The Best Defensive Strategies

Today’s post looks at a recent paper on the best defensive strategies to use within a traditional 60/40 portfolio.

Alpha Architect

I became aware of the paper (from Baltussen, Martens, and van der Linden, called The Best Defensive Strategies: Two Centuries of Evidence) from an article published on Alpha Architect in March 2026.

- Larry Swedroe also wrote about the paper on his Substack during the same month.

The Problem with 60/40

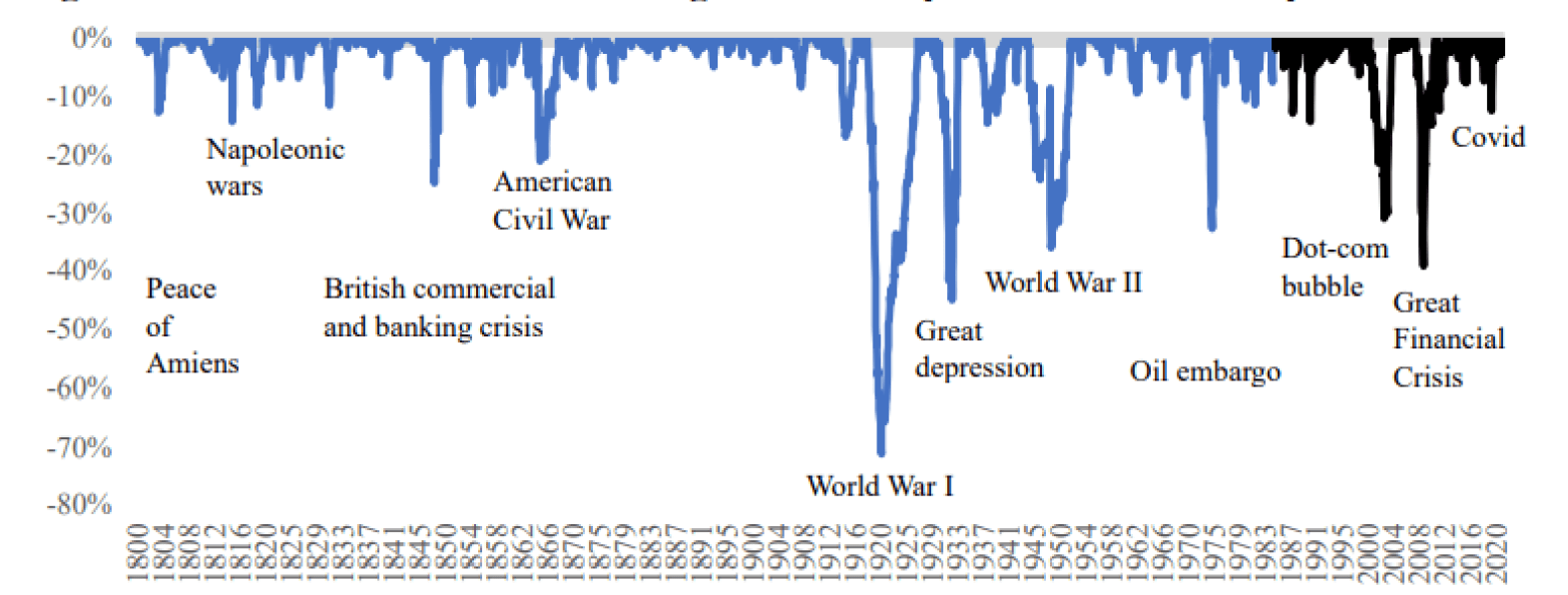

Balanced portfolios (like 60/40) produce strong returns (7% pa over 222 years) but suffer large drawdowns (up to 71%).

- These drawdowns have psychological/behavioural impacts and also produce volatility drag.

The unique feature of this paper is that it evaluates defensive strategies using data dating back to 1800, covering eight instances in which the 60/40 portfolio lost more than 20%.

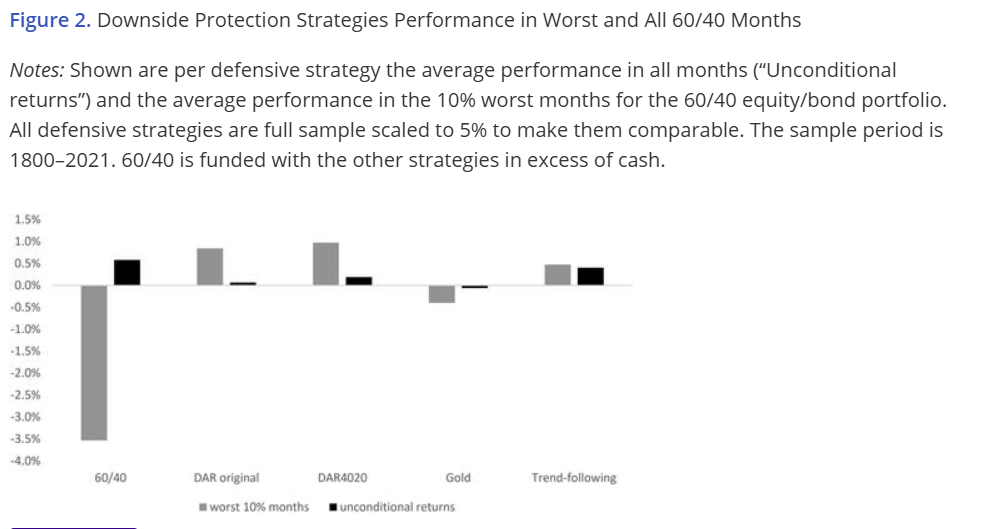

Defensive winners

The main winners are trend-following and factor-based defensive overlays.

The factor overlay used is called defensive absolute return (DAR).

- Regular factors like quality, value, and low risk also helped, but not as much.

Gold looks good using recent data, but less good over the long-term.

Put options can be used to hedge crashes but are expensive insurance if used all the time.

Treasuries are too inconsistent, showing negative performance during the largest equity drawdowns.

DAR

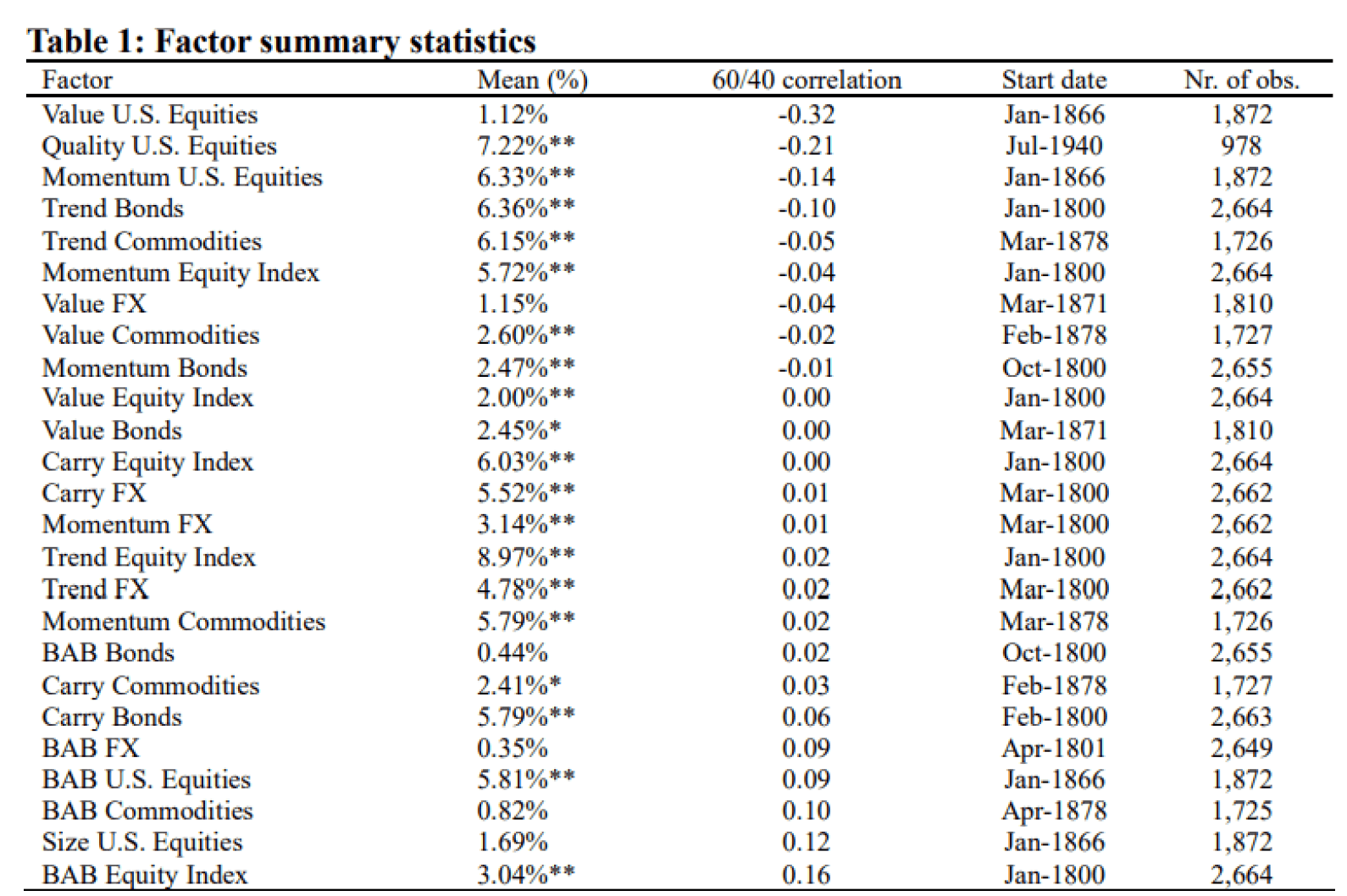

The original DAR portfolio is constructed by sorting a broad set of factor strategies by rolling correlation to the 60/40 benchmark. It goes long the most negatively correlated tercile and short the most positively correlated tercile, producing a negative correlation but near-zero long-run return by construction.

The paper proposes a modification – DAR4020, which is long the 40% most negatively correlated factors and long only 20% of the most positively correlated factors.

- This is net long (improving returns over the full cycle) but preserves much of the defensive protection.

Trend

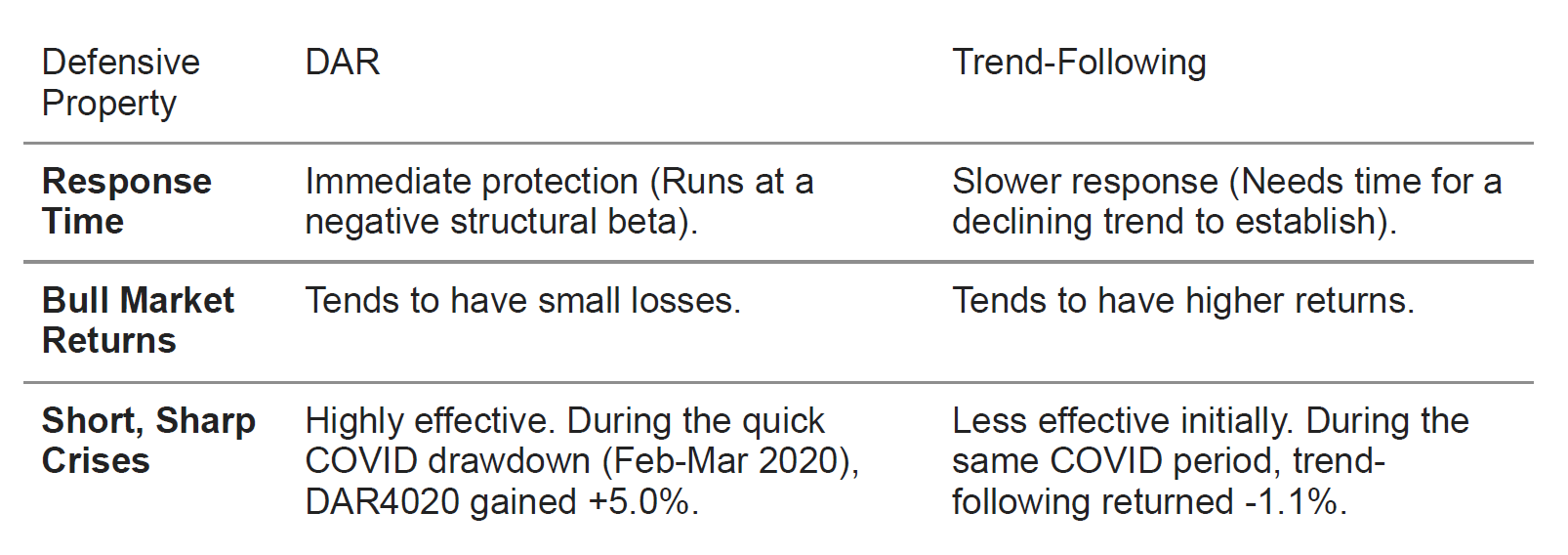

The paper suggests using DAR4020 in combination with trend.

Trend-following is often less helpful at the start of drawdowns, particularly when declines are sharp and short-lived, because signals can be slow to reposition at turning points.

DAR4020, by contrast, tends to provide immediate protection because it is structurally positioned with a negative 60/40 beta. Over longer drawdowns, trend following tends to “catch up” and often becomes highly effective.

Conclusions

It’s another vote for Trend as a defensive strategy.

The DAR4020 sleeve would be hard to implement fully within UK tax shelters.

- Going long some regular factors (plus gold and treasuries) should help a little.

That’s it for today.

- Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.