Rebalancing 3 – Value Averaging

Today’s post looks at a form of rebalancing we’ve previously overlooked – Value Averaging.

Rebalancing

We’ve looked at rebalancing twice before.

- The first time was a couple of years ago, as part of our Money Deck series.

- Then a few weeks ago, I caught up with the re-balancing articles I’d read in the intervening two years.

I won’t recap what I said in those two posts, but instead today we’ll look at a form of rebalancing that I’ve ignored so far – Value Averaging.

Value Averaging

Value averaging is a bit like dollar cost averaging.

- But instead of investing the same dollar (pound) amount each month or year, you invest more when markets are down.

This tell us two things:

- It’s a form of cash flow rebalancing that requires us to be adding money to the portfolio.

- We need to look under the hood, because dollar cost averaging (DCA) doesn’t work.

- On average, spreading your payments evenly leads to a lower portfolio value.

- That’s because stock markets trend upwards, which means that time in the markets is important.

- You are usually better off investing lump sums as soon as you have them.

At first glance, value averaging seems every bit as appealing as DCA, yet for some reason it’s much less well known.

Value averaging can also be viewed as a market timing strategy, since unlike DCA, it includes a sell rule.

- It includes both halves of the “buy low, sell high” adage.

Edelson

Value Averaging was first described by Michael Edelson, a former Harvard professor, in 1988.

- In 1991 he turned that article into his book Value Averaging.

Edleson defines VA as:

Make the value not the market price of your stock go up by a fixed amount each month.

Which isn’t particularly clear to me.

Edelson says that value averaging (VA) would have beaten DCA in 57 of the 66 years from 1926 to 1991.

- It returned 13.8% pa, compared with 12.6% pa for DCA.

- He didn’t say how lump sum investing would have fared.

There’s a second edition of the book from 2006 which confirms that success of the strategy between 1991 and 2005.

VA sets a target growth rate for an investment.

- When returns are higher than expected, you “sell” back to the expected level.

- In practice, since VA is generally used during accumulation, you actually add less cash the following month.

- Extreme performance (of greater than the next monthly contribution) might mean that you should sell part of your holding.

- But you might prefer to suspend payments until the valuation reverted to the target, thus avoiding trading fees.

- When returns are lower than expected, you top up (add more cash than expected) to bring you back to the target level.

Edleson says that two to four revaluations per year would be fine, though he often refers to monthly increases in value.

VA reminds me of the long-run mean-reversion rules used by some trend-following traders.

- The further ahead of the long-run trend that a market gets, the lower exposure such traders have to it.

Criticism

Simon Hayley of Cass Business School (( One of my alma maters )) pointed out in 2012 that the reported outperformance ignores the drag from the parallel cash account that is needed to implement the hard version of VA.

Hayley says:

VA is a popular investment strategy which is recommended to investors

because it achieves a higher IRR than alternative strategies.However, this is entirely due to a hindsight bias which raises IRRs for strategies which link the scale of additional investment to the returns achieved to date.

VA does not boost profits (terminal wealth), but can generate attractive behavioural finance effects.

Investors who value these are likely to prefer the simpler DCA, since VA imposes additional direct and indirect costs on investors as a result of its unpredictable cash flows.

Whether VA beats DCA in practice would depend on two things (each unknowable without hindsight):

- How big would the cash pot need to be (in this particular instance)?

- How strongly would the investments outperform the cash (to potentially overcome the cash drag)?

There is also the implementation issue of how to choose the future growth rates.

Historic rates are the obvious starting point, but:

- High growth in eg. stocks is usually followed by low growth.

- There are lots of reasons to believe that future growth will be lower than historic growth (low interest rates, high valuations etc).

A monthly growth rate (for stocks) higher than 0.7% but lower than 1% seems to be optimal for VA.

- That’s 8% to 12% pa, which seems very high today.

Marshall (2006) – the latest in a series of papers on the topic by this author – compared VA, DCA and random investment.

- He found that VA outperformed under most conditions, but that there was not enough data to confirm this statistically at a high confidence level.

A previous paper demonstrated that DCA was not superior to random investment.

- Once again, up-front lump sums seem to have been ignored.

Chen and Estes compared VA, DCA and “proportional rebalancing”.

- Here, proportional rebalancing means moving the portfolio back to the original allocation proportions.

VA came out best of the three methods.

Explanation

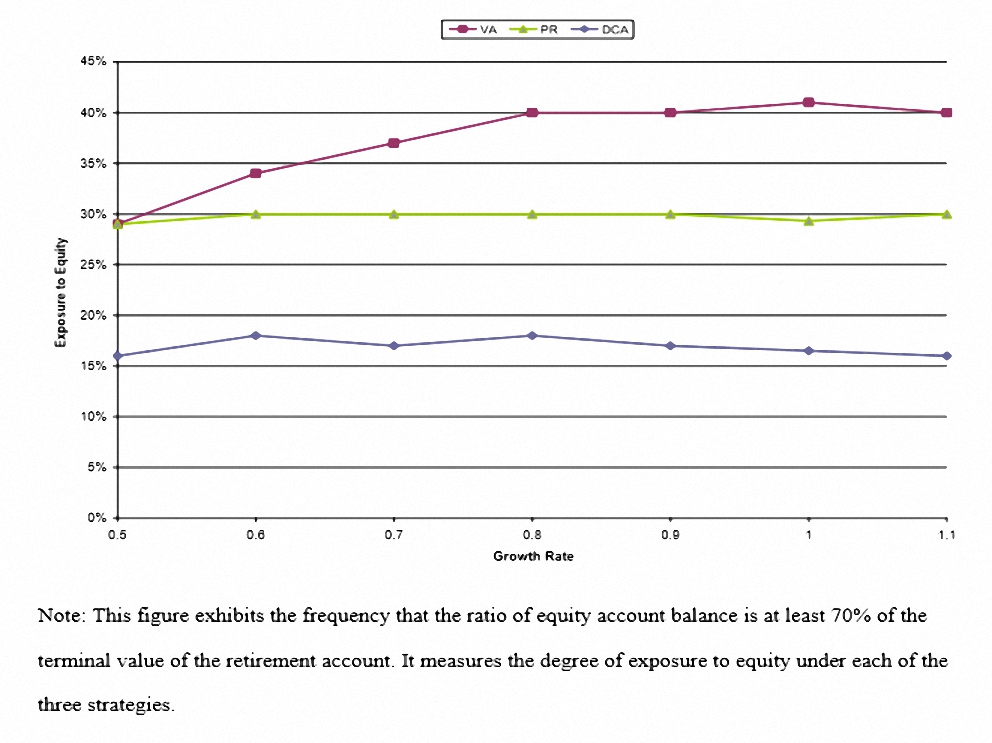

If we think about the mechanisms underlying VA, its outperformance is less surprising.

- It aims to keep assets on track with a predetermined growth rate.

Since risk assets (stocks) will have higher growth rate than stability assets (bonds) this means that over time, the proportion of risk assets in the portfolio must increase.

- So the outperformance comes from taking on more risk.

The chart below from Chen-Estes shows this in an oblique fashion:

Conclusions

VA is an interesting twist on DCA, and seems preferable to it.

- But the advantages disappear when the cah drag is taken into account.

Lump sum early investment is probably even better (in accumulation), and could be combined with VA.

In decumulation, delaying sales as long as possible should work best, but again, VA could be layered on this.

The problem with VA is that it doesn’t provide a stable asset allocation.

- The proportion of risk assets will increase, and you are rewarded (within the main portfolio, at least) for taking on extra risk.

Which is not the point of rebalancing at all.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London.

He has been managing his own money for 40 years, with some success.