Rethinking Equity Tail Risk

Today’s post looks at a recent paper from HSBC multi-asset team on how to think about equity tail risk hedges.

HSBC

I’m not sure that we’ve looked at any other papers by HSBC Asset Management. This paper seems to be a regular newsletter aimed at professional investors. The May 2026 edition:

revisits the foundations of diversification when it is really needed (bad times), asking what it really means to hedge equity tail risk when stock-bond correlations are no longer reliably negative and sovereign balance sheets are under pressure.

The conclusion is that asset behaviour is regime-dependent and related to macro dynamics and market shocks, meaning that no single asset can be relied upon as an evergreen hedge.

- Bonds work well when the stock-bond correlation is negative and bond risks are low.

- Rising real rates and inflation, along with “fiscal uncertainty”, can push correlations into positive territory.

- Regional equity splits are less effective than they were historically, and sector, factor, and option overlays are preferred.

Effective tail risk management now calls for a dynamic, regime-based framework that blends sovereign bonds, alternatives, FX, commodities and options, rather than relying on any single static safe haven.

Equity tail risk

Globally diversified portfolios containing only equities have seen stretches of more than 20 years of negative real returns, while similar bond-only portfolios have, in some cases, faced multi-decade real wealth destruction, particularly around major wars and inflationary episodes.

Even the 60/40 portfolio suffered deep drawdowns in systemic crises such as the First World War and the Great Depression.

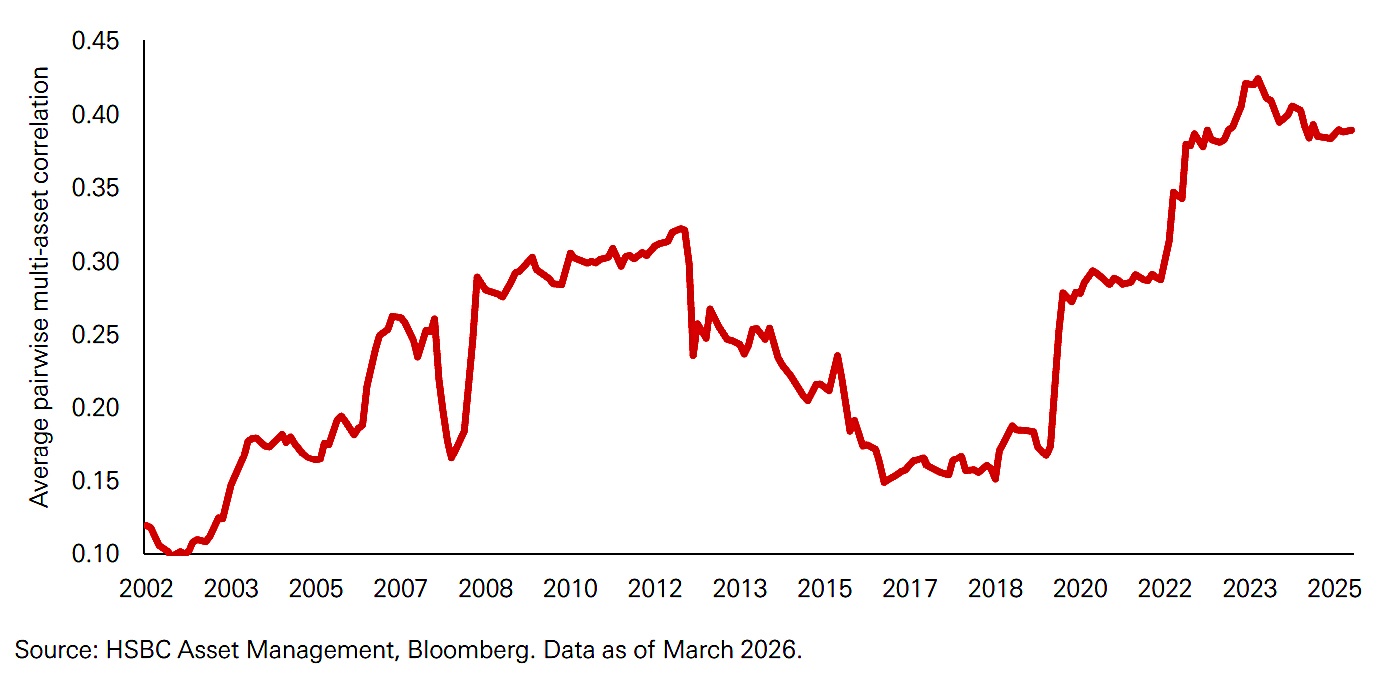

Markets have become increasingly correlated through globalisation, making the search for defensive assets more popular but also more difficult.

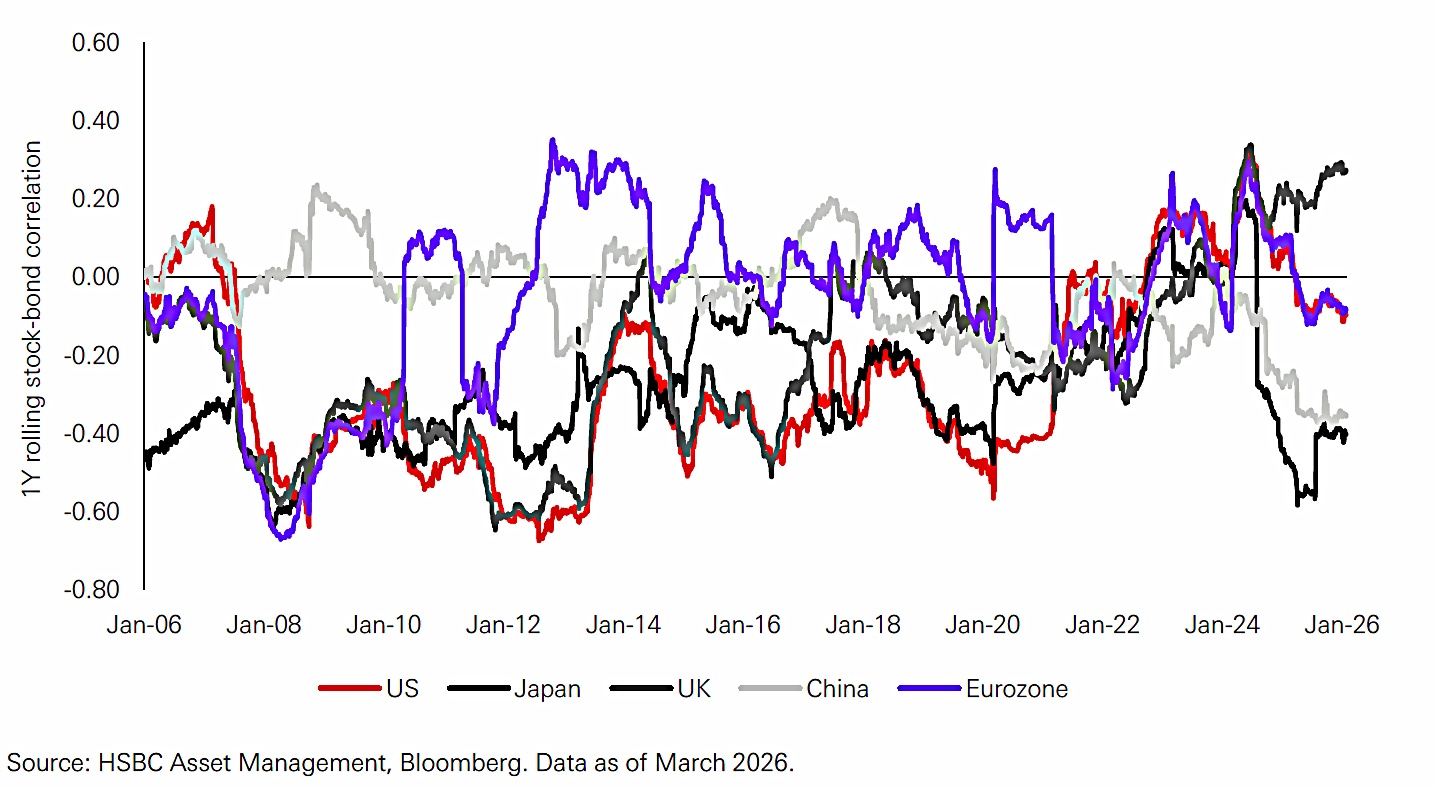

(Government) Bonds are the default hedge, but the stock-bond correlation (SBCV) varies across time and across economies.

The negative correlation exhibited between 2000 and 2020 was mostly limited to North America, whereas in Europe it had already reversed during the European sovereign debt crisis, led by periphery countries and later joined by core European nations.

Rising real rates and higher inflation variance relative to growth variance tend to push SBC higher, as both equities and bonds sell off in response to inflation or policy shocks. By contrast, rising growth risks, increased risk aversion, flight to quality flows and more accommodative monetary policy tend to pull SBC lower, as bonds rally when equities fall.

This doesn’t sound too bad to me – we know what to look for to predict a high SBC, and we have multiple shots (across regions) at finding a low one.

- It sounds like a globally diversified 60/40 with a TAA overlay might do okay.

HSBC consider the current shocks:

Trade and tariff shocks have historically seen sovereign bonds perform relatively well in equity drawdowns, as growth concerns dominate the potential inflation impacts.

By contrast, periods of elevated military spending often involve shifting part of the fiscal burden onto bondholders through surprise inflation and financial repression, leading to weak real bond performance even as risk assets sell off.

This is fine as far as it goes, but it ignores the elephant in the room – whether the current massive investment in AI will pay off.

- We could have greatly increased productivity (growth with deflation) or a complete bust.

I would expect this result to swamp the effects of tariffs and defence spending.

Alternatives

Alternatives to bonds induce commodity and credit carry strategies, and:

Bond trend following, which has delivered strong returns at near-zero correlation to 60/40 portfolios and tended to outperform in inflationary periods.

I have no idea how a UK private investor might access bond trend-following as a stand-alone strategy.

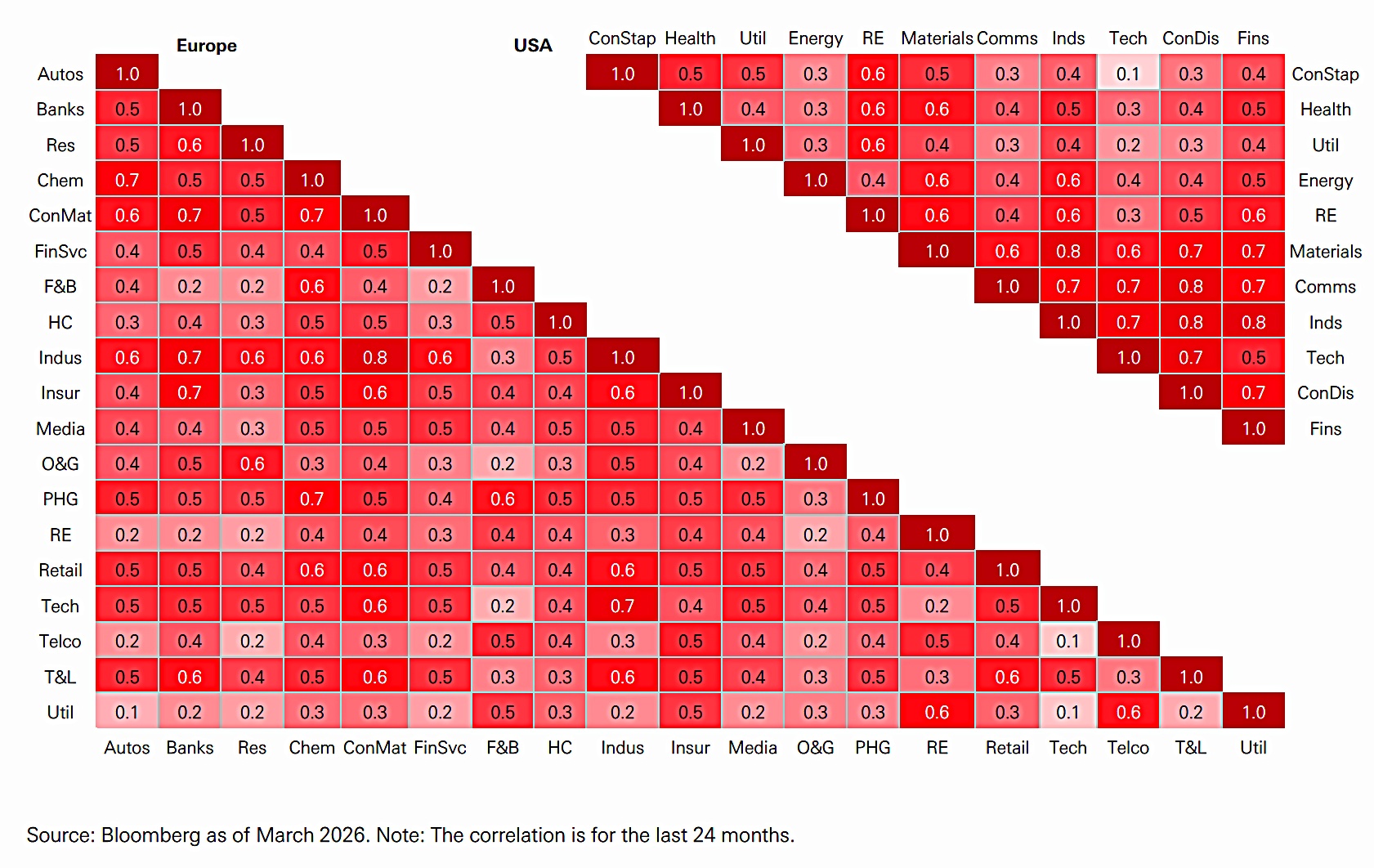

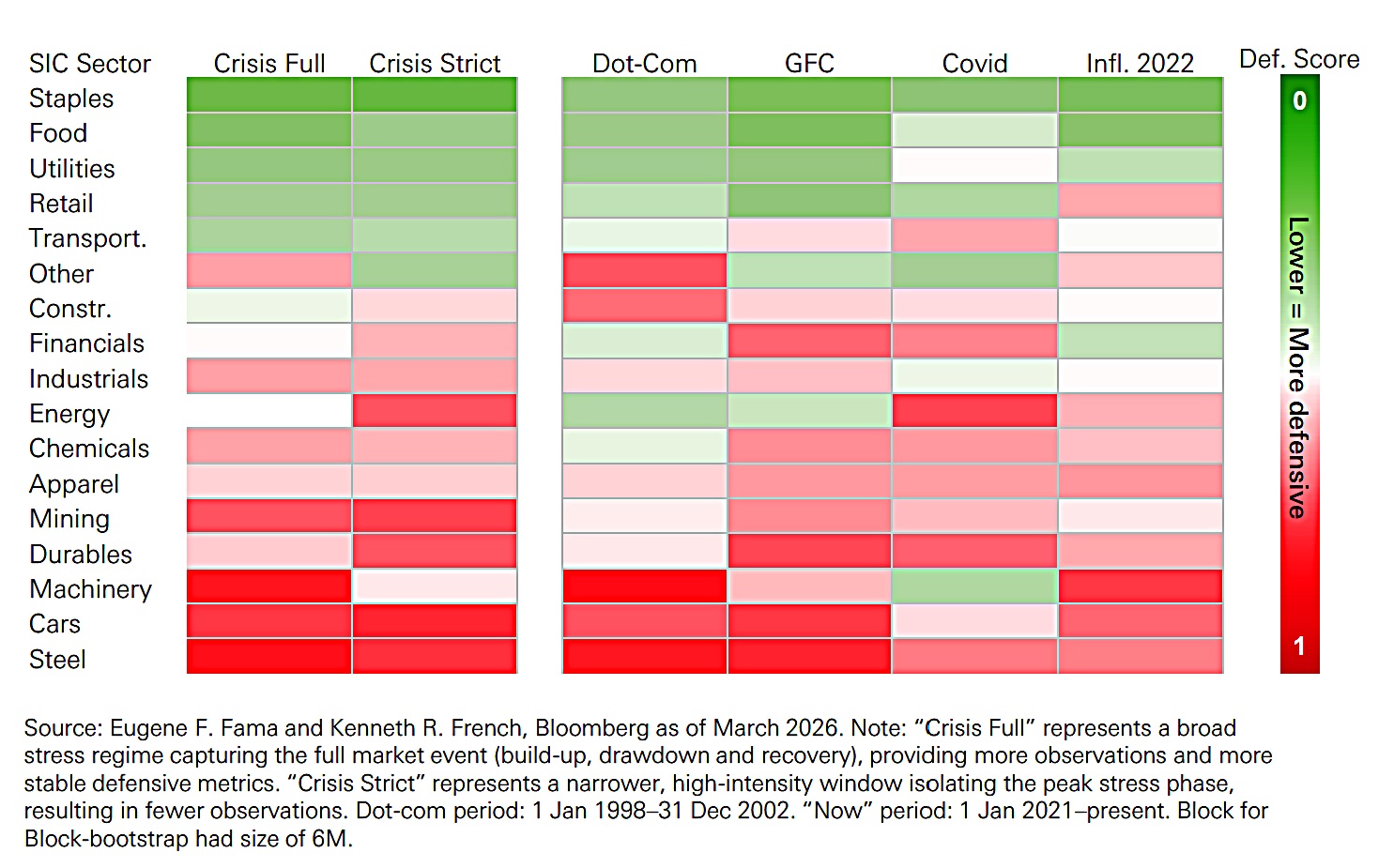

Sector diversification with equities is also useful.

Cross-sector correlations display a much broader range of correlation metrics [than cross-country correlations], with sectors such as utilities, telecoms and consumer staples displaying defensive qualities.

Defensive leadership is persistent, but downside sensitivity is regime dependent. A good illustration is the performance of food and utilities during the Covid pandemic.

Factors can also help, with momentum and value contributing in different parts of the market cycle.

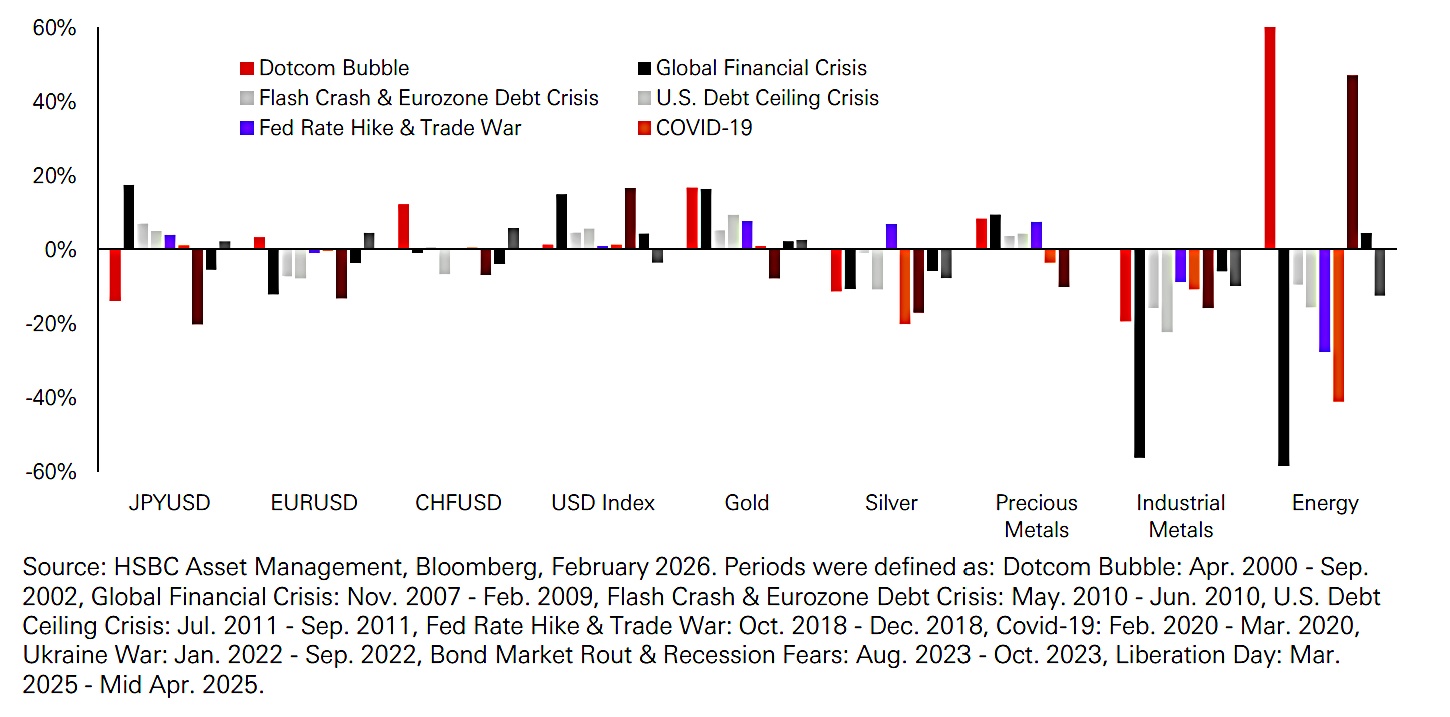

And FX and commodities are also useful:

Historically, the US dollar, Swiss franc and gold have been among the assets most frequently providing protection during equity drawdowns.

Gold has evolved from a passive inflation hedge into a strategic competitor to US Treasuries as a reserve asset, particularly for non-Western central banks seeking sanction-resistant assets with zero counterparty risk.

At the same time, gold’s short-term performance remains sensitive to real yields, positioning and technical factors. Recently, gold has failed to provide an effective hedge during the current Middle East conflict after its strong run in 2025 and early 2026 meant that it was overvalued coming into the volatility.

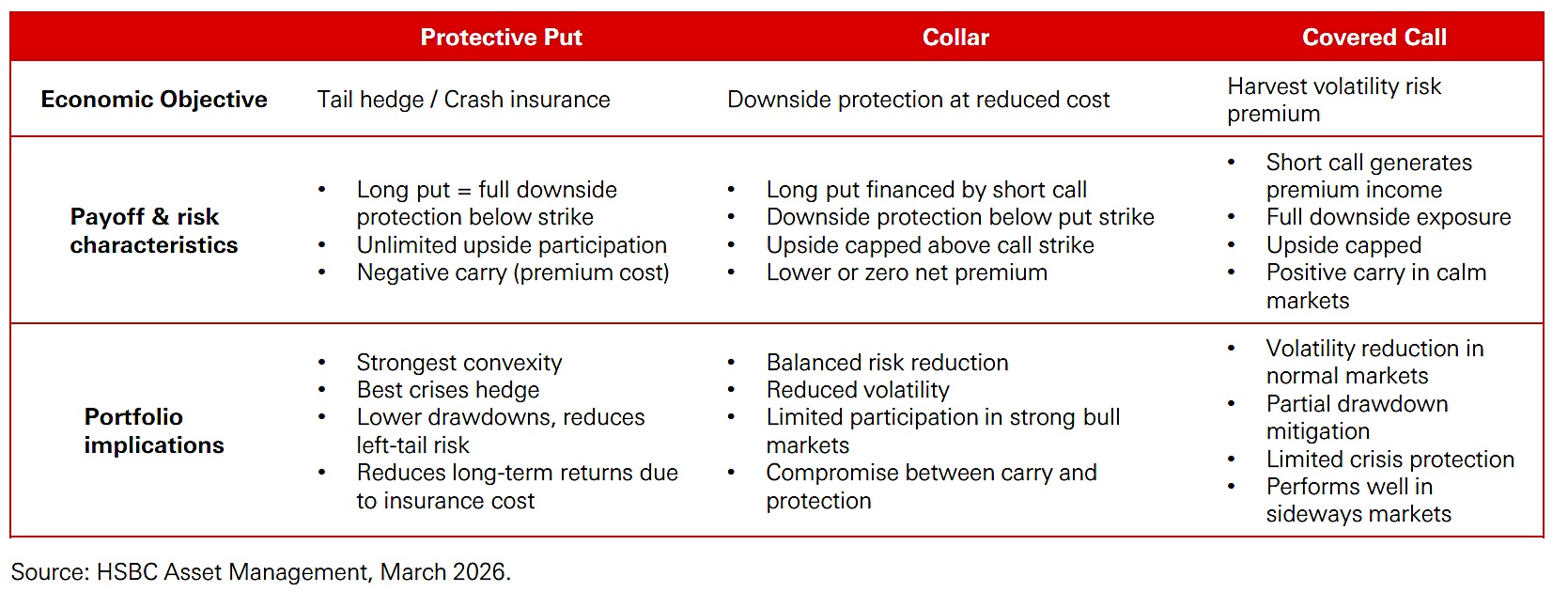

Options

HSBC also looks at the use of option strategies.

Long (equity) option positions typically benefit from rising implied volatility and negative equity returns during drawdowns.

Equity sell-offs are often accompanied by volatility spikes and rising cross-asset correlations, which can weaken traditional diversification. In such regimes, long volatility option overlays may provide a more defensive, convex return profile.

The trick here is knowing when to add the overlays, as they are an expensive form of insurance.

- They also cap returns in extended bull markets, so adding them too early can be costly.

No single options strategy dominates across all environments; the choice between long and short volatility structures depends on expectations about crisis frequency and severity, the level of implied volatility and tolerance for carry costs versus drawdowns.

Conclusions

There’s not much new here, and not much that’s directly applicable to a UK private investor.

- In particular, the conclusion that dynamic, regime-based hedging is best is not much use without a set of rules that can be applied systematically.

But it’s always good to have new data from a new source.

- One surprising omission for me is the absence of trend-following as a hedge.

That’s it for today.

- Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.