NVM VCT Seminar, November 2014

A Venture Capital Trust (VCT) is probably the best tax-efficient investment after pensions and your house. I was a big fan until Gordon Brown’s pension reforms around 10 years ago meant that I could put my VCT money into my pension instead.

As the coalition has brought the ceiling on SIPP contributions down from £200K+ to £40K annually, they once again have some attraction for anyone earning above £85K. Sadly in my semi-retirement I don’t bring in nearly this much.

But I have held on to some of the VCT shares I bought before 2005. They pay a large tax-free dividend, and I haven’t needed the cash up to this point. You also feel as though you are doing some small good turn to British Industry.

Investor seminars are for shareholders only, and as I hold my VCT shares through a nominee account, I only heard about this seminar through a friend. One quick email to NVM to verify my credentials and my invite down to Kings Place was in the mail.

I’ve been to this event before, and it can be very jolly. VCT investors are a cut above the crowd at the usual trade shows, and the private equity guys themselves are a nice bunch. Northern with their regional bias are one of the best outfits in the market, and the free wine and sandwiches are always welcome.

The structure of these events is fairly standard: there’s a review of the past year’s activity and fund performance, presentations by a couple of firms that the fund is invested in, and an overview of the VCT market and the outlook for the next twelve months. And so it proved.

Investment review

First up was Martin Green the MD with a review of investment activity. NVM’s general investment strategy is:

- invest alongside the incumbent management team

- invest across all sectors

- look for growing firms in growing markets

- make bids that are at the low-end of the market

- focus on regional corporate finance opportunities

- for larger deals, the funds invest together with a separate limited partnership owned by NVM

- NVM aims to take 10% market share in VCT deals

In the year to September, the four funds made two exits at a value of £14M:

- £3.4M, a return of 360% from 2004, plus a stake in the quoted company which the holding was reversed into

- £10.6M from an investment of £3.4M in 2000 (400% return – Alaric, of which more later)

- there was also an exit at a loss (30% return)

There were six new investments to a total of £26M (c. 10% of a £220M VCT market), across a variety of sectors and locations. The portfolio now consists of 55 companies (mostly unquoted and a few AIM-listed) with a total value of £151M. Annual returns (dividend plus NAV increase) on the funds ranged between 5.4% and 7.4%.

The outlook for the existing investments is mixed, with the UK looking good (3% growth) but the stagnant euro-zone likely to have significant impact (more than 50% of sales are exports, mainly to Europe). The froth has gone from AIM, so there may be good opportunities in the next year. The threat of tax changes after the UK election may increase deal flow in the run-up.

Bank lending to SMEs remains non-existent, but the Business Growth Fund (BGF) – set up in 2010 with £2.5bn from five banks (Barclays, HSBC, Lloyds, RBS and Standard Chartered) is emerging as a serious competitor, offering better terms than NVM.

New investment – Bouyant Holdings

Joel Rosenblatt, the NVM-appointed Chairman of Bouyant Holdings (on the left in the photo, with MD Mike Aramayo) , gave a presentation on one of the year’s new investments.

Bouyant is a firm in Nelson, Lancs which employs 760 people and makes 95,000 sofas a year. They are the largest independent manufacturer in the UK and are cash generative in a growing market.

Upholstery is a £2.9bn business which forms 30% of the £10bn furniture market in the UK. Sofa sales are more resilient than other furniture and grew even through the pre-2011 declining furniture market.

Bouyant manufacture (and do everything else) in house:

- their sofas are fashion led, so lead times are an issue

- the focus in the UK is on quality, rather than cost as in Europe

- the UK has tougher fire regulations

- transport costs are high relative to sale price

The firm offers 800 options within 120 design “families”, each with a choice of 1000 fabrics. They hold no stock, delivering a sofa the day after it is made. This rapid delivery and wide range is exactly what the customers in their market require.

They have recently moved from being an outsourced manufacturer for two major retailers to being an independent design-led, customer-focused firm. They now sell through a variety of channels from John Lewis downwards, with no channel accounting for more than 15% of sales.

The firm has annual sales of £52M with EBITDA of £4.7M. The deal was done at less than 4 x EBITDA and is asset-backed, allowing the addition of leverage.

[The next two presentations were on VCT regulation and the state of the VCT market, and will be covered in a follow-up post next week.]

Exit – Alaric

Mike Alford, MD of Alaric, presented the story of NVM’s investment in his firm – a thirteen-year journey to a big exit . Alaric offers high performance, high availability payment processing and fraud detection systems. Their biggest client is American Express, who process 500M transactions per month, with peak volume of 2.1k transactions per second.

Alaric make money from licence fees, customisation and support. Most of their competitors use systems that originated in the 1980s (Alaric’s software is Java-based).

The firm first attracted external funding in 2000, but despite winning the Amex contract in 2005, and the subsequent success of that project, they found further progress in the marketplace difficult, and were in crisis by 2007. Only NVM and the management team were willing to invest further. Since 2008 lots of new accounts have been won, and the company became very profitable and cash generative.

In 2010 sector consolidation actually helped Alaric, with some of their best competitors being taken over by inferior firms. By 2013 they were one of the few independents left, and commanded a higher valuation. The final sale to NCR was in December 2013 at £52M (5 x revenue) with the NVM return being 400%.

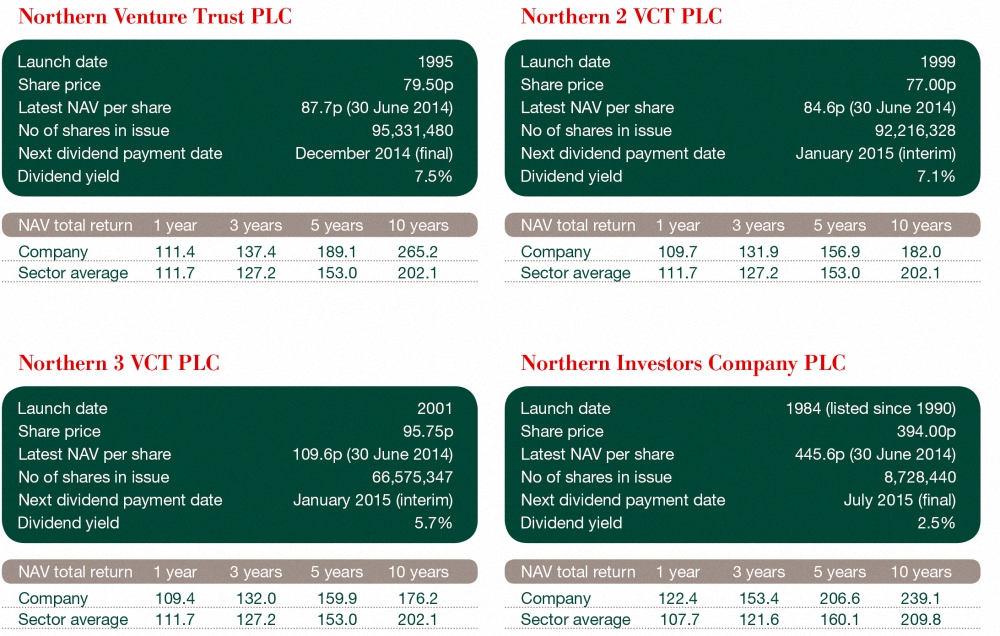

Fund Performance

Tim Levett, the Chairman of NVM presented the performance of the four funds (see table below). Alongside the steadily increasing NAV and share price, I would like to highlight the high yields (5.7% to 7.5%) of the three VCT funds.

These dividends are tax-free even to those who buy the shares in the secondary market (annual turnover in the shares remains low, at around 5%). Annual allowances for tax shelters in the UK are so generous now (£55K per person across SIPP and ISA) that few private investors will need to keep money outside them, but for those who do, these returns will be hard to beat.

NVM are not raising funds this year, having raised £50M last year and invested only £26M of it. There are also further realisations looming.

Q&A

Tim stayed on to moderate the Q&A session.

- Would consolidating the funds increase liquidity in the secondary market? NVM feel that low liquidity is primarily due to the primary market (with it’s 30% tax relief) satisfying demand. Consolidation would be expensive, with at least an 18-month payback period.

- What changes in regulation are anticipated? The EU would like to restrict “state aid” (which it deems to include tax-incentivised venture capital) to companies which are less than 7 years old.

- What changes would NVM like to see? Relief from inheritance tax, investments split between equity and debt, and an increase to the annual investment limit per company.

- Why not increase the pay-out rate and raise more money (with 30% tax relief)? NVM has a policy of maintaining or growing the net asset value and paying a true dividend, and this is unlikely to change.

- What would be the impact of a Labour government? The indications are that Labour would support the current regime, which has been in place since 1995, largely under Labour.

The presentations had now been running for more than two hours, and we adjourned for refreshments. After a serviceable buffet and a few glasses of “free” wine ((I realise that as a shareholder I was paying for it myself, but it never seems that way at the time)) my contribution to British Industry seemed once again to be a win-win situation.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.