Rabener on Leverage and Trend

Today’s post catches up with four articles from Nicolas Rabener at Finomial, on the use of Leverage and Trend.

Finomial

I’ve been following Nicolas’ work since his firm was called Factor Research. Unfortunately, he put most of his material behind a paywall a few years ago, so nowadays you only get the headlines (which can still be useful).

One type of article that remains outside the paywall – Nicolas’ portfolio reviews. We’ll look at one of those today.

Trend

The portfolio is a leveraged one, but before we look at it, let’s catch up with a couple of headline emails on the other element of a portfolio that I’m particularly interested in at the moment – Trend.

We got our first Trend ETF (strictly, managed futures) here in the UK almost a year ago, and I’ve been keen to read anything on how useful Trend can be as a diversifier.

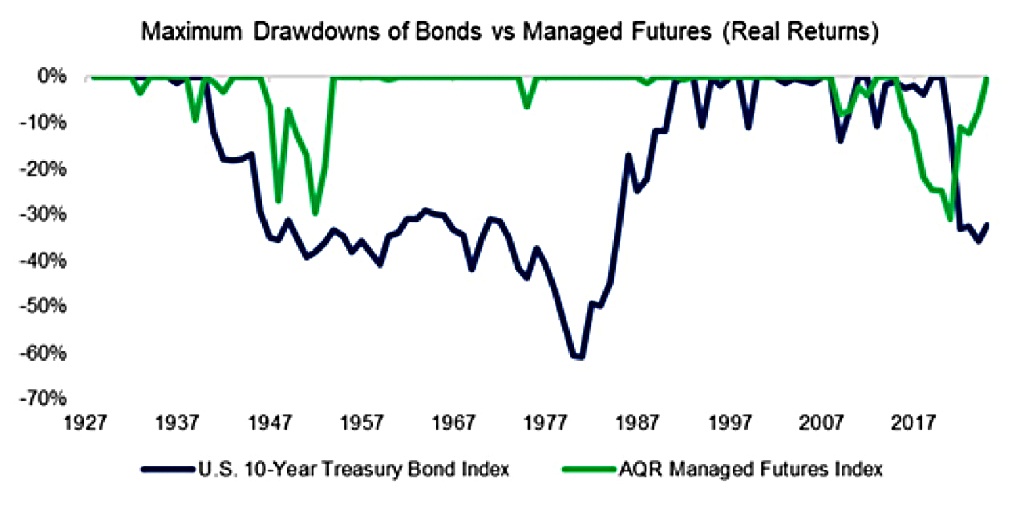

The first email compared Trend (futures) with bonds as a diversifier. Here are the headlines:

- Managed futures generated a significantly higher long-term return than bonds

- U.S. Treasury Bonds experienced a 61% loss in real terms historically

- Correlations of bonds and equities are elevated, limited diversification benefits

Futures also have much lower drawdowns.

The (outside the paywall) intro to the article notes that stock and bonds now have positive correlations and that bond yields are no longer declining (prices rising) as they were for most of the 21st century until 2022.

- By contrast, futures coped with this shift by switching from being long bonds to holding short bond positions.

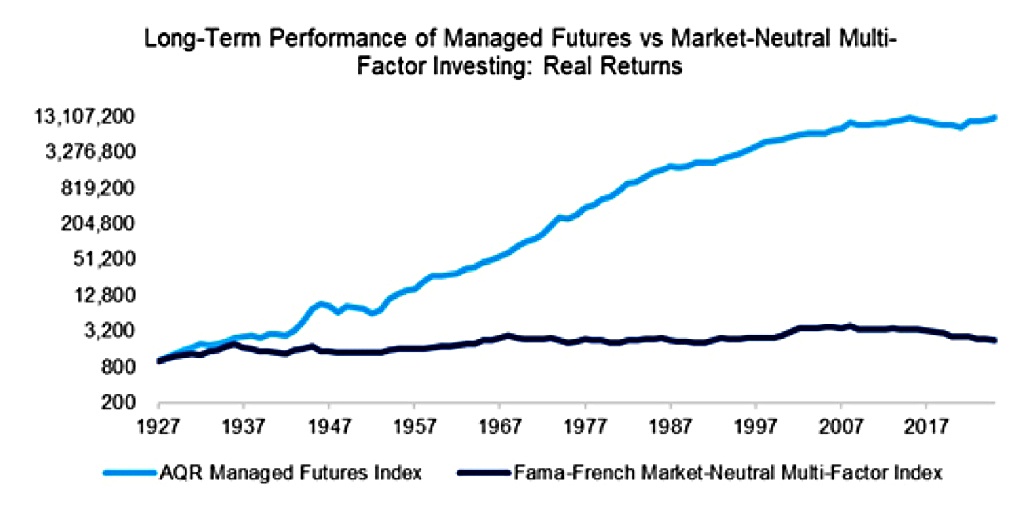

The second email compared futures with factor investing. The headlines:

- Managed futures generated higher returns than a simple market-neutral multi-factor portfolio

- Naturally, the factor selection matters

- Combining both generated the largest diversification benefits

The outperformance from futures is huge over 100 years:

The intro to the article made a couple of additional points:

[In] conventional asset allocation frameworks, bonds occupy a central role while managed futures remain largely absent. The limited adoption of managed futures is especially puzzling given the extensive body of academic research supporting the strategy.

A similar pattern can be observed in factor investing: investors frequently rely on evidence derived from long-short factor research, yet allocate predominantly to long-only implementations.

I can’t speak for institutional or US investors, but for UK investors working within tax-sheltered accounts, implementing futures was difficult until recently, and shorting remains so.

Leverage

I think the purpose of the free portfolio article is to highlight the methodology used to analyse it, but I’m interested in the portfolio itself:

- An all-weather portfolio using leveraged equities + diversifiers

- Most funds are uncorrelated, offering diversification benefits

- Generated higher returns & Sharpe ratio than an 80/20 portfolio

That sounds right up my street.

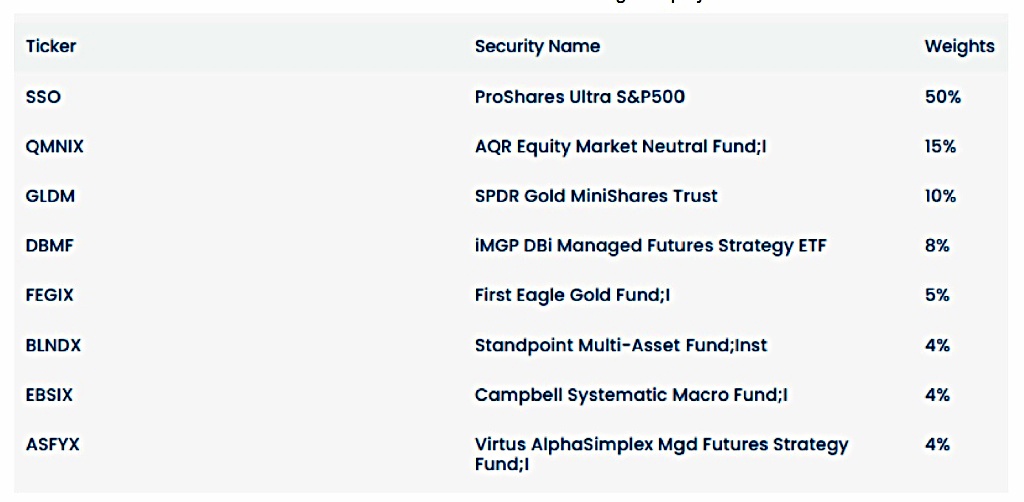

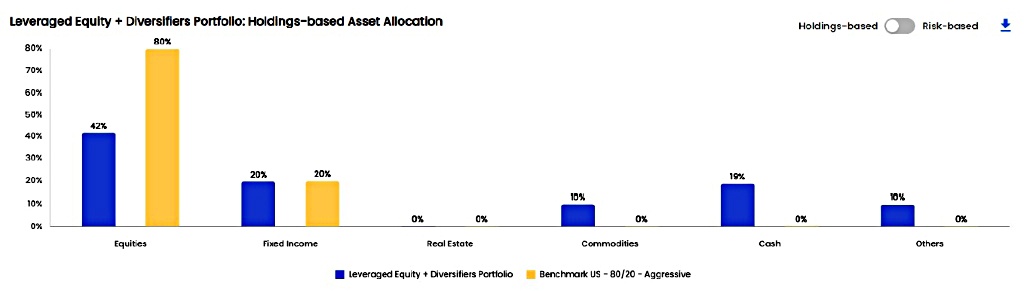

First up is a breakdown of the holdings.

- It has a 50% allocation to a 2X S&P 500 ETF

- There’s around 25% of managed futures (trend)

- There’s 15% in an equity market-neutral fund

- And 10% in gold.

So the leverage is 50%, a bit steep (and impractical) for me.

- And the annual fees are 0.93%, way too much for me.

Some of the funds are quite new, so the performance record only goes back to 2019.

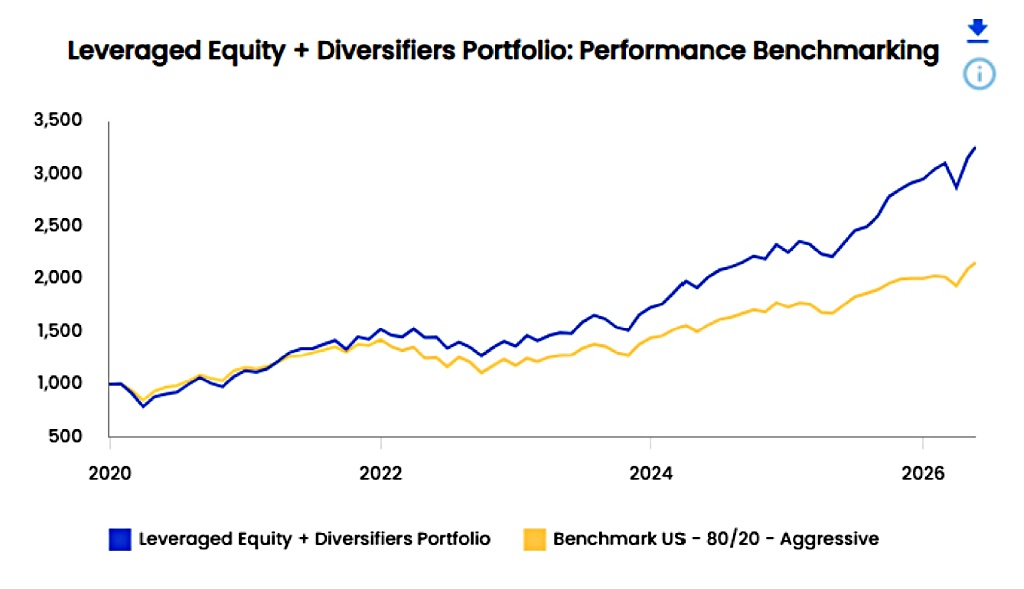

- Nicolas chose an 80/20 benchmark, as the portfolio is leveraged/aggressive.

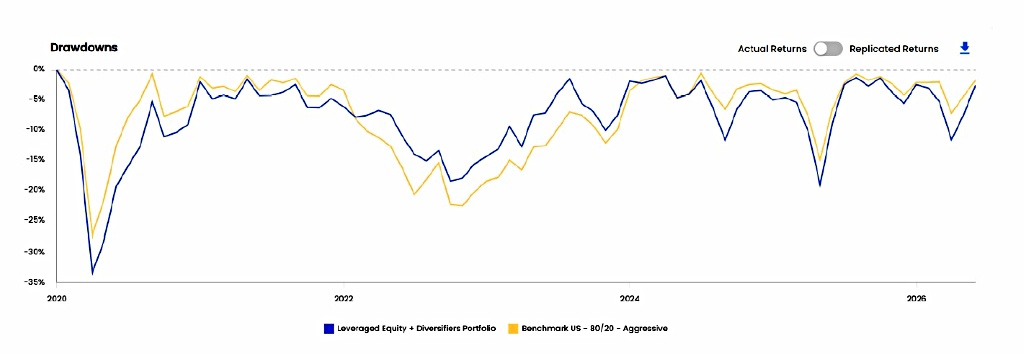

The all-weather portfolio generated a significantly higher CAGR (20.3% vs 12.8%), a higher Sharpe ratio (0.89 vs 0.61), and a higher drawdown (-33% vs -27%).

The AWP is more diversified, as it has allocations to commodities, cash and other assets as well as bonds and stocks.

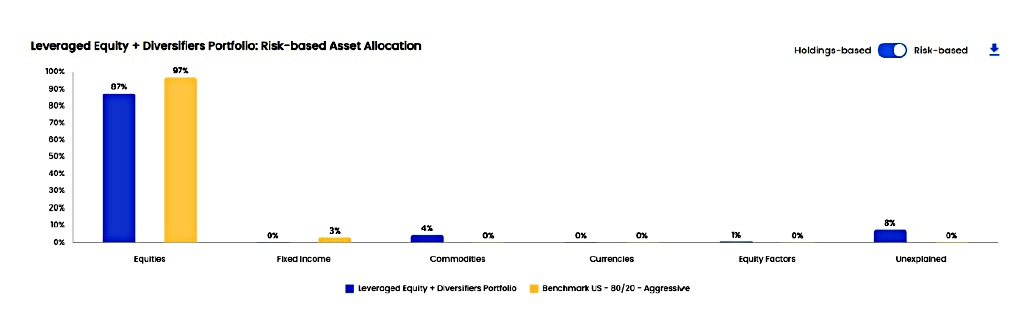

A risk-based asset allocation shows that equities dominate both portfolios, but the AWP has some other minor contributors.

Most of the funds in the AWP have low correlations with each other, which means there are significant diversification benefits.

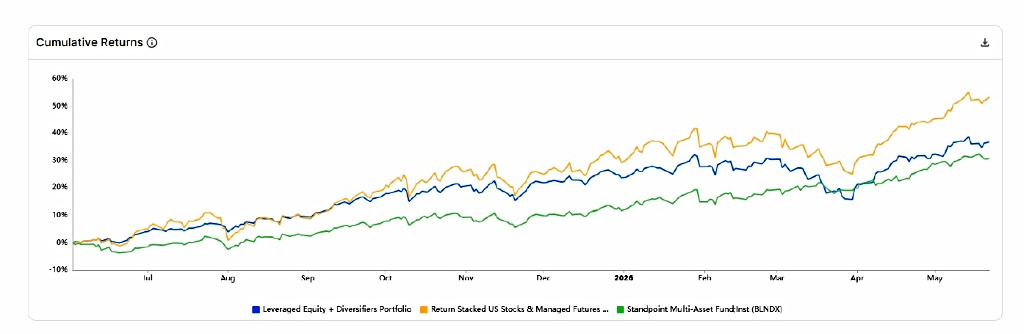

The only fund worth replacing is the Standpoint Multi-Asset Fund(BLNDX), as it is a combination of equities and managed futures, but the portfolio already includes these exposures. BLNDX can be replicated via the S&P 500 and DBMF, and removing it simplifies asset allocation.

Next, Nicolas looked at the performance under stress:

The all-weather portfolio performed worse during the COVID-19 crisis in 2020, which we attribute to its leveraged equity allocation and the lack of bonds. However, during 2022, when stocks and bonds fell, the portfolio outperformed as managed futures were short bonds.

The portfolio’s average volatility was higher (19.6% vs 16.3%), but so was its return.

He also looked at the options for simplifying the AWP:

The various managed futures funds could be replaced by a single fund, e.g., DBMF.

However, investors could also consider allocating to funds such as Return Stacked US Stocks & Managed Futures ETF (RSST) and Standpoint Multi-Asset Fund (BLNDX), which provide equity and managed futures exposure in a single fund. However, RSST has no meaningful track record, and both are less diversified yet more expensive.

DBMF is the US equivalent of the only UK futures ETF.

- Sadly, RSST is not available in the UK – the only leveraged multi-asset funds here use stocks and bonds (better than nothing, but it complicates allocation).

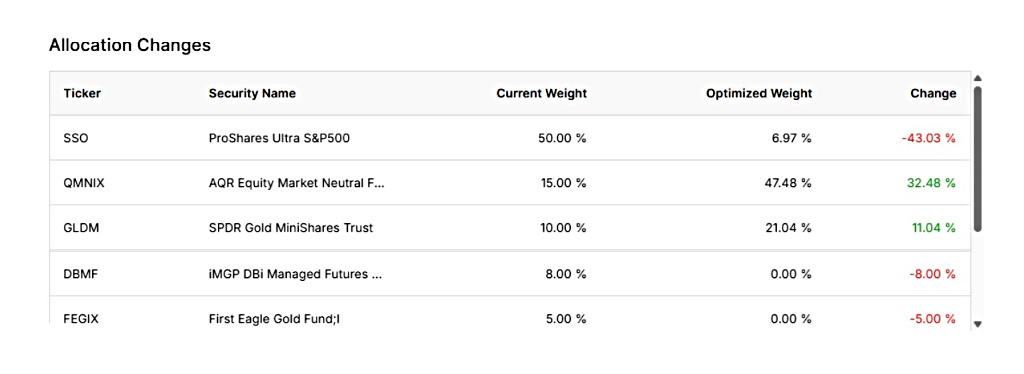

Finally, Nicolas looked at an optimised version of the portfolio.

A simple, unconstrained Sharpe optimization would allocate almost entirely away from the leveraged equities position (SSO) toward the equity market-neutral fund (QMNIX).

Gold is preferable to gold miners; all managed futures funds would be allocated to the Campbell Systematic Macro Fund Class (EBSIX). Food for thought.

Follow-up

A follow-up article in June 2026 extended the track record of the portfolio from five to sixteen years, using similar funds with longer track records.

- The two portfolios performed the same over five years, with the newer funds doing better over the last two years.

Over the longer term, the performance since 2010 was similar to the S&P 500 (albeit in a very good period for the S&P), apart from the last two years.

Almost all risk could be attributed to the global stock market, as proxied by the MSCI ACWI. The portfolio had only 8.3% idiosyncratic risk, which seems low given that 50% of the allocation was to diversifying strategies.

Nor did the portfolio show consistently lower drawdowns in stress periods than the S&P.

This is partially a function of including a leveraged equity allocation, which offers a higher return, but poorer risk-adjusted returns than unleveraged equity, given the characteristics of leveraged products.

If we replace this 50% allocation with the S&P 500, the all-weather portfolio has generated higher returns and a higher Sharpe ratio than the traditional equity/bond portfolio. Stated differently, investors do not need bonds in their portfolios for diversification.

Nicolas notes that the diversifiers have only really performed over the last five years.

- At the same time, the portfolio outperforms a traditional 60/40 model, so its success depends on the benchmark you use.

Conclusions

Whilst Nicolas’ approach to portfolio analysis is interesting, the main takeaways for me today are that trend and leverage can be valuable additions to your portfolio.

- I wish the UK regulators would make it easier to add them to ISAs and SIPPs.

That’s it for today.

- Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.