Weekly Roundup, 3rd February 2015

We begin our weekly roundup as usual in the FT.

Contents

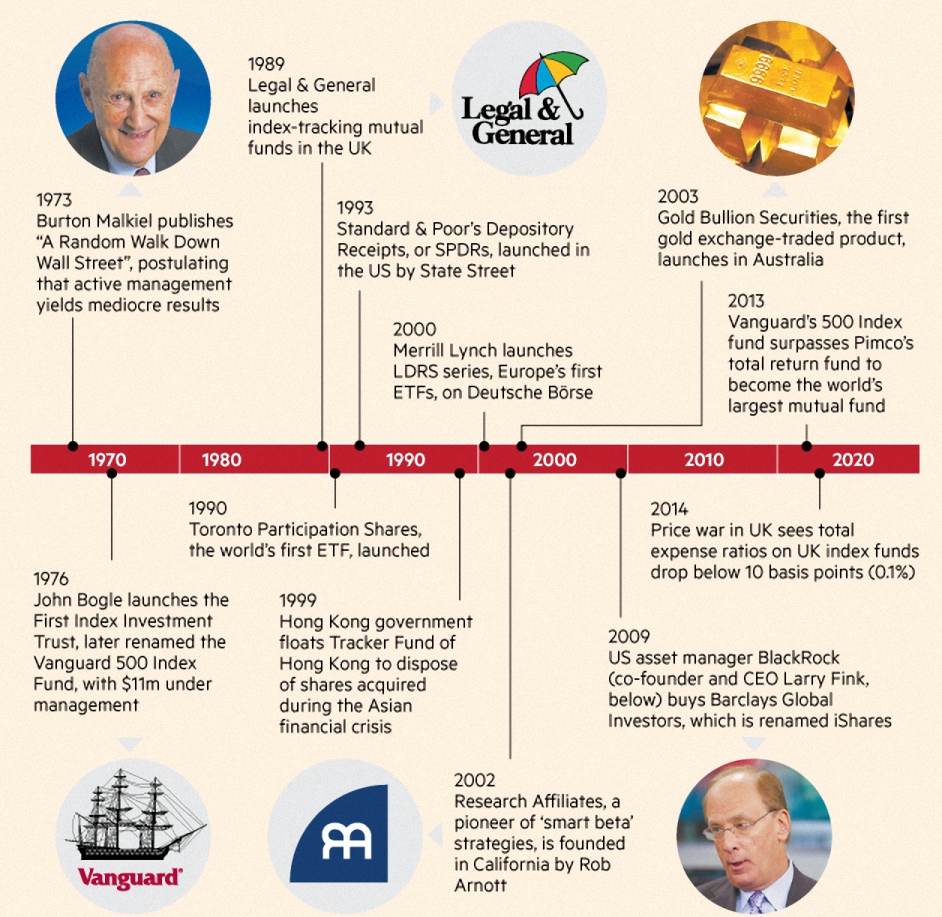

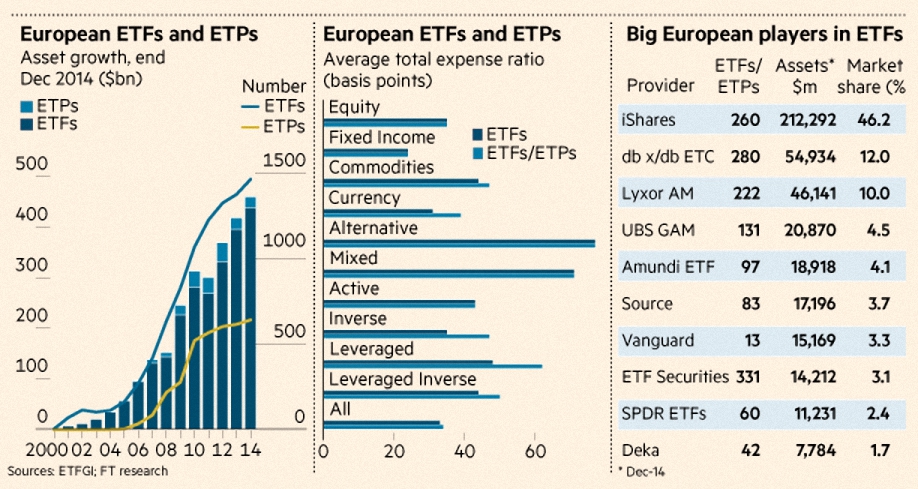

Passive investing

Judith Evans and Jonthan Eley put together a special feature on the impact of passive funds, and ETFs in particular, on small investors. They covered the history of diversified investment products for the masses, beginning with investment trusts and moving through active mutual funds to passive funds to ETFs.

Despite the attraction of lower running costs (typically 25 basis points cf. 75 bp for active funds) and a wide range of underlying asset classes, passive investing is still a small part of the market (10% of assets are in open-ended passive funds and less than 5% are in ETFs). However, growth in passive assets is rapid – estimated 15%+ for 2015 – and consolidation of smaller active funds is expected by many.

But something is stopping the message getting through to new investors. Nick Hungerford of Nutmeg, which offers ETF-based managed portfolios with a minimum investment of £1,000, has been surprised that users of the platform are largely more experienced investors.

Terry Smith warned against the potential divergence of ETF prices from those of their underlying asset during a crisis. ETF providers sometimes create liquidity on an illiquid underlying asset class by using derivatives to generate the index returns and holding investors’ money as “collateral” in government bonds or blue-chips.

The report also touched on smart beta, ((also known as factor investing)) the passive/active hybrid that aims to combine low costs and stock selection by replacing the standard index weighted by market capitalisation, with one weighted by value, size, momentum, volatility or dividend yield.

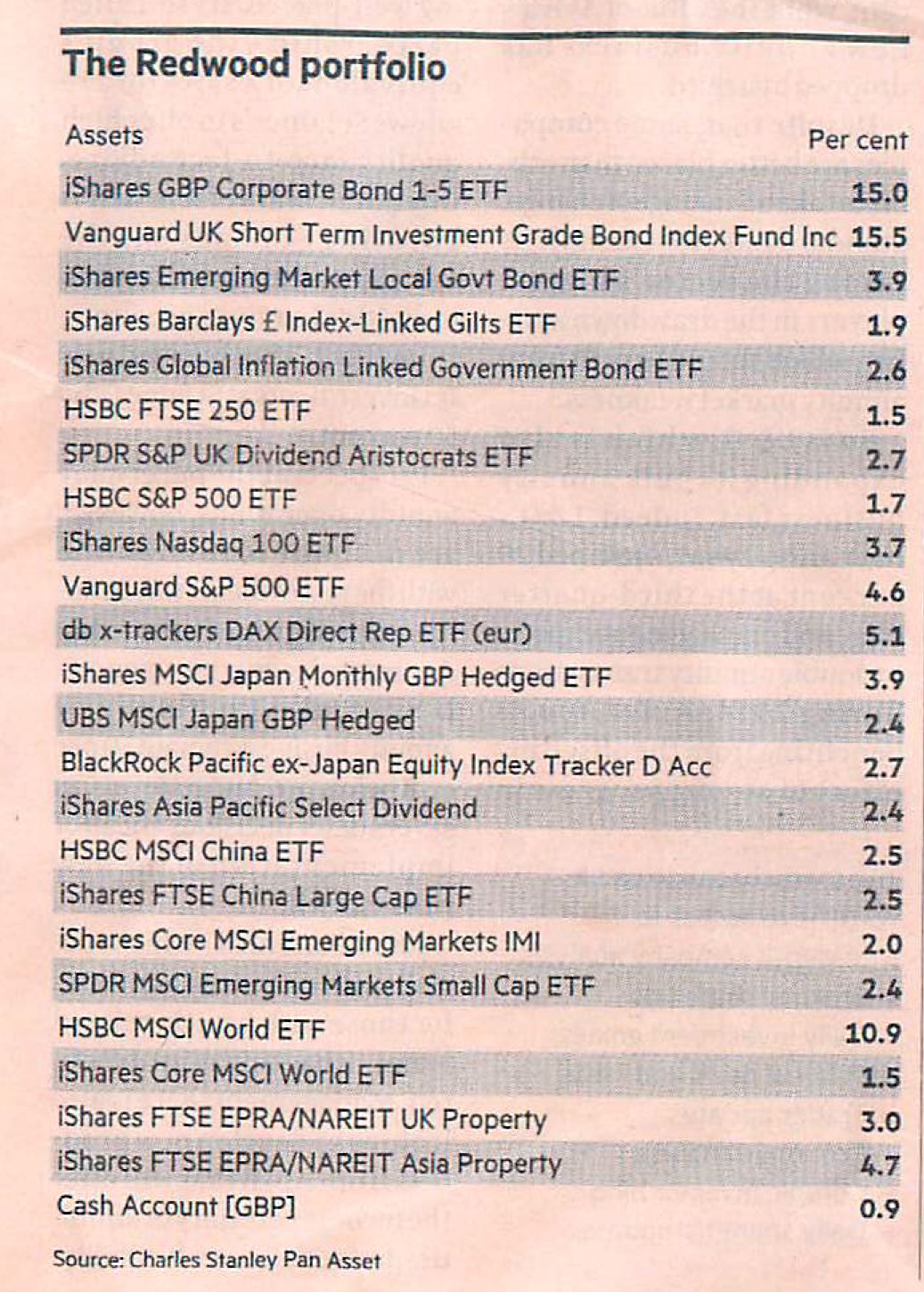

Redwood ETF porfolio

Over the page was the latest update from John Redwood on the model ETF porfolio he runs. Now that ECB QE is finally here, he’s taking profits on US, German and World shares. This will bring down the equity allocation from the portfolio maximum of 60% where it stayed during 2014, towards 50%.

The sold funds are being replaced with a German-dominated currency-hedged Euro fund and a UK Gilts fund (yielding only 2%, and with a weighted average maturity of 15 years). Here’s how the portfolio looks now:

Flowgroup boiler launched

The FT also reported on the poor reception for Flowgroup’s long-awaited combined heat and power boiler, which we discussed in our earlier post on the Equity Development Investor Forum. Shares fell almost 20% after the product announcement.

The boiler costs £3,675 (£4,530 with finance costs included) but should break even over five years. It’s still a lot of money for that “I’m being green” feeling.

Grexit?

![]()

In a couple of articles, the Economist looked at the impact of Syriza’s win in the Greek elections. Grexit is a possibility:

- In 2011 Merkel decided against Grexit since Germany would take the blame, but now it would look more like the Greeks’ fault

- Eighty percent of Greek debt is now owned by other governments or official bodies

- The Finns and the Dutch don’t want to let Greece off the hook

- The southern European governments don ‘t want to encourage their own populist opposition parties

Grexit would probably mean bust banks, capital controls, lower wages, higher unemployment and possibly Greek exit from the EU. It would also stir up trouble in Portugal, Spain and Italy. The biggest loser from a potential Euro breakup would be Germany.

Syriza is correct that austerity is throttling European growth (hence the recently announced QE) and that Greek debt (now 175% of a significantly reduced GDP) won’t be repaid as currently planned. An extension of repayment schedules will be needed at the minimum.

But the proposed increases in public spending in Greece will make the country even less competitive internationally. The price for the debt deal needs to be that the Socialist programme is not implemented. We appear to be some way from this at present.

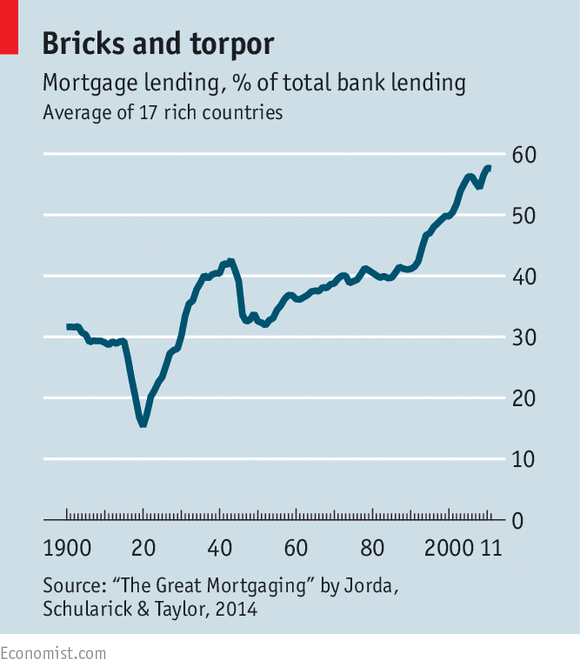

Banks as real-estate funds

Elsewhere in the Economist, Free Exchange looked at a new paper by Oscar Jorda, Moritz Schularick and Alan Taylor on the impact of increasing mortgage lending on corporate loans.

The basic idea in the “circular-flow model” is that banks turn household savings into loans to businesses, helping them to grow. In periods after financial crises, banks are unwilling to lend, impacting growth. But the new paper suggests that the model is out of date: 60% of bank lending is now for mortgages. Corporate borrowing has been flat since the 1970s. Banks are like real-estate funds.

The authors also find that rising levels of mortgage debt are a good predictor of financial crises, and that these crises produce deeper recessions and slower recoveries. Two things explain why banks are keen on such risky loans:

- mortgages are often subsidised (eg. in the US, where interest is tax-deductible)

- Basel I in 1988 deemed mortgages to be half as risky as corporate loans, increasing the effective rate of return to banks

Instead of banks, firms have turned to the bond markets. US corporate bonds are now 70% of GDP, compared to 11% in 1970. This trend is exacerbated during downturns when banks try to shrink their balance sheets.

This may be a good thing in one sense, as corporate default will have less impact on the “real” economy, because losses hit investors rather than imperil banks. But smaller, riskier firms (which are the fastest growing and most technically innovative) will find it more difficult to raise money, and economic growth will slow.

Perhaps there is a role for P2P and crowdfunding here.

Tobin tax

The paper also reported that the meeting of European finance ministers in January had resurrected the proposal for a harmonised financial transaction tax (an FTT or a Tobin tax).

Britain has had stamp duty (0.5%) on shares for centuries. Sweden had one in the 1980s but cancelled it when share-trading moved elsewhere. France (0.2% on shares in French firms larger than €1bn) and Italy (0.12% on shares in Italian firms larger than €500m) have recently introduced taxes.

Volumes in France have not been greatly affected (compared to countries without the tax – the general volume of trading has fallen everywheres since the tax was introduce) but in Italy there was a 20% relative impact.

Britain and Luxembourg in particular oppose the FTT because of their large asset management industries, but 11 countries seem determine to press ahead from 2016.

They are less united on what the tax should cover. France wants to exclude derivatives, where it is strong. Nor is there agreement on whether the location of the issuer, buyer or seller should determine if the transaction is taxable, and who gets the money.

An earlier article from 2009 explained the three problems with a Tobin tax:

- everyone needs to sign up, or trading simply emigrates

- liquidity is reduced, making prices more volatile

- it fails to address the key problems in banking: too much leverage, poor risk assessment and “too big to fail”

Trading volume is a poor indicator of the size, complexity or riskiness of a bank (extra trades are often use to hedge risk, not increase it).

The most recent crisis originated in the highly regulated and high-transaction cost area of US housing. Bubbles inflate despite the tax on the way in. International cooperation would be better directed to cross-border regulation and capital adequacy rules.

Dodging the mansion tax again

In the Evening Standard, Lucy Tobin had more anecdotal evidence that the rich are planning to dodge Labour’s mansion tax. Builders are preparing quotes for house splits. Accountants and solicitors are being hired to work out ways to turn homes into B&Bs or “conference facilities”. It’s the window tax all over again.

Cradle-to-grave savings

In City AM, Conservative MP Mark Hoban argued for the expansion of the new PensionWise advice service into a “Retirement Saver Service.” ((Suggestions on a postcard please, for a snappier title than that)) The idea is to put the saver in charge rather than the provider.

The RSS would have two features:

- a single view of current wealth, aggregating all pensions and savings from whatever source

- tools to help people put together a plan for saving, taking into account life expectancy and risk tolerance

As usual, the Dutch and the Swedes are already ahead of us in this.

It’s a good idea, but it doesn’t go far enough. The key element of the PensionWise service is the face-to-face free impartial advice.

We need to make sure that people regularly sit down and consider their financial situation and work out to get from where they are to where they want to be in the future. This needs to take place at regular intervals from a young enough age for it to make a difference.

Eighteen would be a good place to start – if you’re old enough to vote, you’re old enough to take responsibility for your future.

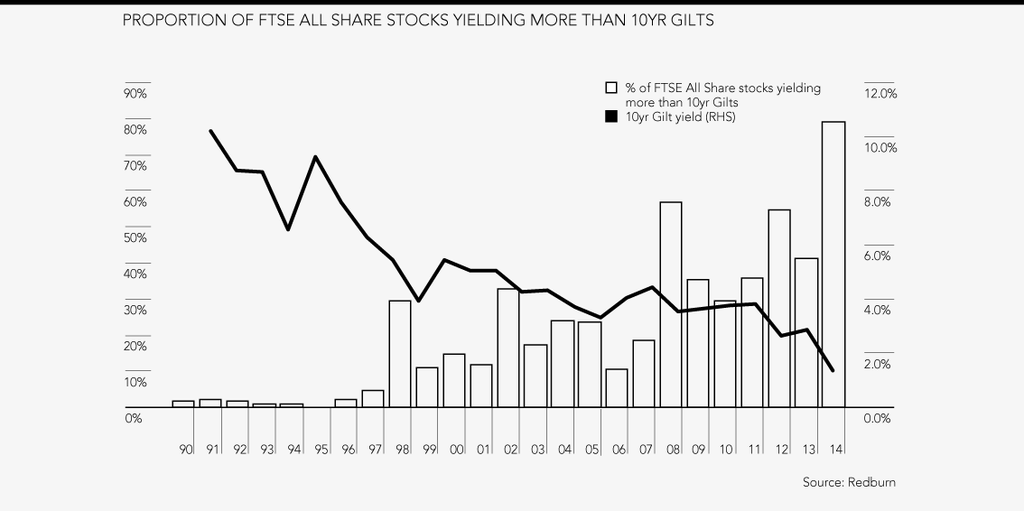

Stocks yielding more than gilts

Finally, I am grateful to JJ IS on Twitter (@CompundIncome) for pointing me at the graph below, which shows that the proportion of stocks yielding more than the 10-yr gilt is at an all-time high (11%). Not that surprising, given that the 10-yr gilt yield is at an all-time low, but I know which side I’d rather be on.

Until next week.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.