The Most Important Thing 4 – Patience and Luck

Today’s post is our fourth visit to The Most Important Thing by Howard Marks.

Patient Opportunism

Chapter 13 of Marks’ book is about patience.

There aren’t always great things to do. Patient opportunism – waiting for bargains – is often your best strategy.

You tend to get better buys if you select from the list of things sellers are motivated to sell rather than start with a fixed notion as to what you want to own. There’s nothing special about buying when prices aren’t low.

You simply cannot create investment opportunities when they’re not there. When prices are high, it’s inescapable that prospective returns are low (and risks are high).

You want to take risk when others are fleeing from it, not when they’re competing with you to do so.

Marks quotes Buffett’s philosophy of waiting for the “fat pitch” in the “sweet spot”.

- The idea is that you never have to swing – you can wait until you are ready.

This is not quite correct, of course – not swinging (doing nothing) incurs an opportunity cost.

- There’s always something that’s in a bull market.

For investors like Buffett and Marks, it’s all about the big winners.

- But you have to have the confidence that you will spot them when they arrive.

My own philosophy of incremental marginal gains is almost the opposite.

- I trust in the system – my role is to keep turning up and applying it.

On the other hand, Marks’ comment does demonstrate one of the advantages that the amateur investor has over the professional, who must keep swinging in order to deliver competitive results every quarter.

Marks also warns against reaching for yield, where investors buy ever riskier credits as the yields on safer ones decline.

- It’s another situation (for Marks – the first for me) where doing nothing is a better option.

Marks looks for situations where the may be forced sellers:

The funds they manage experience withdrawals, their portfolio holdings violate investment guidelines such as minimum credit ratings or position maximums, or they receive margin calls because the value of their assets fails to satisfy requirements agreed to in contracts with their lenders.

Why else would people sell assets for less than they are worth?

The key during a crisis is to be (a) insulated from the forces that require selling and (b) positioned to be a buyer instead.

To satisfy those criteria, an investor needs the following things: staunch reliance on value, little or no use of leverage, long-term capital and a strong stomach.

Knowing What You Don’t Know

In Chapter 14, we hit Rumsfeld’s “unknown unknowns”.

One key question investors have to answer is whether they view the future as knowable or unknowable.

Investors who feel they know what the future holds will act assertively: making directional bets, concentrating positions, levering holdings and counting on future growth – in other words, doing things that in the absence of foreknowledge would increase risk.

On the other hand, those who feel they don’t know what the future holds will act quite differently: diversifying, hedging, levering less (or not at all), emphasizing value today over growth tomorrow, staying high in the capital structure, and generally girding for a variety of possible outcomes.

Marks believes that it’s hard to have an edge on macro, but less hard to become an expert in a particular stock.

- And of course, he believes that it’s possible to work out where we are in a cycle.

He spends most of the chapter bashing forecasters.

- In essence, most forecasts extrapolate the past and are least useful at turning points, where there is the greatest potential for profit.

I like Marks’ separation of investors into two groups, and I definitely prefer the behaviours of the “know nothing” group to those of the “know-alls”.

But although I’m also somewhat cynical about forecasting, I believe in historical macro data in aggregate, and in current data.

- And I think that trends persist long enough to be useful.

Further, since the 2008 crisis, government and central bank action has become much more important and is certainly worth keeping an eye on.

- Even narrowing the range of possible future scenarios can be useful.

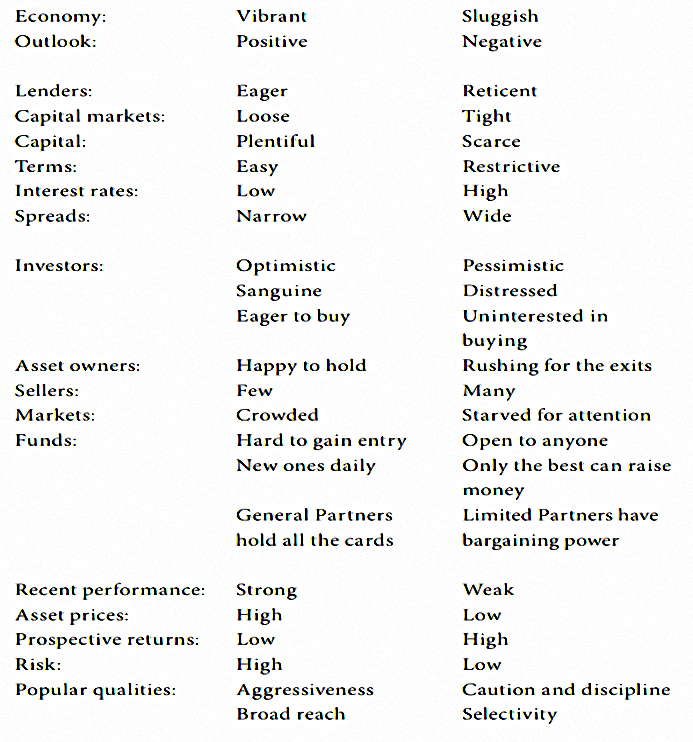

Where We Stand

Chapter 15 returns to the topic of market cycles.

Marks begins with two approaches that he thinks should be avoided:

- try to predict the future (see the previous chapter)

- ignore cycles (buy and hold).

Instead, we should try to figure out where we are in the cycle and look at the investing implications of that position.

- Marks is basically looking for situations where a market may have reached an extreme.

And he’s looking to the opposite of what the majority of market participants might do.

Are investors optimistic or pessimistic? Do the media talking heads say the markets should be piled into or avoided?

Are novel investment schemes readily accepted or dismissed out of hand? Are securities offerings and fund openings being treated as opportunities to get rich or possible pitfalls?

Has the credit cycle rendered capital readily available or impossible to obtain? Are price/earnings ratios high or low in the context of history, and are yield spreads tight or generous?

Marks looks at the signs that were present before the 2008 crisis:

- lots of high-yield bond issuance at low credit ratings

- debt issued to fund dividends (these days its for buybacks)

- lots of buyouts (PE) at high multiples of cash flow and high leverage, and in cyclical industries

- the increasing appetite for “silver bullet” (can’t lose) investments – hedge funds or “absolute return” in this case

Or as Marks puts it:

Too much money chasing too few deals. It helps to think of money as a commodity. Everyone’s money is pretty much the same.

Marks has a checklist of words to look out for (the left column is the dangerous one):

Luck

Chapter 16 is about recognising that not everyone who is successful is a genius.

- They could just be someone who got lucky with a risky bet.

And many of life’s “losers” could be just as skilled as they are.

The chapter leans heavily on Taleb’s ideas from Fooled by Randomness.

- Taleb talks in terms of alternative histories to the visible histories we can observe.

At a given time in the markets, the most profitable traders are likely to be those that are best fit to the latest cycle. This does not happen too often with dentists or pianists – because of the nature of randomness. – Taleb

The lesson here is pretty simple – don’t get carried away with someone’s past results.

- You need to understand how he got them, whether there is an observable underlying system that you are able to apply, and whether that system is likely to work in the future.

As Marks puts it:

It’s essential to have a large number of observations–lots of years of data – before judging a given manager’s ability.

It can be hard to know who made the best decision. On the other hand, past returns are easily assessed, making it easy to know who made the most profitable decision. It’s easy to confuse the two, but insightful investors must be highly conscious of the difference.

In the long run, there’s no reasonable alternative to believing that good decisions will lead to investment profits. In the short run, however, we must be stoic when they don’t.

Conclusions

It’s been an entertaining read once again, and a slightly more philosophical one today.

- But apart from the chapter on cycles, there hasn’t been too much to help us with our day-to-day investing.

- And I’m finding the relentless focus on value strategies a little tedious.

I’ll be back in a few weeks with a look at defence, pitfalls and adding value.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

An interesting read again, Mike. I think two points emerge:

a) the recent COVID-19 crisis spooked a number of UK investors as in early April when the FTSE stood at 5,400 they sold £700m worth of units in the Fundsmith and Lindsell Train equity funds. Following the market hitting the 6,110 figure this month investors poured nearly £3bn of money into equity funds including both of these. Between these dates the market rose over 12%- sitting tight with your investment strategy and avoiding all the noise around you can reap big rewards!

b) as the article suggests, you need to look under the bonnet of active fund managers and assess why they perform – are they one or several hit lucky wonders or do they have genuine skill? It is noteworthy I think, that the funds that have done consistently well prior to the crisis are still doing that (Fundsmith, Scottish Mortgage, Buffettology, Slater Growth, Guiness Global Equity Income and Threadneedle Global Bond are all still top quartile) that must demonstrate some skill, whilst the dog funds before (M&G Recovery, Invesco High Income, LF (ex Woodford) Equity Income) are still 4th quartile and their managers (or ex managers) are culpable rather than capable!