T-Bills and Chill

Today’s post looks at a 2024 note from Meb Faber of Cambria Asset Management on whether to invest in short- or long-term bonds.

Higher interest rates

Meb’s paper began by celebrating the return of yield for fixed-income investors.

- After 15 years of low interest rates, we now have high (normal) rates (sadly, along with higher inflation).

The paper looks at whether/when investors should move away from the risk-free asset (T-bills) to more “interesting” bonds.

Bond risks

There are two key bond risks:

- Term-premium – in return for the increased volatility and uncertainty of locking away money for years (assuming a hold to maturity), longer-term bonds usually have higher yields (unless the yield curve is inverted).

- Credit premium – other lenders are riskier than the US government, so they have to pay more for people to hold their bonds.

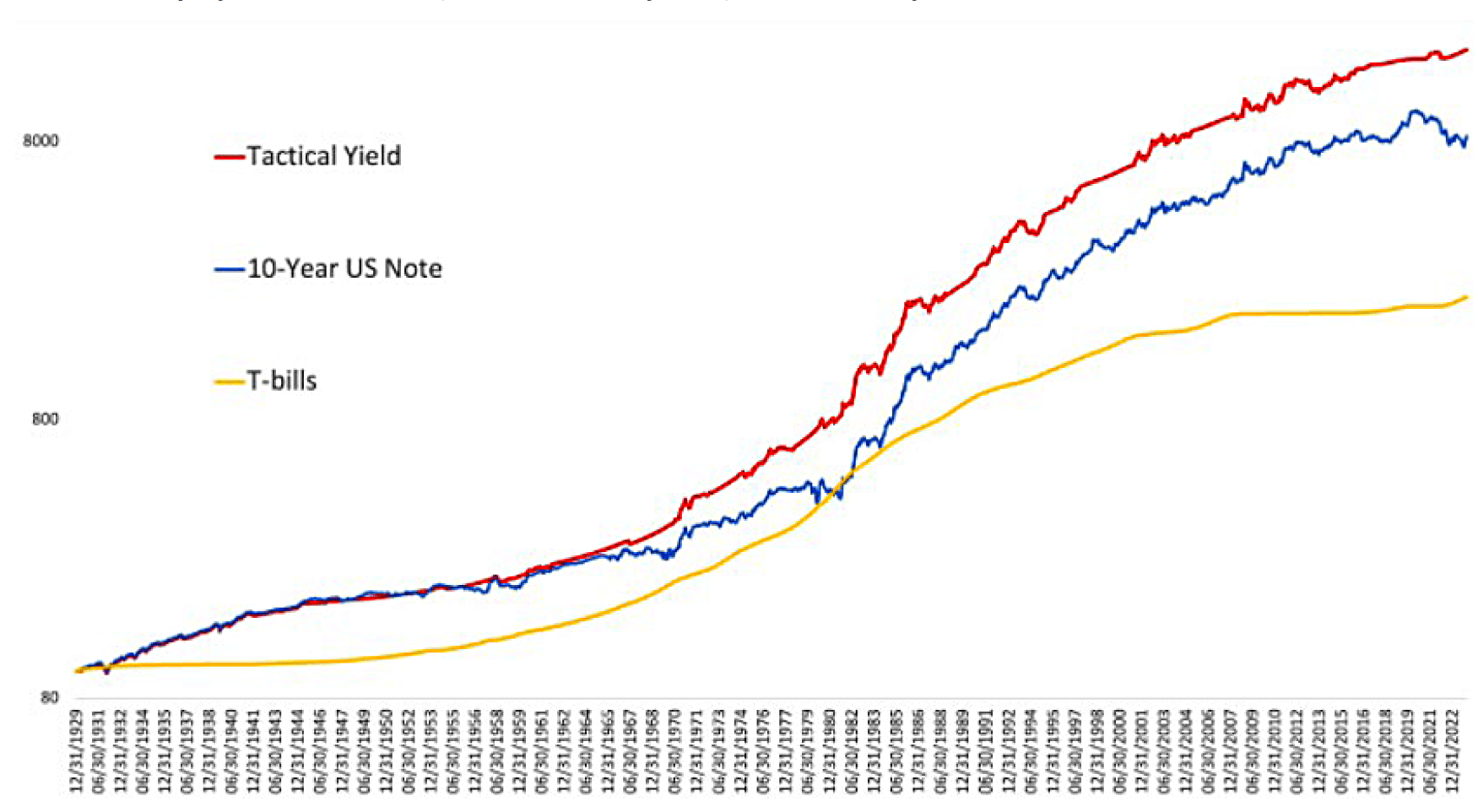

Meb’s objective is to work out when it is worth buying riskier bonds.

The first approach is to rotate into 10-year bonds when the yield spread (over T-bills) is in the top 50% of the historical range.

- This increases returns and lowers volatility and max drawdowns (compared to buy-and-hold T-bills or 10-year).

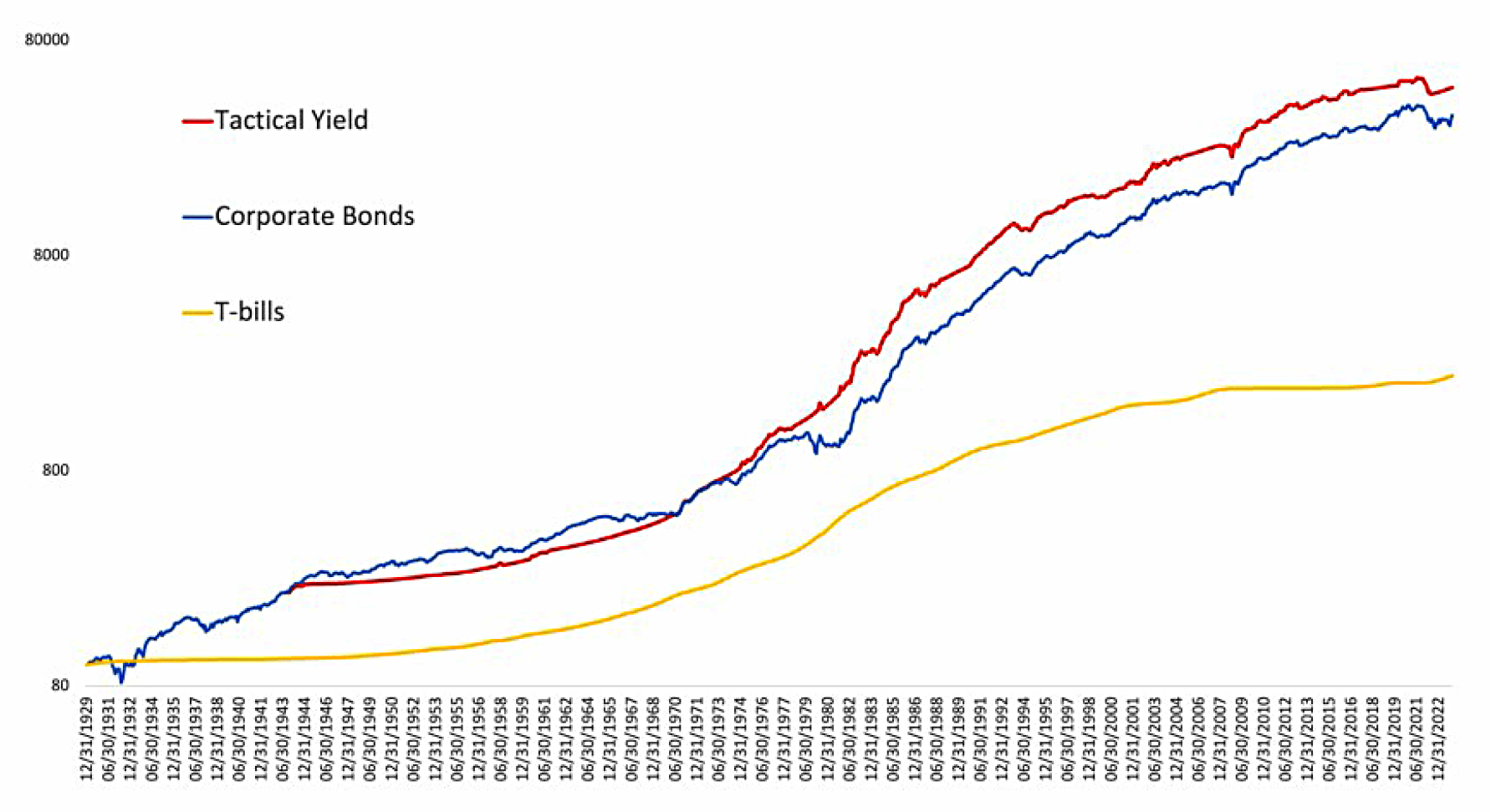

The same result is found for corporate bonds.

System 2 combines the two approaches for further improvements.

System 3 throws in the kitchen sink:

In addition to the 10-Year Treasury Note and corporate bonds, we layer in the 30-Year Treasury Bond, REITs, junk bonds, mortgage-backed bonds, emerging market debt, and 10-Year TIPS as index data becomes available.

![]()

Allocate Smartly

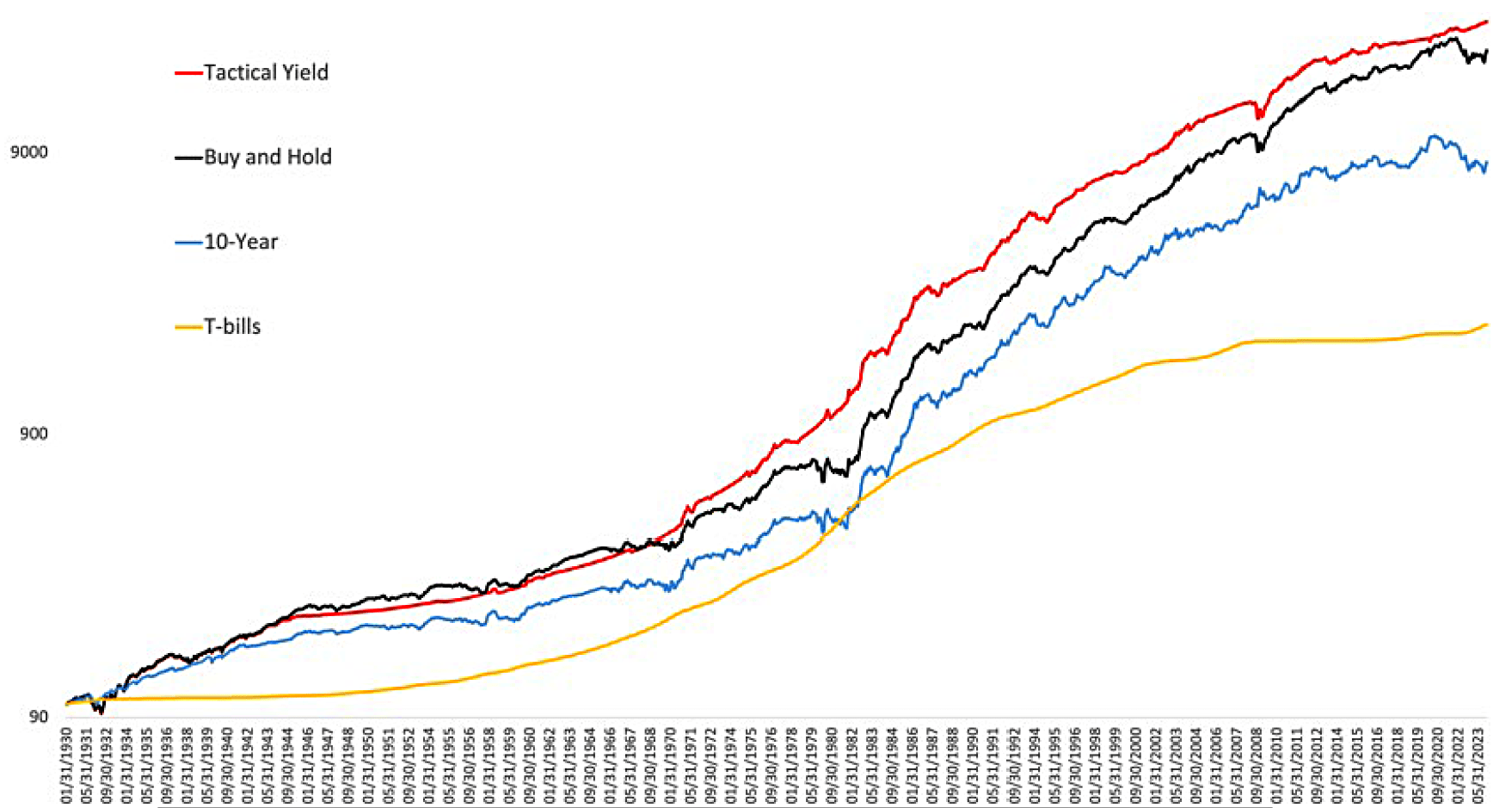

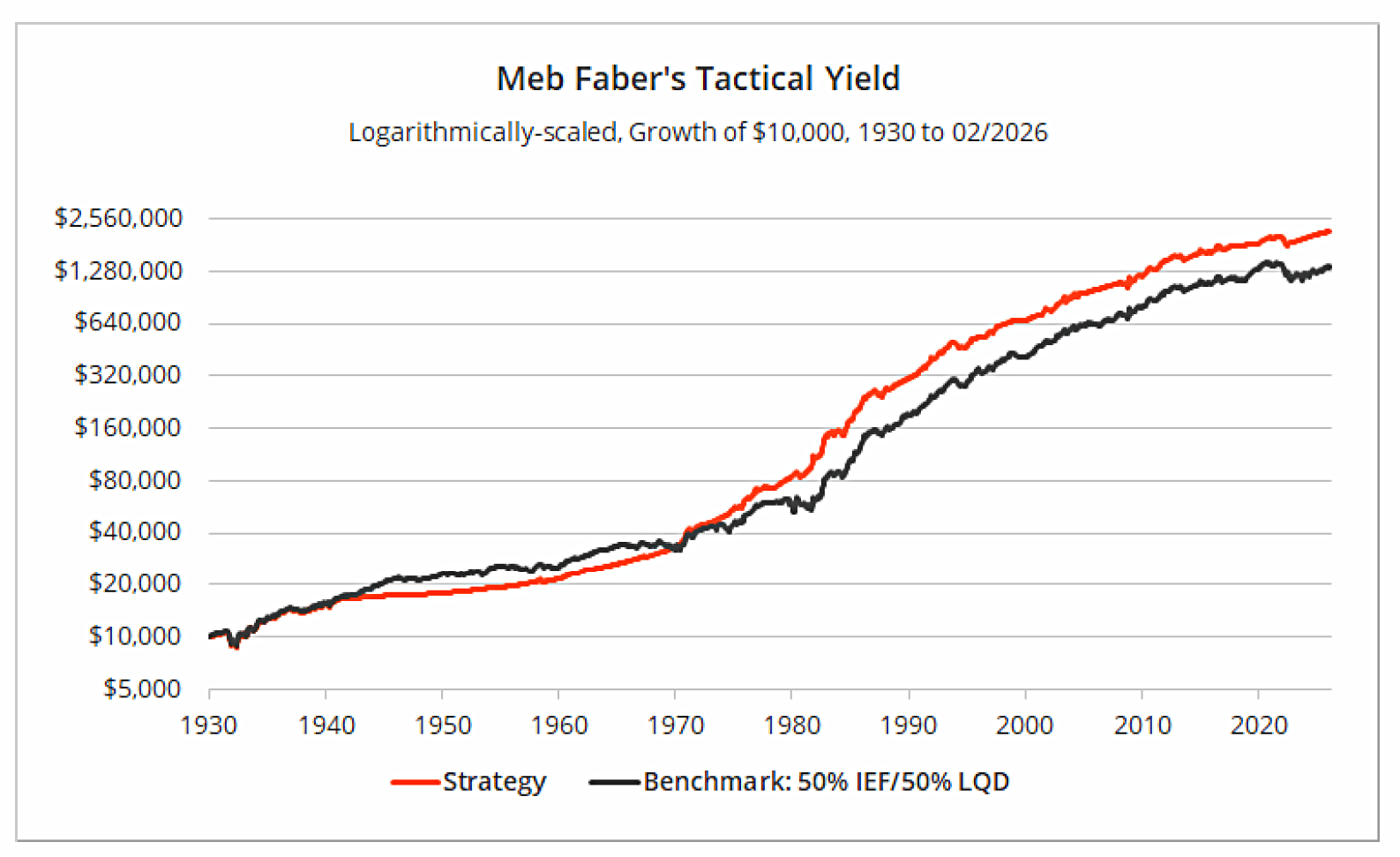

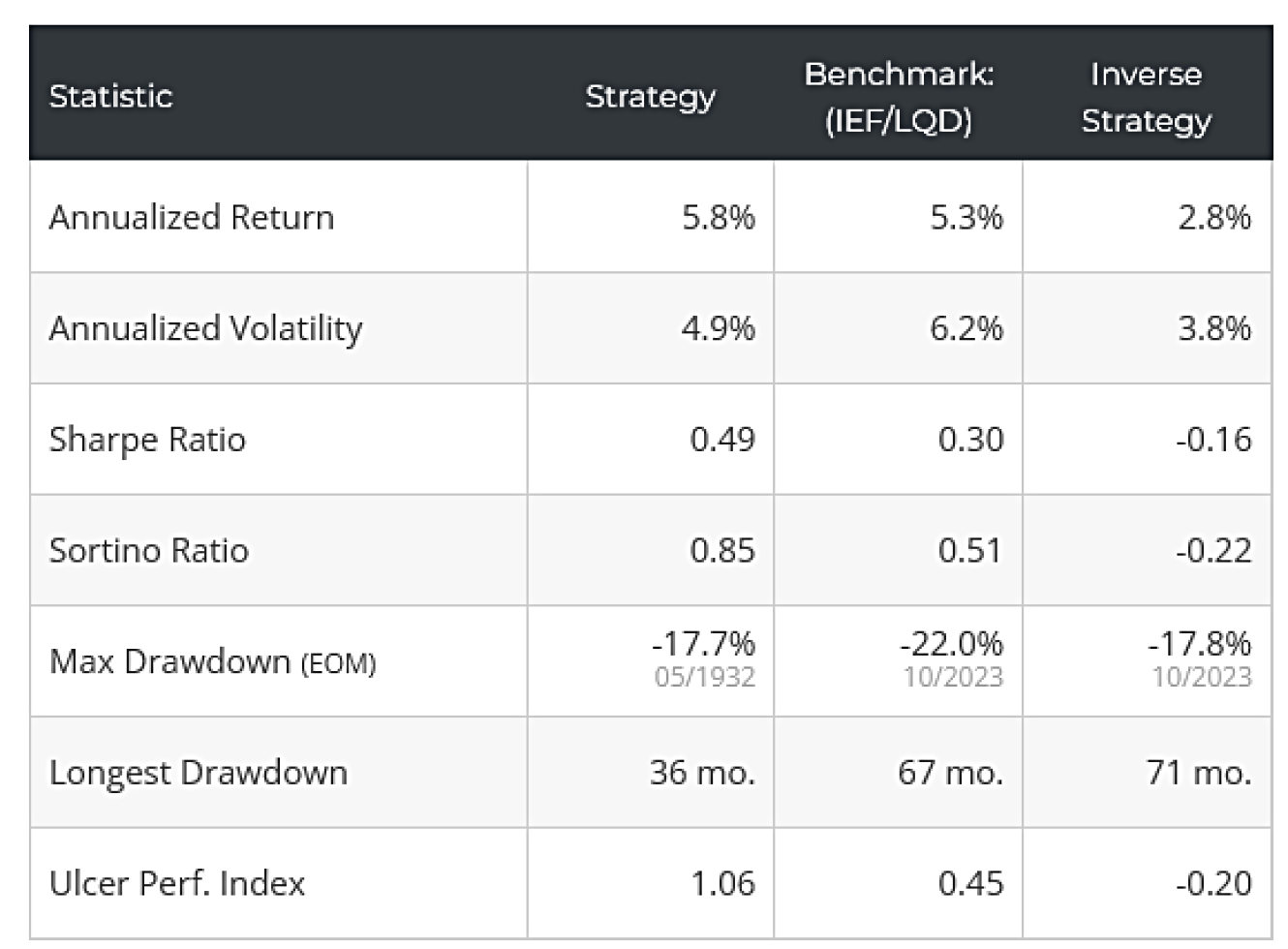

In 2026, the team at Allocate Smartly tested Meb’s tactical yield approach.

- Their benchmark was 50% intermediate term Treasuries and 50% US corporate bonds.

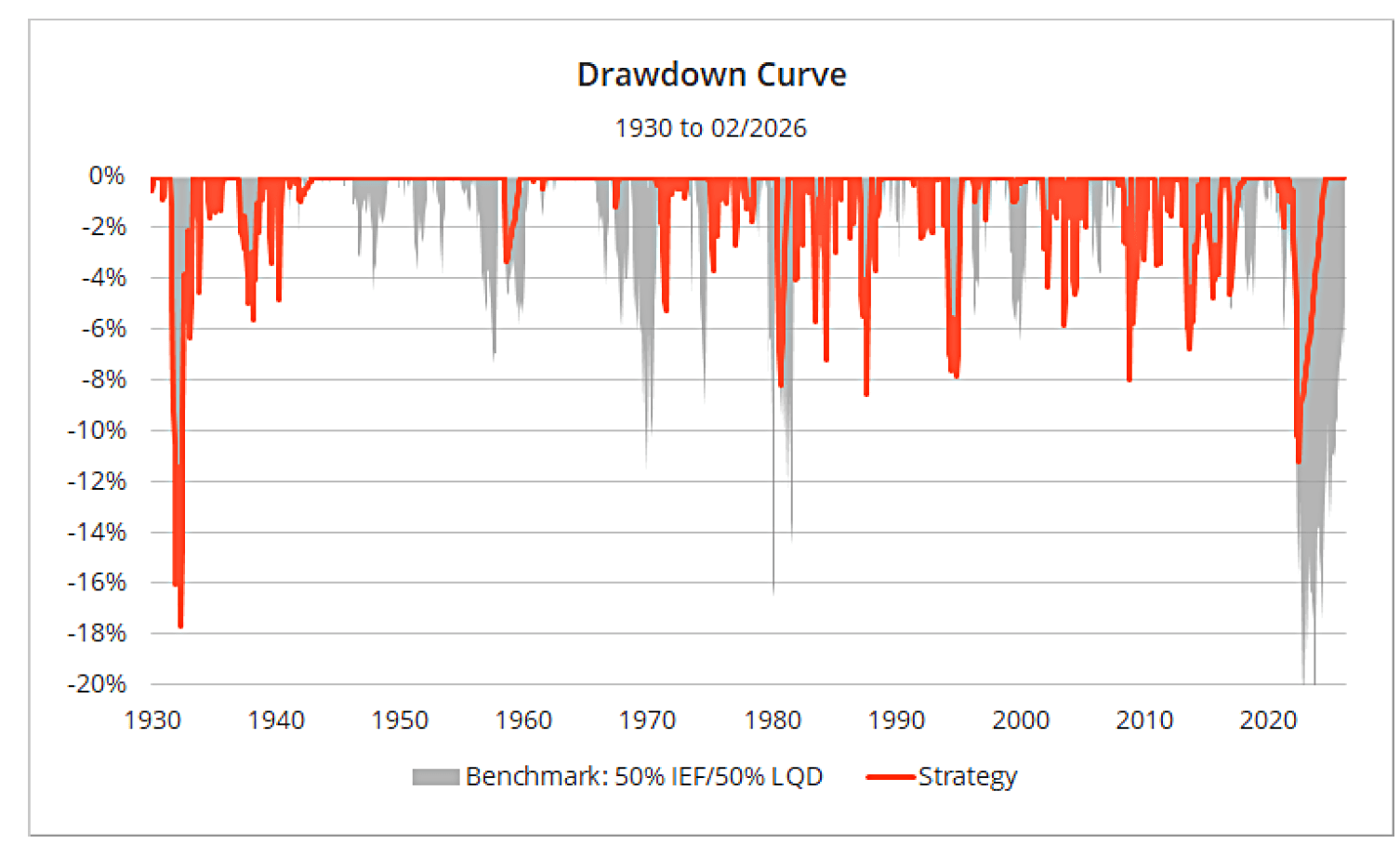

The strategy outperformed.

The purpose of Tactical Yield hasn’t been generating outsized returns. It’s simply been a smarter approach to bond exposure. It has generated bond-like returns, but at substantially less risk.

For fun, AS also looked at the inverse of the strategy, which underperformed the market.

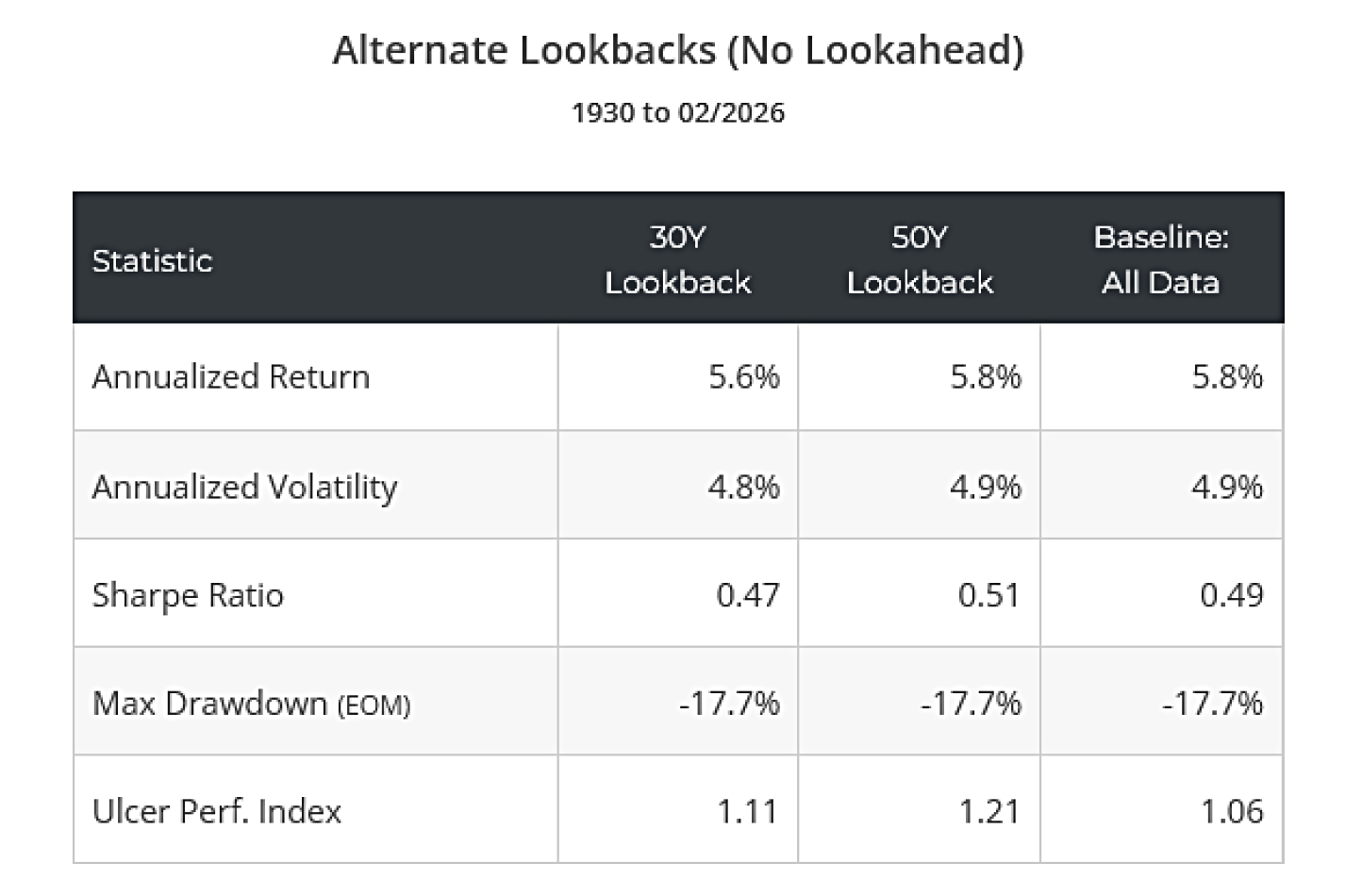

They also looked at different lookback periods (30 and 50 years, rather than all-time).

- There was no significant difference.

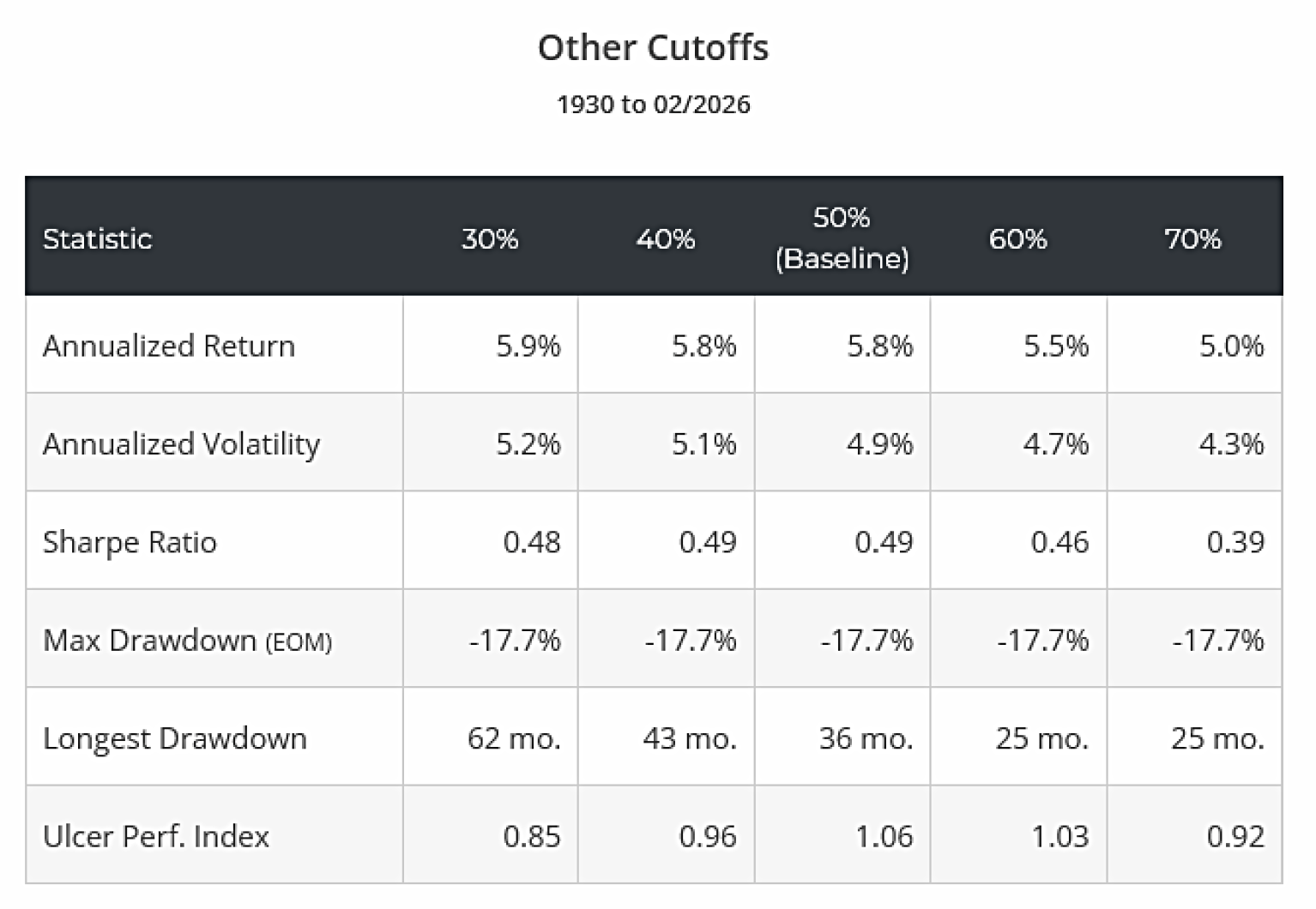

And they tested alternate cutoff levels (from 30% to 70% of the historical range).

The less strict the threshold (30 and 40%), the higher the risk (volatility rises, duration of drawdowns increases). The stricter the threshold (60 and 70%), the less the risk, but total return and risk-adjusted return metrics like Sharpe deteriorate. That matches what you would intuitively expect.

The 50% cutoff is a nice middle ground but it isn’t set in stone. Investors could turn the dial up or down depending on the investment objective.

Conclusions

This looks like a nice and simple idea, but I’m not clear on where I could source the signal indicating whether various types of bonds are in the upper half of their historical yield-spread range relative to T-bills.

- Nor am I clear how far the lookback period should be, though this doesn’t seem to matter (so long as it is large).

Of course, Cambria has an ETF which will do all this work for you, but it’s not available in the UK.

- How many times have we heard this story?

AS considers using starting (current) yields as the test, rather than the premium over T-bills, but even here, it’s not obvious what the trigger value would be.

Alternatively, a trend-following (or, more strictly, a TAA) approach would use ETFs that cover the various subtypes of bonds.

- 1-year returns and various MAs (probably 50- and 200-day) could be used to allocate to the most promising categories.

That’s it for today.

- Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.