Fifteen things that could happen in 2015

We end the year with a look forward to what 2015 might have in store.

Contents

US divergence

The Economist has drawn parallels with 1998, when the US last forged ahead on the back of a digital revolution. In contrast, Japan was in deflation and Germany in trouble. The dollar was strong and emerging market currencies weak.

The US boom ended two years later and a year after that the US was in recession. It’s far from all good news this time either: falling oil prices could bankrupt some US shale oil producers and the strong dollar will hurt exports.

Elsewhere, Britain will be dragged down by the Eurozone and emerging markets will be hit by the oil price crash and the strong dollar: Russia is already in crisis and Nigeria, Ghana and Brazil look vulnerable. Fear of defaults will only exacerbate the rush to the dollar.

But stock markets are not as frothy in the late 1990s, and this time the digital giants making reckless investments are real firms with profits and balance sheets, rather than mere ideas for a company.

The long recovery from the 2008 crisis means that the global financial system is in better shape to cope with a new shock, but the measures already taken to restore stability mean that there is little further room for manoeuvre (in 1999 the Federal Reserve rate was 5%).

China slows

On the back of a cut in interest rates, the Chinese stock market has boomed late in 2014 even as economic growth has slowed. This is yet more evidence of the generally poor correlation between the two. Whether the Chinese financial system can cope with weakening growth remains to be seen. The market has become choppy and there is some evidence of illegal margin trading.

There is also the impact on imports (and hence global exports) to consider. Germany (machinery) and Australia (raw materials) are particularly exposed. And finally, there is the risk that China will export deflation to the rest of the world.

Japanese QE continues

Abenomics has a renewed mandate, and QE can be expected to continue. The low oil price will reduce the import bill, but will impede progress towards the government’s inflation target. The stock market is relatively cheap and corporate profits are rising, but the balance sheet of the Japanese central bank is growing alarmingly.

US rate rise

The performance of the US economy in 4Q14 means that an interest rate rise is possible in 2015, though inflation remains low and a rise may not be necessary. A hike might trigger panic in the markets, which appear to have been propped up for years by easy monetary policy. If there are market problems, will the authorities respond once more?

UK rate rise

In March, UK rates will have been at a 300-year low for six years straight, but a UK rate rise still seems a long way away, and may not happen in 2015. Inflation is low, wage growth is non-existent, and our major trading partner (the Eurozone) has serious problems. The recent excellent rate of UK GDP growth is unlikely to be maintained in 2015 and deflation is a possibility.

Bond market fails to crash again

All of the above implies that bonds and gilts will have another better than expected year, but we are clearly in the end game, and I will not be a buyer in these circumstances.

Oil price remains low

On paper the oil price fall – though deflationary – is good news for consumers, and would normally boost global GDP. But oil exporters (Nigeria, Russia, Venuzuela) will suffer, and this in turn will bring political instability. Emerging market currencies have already begun to tumble.

There is also the possibility of a demand shock to match the current over-supply: China is slowing, and the Baby Boomers are starting to retire. In addition, the impact from the bankruptcy of leveraged oil-producing companies – energy bonds make up 13% of the US junk-bond market – is difficult to predict, though it is probably not the full Sub-Prime 2.0 that some fear.

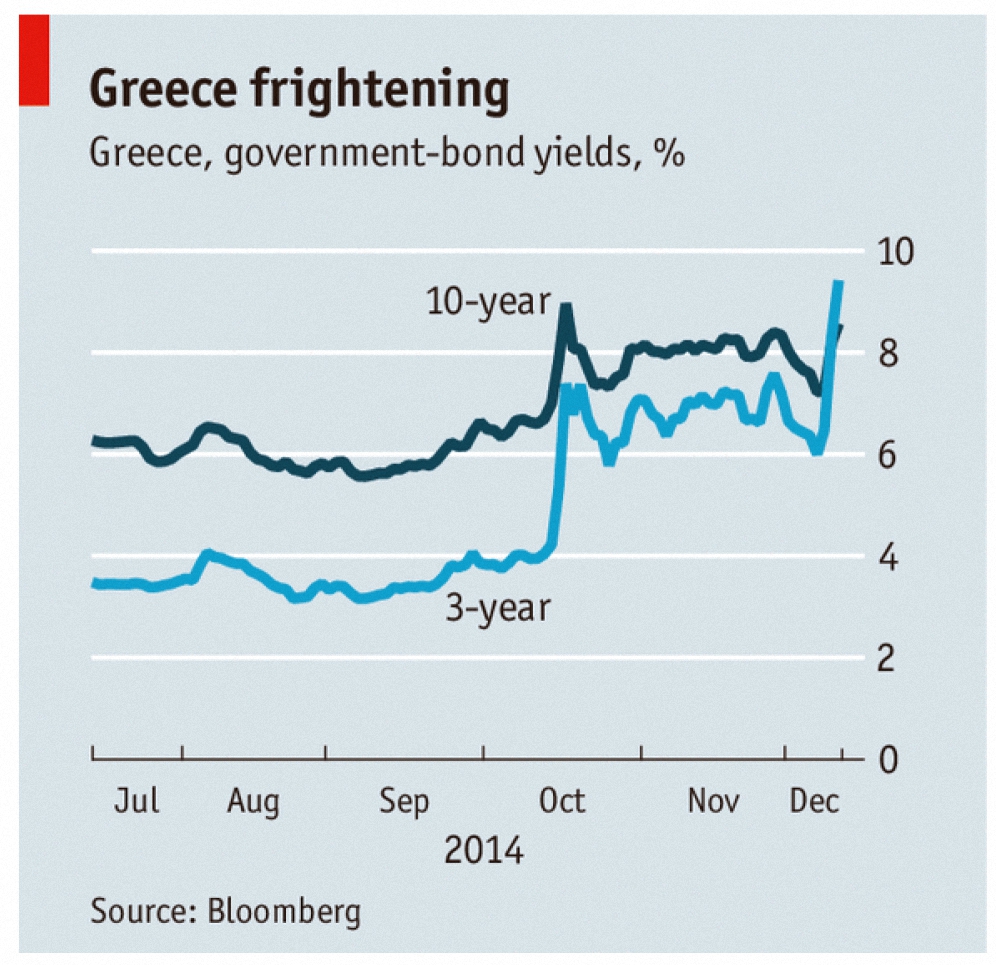

Grexit?

The failure of the Greek parliament to back the government’s presidential candidate has led to a snap election in January 2015. Syriza are top of the polls and have rejected the current austerity bailout, threatening instead a default on Greek debt. If the Eurozone rejects a deal, the Greek exit from the Euro would set a precedent for Portugal and Italy, with predictable impact on their bonds.

Agreeing a softer deal with Greece would bring those countries in turn to the negotiating table. The Greek 3-yr bond yield is now higher than the 10-yr, implying that investors are worried about a haircut.

Taking a more optimistic view for a moment, perhaps the Greek crisis will prompt real QE in Europe, which would be positive for markets (though negative for the euro). Given recent German parochialism and intransigence, I don’t expect this to be the case.

Political problems in Europe

The 1990s crisis came at the end of a long boom with increasing real wages. Workers in 2014 have already suffered in the quest to fix the 2008 crisis and are unhappy with their governments.

They see little difference between the mainstream parties and are turning to the extremes (Syriza in Greece, Marine Le Pen in France, UKIP in Britain). The risk of an exit from the EU in the next few years continues to rise.

Deflation

Inflation is uncomfortably low across most of the developed world, and parts of the Eurozone are close to deflation already. Any of the issues detailed above could further reduce growth and produce deflation in Europe and possibly the UK. That is whole new set of economic and investment problems, and something that I will return to in a later post.

UK pension reforms

We already know what changes will come into force in April, but how people will react to the new opportunities remains to be seen. No doubt some savers will withdraw large amounts from their SIPPs, ignoring the cost in extra tax; many more will not. Perhaps some platforms and pension firms will be unable to cope with the initial rush of redemptions.

Crystallisation of certain more exotic investments for early withdrawal (“the tide going out”) will reveal their inadequacies (“who is wearing a costume”). Public sector and remaining private-sector final salary scheme holders will for the first time in 20 years be jealous of their defined contribution friends and colleagues who can access their money immediately.

UK election

This is definitely going to happen, but the outcome is as unclear as any UK poll for decades. We have a four-way (UKIP) and arguably a six-way (Greens and SNP) fight, with fine margins as to who will be the largest party and whether they will be able to form a stable coalition. UKIP will hurt the Tories (and perhaps Labour) in England, and the SNP look likely to overrun Labour in Scotland. The Liberals could be obliterated by a combination of the Greens and the major parties.

UK market instability in the first half of 2015 is likely (though low interest rates should lead to the search for yield underpinning equities) and a second election is more than possible. The ugliest prospect is that of a Labour minority in England being propped up by a party that has just finished campaigning to leave the UK.

This reinforces my view that we in England would have been better served by a Yes vote in the referendum. Scottish political opinion is completely at odds with that in the South of England, and they cost us money every day. The issue is likely to drag on for decades. Let’s hope that the increasingly similar relationship with the EU is resolved more quickly.

UK tax hikes

With any result other than a Conservative-led government, we must expect tax rises, since no-one else is prepared to reduce public spending. Labour and the Liberals are committed to the “mansion” tax (or terraced house tax as it is here in London) and Labour has also pledged to remove 45% pension tax relief.

Some feel that 40% relief will be too tempting a target for the lifetime of a parliament. The annual allowance might also be trimmed by Labour from the present £40K. VCTs might then become more attractive to many, and I will look at the sector in a future post.

On personal tax, the Tories plan to raise the higher rate threshold to £50K (from £42K) in the next five years, while Labour plans to increase the “additional” rate (paid over £150K) from 45% to 50%. The Conservatives have also talked about raising the inheritance tax threshold to £1M (from £325K).

UK house prices stall

The increase in high-end stamp duty has already impacted the corresponding sector of the housing market (to be found predominantly in London). The fall in transactions can be expected to ripple out from the capital next year, exacerbated in the first half of the year by electoral uncertainty. Any interest rate rise would only compound this effect.

There is a possibility that the new pension freedoms will stimulate the market by tempting some to become buy-to-let landlords, but these are as popular in the UK as bankers at present, and the political mood means that some kind of bureaucracy or regulation in this area can’t be ruled out.

There is also tougher mortgage regulation (outlawing high income multiples) to consider. Increased loan terms of 30 years may kick the can along the road for while, but they brings their own problems. There are already reports of people over 40 being refused loans that they are seen as too old to repay. With the age of first time buyers rapidly approaching this number, the window of opportunity to get on the housing ladder appears to be shrinking.

P2P lending goes mainstream

I opened an account with Zopa some 7 or 8 years ago, but stopped peer-to-peer lending when the credit crunch led me to believe we were in for a wave of defaults. This hasn’t happened, and the only thing that has stopped me re-entering the market is the lack of a tax shelter (a more important factor since rates fell).

This may be about to change, with the likelihood that a Tory government at least will introduce some form of P2P ISA. A SIPP offering would be welcome, too.

The logic of the product (cheaper loans for you, a higher interest rate for me) is irresistible, and 2015 could be the year when the public catches on. The risk of defaults remains, but as a small part of a diversified portfolio it has its attractions. This is another sector that I will return to in a future post.

* * *

And so we have somehow managed to end on a fairly upbeat note.

Happy new year to you all, and see you in 2015.

Sources

- Past and future tense – Economist 20th Dec 2014

- Frozen or Buzz? – Economist 13th Dec 2014

- Hargreaves Lansdown investment times, Dec 2014

- Two big global risks for 2015, Merryn Somerset Webb, Money Week, 19th Dec 2014

- Greg Kingston’s 10 expectations for 2015, FT Adviser, 22nd Dec 2014

- Five issues that will make – or break – the world economy in 2015, Observer, 28th Dec 2014

- A year of change for your money, FT, 19th Dec 2015

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.