Hoarding Cash at Home

Today’s post is about hoarding cash at home as protection against negative interest rates. Is it really a practical option?

Contents

Hoarding cash

Today we’re going to talk about hoarding cash at home, in case we ever face negative interest rates here in the UK.

- I know Mark Carney has said that we’ll never have them here, but given the spread of “forward guidance” we’ve had from central bankers on both sides of the Atlantic over the past few years, I don’t entirely believe him.

This article is prompted by Merryn’s column in the FT last week, where she suggested buying a safe, and helpfully provided a couple of websites where you could do just that.

- More on that later.

Negative rates

Merryn lists the causes of negative rates:

- ageing global demographics

- oversupply in many industries

- lots of post-crisis debt

- low oil and commodity prices

- a weakening Chinese currency

- the rise of robotics and automation

The main expression of these factors is via low and now negative bond yields, but since private investors are under no compulsion to buy things that return less than you paid for them, we can easily dodge that bullet.

For a few countries (eg Japan), negative rates have spread to deposit accounts.

- Savers are being charged to keep their money at the bank.

The obvious way around that is to keep cash at home instead.

- Your interest rate is then a maximum of zero, but that’s better than a negative number.

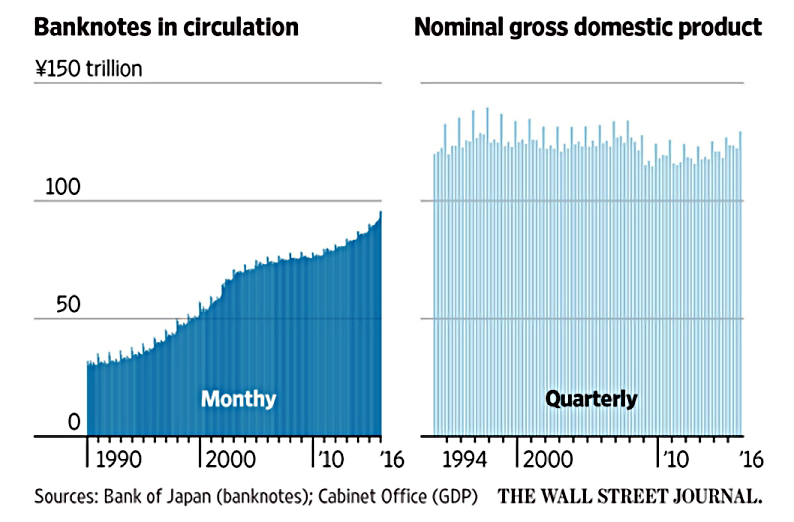

That’s what’s been happening in Japan.

- The amount of cash in circulation has steadily increased, and there has been a run on safes (sales were up 250% in 2015).

- Similar things have been happening in Switzerland and Germany, too.

Even here in the UK, one in five people already keeps cash at home.

- The average UK stash is £345, so the national total is around £3bn.

- Some people think there’s a lot of under-reporting, and the real total might be £5bn.

- And the amount of money in circulation has risen to £63bn, or £1K per person.

So is keeping your money at home in a safe really safe – or even practical?

How much do we need?

Before we take a look at Merryn’s safe-selling websites, let’s work out how much money we’ll need to keep at home.

Most visitors to this website will have a long-term perspective on saving, and will be working towards retirement (at an early or a normal age).

- To retire safely in the UK requires getting on for £1M.

- An annual income of £25K at a withdrawal rate of 3.5% pa needs a pension pot of £714K

- The average house price in the UK is £217K

- So that’s a total of £931K

Now of course in some parts of the county houses are much cheaper, and of course two people can live (almost) as cheaply as one.

- Many people will be able to survive on less than £25K a year, as well.

But as a ballpark figure, most people will be looking to save between £0.5M and £1M over their lifetime.

So if cash hoarding is to make a significant difference, the amount we hoard needs to be a significant portion of that pot.

- We’re not talking about taking £200 out of the cash point and hiding it in the coffee jar.

Let’s be conservative and say 10% of your portfolio.

- And let’s be even more conservative and say that lots of people will be interested in hoarding when they are only half-way through their journey to £0.5M / £1M.

So we have a range of hoard sizes from £25K (10% of £0.5M / 2) right up to £100K.

The other way to look at this problem is from the spending point of view.

- If you only spend £25K a year, how much cash do you need to have on hand?

But this is more a question of emergency cash, rather than avoiding negative interest rates.

- Negative interest rates might last for years, in which case you’re back into the £25K to £100K ballpark.

That’s a lot of money to hold at home, and there’s another potential problem.

- If interest rates go negative, the Government might place restrictions on what you can hold at home. ((You might of course decide to ignore such restrictions, since cash is untraceable – a maddening fact to central bankers ))

- Greeks currently have to declare cash of more €15K, and back in the 1930s, private ownership of gold was banned in the US (and the gold was confiscated).

The final thing to consider is how much money you are saving by hoarding.

- If interest rates were at -1% (which is unthinkable to me) then on £25K you would be saving £250 pa.

- On £100K you would be saving £1K pa.

Solutions that cost more than this to implement are not economical.

Which notes?

Here in the UK, we have a limited range of note denominations in which to keep the cash.

- We have the £50 note, but you don’t see many of them in everyday life (Mike Ashley’s wad excepted).

- Lots of retailers don’t like to accept them.

It’s also been noticed in the wake of the new plastic fiver ((Insert money laundering joke here )) that while a timetable has been announced for the introduction of plastic tenners and twenties, there’s no timetable for the plastic fifty.

Interestingly, the EU plans to withdraw the €500 note – known as the Bin Laden – since it apparently supports criminality.

- It forms an ever-increasing share of the euros in circulation.

- It’s the same story in Japan, with 10 thousand yen notes (only worth around £70) on the rise.

Even the US is taking a close look at the usage of the $100 bill.

- Perhaps there really is a war on cash after all.

I’m going to assume we’ll keep our cash in widely accepted twenties.

- That’s 50 notes to a thousand pounds, meaning our stash is somewhere between 1,250 notes and 5,000 notes.

Collecting the notes

Most banks won’t issue you with a large sum in cash, so you may well be reduced to taking the money out of a cashpoint, £500 at a time if you are lucky.

If you can be bothered to walk to the cashpoint three times a week (and are happy to walk back with £500 in your pocket) then you’ll be collecting £1,500 a week.

- That means that it will take more than three months to amass £25K, and well over a year to collect £100K.

Better make that a daily trip to the cashpoint.

- Now you’re up to £3.5K a week.

- £25K takes just over seven weeks to withdraw.

- £100K still takes more than six months.

Cash really isn’t that convenient, is it.

- This is all a boring waste of time, and means that you need to plan ahead before negative interest rates hit.

How much space?

I’ve consulted the internet to find out how big such stacks might be, and apparently each note is 0.113 mm thick.

- They are also 149 mm long and 80 mm wide, if you are interested.

So a stack of 1,250 brand new notes would only be 14.1 cm high.

- Let’s play safe and assume used, crinkly notes take up two to three times the space.

That would make a £25K stack around 35cm tall, and a £100K stack around 1.4m high.

I managed to find a picture of £100K in twenties, albeit arranged in nine stacks.

- It looks about right – maybe just over 1m in total, rather than 1.4m.

- So we’ll assume a used note is twice as thick as a new one.

So at the top end we’re looking at quite a big briefcase of money, or perhaps two slimline ones.

- £25K is only half a slimline briefcase.

- £100K would apparently weigh around 5kg, so we would be able to pick up the briefcase.

But we’ll need a safe that’s a lot bigger than the ones you find in hotel rooms to keep your passport secure.

Buying a safe

Merryn suggested two sites (1 and 2).

One thing we need to consider is insurance.

- If you do get robbed then you’ll want to make sure you get your cash back.

- So we need a safe with a £25K to £100 insurance rating.

I’m guessing we also need to tell our home insurer about the cash, and pay an increased premium.

- Most home policies only cover around £500 in cash by default.

- Large companies can insure £100K for around £100 pa, but I suspect that private individuals would be charged quite a bit more.

- And of course insurance exposes us to counterparty risk, which is an odd thing in the context of cash hoarding.

We also need to consider where to put the safe.

- A safe that is easy to find is easy to carry away, unless we can bolt or concrete it into the floor or wall.

We need the safe to be fireproof to some extent.

Looking at the websites, safes with a £100K insurance rating and a 60 minute fire rating started at just under £4K, and were very large and heavy (600 kg).

So this is a pricey route to take.

Safe deposit box

If you trust banks, but just not the central bank, you could always keep your cash at a safe deposit box.

Unfortunately, not many banks provide these facilities these days.

- Barclays and HSBC pulled out in 2015

- RBS and Lloyds only provide services to existing customers.

- None of Halifax (owned by Lloyds), Bank of Scotland (owned by Lloyds), Santander, Co-operative, Nationwide, Virgin Money, TSB Bank and Tesco Bank, provide any safe custody services in the UK.

Coutts and Metro Bank are the only familiar banking names that do provide a service.

- Harrods and Selfridges offer a service, but they are full.

There are some vaults attached to bullion and jewelry dealers, and then there are standalone vaults like Metropolitan Safe Deposits.

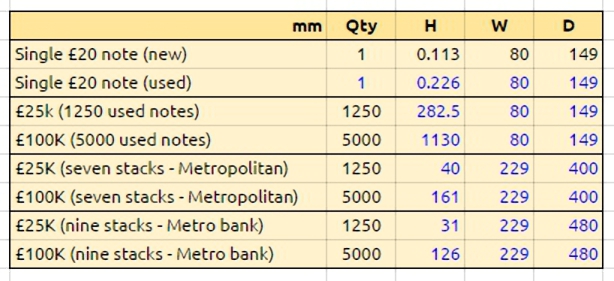

To fit the money into a safety box, we need to re-stack it from its single tall pile.

All of the calculations are shown in the table below.

Metropolitan’s smallest boxes are 110 x 410 mm, which will only fit two stacks.

- We need the medium boxes, which are 260 x 445 – these will fit 7 stacks.

So we need a box that is 40mm high to store £25K – this costs £370 per year including insurance.

- For £100K, we need a box that is 161mm high – this costs £630 per year including insurance.

Without getting into the details of the insurance policy, these boxes won’t be good value unless interest rates fall to around -1% (for £100K) or -2% pa (for £25K).

- There seems to be very little chance of this happening at the moment.

Metro bank’s smallest boxes are 12.5cm x 53.7 cm – these will only fit 3 stacks.

- Their medium boxes are 25cm x 53.5cm and will fit 9 stacks.

So for £25K we need a box that is 31mm high – this costs £325 a year.

- For £100K we need a box that is 126mm high – this costs £475 a year (actually 125 mm high).

Metro bank’s boxes don’t include insurance, so we need to add £50 to £200 pa respectively to these prices.

So safety deposit boxes only stack up ((Geddit )) for large sums at very negative interest rate.

Hiding it at home

The cheap skate approach to all this is to split the money into smaller parcels, and hide it around your house.

Here’s a list of places to consider, excluding under the mattress: ((Credit goes to thesimpledollar.com for these ))

- taped under a shelf or drawer

- in the toilet cistern

- in the freezer

- inside a sock in the sock drawer

- in a medicine bottle in the medicine drawer / cabinet

- in a pocket in one of your shirts or jackets in a wardrobe

- in a filing cabinet

- under the cat’s litter tray

- behind a painting

- in a book or a DVD case on a shelf

- buried in the garden

- in your car

- in / under a pot plant

- with the Xmas decorations

- in the fridge (eg. in a beer bottle)

- inside a flour or coffee jar (any dried goods will do really)

For obvious reasons, I won’t tell you which of these I think are the best.

I will tell you which ones are the most popular (perhaps you can join the dots):

- sock drawer

- mattress

- freezer

You could also use diversion safes, which look like cans of beans / Pringle packets / Coke bottles, or electrical plugs.

I would probably go for using two or three places per room (including the cellar and the garden), which would give me more than 20 places to store some cash.

- That means each envelope would only need to hold £1,250 to £5,000.

- Of course, you’d also need to keep a list of where it was all hidden (and then keep that list very safe).

Conclusions

I sincerely hope we never get negative interest rates, and that we never have to consider hoarding cash at home.

- If we do, then it’s a lot harder than it sounds.

It takes a while to get the cash together, and it costs money to use a safe (with insurance) or a safe deposit box.

- Safes and safety deposit boxes only stack up for large sums at very negative interest rates.

The cheap skate alternative is to split the money into many parcels (20?) and hide it all over you house.

- Even then you’d need a list of where you hid things, which you would in turn need to keep safe.

An alternative to holding cash is gold, which we’ll look at in a future post.

I think it makes some sense to have an emergency stash of a month or two’s cash, but things would have to get pretty bad for me to go full survivalist on this one.

- One per cent a year probably wouldn’t do it for me.

- One per cent a month and I might think differently. ((This actually happened in Austria in the 1930s – Google “Worgl” or “Michael Unterguggenberger” ))

What would you do? Let me know in the comments.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

Interesting article. holding more than a few months worth seems very unpractical.

Good article. I hope it never happens here, since as you point out things could get a little crazy! What about the £50k premium bond allowance? If it still existed in this scenario, it would be of some use unless NS&I charge negative interest on that too (to fund the prizes..). Otherwise, disguising cash as loft insulation (might actually work!) or new fivers at the bottom of the cold water storage tank might be other options to add to the list.

I guess I’m assuming that there would be no accounts (inc. Premium Bonds) with positive returns.

I’ve done my loft already, and I don’t have a water tank, but they’re good ideas.

It is not often that people are prepared to talk about practical ways of hiding wealth, a very necessary activity for those of us most under the threat of losing what we have worked hard for. Be careful however. Some of the above suggestions are not wise. From practical experience I can tell you that paper money can go rotten surprisingly quickly in a damp and airless environment. I do not like banks and have managed without them for most of my life, but acknowledge that the Bank of England were good enough to replace the value of my disintegrating stash as I was able, just about, to identify most of the serial numbers.

I bow to your superior experience – I’ve never hoarded cash to date.

Looking on the bright side, soon all our notes will be plastic, and should last a bit better.

Most of the times people feel insecure if they are hiding money for the purpose of tax evasion and things like this… This post of yours is very much beneficial for those.

Very helpfull article written by a wise person. Thank you!