Growth Stocks Investor Forum, 21st Jan 2015

I haven’t invested in growth stocks for a decade, having got by since then with sensible asset allocation and directing new funds to passive vehicles. But one of my investing resolutions for 2015 is to get back in, now that I theoretically have the time.

And so I found myself on Wednesday evening in a darkened room with a hundred other middle-aged men. “My name is Mike, and I am a recovering value investor” I wanted to say. “How do you cope with these ridiculous valuations?”

But I remained silent. I was at the growth stocks Investor Forum organised by Equity Development and hosted by law firm Fasken Martineau in their comfortable Hanover Square offices. There were four company presentations to enjoy. ((For reasons of space, I won’t go into too much detail on any of the companies, but if you want more information, let me know and I will put together a dedicated post on the company you’re interested in.))

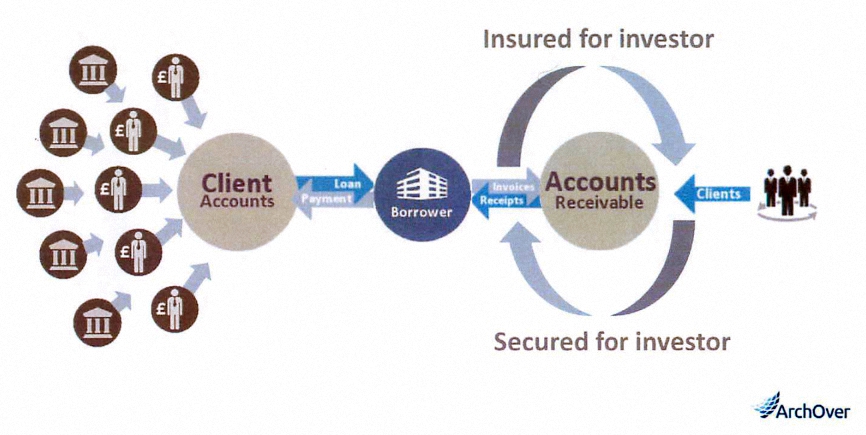

ArchOver

First up was ArchOver, who are not a growth company at all, but rather a P2P lender to business, like Funding Circle and Thin Cats. They are owned by the Hampden Group, an insurance firm. Their USP is taking a charge over the borrower’s accounts receivable and adding credit insurance to provide security for lenders.

Other notable features:

- loans last from 3 months to 3 years

- returns are 5.5% to 7.25%

(or 9%, depending on which part of their pack you read) - there are no fees for investors (lenders)

EasyHotel

Next up was EasyHotel, which clearly is a growth company. They are a budget hotel group, operating 1600 rooms across 20 sites. The majority of the hotels (17) are franchises at the moment, but the model has now changed to owning most of the sites going forward.

Their low prices (£60 a night in London) mean that occupancy rates are high and they should be resilient in recession. They should also hold up against competition from web alternatives like AirBnb. Because of the association with EasyJet (easyGroup holds 56% of shares and 49% of votes) they also have very strong brand recognition for a budget chain.

The business is easy to understand, and is growing, with lots of potential. The only issue for me is the valuation – the PE from the 2014 accounts is around 35, and the forecast for 2015 is 75. The company only listed on AIM in July 2014, so there’s nothing to see in the charts. Pass.

Anite

The third presentation was from Anite. They’ve been around a long time, and are a bit bigger than the kind of company I was expecting to hear from. ((I think they were a last-minute stand-in for a smaller company who dropped out.)) They are now a focused wireless testing group (handsets and networks).

The details of the business are lost on all but the telecoms buff – see if you can work them out from the diagrams – and it’s hard not to worry that the gradual consolidation of networks and handset manufacturers might lead to a shrinking market for their services.

Globally, they claim to have only two competitors (one in Germany and one in Japan). They had decent growth from 2010 to 2012, but have run out of steam a bit and had a difficult year in 2014. They are not cheap (PE of 25) and the charts are poor. Another pass.

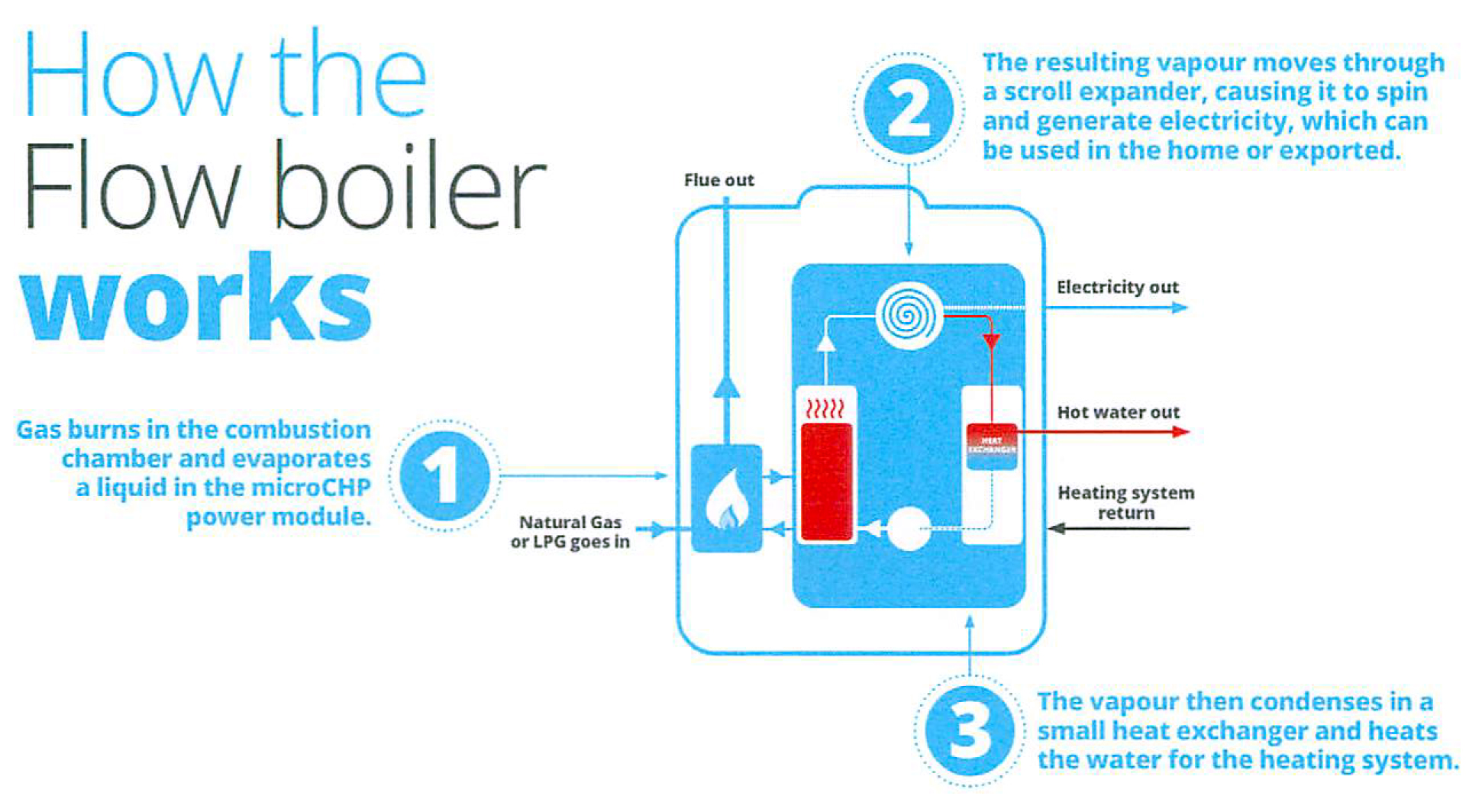

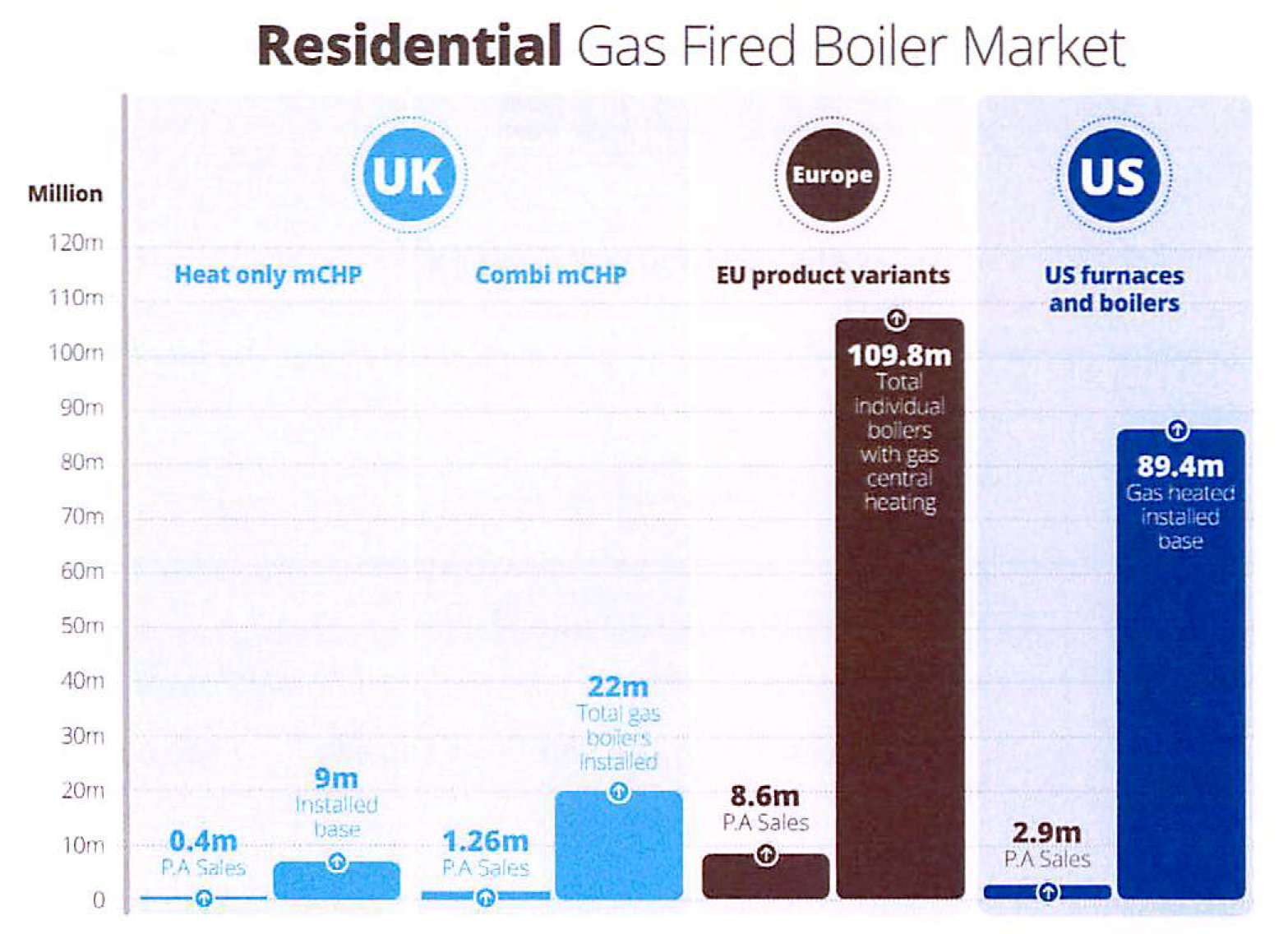

Flow

The final presentation was from Flowgroup. They have been around for quite a few years, but remain a real blue-sky, jam tomorrow growth opportunity.

They listed in 2006, when they acquired the IP for a MicroCHP boiler (a gas boiler that generates electricity as well). It’s taken them eight years to get the thing working, but it finally launches on Monday. In the meantime they have turned themselves into an energy supply company to generate cashflow.

The launch offer will be a free boiler for anyone who switches to their energy supply business. In fact the boiler is financed and Flow pays the finance charges as long as the customer buys energy from them. There’s also an installation charge of £1000+.

Predicted savings are £500 per year, but this includes a feed-in tariff which will end soon. Manufacturing is outsourced, and management believes that they have enough cash to make it to profitability.

The potential market is huge, but getting there will require significant product development. The current boiler is not a combi (it needs a water tank) and too large and powerful for flats. Foreign sales will also required tailored versions. The eight years it’s taken to get this far is not an encouraging sign.

My basic concern is that when the feed-in tariff goes (after less than 40,00 installs, so around 18 months from now), the sales pitch for what is a lovely thing in technical terms becomes a bit like double-glazing or solar panels.

When the boiler is no longer free, the offer is “buy this slightly (we hope) more expensive version of what you need, and make small (£200?) savings each year”. You can save that much by shopping around on your energy supplier, and we know how few people do that.

Then again, what do I know? I thought the iPad was stupid. I guess we’ll know more about how the press and the public react next week.

Longer-term, Flow has big plans to be at the centre of the connected home. If sales of the boiler rocket, I suppose they have a shot at this, but I would expect Google to think otherwise.

I really like the concept of a boiler than generates electricity, but I have my doubts about Flow’s vision of global domination. This may be worth a short-term punt (I can see the share price rising after next week’s announcement) but I don’t think this is a long-term hold.

Conclusions

I deliberately went into the forum without doing any research on the companies involved. I enjoyed the presentation, and the location and timing (5.30 to 7.30) was very convenient.

In terms of finding stocks for a small-cap growth portfolio it was not a great success – I came away with one potential short-term gamble. In terms of getting rid of the rust and hearing face-to-face company pitches it was useful. ArchOver looks to be an interesting P2P operation, but I will wait until I can put my 5% inside a tax wrapper before investigating further.

I plan to go to the next forum, but whether I will be able to resist the temptation to do my research first is another thing. And if there are no fairly priced, true growth companies on the bill, will I make it in the end? In my journey from value to growth investor it’s a case of “so we beat on, boats against the current, borne back ceaselessly into the past.”

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London.

He has been managing his own money for 40 years, with some success.