RPC Stacked Portfolios

Today’s post looks at the portfolios tracked on the Risk Parity Chronicles website, and in particular, their use of leverage.

RPC

We’ve come across Risk Parity Chronicles (RPC) before – it’s one of the best blogs out there talking about Risk Parity (RP) and leverage for DIY investors.

- Like me, author Justin was a fan of the Risk Parity Radio podcasts from Frank Vasquez.

- Frank doesn’t have a blog, so Justin put one together to cover the issues from the podcast.

- Also like me, Justin took some time off from blogging but now he’s back (in his case on Substack).

RPC portfolios

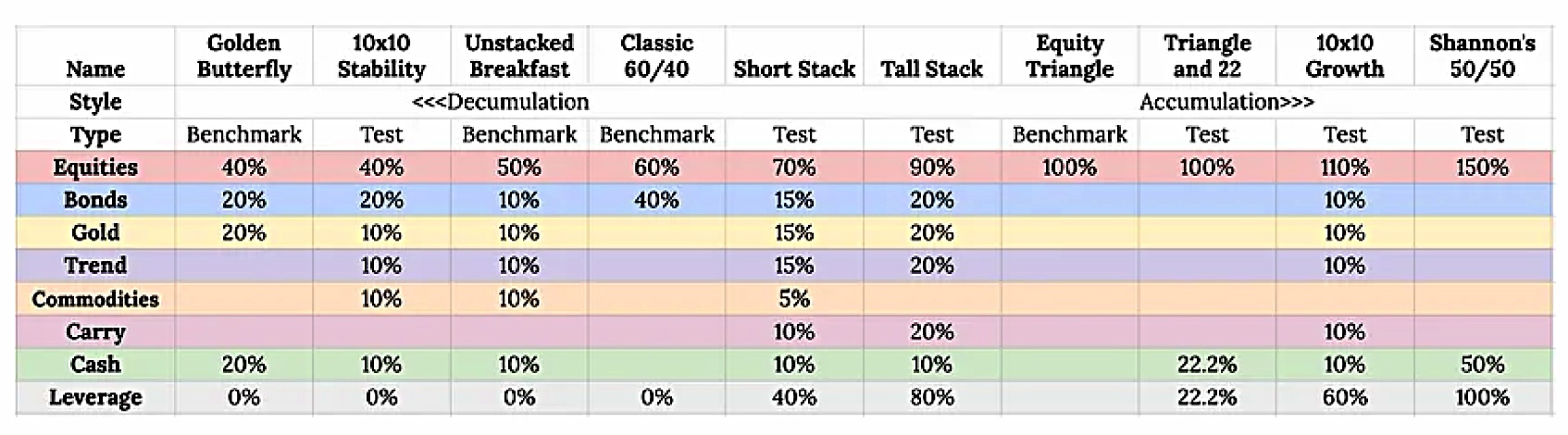

Justin used to track 14 portfolios, but back in August 2025, he cut this down to ten.

- Five of these are aimed at accumulation, and five at decumulation.

- Justin splits these on the basis of equity allocation.

I’m in a bit of a grey area here – I quit work 14 years ago, but my partner still takes on projects regularly, so we’re not quite in decumulation (though we are edging closer to it each year).

- I don’t expect my equity allocation to drop in decumulation – my nominal targets are 70% equities (including equity alts like property), 20% bonds (and bond alts) and 10% true alts.

- At the moment, I’m a bit heavy on stocks and a bit light on true alts.

Four of the RPC ten portfolios are designed to be benchmarks, and six are “experimental”.

- Six are effectively the same two base portfolios with different amounts of leverage, and it’s these that I’m most interested in today.

Justin uses a pancake metaphor to describe one set of portfolios (he says it’s a reference to the Return Stacked series of ETFs that he uses):

- The Unstacked Breakfast is 50% stocks and 50% diversifiers

- The Short Stack is 70/70 (using 40% leverage)

- And the Tall Stack is 90/90 (80% leverage – which involves using some scary 3x leveraged funds)

There’s another set of three separated by leverage:

- The Equity Triangle is all stocks (using three funds – US large cap growth, US small cap value and International)

- Triangle +22 adds 22% leverage (again using 3x funds) to give 100% stocks plus 22% cash/tail-risk protection

- Justin’s Shannon portfolio is 150% stocks and 50% short-term bonds (which is Shannon’s original 50/50 with 100% leverage added to the stocks). This uses the 3x stock fund plus the tail-risk fund, so Justin calls it Shannon 50/50.

The other four portfolios are:

- Classic 60/40 (benchmark)

- Golden Butterfly (40% stocks, 20% each of bonds, cash and gold)

- 10×10 Stability (since renamed the Tortoise) – 10 funds with 40% stocks (including factor tilts), 20% bonds, 10% cash and 30% diversifiers

- And 10×10 Growth (now called the Hare), which has 100% stocks (including factors) and 50% diversifiers (including Bitcoin)

Here are the asset allocations for all ten:

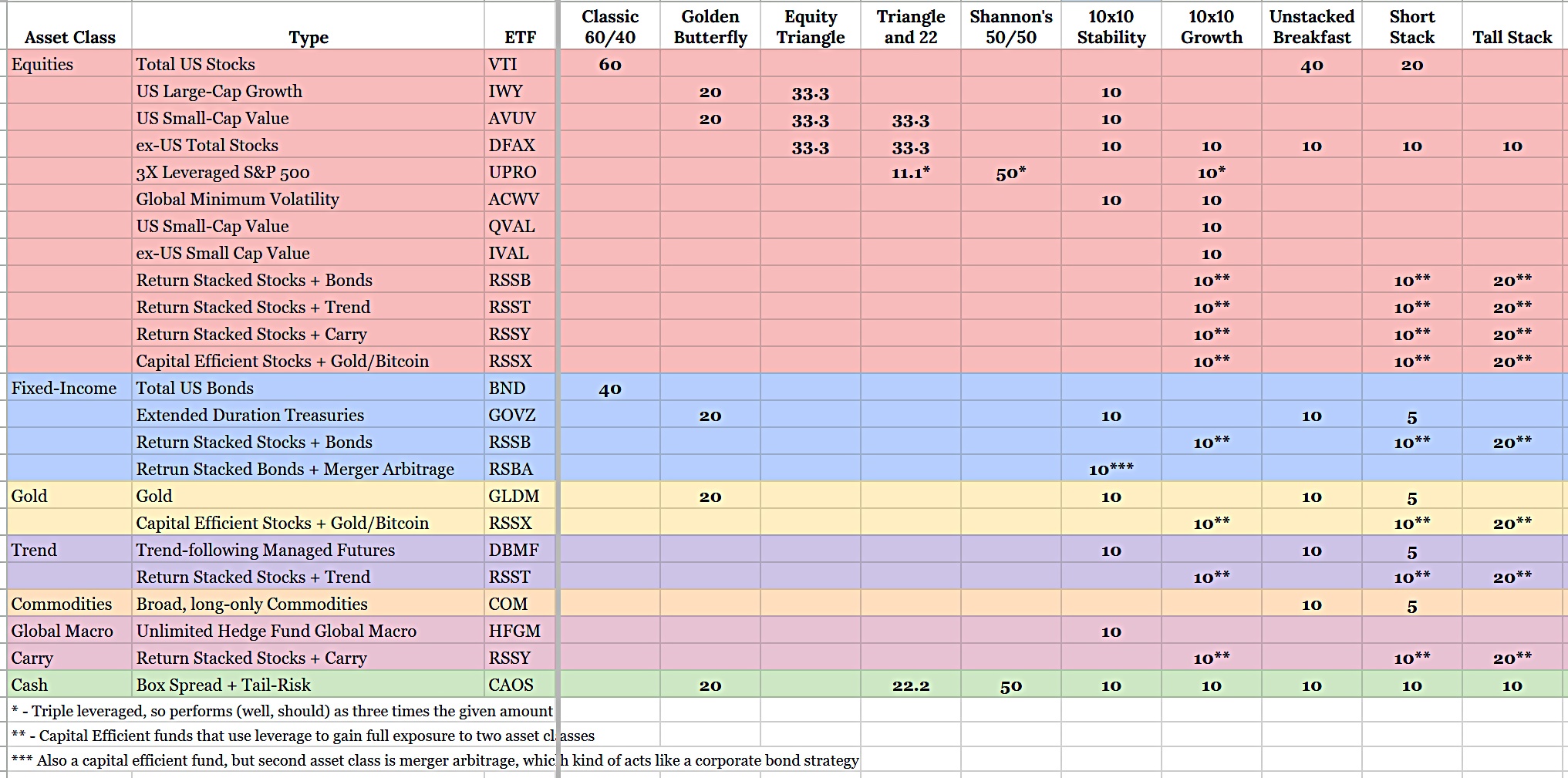

And here are the (US) ETFs that Justin uses:

You’ll notice that he is blessed with several options not available to UK investors.

RPC Tracking

Justin tracks the portfolios quarterly.

- He treats them as decumulation portfolios, withdrawing 1% each quarter

- The portfolios started at $1M, so 1% is $10K, though this is inflation-adjusted

- He takes dividends first and then sells the two funds most above their target allocation

- He also has a 20% rebalancing threshold to correct major drift from the target.

- Where dividends exceed the required distributions, the lagging ETFs are topped up.

RPC Results

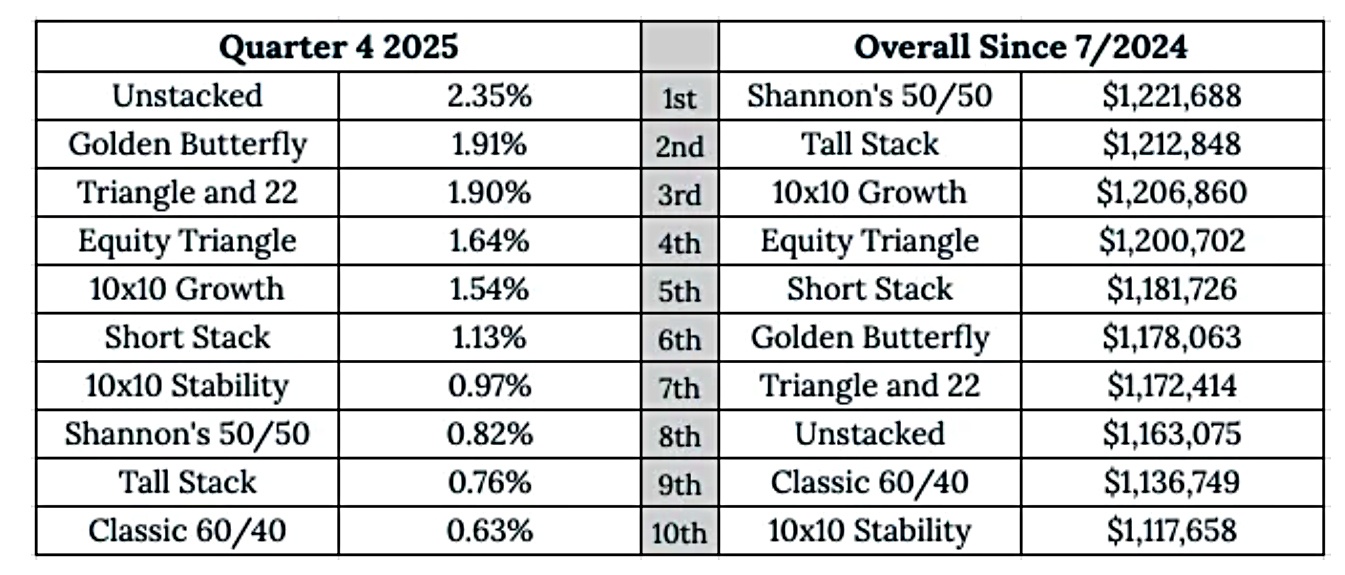

At the time of writing, the latest results published on ROC are for 4Q2025.

- That gives 18 months of runway for the ten portfolios.

- Payouts to date are around 6% of the portfolios’ starting value.

At the moment, the levered portfolios (Shannon, Tall Stack and Growth/Hare) are out in front.

- The stable benchmarks (60/40 and Stability/Tortoise) are to the rear.

But it’s early days, and the spread across the portfolios is only 10%.

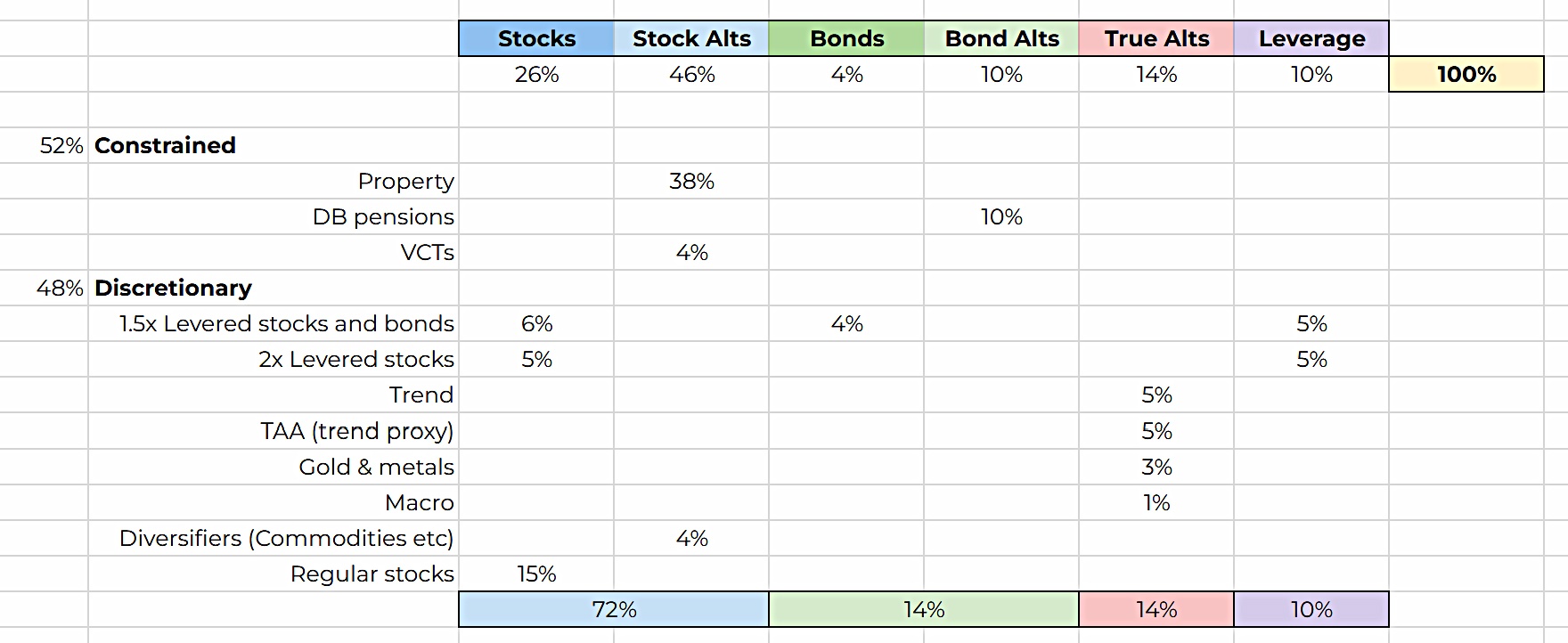

My Target Allocation

The main point of this review is to make me reflect on my own target allocation.

I have a few constraints:

- 38% of my assets are in property

- 10% are in DB pensions

- 4% are in VCTs (tax sheltered small, largely unlisted equities)

That leaves me with 48% to allocate as best I can.

- With the launch of the DBMG trend/managed futures ETF, I can access a trend allocation within my tax shelters (SIPPs to be specific).

- I have a self-imposed 5% cap on a single ETF, so I will supplement this with another 5% of TAA.

- The remainder of my True Alts allocation is made up of Gold/metals (3%) and Macro (1%)

- There are two 1.5x levered stock/bond ETFs (one with a US bias, the other using global stocks), so I can allocate 10% to these, giving me 5% leverage.

- My diversifier allocation (mostly commodities) is around 4%, which leaves just 15% to allocate to plain old unlevered (but diversified) stocks.

- This includes allocations to themes and factors (some of which are managed as TAA and will appear in that allocation instead).

Here’s how that all looks:

So my target allocation for 2026 is 72% stocks, 14% bonds, 14% true alts (of which 10% is trend/TAA).

- Thanks to the trend ETF, that’s a record high for the true alts allocation.

Let’s see how close I can get.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.