostly utilities and industrials.

- Morningstar’s index is similar, but includes bonds as well as stocks.

- MSCI’s index includes more telecoms, which may not benefit from the Trumpian stimulus.

- The ETFs typically have 40% in US holdings.

The funds include:

- Lazard Global Listed Infrastructure Equity

- Legg Maxon Rare Infrastructure, and

- First State Global Listed Infrastructure

Some advisers recommend just buying “supply chain” US equities (cement and sand companies, for example).

The article also suggested that “Infrastructure bonds” aimed at retail investors might be unveiled in this Autumn Statement later this week – let’s see.

Biotech

David Stevenson looked at investing in biotech, which has bounced on the back of the Trump win (since Hilary planned to cap drug prices, and Trump will dilute Obamacare).

We’ve talked about two biotech investment trusts before:

- Biotech Growth, which is still only trading on a PE of 11.1 (less than the S&P at 16, and very low compared with a long-term average PE of 23.1)

- Polar Capital Global Healthcare

A third fund – BB Healthcare (BBH) – will list in London by the end of November.

David also wrote about recent developments at BACIT, the “battle against cancer” trust.

- This is a hedge fund of funds run for free, that contributes 1% pa to cancer charities.

- It’s an absolute return fund, so it underperforms in bull markets and outperforms in bear markets.

- It’s also not highly correlated with equity markets, and yields 1.75%.

BACIT now plans to change radically, with help from the Wellcome Foundation and Cancer Research UK (CRUK):

- BACIT will buy Syncona – a portfolio of life science investments – from Wellcome.

- BACIT will also buy most or all of CRUK’s CRT Pioneer Fund.

David is excited about being able to buy into life science assets at close to book value, with upside potential if they re-rate to the levels of the other trusts

- That’s true, and this is probably good news for cancer research, but it’s not all positive for private investors.

- We already have three biotech trusts, whereas the old BACIT was almost unique.

Uncorrelated hedge funds accessible by retail investors are a dying breed, and I can’t cheer another departure.

US institutions

John Authers was worried that Trump might damage US institutions, provoking a backlash from investors.

There’s been a big swing – 10% in a week or so – towards the US and away from emerging markets (EMs) since Trump was elected:

The big worry for EMs is trade protectionism, of course, but higher US bond yields and a stronger dollar will also draw money away from EMs.

John notes that this is decoupling – the debunked notion that EMs could prosper as the developed world fell into recession – in reverse.

- Now we have to believe that the US can do well while EMs suffer, something that is also far from clear.

John points out that one of the distinguishing features of EMs is their weak institutions.

- He worries that the US and UK might join them in this.

I can’t see it myself, but John often knows better than me.

Pension contributions

In the Economist, Buttonwood looked at a new paper which suggests that US workers are not contributing enough money to their DC pension schemes (known over there as 401[k] schemes).

- DC schemes average 9% in contributions (6% from employees and 3% from employers)

- DB schemes average 25% (6% from employees and 19% from employers)

The paper suggests that workers don’t contribute more to make up for the lower employer contributions to DC schemes because there have been high returns in the past.

The researchers assumed that target retirement income was 75% of salary, with 30% of this coming from other sources like Social Security.

- They also assumed that workers would buy an annuity on retirement (a bad idea) and that wage growth during the worker’s careers would average 2% pa real (after inflation).

Based on historical returns (7.5% pa from equities, 2.5% pa from bonds), workers only needed to save 8% of their salary throughout their careers to hit the 45% annuity target.

But future returns are likely to be lower (the researchers assumed 5% pa from equities and 1% pa from bonds – higher than I would have chosen).

- Thus a 60:40 equity to bond split returns 3.5% going forward, 2% pa lower than in the past.

- That means that workers would need to save 15% pa in order to hit their target.

Buttonwood agrees with me that the 3.5% return is optimistic, and suggests 2.5% pa instead.

- This means that workers would need to contribute 19% each year.

Even if they started with more equities and switched to bonds as they approached retirement, they would need to save 15% pa.

The other explanation for why workers don’t save more is, of course, a lack of spare cash.

- Flat incomes over the past 15 years mean that many Americans are resigned to working longer, rather than sacrificing their income today.

Pot of gold

Underneath all the noise about the Trump victory last week, it went largely unnoticed that another four states voted to legalise recreational cannabis use, bringing the total up to seven, plus the District of Columbia.

The Economist looked at the drug’s transition from illegal menace to consumer staple.

- There are 32M regular users already, and the new votes will attract more customers.

- Analysts are predicting that sales will triple by 2020.

Federal bans on the drug make business difficult:

- most banks won’t lend to cannabis firms

- companies can’t operate across state lines

- lots of normal expenses can’t be deducted from tax filings, squeezing profits

It still looks like a promising industry, but the big question is when the tobacco firms will enter.

- It’s also not clear at the moment to what extent smoking the flower will be replaced by other forms of consumption – vaping, or biscuits, sweets, oils and sauces.

From an investment point of view, it seems a bit early.

- If a fund or ETF was available, it might be worth a punt, but I don’t know of any. (( If you do, please let us know in the comments ))

Bonkers freedoms

In the FT Adviser, James Fernyhough reported on a survey of 1,000 soon to be pensioners by Retirement Advantage (RA) on their plans under the Pension Freedoms:

- almost a quarter planned to take more cash than the 25% tax-free lump sum

- this included almost a third of those with larger pots (more than £100K)

- more worryingly, the joint top reason for taking the cash was to “save for a rainy day”

This was described by RA as “bonkers”, and I have to agree – money is better left in a tax shelter if you have no plans for it, and don’t plan to move it to another tax shelter (an ISA).

Other reasons for withdrawals were:

- to generate an income (28%)

- pay off debts (17%)

- pay of a mortgage (12%)

These are much more sensible ideas.

Less good, but also featuring were:

- home improvements (17%)

- giving money to family (8%)

- holiday of a lifetime (15%)

- new car (11%)

We’ve a long way to go with financial education in the UK.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.