Robo Advisors 13 – Open Banking

Today’s post is a little off-centre for our Robo Advisors series. We’re going to take a look at the Open Banking initiative, and what it means for FinTech and for investors.

Open Banking

Over the recent holiday period, the Open Banking regulations came into force in the UK.

- You may have come across the ban on payment method surcharges, but the more interesting parts of the new legislation to implement the Second EU Payment Services Directive have had less media coverage.

- Back in September, Which? found that 92% of people had not heard of Open Banking.

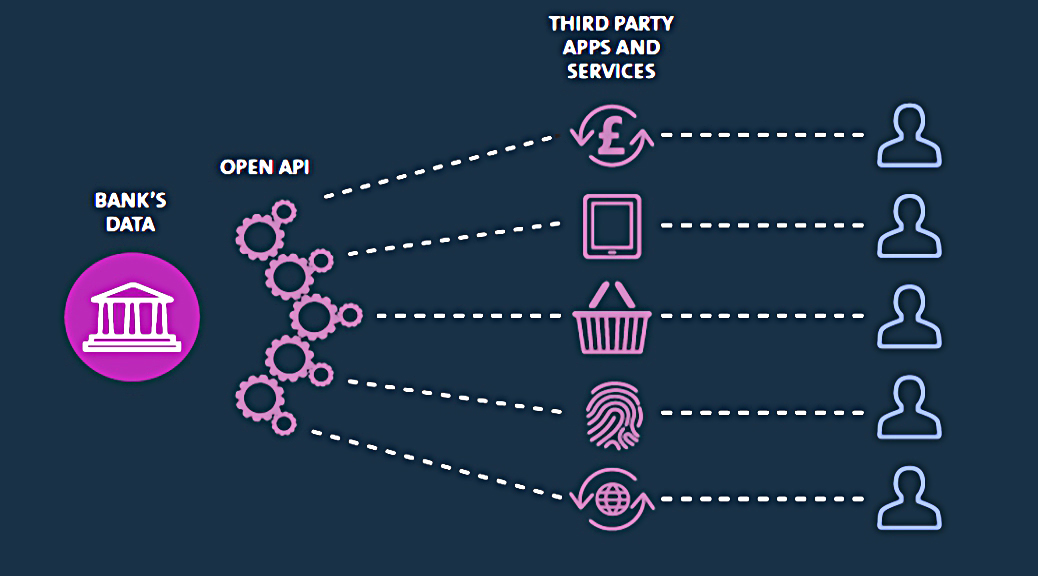

Under the new rules, the nine banks with the largest market share are required to adopt and maintain common API (application programming interface) standards.

- With your permission, your bank can now hand over details from your current account – right down to the transaction level data – to other banks and third parties.

- The data can go as far back in history as your bank has records.

Conceptually, your data now belongs to you, rather than to the bank.

- The Which? survey found that 51% were unlikely to share their financial data, even if it meant they were offered more relevant products and services.

- A similar survey from Accenture found that 69% would not share data.

Third parties can also be given the power to make payments or move money from one account to another (for example, to avoid a current account going into the red and incurring overdraft fees).

- Transaction data has been able to be shared since 13th Jan 2018, but third-party payments don’t come into force until 28th Feb.

Third parties will need to be regulated by, the FCA or another European regulator.

Open Banking was developed by the Competition and Markets Authority (CMA), which worried that people were paying too much for current accounts, and the difficulty of comparing deals was holding them back from switching.

- Just 3% of people switch accounts each year.

The UK is the first country in the world to introduce these standards.

- The hope is that they will enable rival firms to compete for your business (current account services, savings and loans) and also to allow companies to offer services that help you to manage your finances.

Eight banks and building societies, including Barclays, HSBC, Lloyds, RBS, Santander and Nationwide, have joined up straight away, though their business banking arms are not all involved yet.

Sounds familiar

Services like this have existed for a few years, but until now they have not been supported by the current account terms and conditions of the high street banks.

- You usually had to handover your account passwords, which could invalidate your fraud protection if anything went wrong.

Yolt (from Dutch bank ING) was one of the biggest players in this space, with more than 100K users.

- Their app can now use real data rather than screen-scraping and shared passwords.

- Screen-scraping will be banned from September 2019

Yolt is regulated by De Nederlandsche Bank, the Dutch central bank.

The new apps

Andy Webb took a look at some of the new apps over on his blog Be Clever With Your Cash.

Lucy Warwick-Ching had a similar article in the FT.

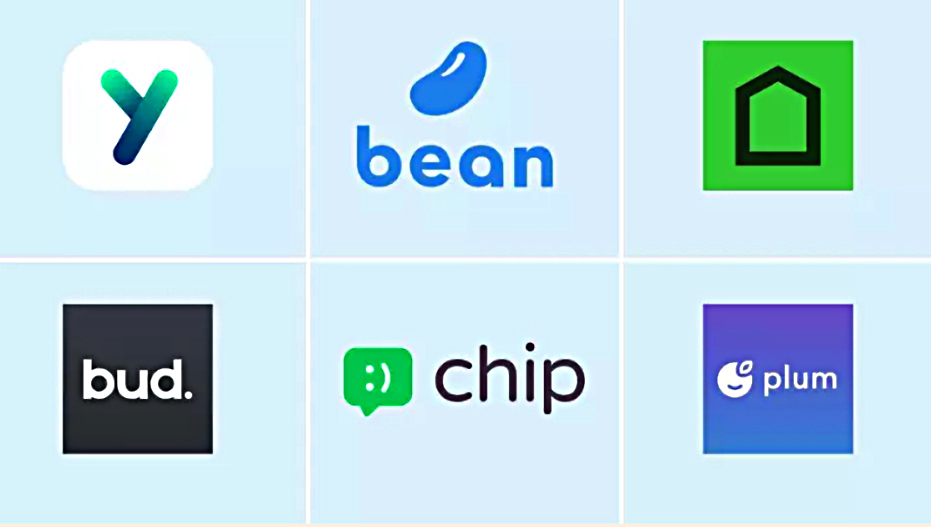

Here’s a quick summary of the apps they looked at:

1 – Yolt, which we mentioned above – this is the phone app that Andy uses the most.

Yolt predicts future spending so you have a “smart balance” – i.e. what you really have to spend or save after forthcoming credit card and household bills are taken away.

2 – Cleo – this is a chatbot in Facebook, which immediately means I’m not interested.

3 – Money Dashboard

4 – Emma

5 – Chip

- This is one of the apps that analyses your spending data to work out how much you can afford to save.

- And if you let it, it will even make the transfer to your savings account (with Chip) on your behalf.

6 – Plum

- This is another savings app, but it sends your money to peer-to-peer lending.

- I think this is a bad thing, as the risks are much higher than with savings accounts, so tying the two together is potentially misleading.

- Plum is also a Facebook Messenger app, which means that it’s not for me.

7 – Bean

- This is a switching app – it analyses your data to work out where it thinks you are overspending.

- You can authorise it to switch you to a cheaper deal,or just cancel your existing service.

8 – Mespo

- This is another switching app, but it runs on Messenger so I will be ignoring it.

9 – Bud

- Another switching app.

Its app trawls through thousands of deals from third-party providers to recommend the best offers on mortgages, broadband and energy deals.

10 – Coconut

A business current account that allows freelancers to track the tax they owe in real time. It also helps them manage client payments and expenses.

11 – Fluidly

- This app uses accounting software and your bank account to “help small businesses get paid faster”.

12 – Trussle

- This is a mortgage-switching service.

Retail

It won’t just be FinTech firms that want to get hold of your data.

- High street retailers will want it, so that they can deliver a more rewarding shopping experience in order to compete with the highly-personalised online environment.

Another survey by Accenture found that 74% of retailers were interested.

Shops like Caffe Nero already have apps that tap into their own shopping basket data, but access to your entire shopping habits will lead to ever more tailor-made offers to consumers.

- This could be the beginning of the end for loyalty cards.

As well as shops, insurance companies and utility providers (phone, broadband, water, gas and electric) will also be interested.

Fraud

Some commentators are still worried about crime.

- Apart from the risk that Open Banking security could be breached, it’s also likely that vulnerable people will be targeted by fraudsters claiming to represent legitimate Open Banking services.

Which? fears a rise in “authorised push payment scams”.

- Here fraudsters trick account holders into making a payment to a bogus account, often by posing as their bank or the police.

Cases of “remote banking fraud” have doubled in the last four years to 18,848 in the first six months of 2017.

- Losses went up from £31.7M to £73.8M.

In response, the government has set up Get Safe Online, a fraud awareness and advice service.

Conclusions

The good news is that the CMA decided to make it easier to switch current accounts, rather than opting for market intervention like a charges cap.

I don’t see this stuff as a game changer, since my current account and cash saving are such a small part of my financial plan.

- Most of my time is spent managing investments, and I have no desire to join those accounts together.

But it might be useful to tie your current account to your credit cards, to make analysing your yearly spending much easier.

- Even then, my most active accounts include a joint credit card, and a company current account and credit card, so the analysis software would need to be fairly sophisticated.

And I suppose having the utility providers contact you to beg you to switch could be fun.

On the down side, I worry that the line between savings and investments (probably P2P and crowdfunding to begin with) will become more blurred.

- I’m all for getting people out of the habit of keeping their savings in cash, but P2P and crowdfunding are the last place they should be heading.

At the moment, I’m viewing this initiative in the same way as the early days of the internet.

- Joining everything together is just the start – it’s what we do with the data that matters.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.