AQR on Diversifiers

Today’s post looks at a recent note from AQR on the best, rather than the most frequently marketed, diversifiers.

AQR

We’ve come across AQR many times before on the blog. This paper was published in April 2026 and is called “A Positive Stock-Bond Correlation Is a Terrible Reason to Add More Equity Risk to Your Portfolio”. The authors are Cliff Asness, Daniel Villalon and Antti Ilmanen.

Positive Stock-Bond Correlation

The paper was written in response to questions from clients on what to do about the recent positive correlation between stocks and bonds, and in answer to other papers from the industry that recommend the wrong diversifiers.

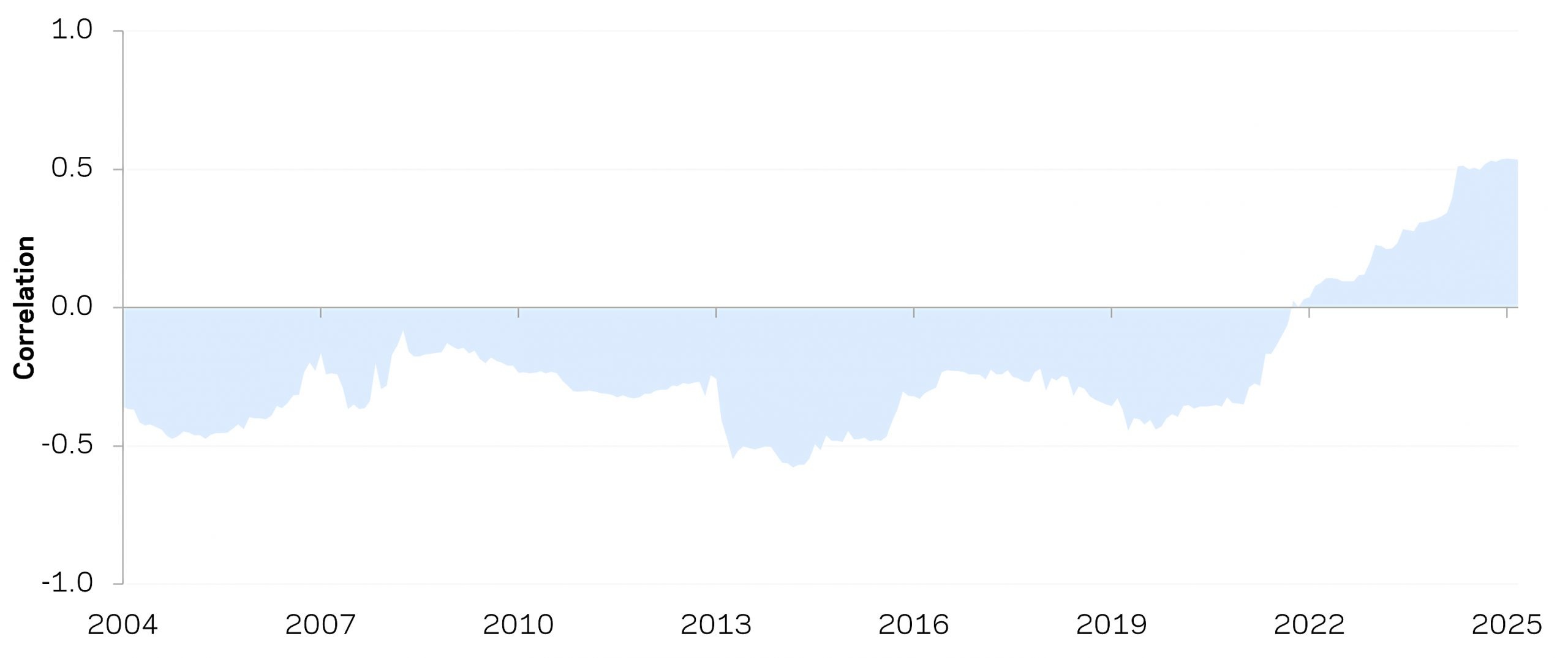

After a decent run of negative correlations (largely because of falling bond yields and later supported by falling interest rates), the correlation between stocks and government bonds turned positive a few years ago (chart below).

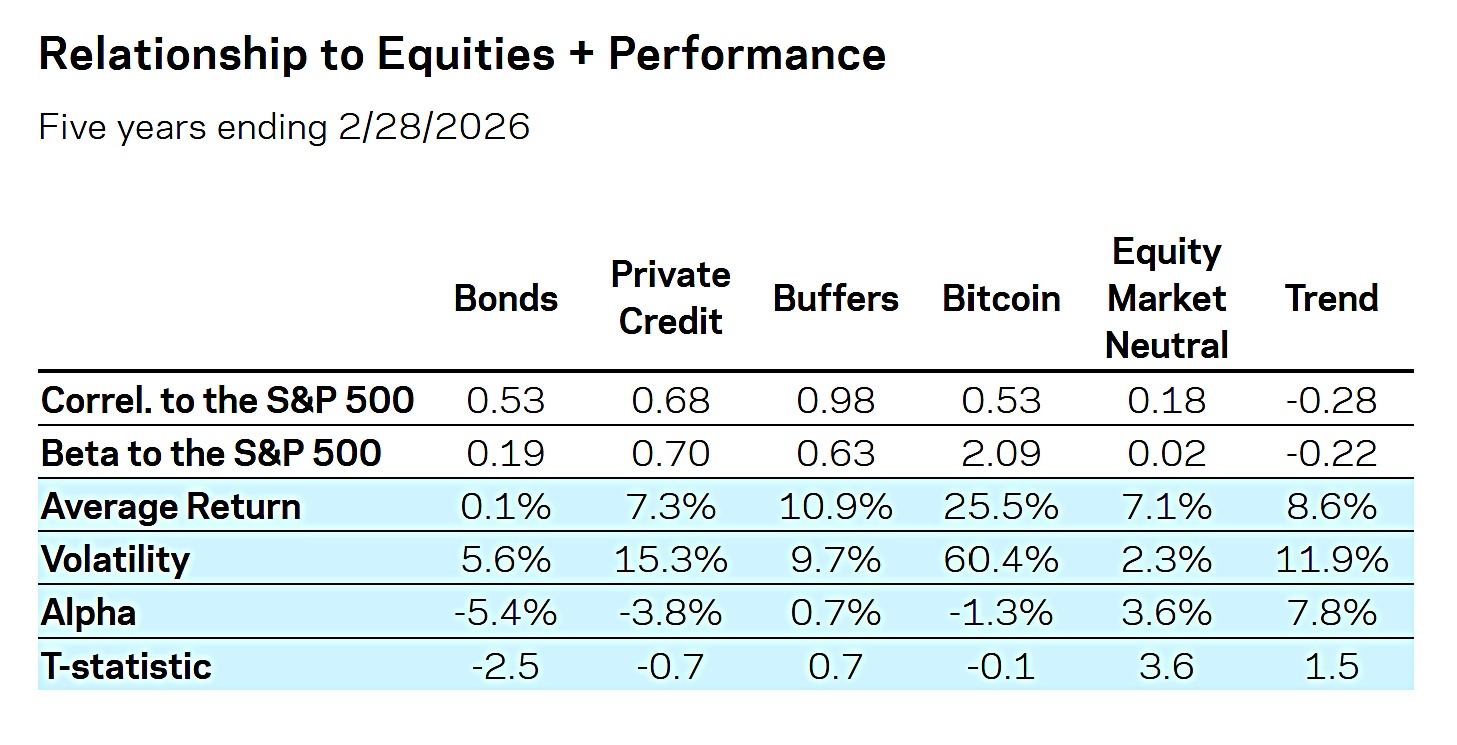

With bonds unable to diversify equity risk (but did they ever – see below), investors are being pushed into private credit, buffer funds and crypto. AQR points out that these assets have more equity market risk than bonds, so they are not really helping with diversification.

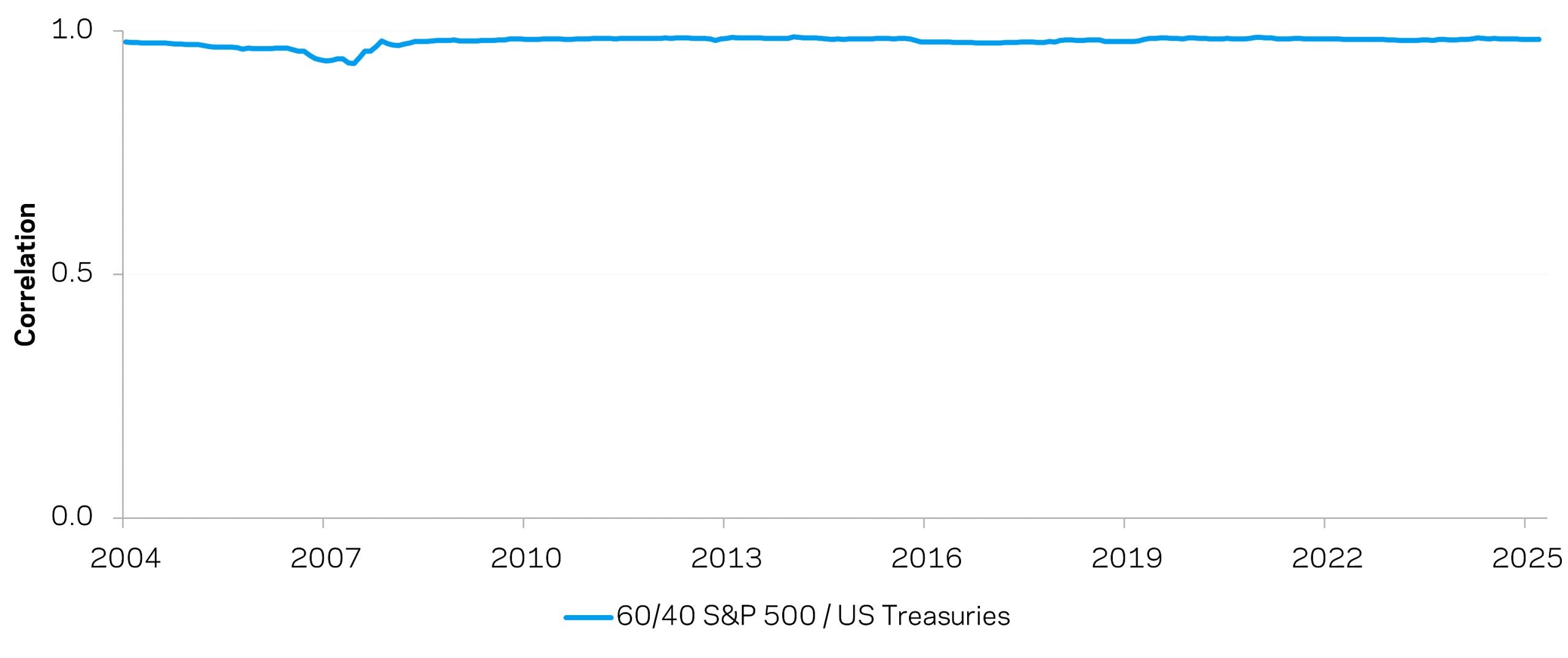

This chart shows that the classic 60/40 portfolio has always been very closely correlated with stocks. In other words, bonds don’t really diversify (largely because they are not volatile enough).

So the stock-bond correlation doesn’t matter that much – what we need are assets and strategies that really diversify away from stocks.

Beta

AQR wants to talk about beta, not correlations.

While correlations can tell us something about how strongly prices move together, to get a better sense of economic magnitudes – or how much equity risk something has – beta is a better statistic to look at.

Beta has a very simple economic interpretation: an equity beta of 0.5 means that for every dollar allocated to the asset, you get about 50 cents of equity exposure.

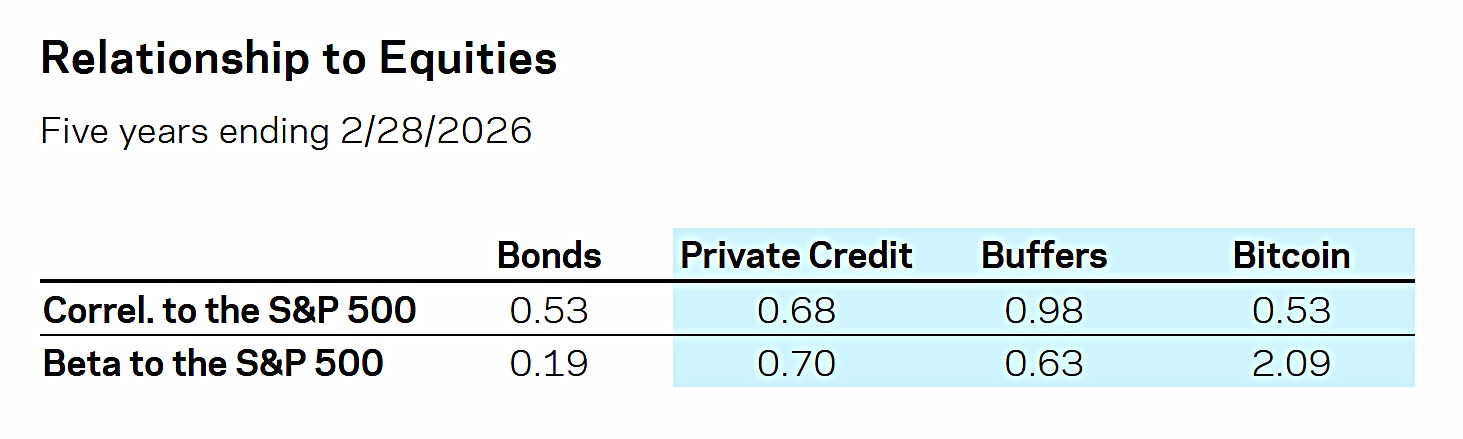

Bonds have recently had a high correlation to stocks, but with a beta of 0.19.

- The three popular alternative assets have both similar or higher correlations, but more importantly, much higher beta.

Private credit often understates its true economic risk and volatility, thanks to how loans are valued, and thus how returns are reported. One way to get a more market-based estimate of these risks is to look at the performance of lending-oriented exchange-traded Business Development Companies (BDCs). Over the past five years, these private credit proxies have delivered returns with more than three times as much equity risk as Treasuries.

Buffer funds use options to deliver a “pre-defined outcome” based on the unknowable future performance of an equity index. Proponents of “buffers-as-bond-replacements” often argue that, like bonds, buffers offer “known” pay-offs. [But] concerns about inflation risk mean that, arguably, you should add some inflation-sensitive assets to a portfolio, not more equities with options added on top.

Buffer funds also return less than the equivalent risk portfolio of stocks plus cash (I don’t use them, for similar reasons to why I avoid dividend stocks and other income strategies).

Bitcoin is often touted as a diversifier, but it isn’t:

Over the past five years, the correlation between Bitcoin and stocks has been about as high as the feared correlation between stocks and bonds – but due to Bitcoin’s super high volatility, its equity beta is 2.0. Investors moving from bonds to Bitcoin for diversification reasons are getting 10x the equity risk for every dollar they move.

What the other commentators are really doing is performance-chasing of assets that have done well in recent years (private credit and bitcoin) and/or selling unproven financial innovation (buffer funds and bitcoin).

Real Diversifiers

Of course, real diversifying strategies are available (and I’m sure they are available from AQR).

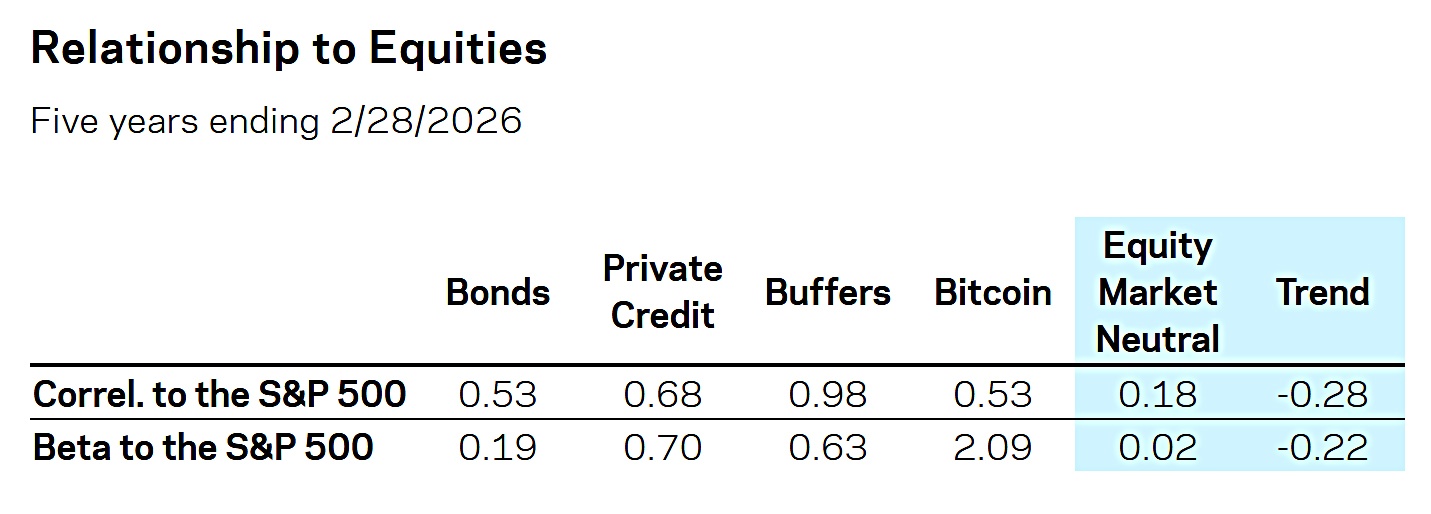

- The paper highlights two specifically for equity risk diversification – Equity market neutral (long/short) and trend-following.

EMN has a stock beta of zero over the past five years, and trend has a negative beta. Trend is also particularly helpful during equity drawdowns.

For UK tax-shelter investors, trend is now available via an ETF, but shorting would have to be manual and outside the tax shelter.

Performance

Diversification with low returns is not much help. So the final table in the paper adds returns, volatility and “alpha” relative to stock returns.

The first three alternatives all have attractive returns relative to bonds, but this comes from their equity exposure.

- EMN and trend have both attractive returns relative to bonds and significant alpha over their (low/negative) exposure to stocks,

Conclusions

AQR have two points:

- Positive stock-bond correlations don’t mean you have to dump bonds

- If you do cut bonds, it’s better to replace them with assets that have less equity exposure.

We generally like bonds as part of an overall portfolio, even with recently higher correlations. There’s little else out there that performs as consistently well during recessions and related environments of falling growth.

I get a lot of my bond-like exposure from DB pensions and cash, so replacing bonds isn’t a hot topic for me.

- I have never looked at private credit or buffer funds, and whilst Bitcoin did look like digital gold for a while, it now looks more like a crazy tech stock.

So I’m happy to take AQR’s advice and look at EMN and trend instead.

- In practice, this means a 5% allocation within my SIPP to the single trend ETF available in the UK.

I’ll keep my eyes peeled for developments in these areas.

That’s it for today.

- Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

You didn;t give us the name of the Trend ETF !

Sorry – DBMG – iMGP DBi Managed Futures R USD

What is the trend ETF available in the UK?

Sorry – DBMG – iMGP DBi Managed Futures R USD