Idle Investor 1 – Lessons, Axioms, DIY and Assets

Today’s post is our first visit to a new book that I read over the Xmas break – The Idle Investor by Edmund Shing.

Contents

Edmund Shing

Edmund Shing is someone I follow on Twitter (@TheIdleInvestor – he used to have a website at www.idleinvestor.com, and then at edmundshing.co.uk, but neither seem to work anymore)

- I’d been meaning to read his book since it was published in 2015.

I noticed in the run up to Xmas that second-hand copies were now cheap enough to go on my Xmas Wish List at Amazon.

- Sure enough, it turned up over the break and I read the whole thing in one afternoon (it’s not a long tome).

Ed is a Global Equity portfolio manager at BCS Asset Management, and a consultant for a French unit trust that invests in smart beta ETFs using the principles in Ed’s book.

- He previously worked at Barclays, BNP Paribas Julius Baer, Schroders and Goldman Sachs over 20 years in the markets in Paris and London.

- He also holds a PhD in AI from Birmingham University.

The Idle Investor

Ed’s boast in his subtitle is that you only need “5 Minutes a Week” to “Beat the Professionals”.

- That’s some claim, particularly with respect to the amount of time required, so I expected this to be the laziest choice out of several possible approaches.

Indeed, the preface says that:

This book contains three simple investing systems for long-term savings. Each of these systems require only a limited amount of your time per month and all use low-cost index funds.

Who is the book for?

Ed’s book is aimed at those who are frustrated by low interest rates on savings accounts, and would like to do better over the long-term (which Ed defines as at least three years).

- The reader is likely to be cash-rich, but time-poor, and worried by the two stock market crashes since 2000.

Ed says that:

There may be short-term periods of underperformance but the systems outperform in the long-term as long as you stick to them.

This will therefore require a good amount of self-discipline and patience, but should over time handsomely reward the disciplined, patient investor.

Ed also assumes that those wanting to apply the systems will have at least £10K to begin with.

What knowledge is assumed?

Ed assumes that readers have some experience of:

Unit trusts, ETFs, investment trusts, pension funds, life assurance products or even directly in individual shares.

He’s not aiming at the complete novice, and he lists some better books for beginners in an Appendix.

Eight lessons

The first chapter in the book is largely autobiographical, but in-between the sections of personal history, Ed lists a few lessons that he has picked up along a 20-year career:

1 – Don’t waste your time trying to forecast future levels of share market indices. There are so many macro-economic, geopolitical and share-specific factors at work that you have little chance of being consistently right.

2 – Long-term investment trends can last a surprisingly long time. They can be very profitable for those who (a) manage to identify the trend early on, and (b) have the confidence and resolve to stick with that trend. “

3 – The majority of active fund managers do not outperform market averages over time, and charge their clients handsomely for this failure

4 – Obsessive screen-watching is deleterious to your long-term financial and mental health, as you are tempted to panic into and out of investments. Full-time trading requires a remarkably cool temperament (as devoid of emotion as possible), and the development of – and adherence to – an investment system.

5 – Your best chance of investment success lies in keeping costs to a minimum (resisting the urge to trade too often), and in following a clearly-defined methodology or system. Risk management (e.g. when to cut your losses) is an under-appreciated but vital element.

6 – Asset allocation (diversification) is a very important way to reduce your risk over time.

7 – Momentum and trend-following have been surprisingly successful ways to invest in various markets over the long-term. However, they are subject to wide swings, and a robust method for controlling risk is also needed.

8 – Smart beta provides the retail investor with access to these investment strategies at low cost, presenting a challenge to actively-managed funds.

The systems

Ed’s resulting systems have four key features:

- they spread investment risk across asset classes

- they use momentum to follow market trends,

- they use low-cost, smart beta ETFs to outperform benchmark indices, and

- they are simple to operate, taking little time (a couple of hours per month).

How Is It Possible To Be An Idle Investor?

The question Ed is really asking in this section is how can DIY investors – private individuals – beat the pros?

- I’ve covered this before (in Become a DIY Investor) but Ed points to a French phrase that roughly means “the cobbler’s children have no shoes”. (( An alternative that I’ve come across a lot during the property boom of the past two decades in southern England is “Builder’s houses are never finished” ))

In particular, Ed says that market professionals often take on too much risk and sometimes have no plan at all for their own finances.

- All you have to do to beat the pros is follow a system, and stick to it.

Seven axioms

Alongside the eight lessons from the previous chapter come seven axioms:

- Keep investing simple

- Investing is about getting from your start point (existing and future savings) to a goal (retirement, school fees etc.)

- A simpler roadmap and rulebook is easier to follow.

- Ed is particularly unhappy with structured products built from derivatives, which he feels benefit the issue bank rather than the end client.

- I certainly agree that structured products aren’t for everyone, but derivatives (spread bets, options) and particularly listed, tradable structured products, can be very useful to sophisticated investors by allowing them to tailor their risk profile.

- Don’t invest in anything that you don’t understand.

- What Ed really means here is “if it sounds too good to be true, then it probably is“.

- He mentions the steady returns from Madoff’s ponzi scheme as an example.

- And he points out that Buffet ignored the dot com boom and bust because he didn’t understand it.

- Ed himself ignores Biotech.

- Don’t follow the markets on a daily basis.

- This is Ed’s version of Cut Out The Noise.

- This rule is much easier to follow – though less so than in the past – for those with a full-time job, rather than those who are full-time investors.

- In practice, what Ed means is that you shouldn’t buy a share on a piece of good news, only to sell it on the next piece of bad news.

- He recommends “the Economist and the weekend edition of the Financial Times” – so do I, but with less enthusiasm than I did a few years ago.

- “The vast majority of so-called business news is simply chatter that does not have any significant bearing on the long- term direction of shares or markets.”

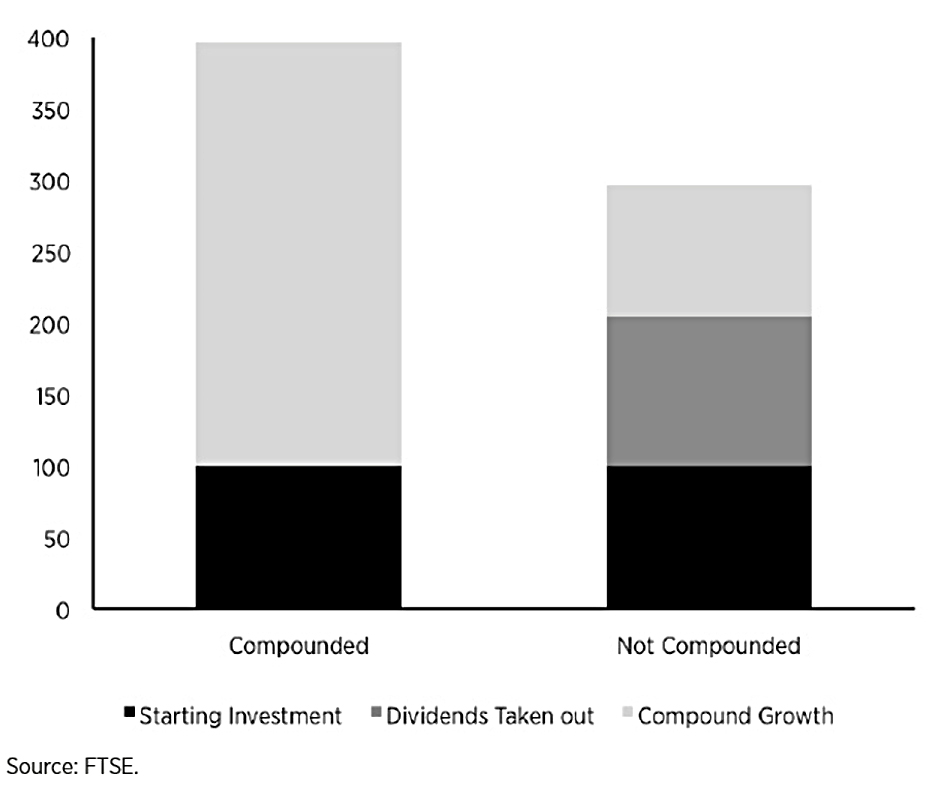

- Make use of compound interest.

- This is another one that we’ve covered before.

- Over the long-term, even 0.5% pa can be significant (see keep costs low – next bullet).

- Keep costs low.

- Or as we put it, Costs Matter.

- Like me, Ed likes to use ETFs, which have no entry or exit charges, low annual fees, narrow spreads and no stamp duty on purchases.

- You do need to pay commissions on your trades, so a discount broker is recommended – iWeb is the cheapest I have found that is UK regulated.

- Ed does consider active management (Investment Trusts, for example) in certain sectors (small-caps, Japan, high-yield bonds).

- Keep the faith when markets tumble.

- Or as Ed (and Corporal Jones) puts it: Don’t Panic.

- This doesn’t mean that it’s never right to retreat from the market, but the largest drops are rare.

- A 10% correction shouldn’t scare you away.

- It’s one thing to sell out when you feel the market will crash (or spot it starting to happen), but quite another to buy back in at the bottom, when fear is the greatest.

- This is one of the ways in which shares are not like other goods – when they are on sale they are often less attractive.

- See Behavioural Investing for more on this.

- Ed notes that the third of his three strategies incorporates some market timing.

- Keep a cash buffer.

- This might seem odd advice in a time of low interest rates.

- There are three reasons:

- for unexpected spending in life, or to cover a break in employment (an emergency fund)

- to take advantage of investment opportunities (crashes and corrections)

- (particularly in decumulation or retirement) to avoid having to sell investments to create income (cash) when markets are low.

Note that in this chart, the benefits come from compounding (rather than spending) your income.

- The specific source of that income (dividends) is not significant.

DIY investing

Chapter Three of Ed’s book explains why DIY investing is the best.

- He begins with the difficulty of choosing an active fund.

They can be classified by:

- style (income, growth, balanced)

- asset type (shares, property, government bonds, corporate bonds)

- geography (UK, Europe, US, Japan, APAC, China, emerging markets)

You also need to decide how to invest (ISA, SIPP, monthly or lump sum), and which of the 200 management companies in the UK you would like to invest with.

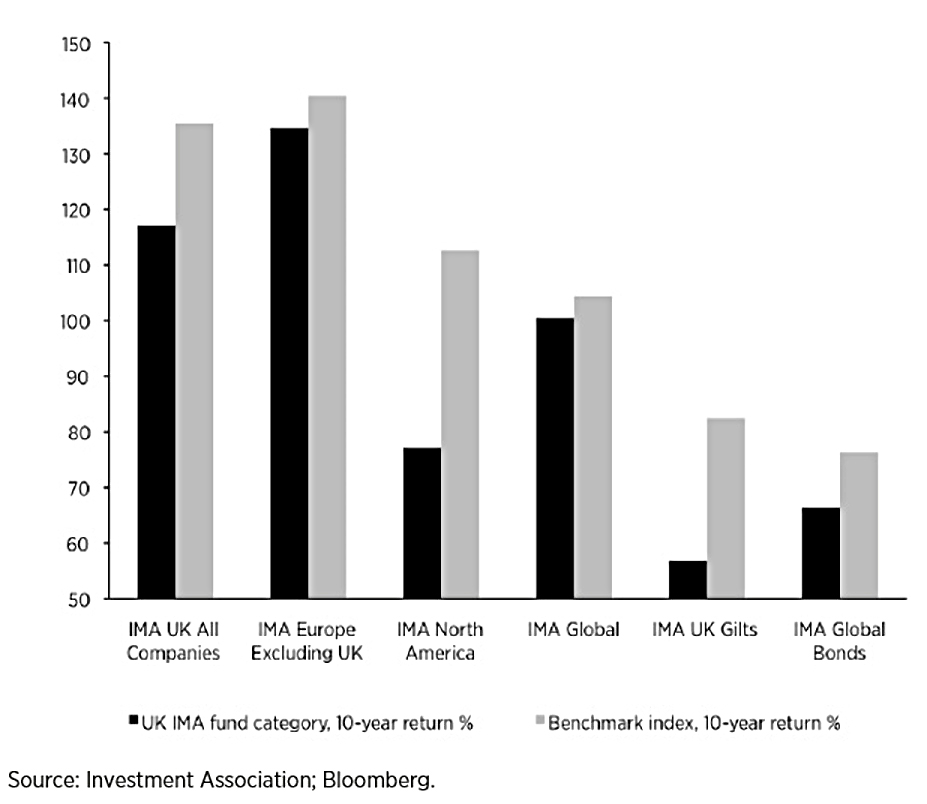

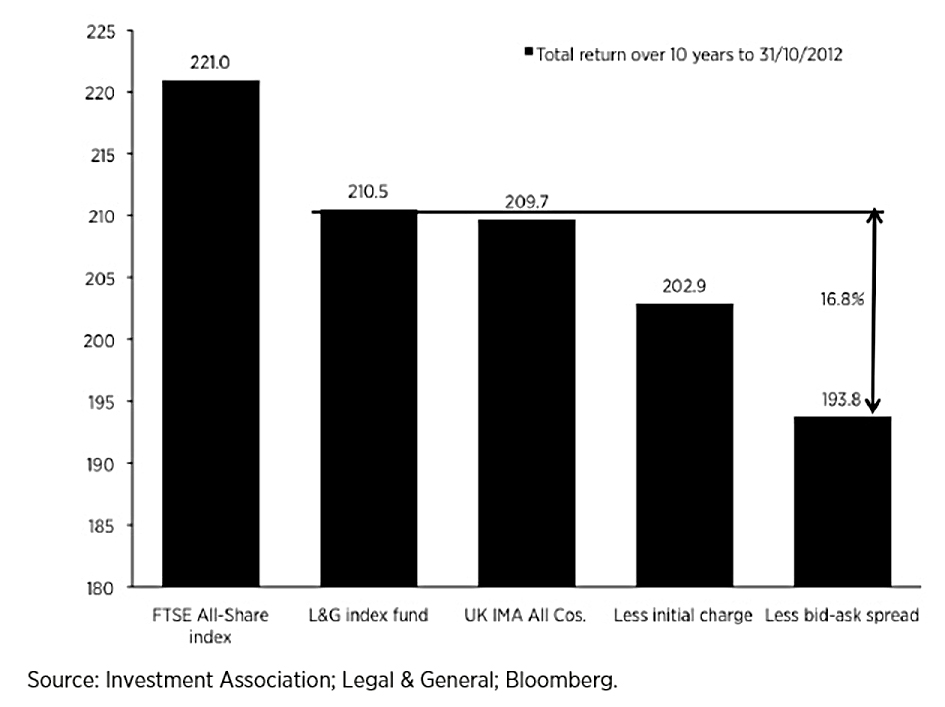

And of course, active managers charge more and (on average) they don’t beat their benchmarks.

- There may also be initial charges, bid-offer spreads and trading costs (churn).

A few managers do beat their benchmarks, but according to academic research, it takes 17 to 25 years of outperformance before you can conclude that investment skill – rather than luck – is responsible. (( Personally, I will accept a shorter track record of massive outperformance, as shown by some of the multi-asset and non-stock traders in the Jack Schwager series of inverview books, Market Wizards ))

I think Ed is mostly trying to say that handing over responsibility to an active manager is not as simple as it sounds.

He makes a good argument for passive investing over active (in general – there are sectors and assets where active makes more sense) but less so for DIY over Do It For Me.

- Ed does recommend passive ETFs (as well as smart beta ETFs) but he uses them in (mechanical) active systems.

Managed passive solutions (usually known as Robo Advisors, but also including auto-rebalanced funds like those from Vanguard) were certainly available when Ed wrote his book, but he doesn’t address them.

- Although it must also be said that Robo solutions are not usually as cheap as they might be expected to be.

Asset classes

Chapter 4 of Ed’s book is about asset classes, or as he calls them, “Investment Building Blocks”.

Ed focuses on four:

- stocks

- bonds

- cash

- property

While I agree these are the central four, I would also consider commodities, FX, private equity, multi-asset funds, hedge funds and infrastructure.

Ed doesn’t actually use property in his three strategies, and explains why:

- mostly it’s because UK investors typically have some (too much?) exposure to property already

- I know I do

- this is a good reason

- partly it’s because property is illiquid and expensive to trade

- this is true of houses, but not of the myriad property ETFs

- this is not a great reason

- Ed also states that property exposure doesn’t offer anything that shares, bonds and cash don’t

- this is theoretically possible, but non-perfect correlations imply lower price volatility, which is their attraction for private investors

- this is a bad reason for me

Compound Annual Growth Rate (CAGR)

In the next section, Ed explains that he uses compound annual growth rate (CAGR) to compare returns across investments and asset classes.

- This gets around the problem of differing time frames.

Risk-adjusted returns

The next section introduces the concept of risk, which Ed defines as:

The probability of getting less than you expect.

- Including perhaps less than you started with.

I prefer this definition to the usual “price volatility” definition, but I also like the quote from Elroy Dimson of LBS:

Risk means more things can happen than will happen.

Ed also talks about finding out your own risk tolerance or capacity for loss.

- You can take our risk tolerance questionnaire here.

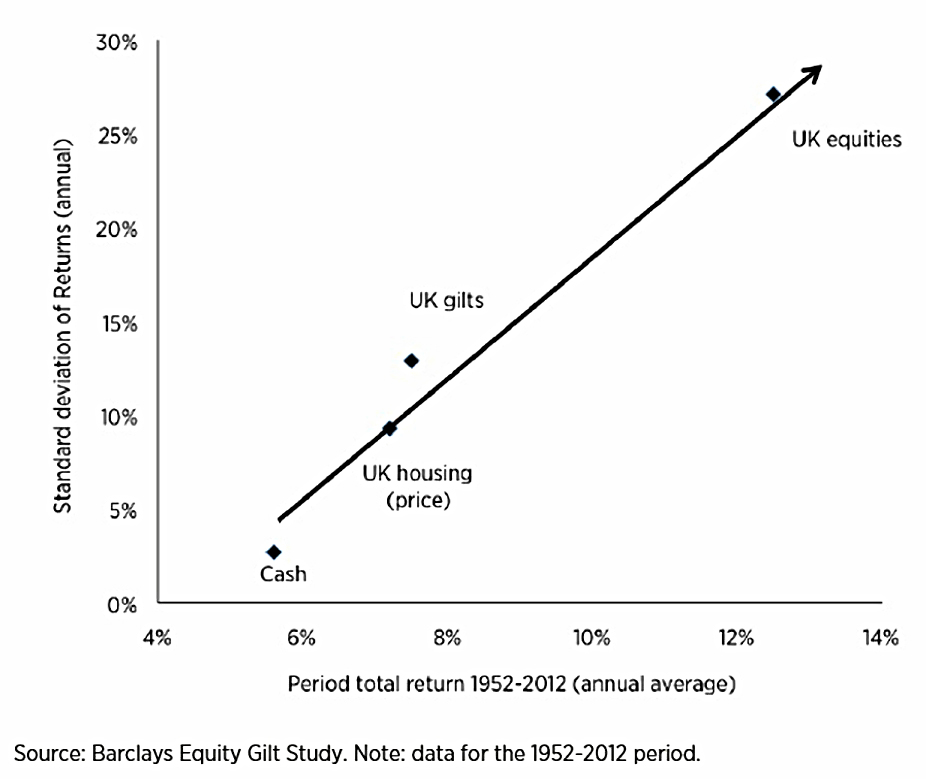

It’s important you understand this, because risk is linked to return, and the higher the level of risk you can tolerate, the higher returns you can expect.

- If investors were not compensated for taking greater risks, they would leave all their money in the bank.

Economic conditions

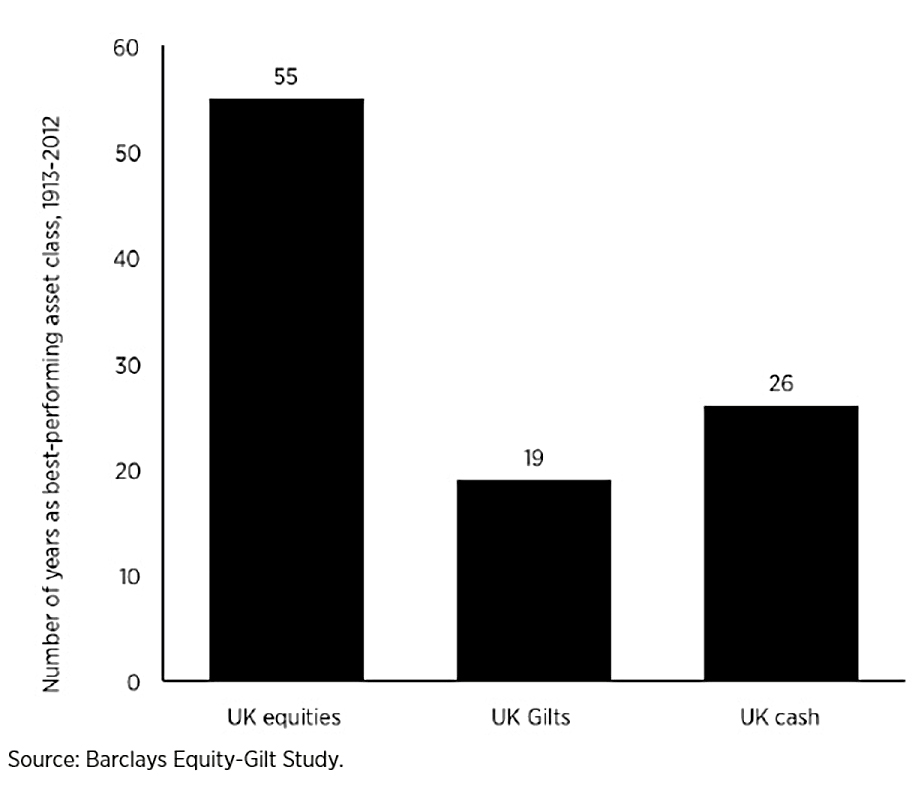

Shares perform best on average, but don’t do well when economies are heading into recession.

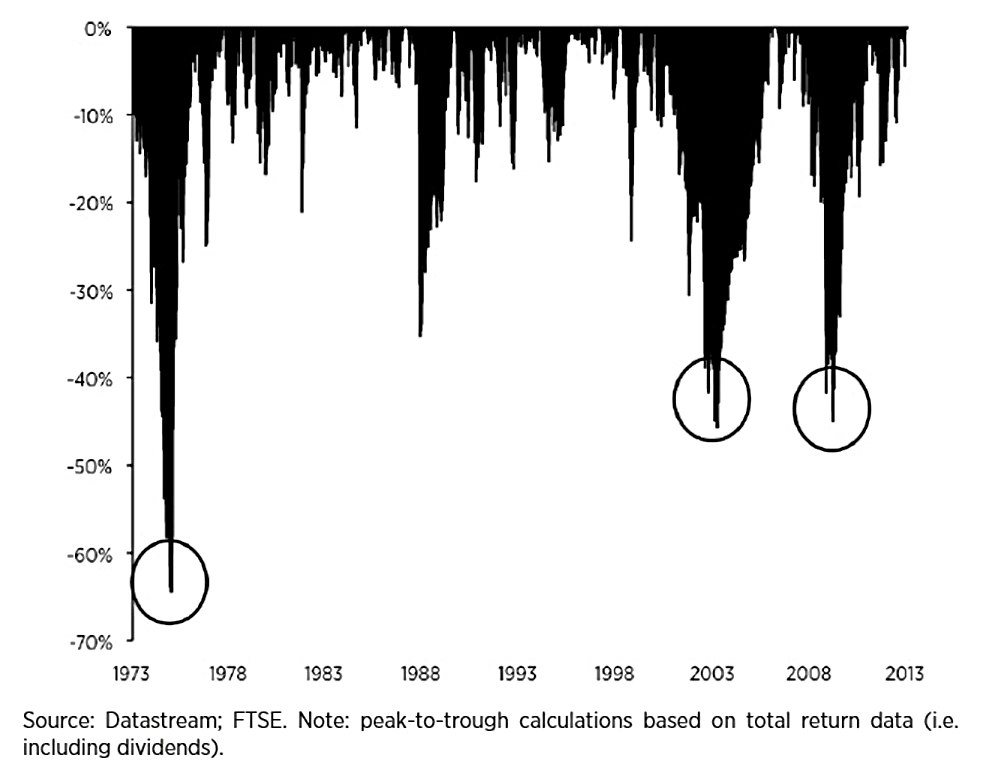

- Most investors will be familiar with this, as there have been two bad crashes (close to 50% in the UK) since 2000.

- From 1973 to 1975 the FTSE fell by 65%.

In general (but not always), government bonds do well when shares go down.

- Which is why they are the traditional diversifying asset.

- In 1973-4, bonds fell alongside shares (ouch!).

- This was because there was a recession and also high inflation (which is bad for bonds).

- Cash was the best asset in those years.

Ed proposes that as a basic principle, his strategies will invest in stocks when they are rising, and switch to bonds when stocks are falling.

- Cash will be used as a last resort asset, when both stocks and bonds are falling.

This is of course, market timing, which most advisors today would warn against.

- But it is also trend following and momentum factor investing, which most people agree works well.

Rather than use plain index-tracking funds (ETFs) to access the three asset classes, Ed will exploit known market-beating effects (presumably through smart beta funds, as per the unit trust he manages).

That’s it for today.

- We’re a third of the way through the book, so I hope to complete our journey in another two articles.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.