Rethinking 60-40 – Part 3

Today’s post is our third visit in 2021 to the topic of whether the traditional 60-40 stocks/bonds portfolio still makes sense.

Contents

Recap

Here’s what we covered in the first two articles:

- Stocks are riskier (more volatile in price) than bonds but have higher long-term returns.

- The logic of blending two assets together comes from the idea that their prices will move in different directions.

- When stocks go down, you hope that bonds will move up in price.

- The riskiest portfolio recommended by financial advisors to customers with differing levels of risk appetite would be 80-20 stocks/bonds – and the safest would be 40-60

- So the 60-40 portfolio can be thought of as the middle option of three.

- In fact, bonds are a pretty bad hedge for stocks in any case, unless you either hold a lot of them (bad for overall returns) or use a lot of leverage (risky).

- But the 60:40 portfolio is easy to understand and has proved pretty easy to market to investors.

- It’s also done pretty well over the decades, so many investors would miss it.

The impact of inflation

- The need to rethink 60-40 all starts with the prospect of higher inflation and its potential impact on the bond-equity relationship.

- If inflation rises for an extended period, this could be bad for both stocks and bonds.

- In quant speak, the bond-equity correlation might turn positive.

- This is actually the normal relationship, but in recent years, investors have become used to bonds rising when stocks fall.

- In particular, recession-driven stock market crashes lead to a demand for safe-haven assets, which are traditionally government bonds.

- So the price goes up, and the yield goes down.

- When the economy recovers, so do stocks, but bond prices fall back.

- But as bond yields approach zero during the good times, they don’t have far to fall in a crash.

- And so they have a limited ability to protect you.

- And with bond yields close to rates on savings accounts, there’s little incentive for private investors to hold bonds at all.

Alternative assets

The simplest fix is to replace bonds with alternative assets:

- The obvious candidates are gold and cash, or perhaps index-linked bonds

- More adventurous investors might consider:

- other precious metals and commodities in general

- private equity and venture capital

- hedge funds (global macro and long/short equity)

- infrastructure funds and royalty companies

- and even a small allocation to crypto (particularly in combination with gold)

- Even more esoteric alternatives include:

- managed futures/trend-following (or CTA funds in the US)

- multi-factor market-neutral funds (providing exposure to value, size, momentum, low volatility, and quality)

- long volatility -often a simple combination of the JPY/AUD FX rate and gold (both safe-haven instruments).

- Real assets – like property, art and farmland – are another way to go.

- most investors in the UK have too much property exposure through their home (since prices are high)

- if you do choose property, be selective – perhaps choose warehousing over office space and retail

- the other two assets are difficult and expensive to access.

- Older investors, in particular, might also have DB pensions, which act as a bond portfolio without you choosing to own bonds.

Previous posts

In the previous two posts, we looked at five articles on this topic. Interesting points included:

- Bond returns are driven by the coupon (yield) – these are currently low

- Stock returns are inversely related to starting valuations (eg. PEs), which are currently high

- The projected return on 60:40 is now just 3.5% pa

- More esoteric bonds offer higher yields, but also higher correlations with equities

- Factor premia (smart-beta funds) are another asset class to look at

- Patience and diversification are required since no single factor works all the time and many factors underperform for years (eg. value right now).

- So are hedge funds (particularly long-short equity, which is not readily available to DIY investors, and global macro, which is), options and managed futures (trend-following).

- The last two are very much DIY pursuits.

- Stocks prefer falling inflation to rising inflation

- Bonds can be diversifying even with (modest) rising inflation, but as their yields rise, they will lower portfolio returns, so the portfolio is not protected

- Index-linked bonds are less diversifying but will impact returns less

- Commodities and gold have close to zero correlation, but correlations are slightly positive when inflation is rising – they also have good returns, particularly in rising inflation

- More diversified portfolios are more stable under inflation.

- Real estate, PE and infrastructure are not true diversifiers – they depend on positive economic growth (like stocks).

- The diversification effects they show on paper are flattered by smoothed and lagged valuations.

- Managed futures and long vol generate similar returns to bonds (with higher volatility)

- Multi-factor market-neutral generates a lower return than bonds with lower volatility.

- Managed futures and multi-factor have zero correlation with stocks

- Long vol has a negative correlation

- Replacing bonds in a 60/40 with long vol works well – the new portfolio has a higher return, lower volatility and lower maximum drawdown.

- Replacing bonds with long vol, trend and multi-factor also beats the traditional 60/40, though only by a little.

Rethinking 60-40 – Part 3

The threat from inflation is a hot topic at the moment, and only a month after the second post, I already have another five articles to cover.

Disciplined Systematic Global Macro Views

Three of them come from systematic investor Mark Rzepczynski on his blog DSGMV.

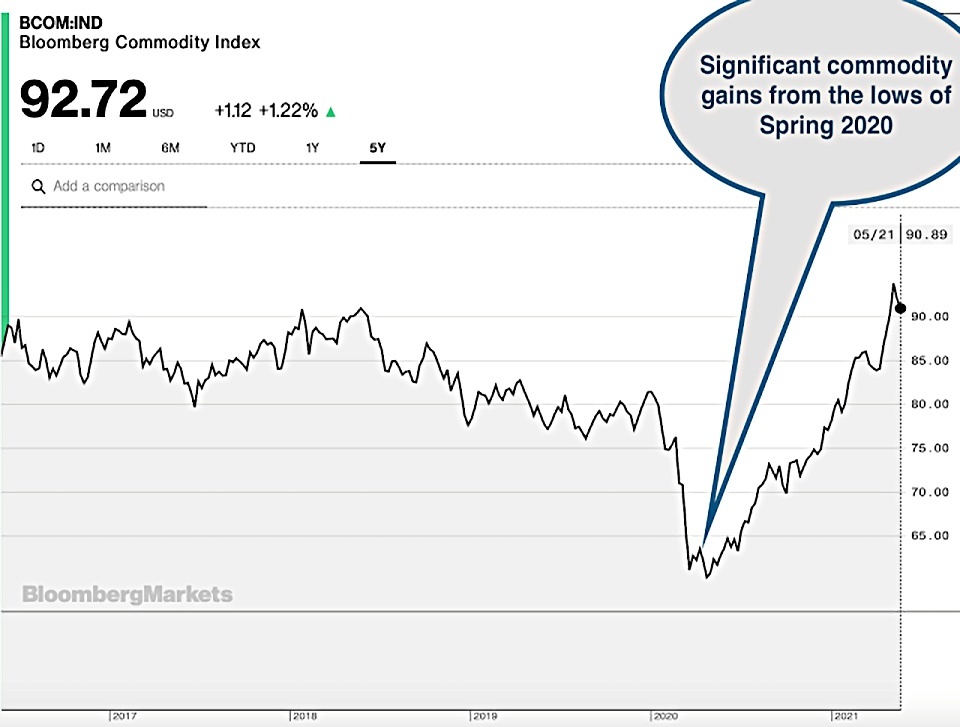

- Mark thinks that it’s hard to go wrong with commodities during inflation decades.

Using any number of strategies would have done well. Whether momentum, basis, value, long/short or long-only, commodities can be a good addition during periods of higher inflation.

Mark notes that we are nowhere near the inflation levels of the 1980s yet.

Nevertheless, the quick pandemic recession coupled with excess money has already created a huge boom for commodities. Whether this will continue is less clear, but the last year has generated explosive commodity upside but may still allow for further price gains.

Thinking longer-term, Mark uses both the 5-year moving average (which has now been breached and is itself moving higher) and production/replacement costs relative to demand.

As prices fall, marginal production is cut and there is the potential for supply and demand imbalances. Low prices solve the problem of low prices – and markets will mean-revert.

Prices are cheap, but there is room for upside and the highs of 2014 have yet to be reached. In an inflationary world, commodities are still a good location for capital.

Mark also believes that momentum and value will help.

Simple value and momentum signals applied to well-accepted benchmarks create improved Sharpe ratios. The benefit of using both value and momentum is through their negative correlation. The combination of both will add more value that using each signal separately.

Man Group

The FT’s Alphaville column featured a guest post from Man Group on how to defend against inflation.

Our research draws on 34 inflation episodes in the US, UK and Japan (using nearly a century of data). The piece also analyses eight US price-level surges over the past 95 years where inflation started from a moderate level and shot past 5 per cent

The latter being the situation we now possibly face. Things are not good for stocks:

The S&P equity market index is likely to get hammered during inflation surges, losing on average 7 per cent in annualised real terms.

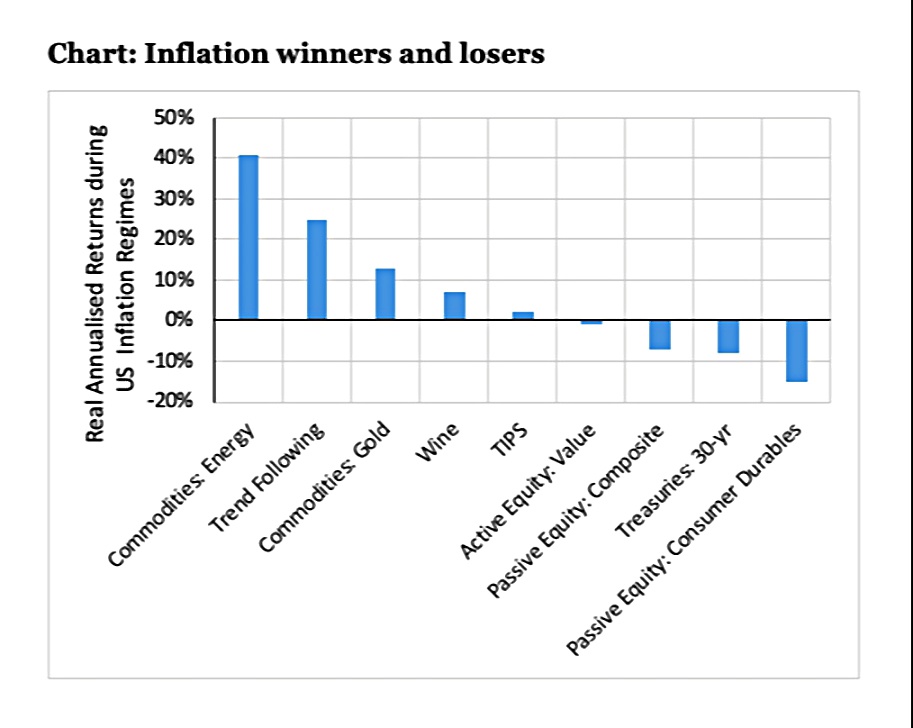

Like everyone else, Man is backing commodities instead:

Commodities have proved a solid historical hedge due. The energy complex has on average returned 41 per cent while industrial commodities have returned 19 per cent – both on a real basis. Gold and silver have also offered low double-digit returns.

Inflation-linked securities also hedge, but given negative starting yields, you need to be prepared to tolerate negative real returns in the absence of inflation – most people would rather not.

Momentum also works:

Time-series momentum delivered a 25 per cent annualised real return during the last eight inflation episodes.

Quality also had a positive return, whilst value was mildly negative after costs.

Energy is the only equity sector with a positive return.

- Health has the smallest negative return, and consumer durables the largest.

Adventurous Investor

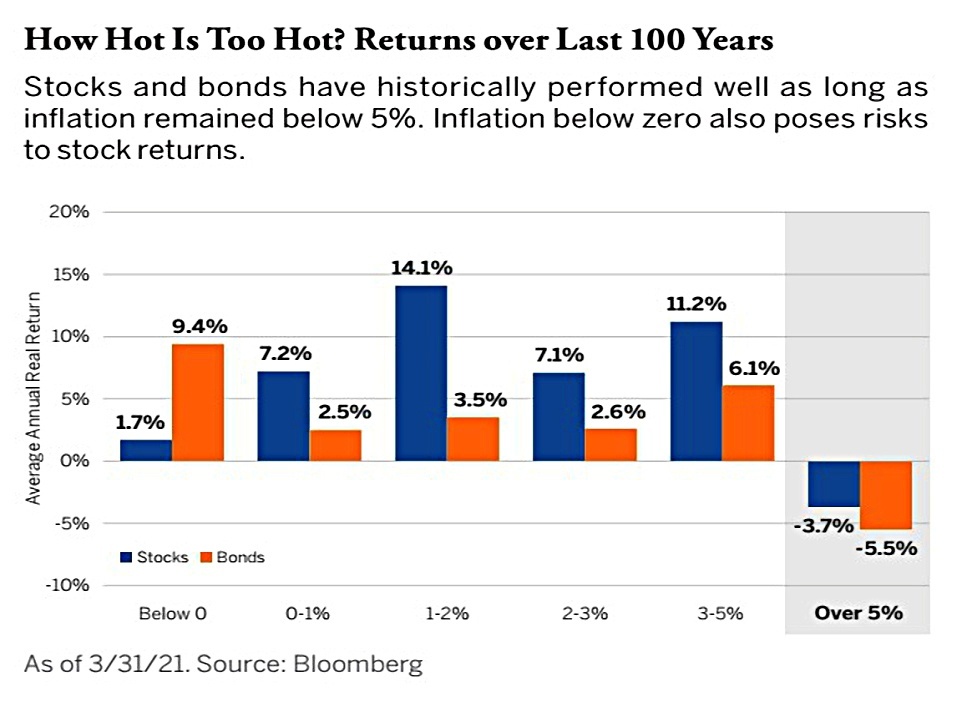

David Stevenson was a little more sanguine about inflation, quoting a Brown Advisory study that shows that stocks and even bonds do okay until inflation gets above 5% pa.

Two other variables matter. Markets don’t like inflation surprises (when rates go up more than expected) and markets also keep a watchful eye on what are called sticky prices (where prices don’t ebb and flow with the business cycle).

Brown favours value and quality as a defence, prioritising stocks that have pricing power.

Conclusions

That’s it for today – the message is the same as last time:

- There’s no “silver bullet” asset that you can replace your bonds with.

But there are plenty of options that you can use together to achieve the same effect.

- Which ones you feel comfortable using is down to you.

I’m a diversification maximalist, so I’ll be using everything that I can get my hands on:

- Cash

- Gold and other precious metals

- Commodities in general

- Private equity and venture capital

- Hedge funds (global macro and long/short equity)

- Infrastructure funds and royalty companies

- Trend-following

- Multi-factor investing (particularly momentum, quality and value)

- Property

- DB pensions

On the maybe/how to list I have:

- Long vol

- Index-linked bonds (if they start to go up in price)

- Crypto

- Art

- Farmland

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

Nice clear graphic from the Brown Advisory study. I guess it was derived from US data. Do you know of a UK analogue?

I am familiar with the second chart extracted by the ADVENTUROUS INVESTOR from the Brown Advisory study and can vouch that UK inflation data is not dissimilar – having previously pulled together such a chart.

I don’t, but I’ve stopped looking for UK versions of US results, particularly when it comes to macro and asset allocation. I haven’t thought of myself as having a UK-focused portfolio for decades (though for practical reasons I am still overweight the UK).

Hear what you are saying.

However the paper behind the MAN group work contains the following interesting snippet on page 19 (see https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3813202)

“Equities tend to perform worst during their own country’s inflationary periods. US equities, for instance, achieve +6% and +9% real annualized return in UK and Japan inflationary periods, compared to -7% in US regimes. The results also suggest benefits to international diversification.

+1 for international diversification, but I can’t imagine running an inflation portfolio in one region and a deflation portfolio in another.

The big issue is the potential reversal of the stock-bond correlation. If there is a significant risk of this, we need to re-allocate from bonds to other stuff. The rest is just noise.

Indeed. And of course maybe this time the forecast inflation period might just be synchronized around the globe.

Other things I noted from the ssrn paper is the evidence base used to calculate some of the asset returns during inflationary periods is at best patchy and they do not in really highlight energy as a ‘special’ commodity either.