New Banks / AltFi London Summit 2018

Back in March, I was lucky enough to get a ticket to the AltFi London Summit 2018. The main item on the agenda was the rise of the New Banks.

AltFi London Summit 2018

This post has been a long time in gestation.

- Back in March, I was lucky enough to get a ticket to the AltFi London Summit 2018.

I really enjoyed the show, and started to write an article about, but for some reason I never completed it.

- The focus of the show was on the rise of the New Banks, and what’s in store for them.

That’s the focus of this post, too – but first, a bit about the show.

Regular readers will be familiar with AltFi.

- We’ve covered some of their previous events.

- And I often quote and link articles by their main man David Stevenson, who writes the Adventurous Investor column in the FT. (( In fact, a series of lectures by David at French investment bank SG were the main inspiration behind me starting this blog ))

AltFi describe themselves on their website as:

The world’s leading news, views and events company for the rapidly growing alternative finance, digital banking and robo-advice sectors.

Each year they organise a series of global and regional summits for industry figures, and at the end of March it was London’s turn.

I was lucky enough to get hold of a ticket for the event, which was held at etc venues in Bishopsgate.

- This wasn’t a location that I was familiar with, but it turned out to be next to a bank that I used to work for – as well as being an excellent conference venue.

Four sessions

The all-day event was split (( By excellent catering over breakfast, lunch and two coffee breaks )) into four sessions:

The early morning session was a kind of “state of the nation”:

- A keynote speech from an MP was followed by an interview with the CEO and co-founder of one of the day’s major sponsors – Funding Circle (which has since IPO’d).

- After that came a panel on whether Fintech is really expanding access to financial services, another panel on the psychology of saving / investing and a short speech on automation.

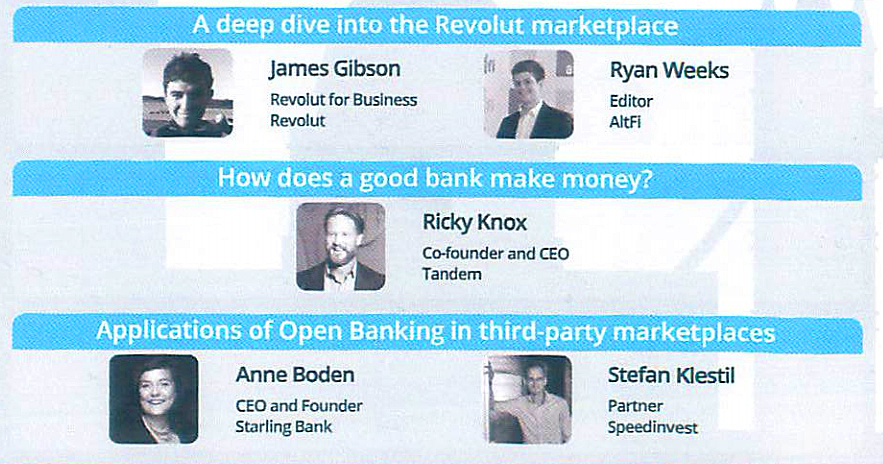

Session two cover three more of the big players (technically, they aren’t all banks) – Revolut, Tandem and Starling.

Session three was all about direct lending, which is what the P2P lending market has evolved into.

- An alternative term (used by Alt-Fi) is “non-bank lending”.

There was a lot of good stuff here, but we’ve covered the area in many previous posts and it isn’t the focus for today.

- My main issues are (1) the poor tax treatment of the product

- and (2) the large amount of cash (£100K+) needed to achieve reasonable diversification within the only tax-shelter available

- this is the IF-ISA, which cannibalises funds that could better be directed to a stocks and shares ISA.

Only the investment trusts (which have a patchy record to date) offer a solution to both issues.

Session four had another panel on lending, and the day was wrapped up with a discussion of technology in fintech and the big banks.

The consumer view

Younger readers (( If I have any )) are probably already familiar with these new banks, but people my age probably aren’t.

Let’s start with a typical consumer view of banking, and what the challengers can provide.

- The most basic need is for a free current account.

- Next comes a credit card, perhaps with cash back.

- And you might want a savings account with a decent interest rate.

- For those who travel a lot, free cash abroad / good FX rates and fees are important.

- For those with a company, free business banking is attractive.

- Younger people especially will want a slick app, a breakdown of their spending into categories, and perhaps budgeting tools.

- Account analysis was previously the domain of specialists like Yolt ((which I use )) but became much more mainstream in 2018 when the Open banking initiative came into force.

- My understanding is that lots of high street banks still haven’t done much with it yet.

- Monzo even has IFTTT integration (is this is of interest to you, you’ll know what I mean).

- On the other side of the coin, lots of people also want a mortgage.

- I will ignore other debt-enabling features like easy & cheap overdrafts, as I’m not a fan of unsecured debt.

- It’s worth noting that most incumbent banks make most of their money through loans of one sort or another (including credit cards and mortgages).

The high street banks do a fair job of providing a free bank account, though perhaps without the slick app and analysis that some people might want.

- Lots of the new banks launched with just a credit card, but most have now added a current account, or plan to.

The simplest (( that is, non-Amex and therefore universally accepted )) cash back credit card is from Tandem, though it only pays 0.5% pa.

- Disclosure – I have this card (and really like it).

Marcus – the new kid on the block (in the UK, at least) from Goldman Sachs – is probably already the leading digital-only savings account.

Starling offers (amongst other things) a free business account.

- I plan to get this account, but I’m in the middle of a long-term project at the moment, and don’t want to fully switch banking facilities until mid-2019.

Revolut became popular on the back of its FX features (which use a prepaid card).

- Starling and Tandem offer similar – and sometimes cheaper – services.

- And Revolut has had recent problems with security and lockouts.

Even new banks that charge for such things (eg. Monzo – a breakaway from Starling which has more than 1M customers, most aged under 30) work out much cheaper than the high street banks.

Atom Bank is the only other digital player that I have heard of – they offer fixed savings accounts and mortgages.

- I prefer instant access accounts to fixed savers, so I’m more likely to go with Marcus.

(I’m excluding bricks and mortar challenger banks like Metro in this section.)

The marketplace

So much for how one consumer sees the playing field.

For the new players themselves, it’s all about the marketplace.

- This will allow them to try to substitute commission income for the loan income (interest) than drives most incumbent banks.

If not, they will need to take deposits and lend them out.

The simplest way to get a handle on the marketplace is think of it as a replacement for comparison websites.

- Instead of you going to visit a website to find a better utility provider, cheaper insurance or a new mortgage, your digital bank will suggest alternatives to you, based on what it knows about your lifestyle.

Alongside this, there will be chosen partners in complementary fields (pensions, investments, FX etc – perhaps P2P lending).

- For business accounts, there will naturally be business marketplaces (accounting, payroll, tax services etc).

If this all takes off, the high street banks will need to respond.

- But they might be held back by their existing relationships and commitment to in-house solutions.

- And the new banks might be expected to have cost-base and technology advantages.

On the other hand, incumbents have a trust advantage, which will be important to many customers, and especially to older (and richer) ones.

There are privacy issues here, too, but as with Google ads (in my opinion), at least the customer’s data is being used to their advantage.

- I wouldn’t personally use a service that required sign-in through, say Facebook (as apps like Plum and Emma – part of Monzo – do).

- And I plan to keep services as separate as possible, rather than using Open Banking to link everything to a central account.

Conclusions

I have a favourable impression of the only new bank that I’ve used so far (Tandem – just a cash back card for me).

- I plan to open a second (business) account (with Starling) soon.

- And I’m thinking about opening a savings account with Marcus.

But how will the new banks shift customers over from the incumbents?

- I see no good reason to move my current account at the moment.

- And if I want the marketplace functionality, something similar will probably be provided by “overlay” apps like Yolt.

With high street banks offering free banking, do the new banks need to offer interest-bearing current accounts to win people over?

The big unknown is the marketplace concept itself.

- But without serious numbers of users, will a winner (or more likely, a few winners) ever emerge?

That’s it for today.

- I’ll be back in a few weeks with a closer look at the two or three products I use (Tandem, and by then, Starling and / or Marcus).

I’ll also take a look at the state of the marketplaces of the leading players.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.