Process – Excess Returns 8

Today’s post is another in our series on the lessons to be learned from guru investors. It’s about Process Errors and how to avoid them.

Contents

Process Errors

Nothing sedates rationality like large doses of effortless money. Normally sensible people drift into behaviour akin to that of Cinderella at the ball. They know that overstaying the festivities – continuing to speculate in companies that have gigantic valuations – will eventually bring on pumpkins and mice.

But they hate to miss a single minute of what is one hell of a party. They all plan to leave seconds before midnight. But they are dancing in a room in which the clocks have no hands – Warren Buffet (in 2000)

In Chapter E of his book Excess Returns, Frederik Vanhaverbeke looks at process errors and how to avoid them.

- Many of these errors will be familiar to students of behavioural finance, since they often have a psychological basis

- Frederik’s other theme is the uselessness of non-fundamental company data, in particular price action and economic numbers (( Note that I don’t agree with him here – both can be useful in the right circumstances ))

[amazon template=thumbnail&asin=0857193511]

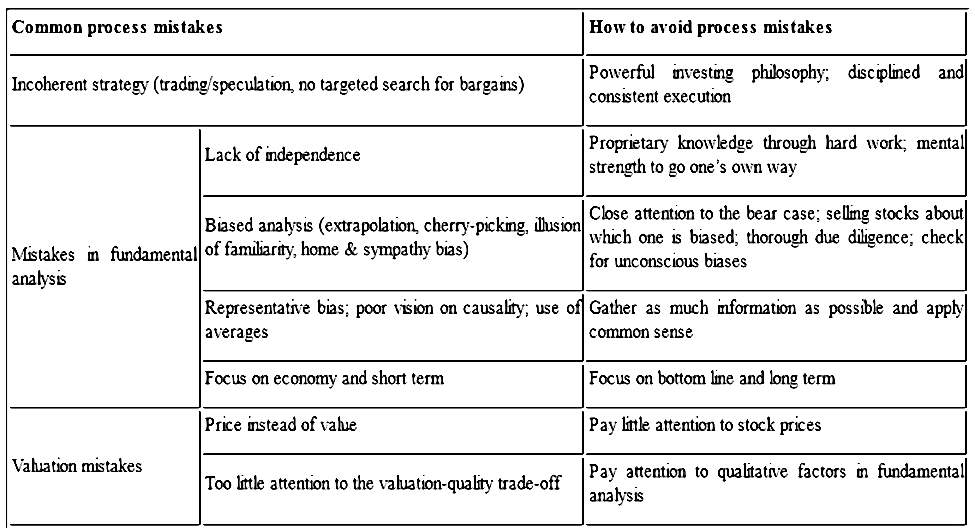

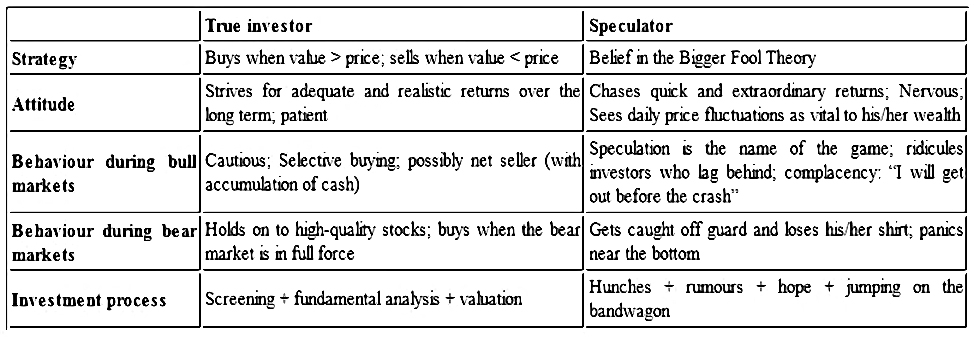

In the grand presenting tradition of “tell ’em what you’re going to tell ’em, tell ’em, then tell ’em what you’ve told ’em”, I will start (and end) with Frederik’s summary table:

No process

The most common mistake is not to have a process at all – it’s certainly the mistake I come across the most.

- Lots of people buy stocks they don’t know much about based on tips or things they’ve seen in the papers or on Twitter.

They may understand that you buy cheap stocks and sell expensive ones.

- But they don’t really know how to work out if a stock is cheap

- And they probably don’t have the patience to hold on until it becomes expensive.

The easy availability of investing information leads to overconfidence and the illusion of being in control.

- Things get even worse on the back of a winning streak.

You have to know what you own, and why you own it. ‘This baby is a cinch to go up!’ doesn’t count – Peter Lynch

Trading vs investing

Frederick’s definition of the two is based on whether you invest from intrinsic value (fundamentals) or trade on price action (technicals)

- Some people combine both, but not many, and even these tend towards trading by not using the intrinsics / fair value concept.

- I fear that I fall into this category.

Another investor who does this is William O’Neil of CANSLIM fame.

- He looks for fundamentally strong companies with good price action, using momentum signals to buy and sells.

Frederik has issues with investors integrating trading concepts into their process:

It makes no sense for pure value investors to use stop-loss orders for long positions.

Stop-losses get traders out of positions where the price action disproves their thesis.

- But for real value investors, the fall in price makes the stock more attractive.

- They might even buy more, whereas in fact you should never average down.

Personally, while I agree with the underlying philosophy, I prefer to reallocate my capital from a falling stock to a more attractive situation.

- So for me it’s more a question of timescale

- I rarely track the price of my long term-holds, but like to get out quickly from short-term positions (say less than a year).

He’s also against pyramiding up (buying more when the prices rises).

- I am quite likely to do this when momentum trading.

- Because the trend is likely to continue.

Value investors see a price rise as taking the stock closer to its true value, and so will more likely be looking to sell than to buy again.

Speculation

Even lower on Frederick’s food chain than traders come speculators. These are people:

Playing the markets based on hunches, rumours, hope and wishful thinking. Their only goal is to unload their stocks on unwary buyers at a price above their own purchase price.

This is the Greater Fool approach:

- It doesn’t matter what price you buy at so long as there’s a bigger fool to sell the stock to – for even more money.

- This style is common at the bottom end of the AIM market in the UK, where lots of share ramping and de-ramping (“pump and dump”) goes on.

Frederik also includes buying stocks in anticipation of a takeover, and buying expensive stocks during a bubble.

I think I have a philosophical difference with Frederik about this.

- I’m somewhat unusual in that I like to mix up a lot of different investing and trading styles, because I believe that no one style is best under all conditions.

- So there will be times when I am momentum trading, and times when I buy expensive stocks in a bubble.

Frederick is correct to say that

Although speculation can be rewarding over short periods of time, it seldom pays off over the long term.

So the correct approach is not to speculate over the long-term, or at all times.

- Instead, Frederik appears to be saying that we should never speculate.

Note that I’m not suggesting that it’s easy to know when to quit.

- Rather, that it’s entirely possible that quitting slightly late will still leave you ahead of the people who never got involved in the bubble at all.

Looking in the wrong places

The average investor doesn’t screen for bargains, but simply “analyses” stocks they accidentally bump into.

- As we found in earlier chapters of the book, lots of investors like “hot” stocks and “familiar” stocks.

- We go for firms whose products we like, those in the industries in which we work and even those that are located close to us.

Independence

It’s vital to form your own opinion about a stock, yet most investors rely on broker notes, newspaper tips, Twitter buzz and the opinions of friends and family.

- We know from our posts on Behavioural Investing that analyst forecasts are poor.

Frederik speculates that is partly down to the egos of the smart people involved:

- they can be overconfident, and less willing to change their minds – but it’s also clear that

Making forecasts about the economy or about a company’s sales and earnings is extremely hard.

There’s also bias involved:

- The job of sell-side analysts is to generate commissions by encouraging investors to turn over their portfolio.

And because these recommendations are public knowledge, in general they will be “in the price” by the time the retail investor can act.

- The same applies to tips in newspapers and magazines, and to attempts to follow the moves of star investors.

The press wants views, clicks and circulation-boosting sales, and will do what it needs to maximise these.

- This leads to sensational stories with a short-term focus, from larger than life characters, rather than actionable long-term investment advice.

- There’s also a bias to making rather than preserving money.

No one ever attained a fortune by seeking the advice of others – David Carret

Bias

Investors suffer from cognitive biases, and in particular the tendency to look for evidence that confirms their investment thesis, ignoring disconfirming evidence.

- As we saw previously in a post on Behavioural Investing, this is the opposite of best practice.

Other things to avoid are:

- Extrapolation

- While last year’s numbers are probably the best predictor of this year’s, earnings and sales will fluctuate, and the numbers that have the biggest effect on prices will be those that are off-trend.

- Cherry-picking

- Investors overweight recent and emotional data (a personal experience, or a CEO they admire).

- Familiarity, sympathy and home bias

- Be careful not to overweight companies whose products you like, or those based near you.

- And the same goes for your employer, or other companies in your industry.

Probabilities

Most investors are bad at statistics and probability:

- They draw conclusions from too few events, that are not statistically significant (eg. sales at the local branch of a chain).

- They confuse correlation with causality, or reverse the causality.

- They use historic averages to predict future events (eg. the length of a bull market).

The wrong factors

Frederik lists the key distractions in analysis:

- Macro-economics, which should be mostly ignored by bottom-up value investors.

- The short term (next year) rather than the long-term (several years).

Price

Frederik is not a fan of using price in your process. He lists some common mistakes:

- Thinking that stocks with low prices ($3, or 30p) are cheap and those with high prices ($100, or £10) are expensive.

- This is quite common with beginners, but surely not part of many experienced investors’ processes.

- Thinking that a price rise over the past five years means a stock is now expensive.

- Thinking that a trading range for the past few years is “fair”.

- I half disagree here – the range may not be fair, but it is likely to persist, and when the stock price breaks out of it (up or down) that move is likely to be significant.

- This means that at the low end of the range, the stock is attractive (in the short-term) and at the upper end it is expensive (in the short-term).

- I accept that this is a form of anchoring, but if the market consists of people who are anchoring, that will be a factor in price movements.

- Anchoring to your purchase price as a “fair” or “good value” price.

- Many people won’t sell below their purchase price, whereas in fact you need to cut your losses (I say).

- At the same time, Frederik thinks that a true value investor shouldn’t sell just because the price has fallen.

Value versus quality

Frederik also warns against placing too much attention on multiples (PE ratios):

- Lots of stocks deserve a low PE because they are rubbish.

- Some investors overpay for quality, regardless of a high PE.

- The connection between the success of a business and its stock price fluctuates.

- Few stocks other than the smallest can grow by 15% pa over a decade or more.

- To beat this rate of return you need to buy exceptional companies at a discount to their intrinsic value.

Our goal is to find an outstanding business at a sensible price, not a mediocre business at a bargain price – Warren Buffett

Avoiding mistakes

It’s time for Frederik’s summary table once more:

- If you don’t have a coherent strategy, get one and stick to its rules

- To maintain independence, cut out the noise

- Some top investors (eg, Buffett) are located far away from the markets

- To counter psychological biases, pay special attention to the bear case (or if you are planning to short, the bull case)

- always look for information that disproves rather than confirms your investment thesis

- sell those stocks where you become aware that you are biased / attached (or indeed, simply “spring clean” your portfolio on occasion)

- Limit your attention to (changes in) stock prices

- don’t check your portfolio every day

- frequent checks lead to the identification of spurious patterns and to anchoring to historical prices

This has been an interesting chapter for me.

- Until now I’ve found Frederik’s book fascinating, but his rigid adherence to a very narrow definition of what constitutes investing felt claustrophobic to me.

- Despite that reservation, there’s a lot of good stuff here, albeit that we have covered much of it previously, under the headings of psychology and behavioural investing.

I’ll be back in a few weeks to look at the next chapter of the book, which is about stock types.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.