Capitalism for Everyone

Today’s post looks at a new report from Joachim Klement called Capitalism for Everyone.

Contents

Inequality

Joachim notes that criticising capitalism has become very popular.

The standard argument is that inequality is now so large, and growing every larger, that capitalism must collapse.

- The Top 1% (however that is defined since – for example – the top 1% for income will not be the top 1% for net worth) has a growing slice of the pie.

It’s hard to argue with the wealth generated by entrepreneurs, or even with those who grow their inheritance.

Successful families ensure that wealth is stewarded across many generations and children and grandchildren don’t become spoilt trust fund kids. Instead, every generation has to contribute to society and the family business. But not all families are that enlightened.

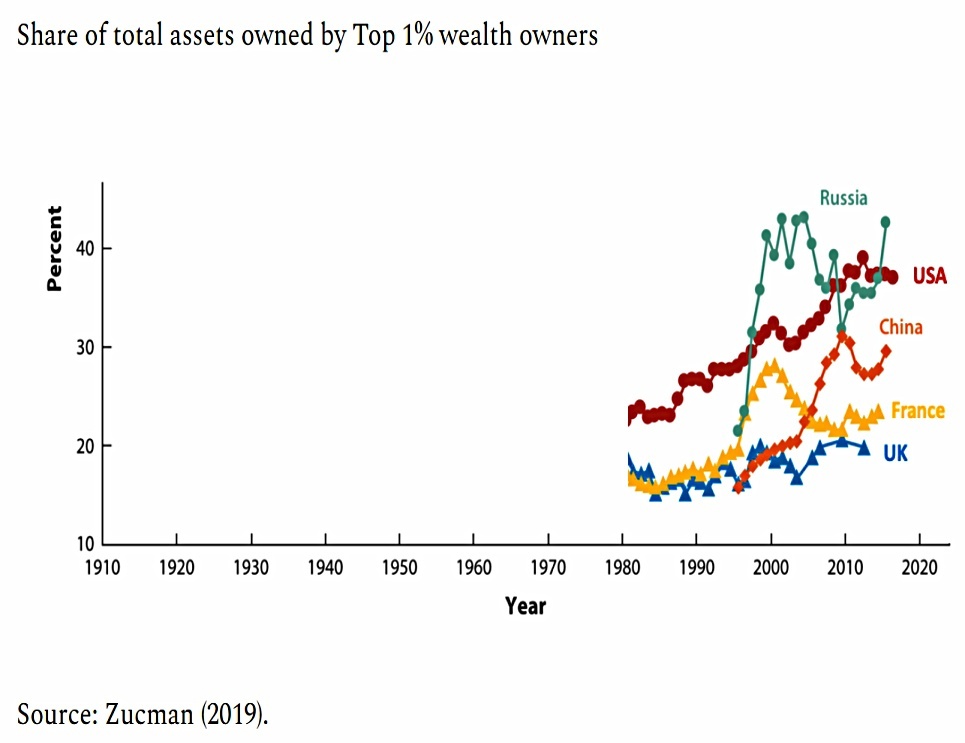

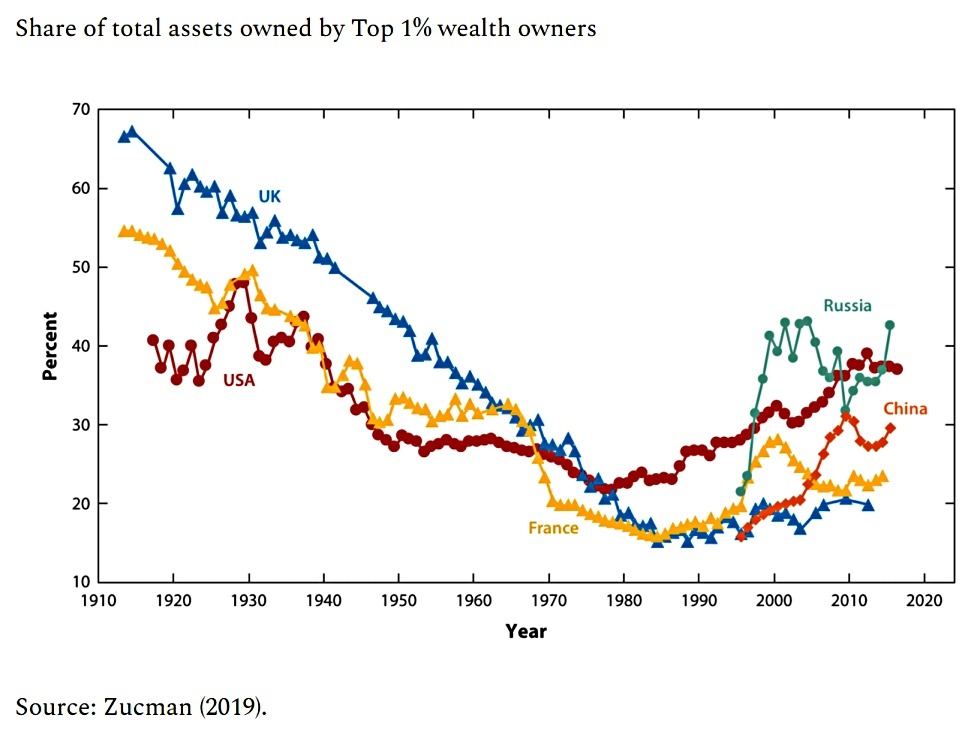

Getting back to the 1%, if you start the chart from 1980, the inequality trends do look worrying.

- But if you go back to 1910, we can see that inequality has been much higher without capitalism imploding.

There was a revolution in Russian, but capitalism in the UK, US and France survived unscathed.

The decline in inequality in the US was driven by the Great Depression, the break-up of trusts under President Franklin D. Roosevelt and the introduction of an improved social safety net as part of the New Deal.

In France and the UK, the decline in inequality was driven by two devastating world wars and the loss of Empire.

Joachim notes that the only things that reduce inequality are bad shocks: war, revolution, natural catastrophes (earthquakes and volcanic eruptions) and plagues.

Peaceful social reform or increasing educational attainment have almost never been able to provide a lasting decline in inequality.

Returns

The current driver of inequality is the “excess” return to capital above the real risk-free rate (which is itself at historic lows).

- We can argue about how big this gap should be, but it seems to me that unless there is a reward for taking on risk, we would all take the risk-free return.

And if the gap is positive, then inequality is likely to increase, since the rich own risky assets, and the poor do not.

- Until we reach a breaking point.

I am afraid history tells us that at that breaking point, things will become very ugly indeed. Luckily, history also indicates tat this breaking point may well be decades away.

Globalisation

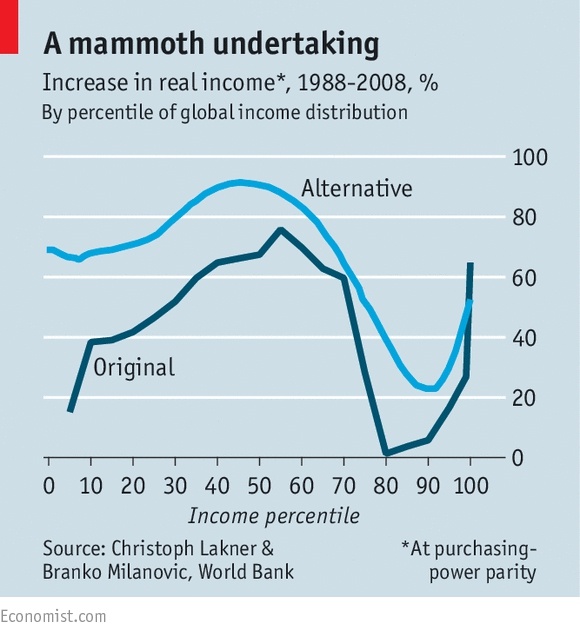

It’s also important to note that since 1980 – the “bad” part of our original chart, capitalism has (largely via globalisation) lifted billions of people out of poverty, particularly in Asia.

- Global inequality has fallen, even though inequality within particular countries has increased.

In the history of mankind, nothing has created more wealth, health, and wellbeing than capitalism.

That said, the economic system in the US particularly does seem to have become less inclusive over the same period.

Joachim is German, and he’s a fan of the German system:

In Germany, by law, workers have to have representation on the board of every company above a certain size. And that doesn’t lead to these worker representatives constantly blocking progress or painful cost-cutting measures. It leads to a better understanding and increased cooperation amongst different stakeholders.

To me, this seems too good to be true.

- If the workers aren’t thwarting the management to some extent, what is the point of them sitting on the board?

Joachim backs up his argument with strike data, which shows that Germany has one of the lowest strike rates in the world.

Capitalism for everyone

Joachim’s new paper was written with his friend Michael Falk of Focus Consulting Group (( I couldn’t find a picture of Michael )) and is available on the CFA Institute website.

Michael S. Falk, CFA, is a partner with the Focus Consulting Group. He has been a chief strategist on a global macro hedge fund as well as a CIO in charge of manager due diligence and asset allocation for a multi-billion-dollar advisory.

The two key recommendations from the report are:

- A move from shareholder value to stakeholder capitalism, and

- The use of sovereign wealth funds to drive a more inclusive form of capitalism.

Externalities and the agency problem

The paper starts with a famous quote from Milton Friedman:

There is one and only one social responsibility of business—to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception or fraud.

I realise that this puts me in a dwindling minority these days, but I’m rather attached to that definition.

- It dovetails with the agency problem, that the managers of the company are not usually its owners, and their interests are not naturally aligned with those of the owners.

A simple goal such as maximising shareholder value can underpin that alignment.

- Shareholders also have less legal protection than debtors and employees should the company collapse, and so it makes sense that their objectives should be prioritised.

Shareholder value can still be compatible with an approach to dealing with externalities (such as CO2 emissions) via a pricing mechanism.

- And the pricing of such externalities would naturally fall to the government.

Stakeholders

If externalities are priced, shareholder value might appear to be rehabilitated. But there are other issues:

- Long-term deleterious effects on customers

- Who should pay for the long-term health consequences of cigarettes, or fast food? (( It might also be the case that the shortened lives of customers lead to net lifetime healthcare savings ))

- The optimum level of pay for employees

- And for the employees of suppliers

- Required infrastructure support from the local community

- Is this covered by increases tax receipts, and should jurisdictions compete for new company locations?

- Employees who are also shareholders might be conflicted

- Shareholders will wish to maximise the value of their portfolios, not of a single stock/company

The authors see four questions for companies:

- Do businesses wish to take responsibility for all their costs, including externalities?

- Do they know what those costs are?

- Can they afford them through their current revenues or potential price increases?

- Would potential price increases be accepted?

Those questions can be answered only by including the stakeholders in the information flow and decisionmaking process.

Jensen

The authors move on to Jensen’s “enlightened shareholder value maximisation”.

- They reject his idea that optimisation for multiple simultaneous goals allows management to avoid accountabilities and exploit stakeholders (I am less convinced).

But they agree that society benefits most if the long-term total firm value is maximised.

- This happens when the corporation produces goods and services valued highly by customers (after taking into account externalities and monopolies).

Stakeholder value maximisation

The next section of the paper looks at various attempts to implement stakeholder value maximisation, in the UK and Germany.

As discussed above, the authors like the German system, which leads to low-ish levels of strikes. But they concede that it might not work for all:

The German model of stakeholder participation is probably not implementable everywhere

because of cultural differences and a lack of trust among different stakeholders.If a company has paid bare minimum wages to its workers for decades and exploited its employees and suppliers wherever possible, giving them a say in the supervision of management is likely to result in retribution rather than collaboration.

That certainly feels like a risk to me.

Sovereign wealth funds

The authors are also keen on sovereign wealth funds, which they see as “shareholders for the public”.

SWFs can act as intermediaries that allow society to participate in the fruits of

capitalism while preventing adversarial relationships from destroying a company.SWFs usually use budget surpluses (typically, but not necessarily, from the export of commodities) to achieve intergenerational equity and other long-term goals for society.

The authors list five goals for SWFs:

- Economic stabilisation via investment in liquid assets uncorrelated with a country’s source of wealth

- Savings of profits from the export of finite resources

- Pension reserves

- Development of local infrastructure

- Investing in domestic firms to protect them from foreign interference (sometimes including “national economic champions”).

Stakeholder “what-ifs”

The final section of the report has some detailed recommendations about how to improve stakeholder capitalism:

- Redesign governments to exploit “the wisdom of crowds”

- Limit acquisitions and stock buybacks for firms with more than 10% share in an economic sector

- Give long-term (more than five years) employees free “participation shares”

- USe SWFs to give society partial ownership of companies

Conclusions

It’s an interesting paper, which I recommend you read in full.

One of the problems with these kinds of top-down improvements to capitalism is the international coordination of approaches to implementation.

- On the one hand, the climate crisis, the move to renewable energy and the rise of ESG in general provides an opportunity and the election of Biden to the White House means that Europe and the US and closer together on issues like these than in recent years.

But China is keen to assume global leadership and any watering down of Western Capitalism could provide them with an opportunity of their own.

- Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.