Weekly Roundup, 14th June 2021

We begin today’s Weekly Roundup with a look at the G7 deal on corporate tax.

Corporate tax

G7 finance ministers meeting in London have agreed to a global minimum corporate tax rate of 15%

- They also agreed to the principle of raising taxes where goods and services are delivered, rather than where a company is domiciled, or where it chooses to declare profits.

Global companies with at least a 10% profit margin would have 20% of any profit above that would be reallocated and taxed in the countries where they operate.

- In return, the national digital services taxes levied by the UK and some EU countries would be scrapped.

The main impact should be on large tech firms, who use subsidiaries in Bermuda, the Netherlands and Ireland to reduce their tax bills.

- Countries like China, Russia and Brazil – and Ireland, which currently has a 12.5% corporate tax rate – will be invited to join the deal at a G20 meeting in July.

15% is not a particularly high rate.

- But taxes have a tendency to start low and creep ever higher.

Government debt

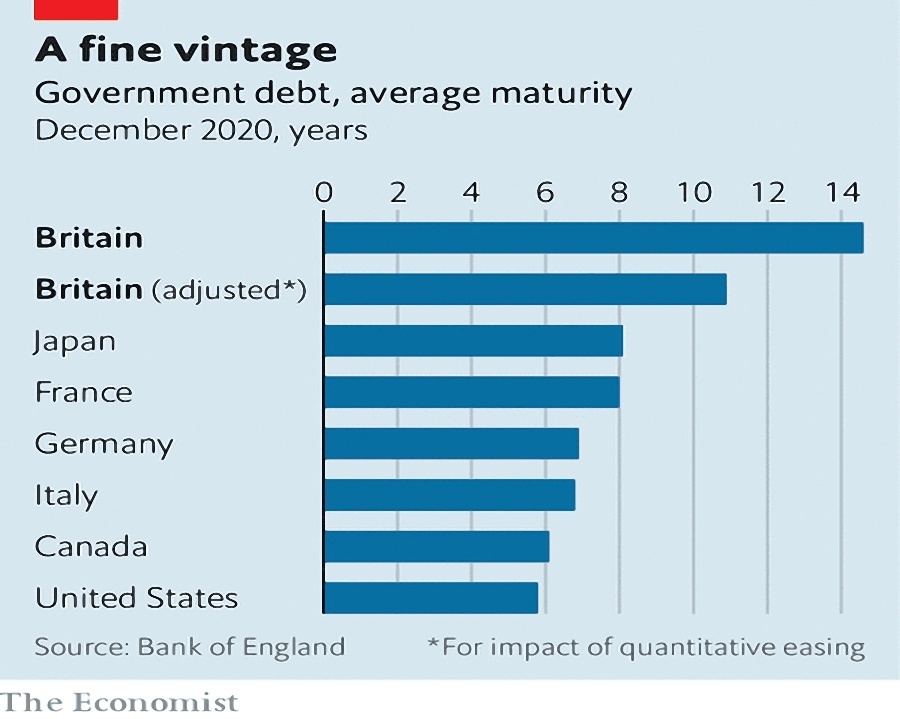

The Economist thought that Rishi Sunak shouldn’t be worried about rising interest rates because British government debt is unusually mature.

- The pandemic resulted in a 2020 deficit of 14% of GDP, the highest for 70 years.

The debt is now close to 100% of a reduced GDP – a level previously thought to be risky.

- But with interest rates at record lows, the cost of servicing the UK’s debt fell from 1.7% of GDP to 1.1%

Sunak’s speeches suggest he is worried about interest rates rising, even by 1%.

QE helps the government, which is now (via the BoE) the biggest debt owner.

- The interest on BoE-owned debt is only 0.1%, rather than the prevailing market rates.

But this means that an increase in Bank Rate feeds through to government interest more rapidly than the maturity profile of the debt would suggest.

- But even the QE-adjusted maturity is longer than all of its peers.

And higher interest rates suggest economic growth and hence higher tax receipts.

- So the UK’s public finances are relatively sustainable.

A second article in the Economist looked at the limits to government borrowing. Biden’s plans:

Assume that annual fiscal deficits will exceed 4% of GDP through to the end of the decade; net public debt will rise to 117% of GDP in 2030 from 110% today.

There are two risks: short-term overheating and long-term catastrophe.

A recent paper looks at the “convenience yield” on government bonds (a yield reduction from the bond’s safety and liquidity) and how it varies with the size of the debt.

- A 10% increase in the debt ratio increases yields by 0.13% to 0.17%.

The real problem comes when the interest rate goes above the rate of economic growth.

- At that point, the debt ratio increases even in the absence of new borrowing.

The authors of the paper also worry about a lower bound of deflation, which drags the growth rate below the interest rate (and into negative territory). (( This sounds like the same problem – growth lower than the interest rate – but for two different reasons ))

- Between the two limits is the “Goldilocks zone” – here, the debt ratio declines even if no new taxes are raised.

The US Goldilocks zone might top out as high as 260% (with a range of 230% to 300%).

- And at this decade’s levels of debt (below 130%) an annual deficit of 2.1% is “sustainable”.

An interesting footnote is that redistribution in the name of reducing equality works against this fiscal free lunch:

Because the rich tend to buy government bonds in disproportionate numbers, efforts to address wide deficits through progressive taxes may not bear much fruit: taxes on high earners will hoover up money that might be used to buy bonds.

John Lee

In the FT, John Lee updated us on his small-cap portfolio. John didn’t sell much during Covid, and has been rewarded:

I stayed with all my major holdings, added to some, and bought into some newer ones. Thanks to the UK’s successful vaccination programme, it now seems we are coming out of a long, dark tunnel, with stock prices responding. My combined Isa and non-Isa portfolios are around an all-time peak.

Stocks he mentions include Vitec, Aviva and STV. He also reports on a wager with an investor friend:

We came up with “The Richmond Challenge” and “The Richmond Bowl” as a test of whether my UK small-cap philosophy would fare better or worse than his strategy of selecting technology and tomorrow’s companies.

So far, John is leading, thanks to stocks like Anpario, Cerillion, Concurrent Technologies, Lok’nStore and Treatt.

- Of these, Concurrent is the only loser.

Three other laggards outside the competition are Air Partner, Appreciate and Christie.

Tax year-end

The Office of Tax Simplification (OTS) has kicked off a review of the benefits, costs and other implications of changing the current date of 5th April to 31st March, or even to the end of the calendar year.

- The UK government already makes its own accounts up to 31st March, and lots of other countries (including the US, France and Germany) use the calendar year.

The OTS said:

The UK’s tax year for individuals runs from April 6 to the following April 5. This

is for historical reasons and has been the case for hundreds of years; the UK’s modern tax system and infrastructure have been developed around this date.By contrast, accounting systems used by businesses have been developed around month and quarter ends. Across businesses and internationally, it is common to account to a month end date. The UK financial year for government accounting and for companies runs from April 1 to March 31.

While primarily addressing tax simplification issues, the review will also take account of the implications of any change in other areas, such as in relation to tax credits and benefits.

The trouble with all this is that the benefits are proportional to the effort and disruption.

- Moving to 31st March should be easy, but would it make a real difference?

Whereas a transitional year of fewer than nine months would throw up issues for lots of people, not least investors looking at company accounts.

- And it still wouldn’t fix the issue of VAT often not using the quarter months.

Crypto

The FCA has given crypto firms another eight months (until March 2022) to comply with money laundering and terrorist financing regulations.

- The temporary arrangements were supposed to end on 9th July.

It appears that an “unprecedented” number of firms (51) have withdrawn their applications entirely.

- Just five firms are fully registered, with 90 operating under temporary registration.

The five firms that are registered are Gemini (twice), Ziglu and a couple I haven’t come across – Digivault and Archax.

- Note that even the registered firms don’t have access to the Financial Ombudsman or the Financial Services Compensation Scheme.

The FCA said:

A significantly high number of businesses are not meeting the required standards under the Money Laundering Regulations resulting in an unprecedented number of businesses withdrawing their applications. The extended date allows cryptoasset firms to continue to carry on business while the FCA continues with its robust assessment.

Cryptoassets are considered very high risk, speculative investments. If consumers invest in cryptoassets, they should be prepared to lose all their money.

In the ETF Stream newsletter, Tom Eckett suggested that the FCA might need to rethink its ban on UK retail investors buying crypto ETNs.

- French and Dutch regulators have now joined Switzerland and Germany in allowing these products.

There are now two ETPs listed in the UK (on the Aquis Exchange), but we can’t buy them.

ETC Group and HANetf launched Europe’s largest bitcoin ETP, the $695m BTCetc

Bitcoin Exchange Traded Cryptocurrency (BTCE), on the Aquis Exchange Multilateral

Trading Facilities (MTFs) in London and Paris. 21Shares also listed its bitcoin ETP.ETC Group’s CEO Bradley Duke said the firm initially sought a listing on the London Stock Exchange but was rejected as the LSE’s clearing house, LCH Clearnet, does not

currently settle crypto strategies. After listing BTCE on the SIX Swiss Exchange,

ETC Group turned to Swiss clearing, which is once again allowed to trade in London.

Our third crypto story of the week concerns Ruffer, who has announced a huge profit on their five-month bitcoin trade.

- They timed their exit well, selling just before the all-time high in April.

Their total profit was around $1.1 bn. In their monthly investment update, managers Hamish Baillie and Duncan MacInnes said:

The bitcoin exposure was put into the portfolio as a defensive investment, to add

diversification to our inflation hedges. Its strong rise thereafter reflected increased institutional and retail interest, and as it hit all-time highs in April we judged its asymmetry to be much lower (and importantly the threat to gold to be lower too).With more attractive risk-adjusted positions elsewhere in the market, we sold the remaining exposure.

A fourth crypto story is an announcement that El Salvador (ES) will recognise bitcoin as legal tender.

- ES President Nayib Bukele also said that bitcoin miners in the country could make use of the countries volcanoes to produce ” 100% clean, 100% renewable, 0 emissions energy”.

Currency adoption sounds potentially significant – not least because it would remove capitals gains tax on profits, at least in El Salvador.

- But ES relinquished its monopoly on money back in 2001 when it replaced the colon with the US dollar (Panama and Ecuador have done the same).

So we’re still waiting for a country that prints its own banknotes to adopt crypto.

Fifth, Michael Saylor of MicroStrategy has doubled down on his laser-eyed bitcoin maximalist persona by not just allocating his company’s cash to crypto, but by raising another $500M in bonds to invest in bitcoin.

As Cullen Roche said on Pragmatic Capitalism:

The asset exposes MicroStrategy to enormous downside risk in the case of a BTC crash that coincide[s] with a tech recession. The major worry is that the firm’s actual cash flows collapse at the same time the BTC position collapses.

And then you risk a perverse feedback loop where the firm becomes a forced seller of BTC to create liquidity to remain solvent, which makes the entire BTC collapse worse. It’s almost like Saylor has turned a nice little boring data firm into a financialized weapon of potential mass destruction.

It’s also difficult to see why anyone would buy these bonds, which offer all of the downsides of bitcoin but with a fixed upside.

- It reminds me of the bizarrely popular “bond” schemes here in the UK where you lend money to property developers (or startups) who retain the upside if their project is a success but burn your money if it flops.

Sixth, the G7 finance meeting which approved the minimum corporate tax also restated their opposition to digital currencies:

No global stablecoin project should begin operation until it adequately addresses relevant legal, regulatory, and oversight requirements through appropriate design and by adhering to applicable standards.

That sounds like a problem for Facebook’s Libra project and China’s independent Digital Yuan.

And finally, the Basel Committee on Banking Supervision said that banks will need to follow strict capital requirements in order to hold bitcoin and other crypto assets.

- According to Basel, their increasing popularity can “raise financial stability concerns and increase risks faced by banks.”

Since BTC rallied on the news, presumably the crypto community had been expecting an even tougher verdict.

Quick links

I have eight for you this week, the first four from The Economist:

- The newspaper had two articles on the green bottlenecks which threaten the clean energy business

- And which could constrain emission cuts.

- The Economist also looked at how soaring factory prices in China were adding to global inflation fears

- And wondered whether empty shopfronts would revive as New York comes back to life.

- UK Value Investor had the 2021 half-year results for his Million Pound Portfolio

- And Musings on Markets looked at the rise of SPACs

- Alpha Architect examined the international evidence for combining the value and profitability factors

- And warned against using book to market as a value metric.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.