Social Discount Rates

Today’s post looks at social discount rates.

Contents

Social discount rates

Social discount rates (SDRs) are used to value costs and benefits in the future in order to make policy today.

- They are a hot topic right now because of climate change.

The SDR is one of the most important inputs to a long-term cost-benefit analysis (CBA), because a small change in the SDR can produce a bug swing in the current value (the NPV).

With a low SDR, impacts in the distant future have a high price today.

- With a high SDR, you can pretty much ignore them.

So which SDR should we use?

Consumption vs investment

CBA uses two discount rates, one for consumption and one for investment.

- investments are expected to produce a positive and compounding return

The consumption rate reflects the willingness of people to swap a “unit of consumption” in the present for a similar unit in the future.

- This represents the degree of time preference, and in aggregate is represented by the risk-free rate (see below).

The investment rate should be higher than the risk-free rate (since investors want a return).

- Thus taxes drag returns on projects that could be useful to society below the hurdle rate required by business.

It is important to note, however, that the SDR is the (lower) consumption rate.

Why use an SDR?

Taking a step back, why use an SDR at all?

- The financial reason is the time value of money – money in the future is not worth as much as money today.

This is the proverb “A bird in the hand is worth two in the bush”.

- It’s also known as time preference.

Some people object to this logic because when applied to social problems, it values future (hypothetical) people lower than the present generations.

- This is ethics, not finance.

The second reason, which is less widely controversial, is that society is expected to be richer in the future (even after allowing for inflation).

- This again means that a pound today is worth more than a pound in the future.

And again, this has the inconvenient result that future generations are worth less.

Another argument used in favour of low rates (or no rates at all) is that the consequences of, say, catastrophic climate change, are so severe that no matter how low the probability of them happening, they weigh very heavily in any cost-benefit analysis.

- This is hogwash.

People face low-probability personally catastrophic events every day (car and plane accidents, for example).

- Applying the climate change logic would mean never leaving the house (and wearing a crash helmet indoors, to guard against falls).

In investment terms, it would mean keeping all your money in cash savings accounts, guaranteeing poverty in old age.

A final argument made against SDRs is that people only show a positive time preference when they are alive (to do more would be impressive).

- Because of this, we should not use time preference for issues with intergenerational consequences.

But then again, those of us who are alive are the ones who have to decide how best to allocate resources.

- The intergenerational argument is more ethics and more hogwash.

Declining SDRs

Some people try to get around this by using SDRs that decline as we move further out into the future.

- The underlying argument is that future growth is uncertain.

There is some logic in this.

- When there is a range of possible discount rates, the “certainty-equivalent discount rate” will be closer to the bottom of the range, and the longer the time horizon, the closer to the bottom of the range it will become.

So there is an argument for using a rate that declines from the middle to the bottom of a plausible range of values.

A similar argument can be made through the lens of expected utility as a risk-averse investor will use a lower discount rate as the time horizon (and uncertainty of future growth) extends.

When it comes to climate change, some people would go further than a declining SDR and argue that de-growth is necessary to save the planet.

- For these extremists, it might be possible to justify a negative SDR.

It certainly looks likely that the huge cost of decarbonising the global economy over a relatively short period of time (25 years) will impact growth rates.

Real-world discount rates

Many people manage their lives without ever worrying about discount rates.

- They live in the present and don’t worry about things that might happen to them many years from now.

Others (including climate doomers) are obsessed with things that haven’t happened yet (and might never happen).

- Ironically, there’s a big overlap between these two groups.

Finance types think about discount rates a lot.

- Any investment (or project) with cash flows that carry forward into future years can only be properly evaluated via discounting.

The starting point for a discount rate is the risk-free rate – the return on a risk-free asset (usually a US Treasury bond) of similar duration to the project we are analysing.

- For reference, the 10-year Treasury yields 4.67% at the time of writing (and the 10-year Gilt yield is 4.37%).

I use this rate as one of the inputs into my valuation of my DB pensions, which promise cashflows for the next 20 to 40 years (I hope).

- So is 4.5% a good SDR?

Actual rates

The long bond yield works for me, but most economists would prefer a rate closer to 2% pa.

- A survey of philosophers – apparently they are experts on (intergenerational) ethics – came up with the same number.

But academics are notoriously left-wing, and a 2% SDR means a lot more money for climate change remediation.

- So they would say that wouldn’t they?

Politicians, who have to spend the money now, and get it past the electorate, might disagree.

It’s also worth noting that, until recently, the bond yield was below the rate preferred by the professors.

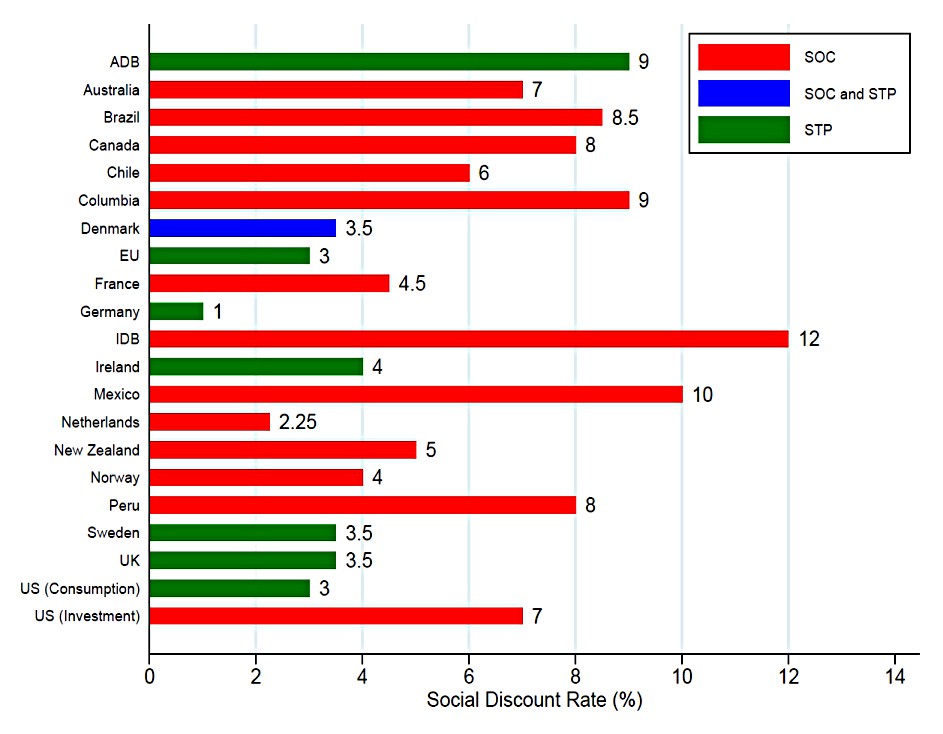

The actual rates in use vary widely.

- The UK uses 3.5%, which is not terrible, but Canada uses 8% and Australia 7%, as does the US (for investment – but only 3% for consumption).

Grantham on short-termism

More than a decade ago, in the FT, Jeremy Grantham weighed in on the short-termism of capitalism:

Let us say that a firm’s current actions are going to cost society at large a billion dollars’ worth of harm in 50 years. Further, let us agree that all of the costs will definitely be imposed on the company. The company would feel that pain today as equivalent to only a mere $1 million hit to earnings [using a 14% discount rate from the 1990s].

Interest rates were already at 2% when Grantham was writing, and set to fall further, but the embedded principle is valid.

- Individuals use much lower discount rates, say 1.5% for real wage growth, and certainly less than 4% real for investments.

I don’t have any wages, but I tend to use something between the bond yield and the failsafe return on a diversified portfolio (around 3.3% pa).

The billion dollar pain at a 4% discount rate is going to feel to the average citizen, who faces the bill in 50 years, not like $1 million, but like $100 million.

But he goes much further:

Shouldn’t the value, and hence cost, of a child’s life in 50 years be identical to the value and cost today?

For me, the answer to that question is clearly no.

- The certain present is more important than the uncertain future.

We’re just trying to decide by how much.

Grantham has a parable which he calls “The Farmer and The Devil”:

A good capitalist farmer had to sign a contract in which the Devil guaranteed a quadrupling of the farmer’s income through very aggressive farming practices at the hidden cost of 1% a year of his soil.

The farmer would enormously profit and eagerly re-up through the first several 20-year contracts only to end up with no soil, no food, and no people at about 100 years out.

I’m no fan of short-termism, but there are two problems with this:

- the soil erosion is hidden

- if the cost were known, it might make the expected value (or utility) of the contract negative (at the appropriate discount rate)

- if the farmer’s time horizon is less than 100 years, he is entitled to spend down his pot of soil

- he has no obligation to sell or pass it on after that

The parable is framed as the tragedy of the commons, but this soil belongs to the farmer.

Conclusions

I think that people who argue for an artificially low SDR have an agenda, even if it’s nothing more than climate change being their new religion and source of meaning in life.

- Looking at things with a financial hat on suggests an SDR between 3% and 4% pa.

Which is precisely what we use here in the UK.

- Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.