Quantica on Stacking

Today’s post looks at a recent paper from Quantica Capital called “If You Can’t Beat It, Stack It”.

Contents

If you can’t beat it, stack it

The subtitle of the paper, released in March 2026, is “How Portable Alpha Overlays May Enhance Equity Returns”.

- I’m a bit disappointed with that “may” – over the long run, portable alpha looks like a good bet to me.

The paper looks at eight “liquid diversifiers”, examining the trade-off between their downside protection and their long-term returns.

- It also looks at how diversification is incorporated into portfolios.

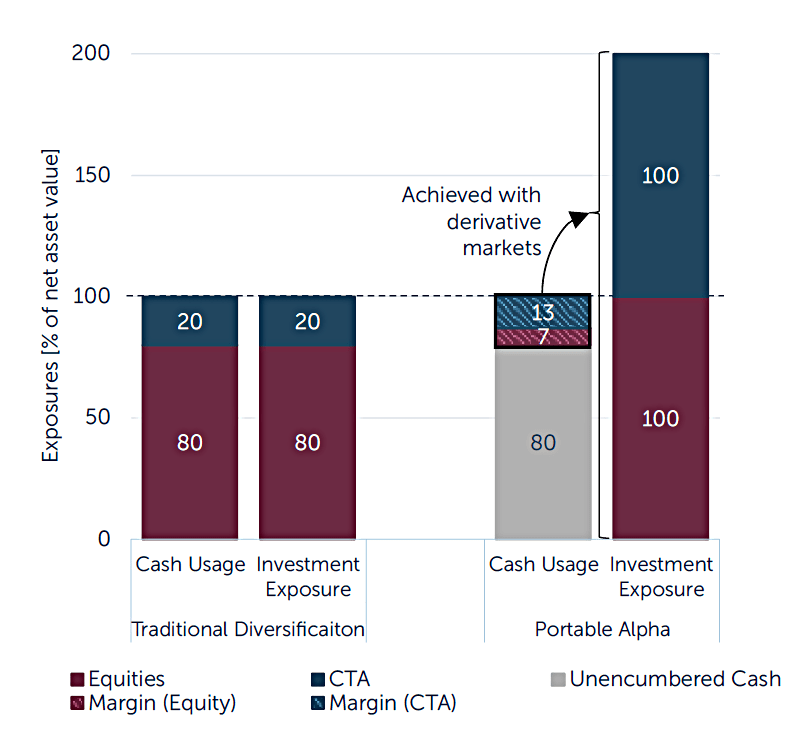

In traditional fixed-weight allocation frameworks such as a 60/40 portfolio, diversification is typically funded by reducing equity exposure. When implemented through capital-efficient portable alpha overlays, diversifying strategies can be layered on top of a core equity allocation rather than replacing it.

Which means that returns during strong periods for equities need not be impacted.

- The key attribute of the diversifier becomes its correlation to stocks.

A diversifier with persistently low or negative correlation creates additional risk capacity, enabling greater scaling without increasing overall portfolio volatility.

This is the same idea as the tracking error budget we came across in the recent note from Return Stacked Portfolios.

- And once again, trend following and gold emerge as the best overlays.

In contrast, liquid alternative strategies with embedded equity beta or structurally positive correlation to equities offer limited overlay capacity and therefore deliver more modest portfolio-level diversification benefits.

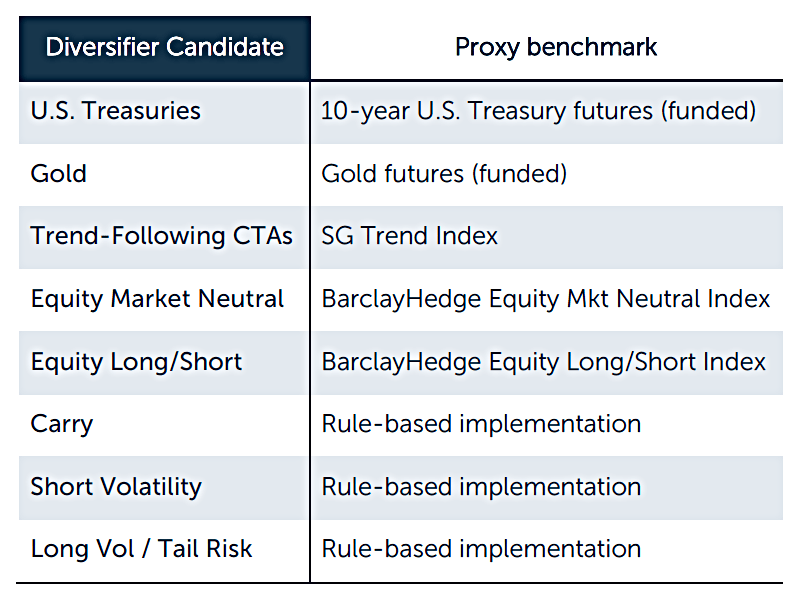

Diversifier candidates

Here they are:

All the usual suspects are here.

- All strategies are normalised to a 12% vol target

- Only five of the eight have a proxy benchmark (how to implement the other three is defined in an Appendix to the paper)

- Only three are readily available in UK tax shelters as an ETF

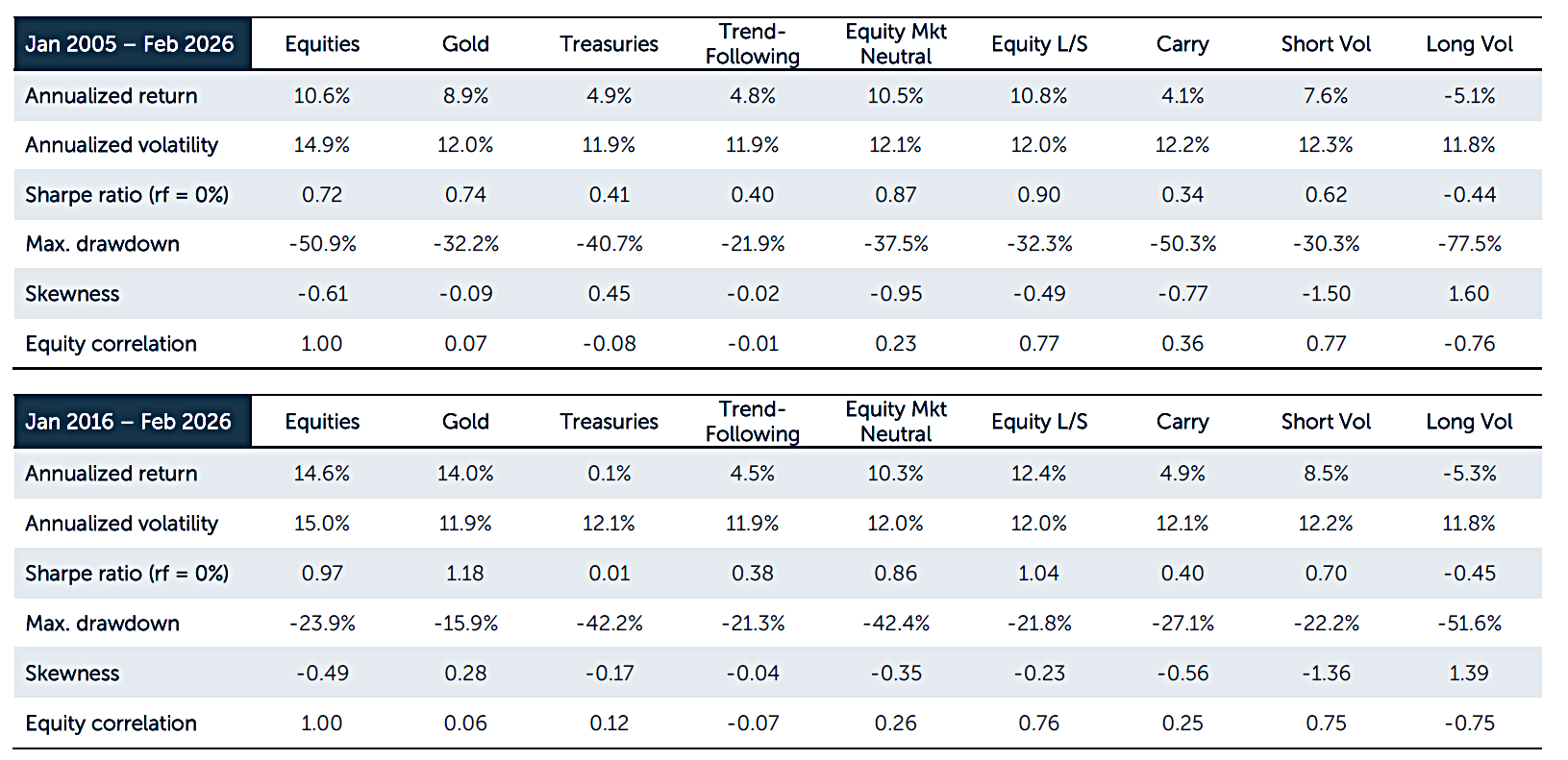

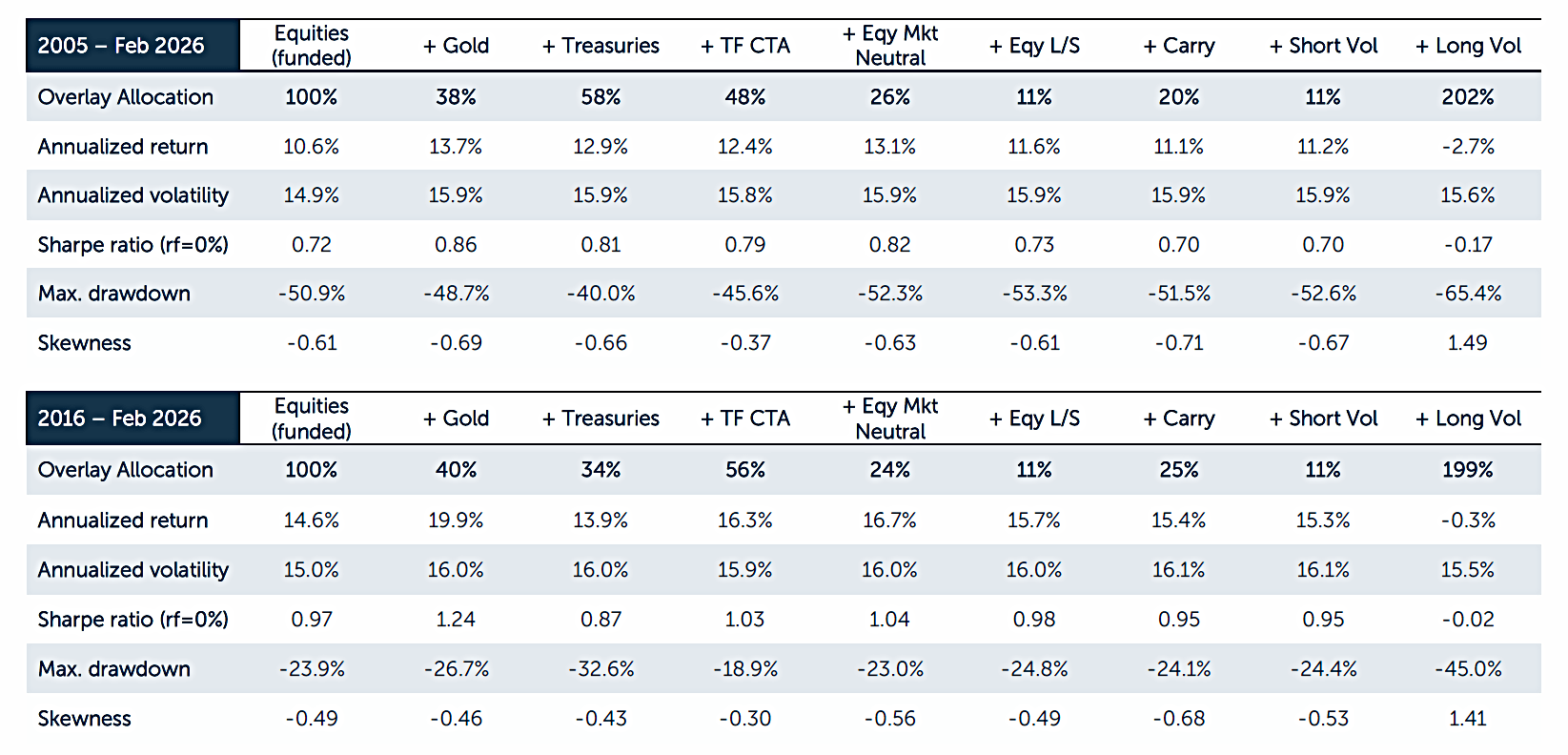

Over the past 21 years, U.S. equities delivered an annualized return of 10.6% at 14.9% volatility. By comparison, the eight diversifiers – normalized to a 12% volatility target – generally underperformed equities, with Equity Long/Short the sole exception, outperforming by 0.2% p.a.

Excluding Long Volatility, all strategies generated positive returns since 2005, with annualized performance ranging from 4.1% (Carry) to 10.8% (Equity Long/Short).

It hasn’t been a bad period for US stocks, so the underperformance is not a massive shock.

Excluding Long Volatility, Trend-Following exhibits the most favourable skewness among all diversifiers over the full sample and the second most favourable, after Gold, over the past decade.

Quantica classify the diversifiers by correlation profile:

Equity Long/Short, Equity Market Neutral, Short Volatility, and Carry exhibit structurally positive equity correlations of 0.77, 0.23, 0.77, and 0.36, respectively.

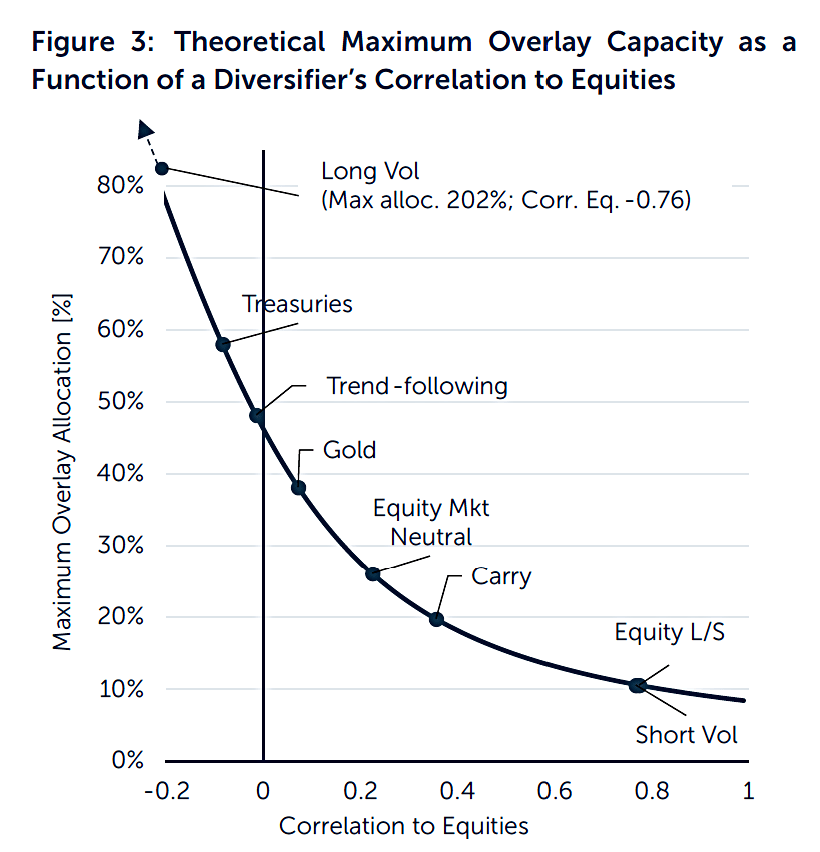

Long Vol has a strongly negative correlation, but also a persistent negative carry, making it expensive to hold.

Between these extremes, Trend-Following, Gold, and Treasuries combine low to near-zero long-term equity correlation with positive risk premia, making them the most cost-effective diversifiers.

Luckily, these are also the three that are easiest to hold within UK tax shelters.

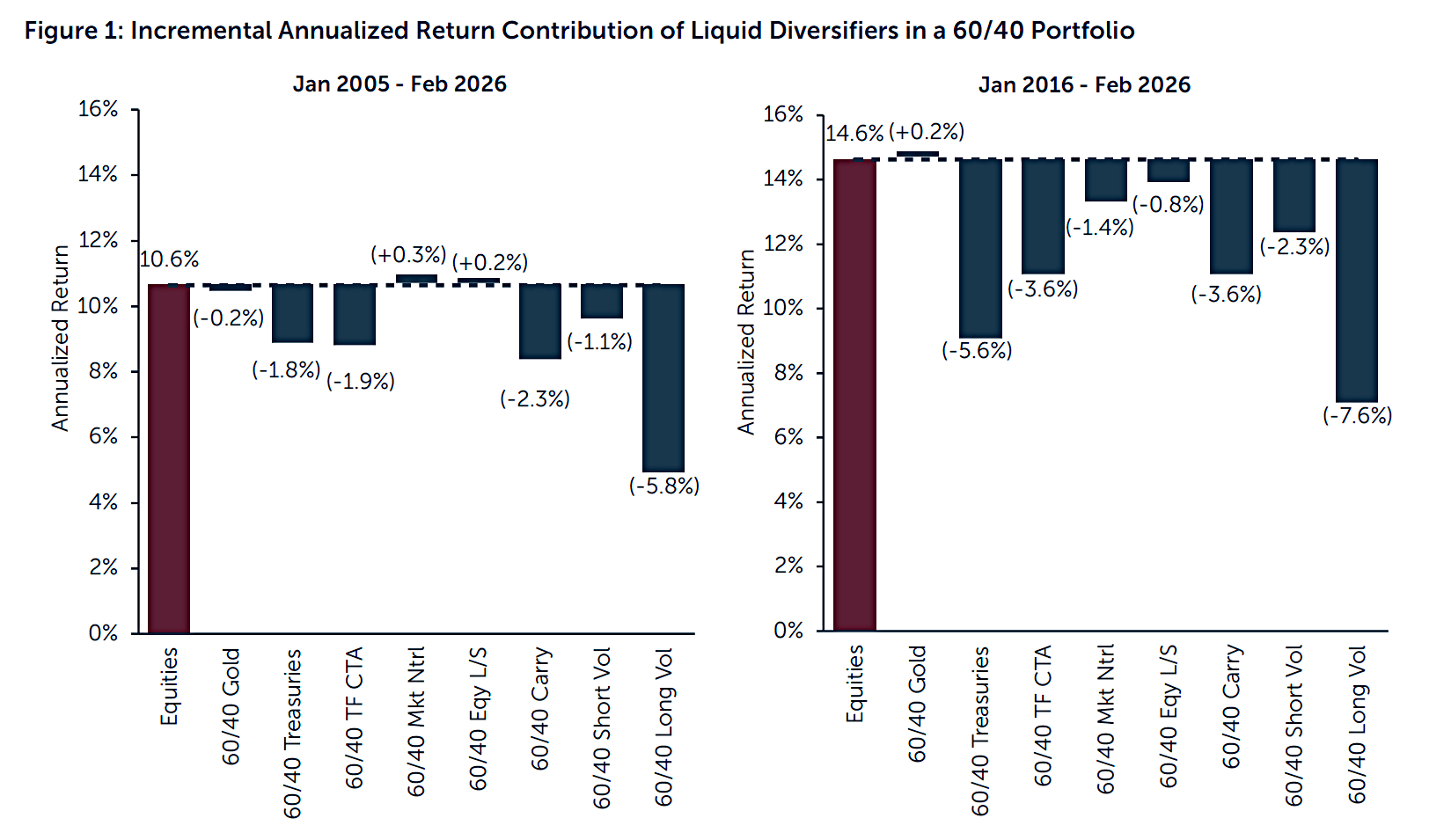

The Cost of Diversification

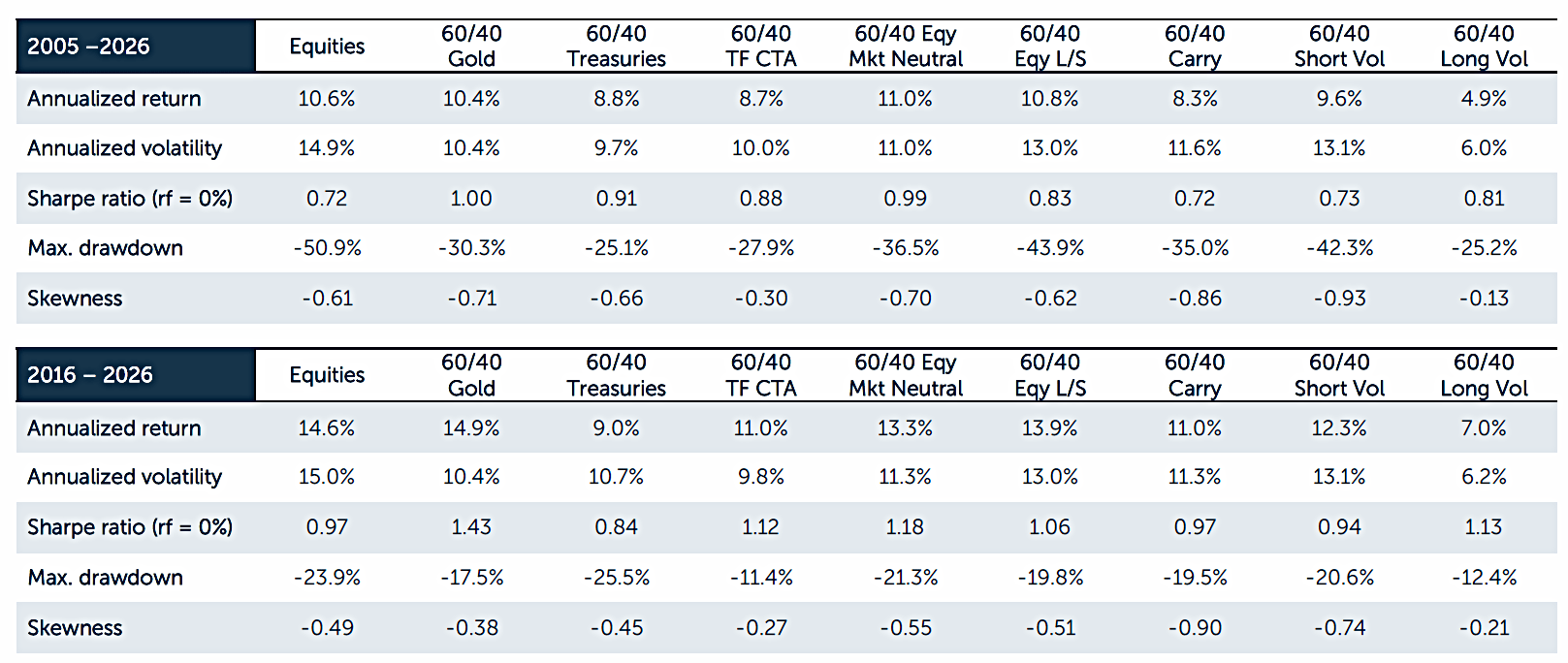

Since 2005, all eight diversifiers would have improved the [60/40] portfolio’s Sharpe ratio. However, none would have meaningfully increased absolute returns. Unsurprisingly, the stronger the downside protection characteristics, the larger the associated performance drag.

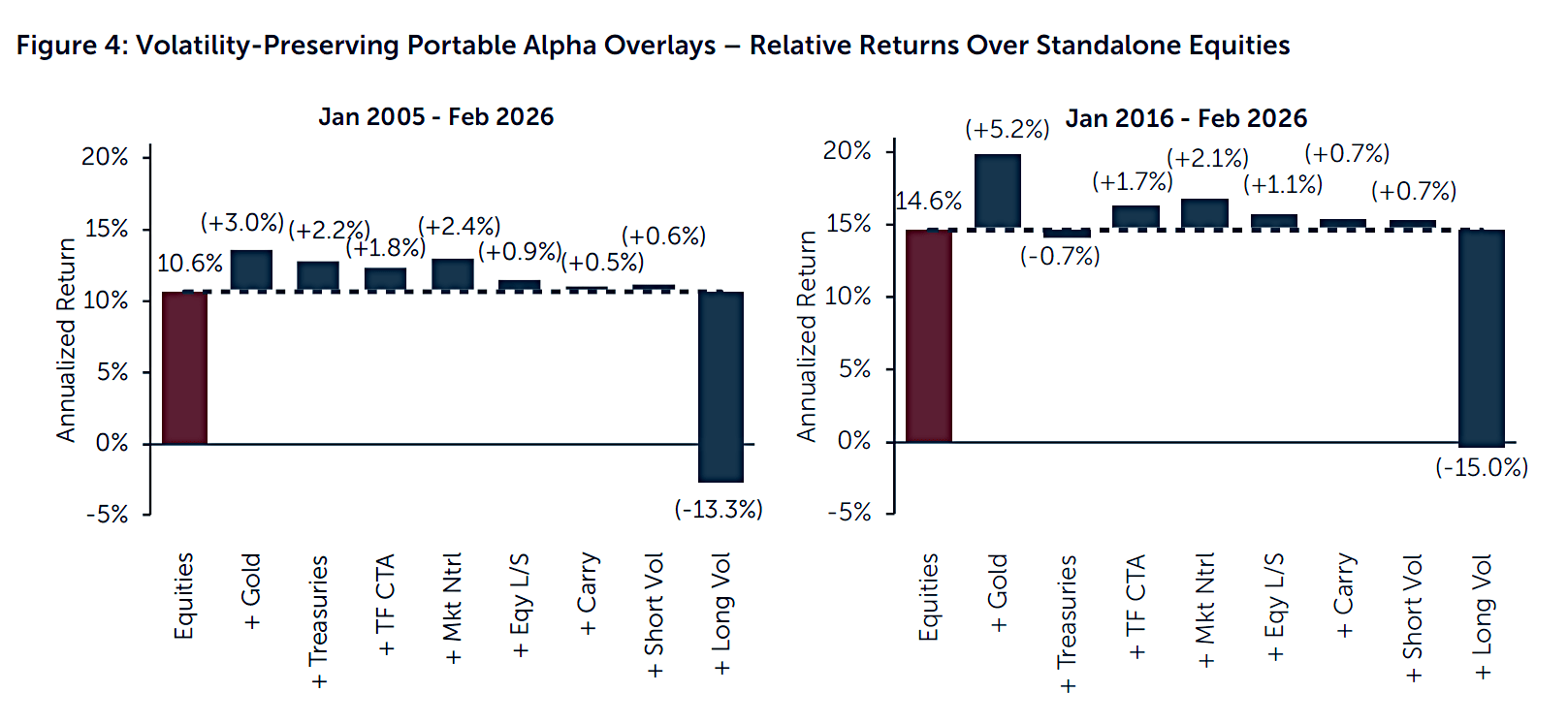

[In] the most recent decade, the performance drag from fixed-weight diversification increased for all candidate diversifiers except Gold. This largely reflects the exceptional performance of U.S. equities.

To counter this drag, Quantica suggests stacking the diversifiers.

Diversification can be implemented by layering the diversifier on top of the equity allocation – an approach commonly referred to as Portable Alpha.

We amateurs can call it leverage.

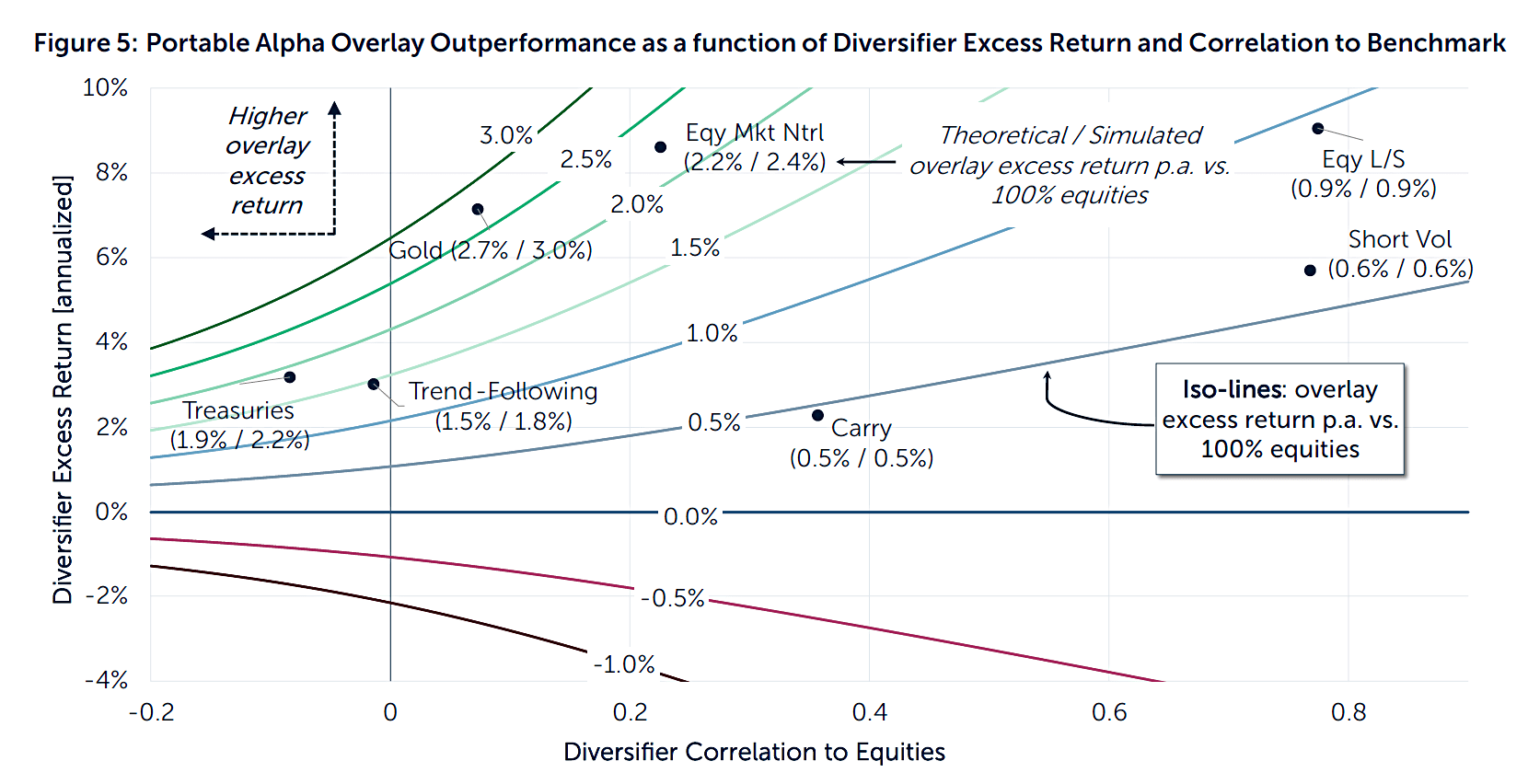

Quantica compares diversifiers by calculating how much exposure can be added to 100% equity without increasing annual volatility by a given “budget” (1% in the initial example in the paper).

- To calculate this, we need the volatilities of stocks and the diversifier, and the correlation between them.

It turns out there is quite a range of allocations when the diversifiers are normalised at 12% vol – from 202% (Long Vol) to 10% (Short Vol and Long/short equities).

- Treasuries are just below 60%, Trend is just below 50%, and Gold is just below 40%.

Portable alpha overlays using Trend-Following, Gold, and Treasuries would have outperformed a pure equity allocation by approximately 1.8%, 3.0%, and 2.2% per annum, respectively, over the past 21 years.

That’s pretty impressive for such accessible diversifiers, although the required overlays are much bigger than most DIY investors could tolerate.

Not constant over time

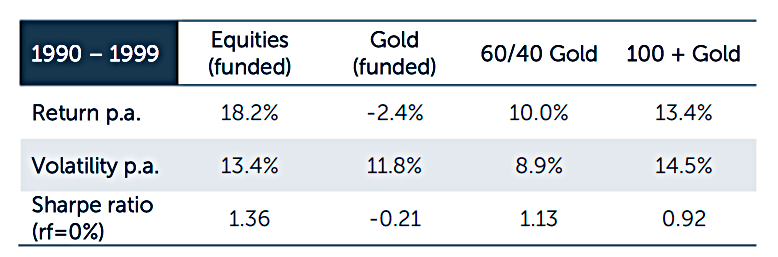

Quantica sound a note of caution around long-term historical context, using gold as an example:

The economic risk premium underlying many diversifier strategies is inherently cyclical and may expand or compress across macroeconomic regimes. Their effectiveness cannot be assumed to be constant over time, as the example of Gold illustrates all too well.

While Gold has delivered strong diversification benefits over the past two decades, its longer-term history includes the decade of the 1990s during which it would have detracted significantly from portfolio performance.

Correlations can also change (Treasuries would be a good example here), though they are generally more stable.

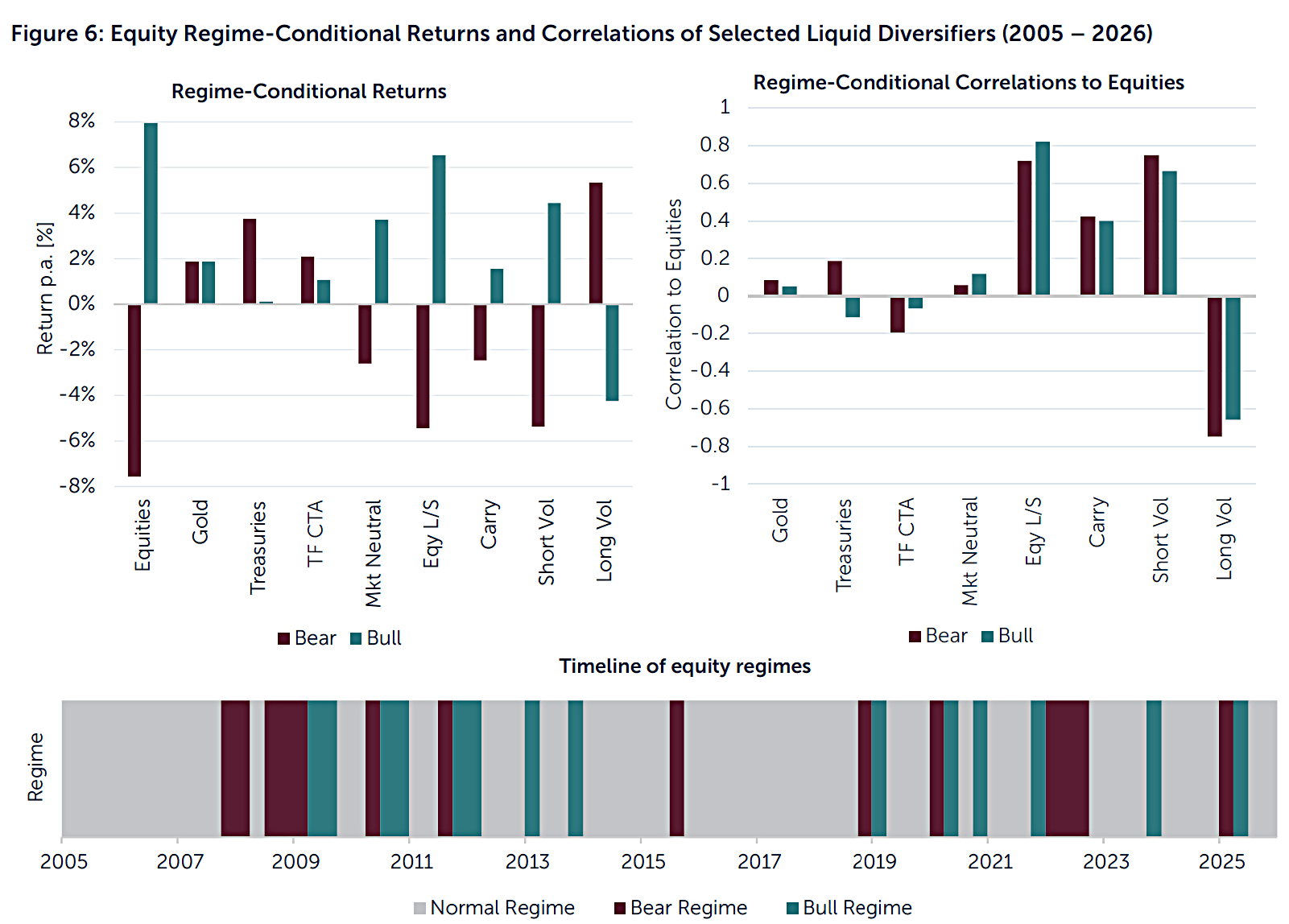

An Appendix to the paper examines the regime-conditional performance of the diversifiers:

Trend-Following and Gold displayed the most balanced trade-off between downside protection and long-term upside capture, delivering positive returns on average in both left- and right-tail equity regimes.

Trend-Following CTAs stand out in particular, having historically generated positive average returns while maintaining a negative correlation to equities in both bear and bull market environments.

Conclusions

The takeaways today are similar to those from the recent Return Stacked Portfolios note:

- We can only overlay so much portable alpha before we exceed our risk/volatility budget or our tracking error budget

- Returns comparable to stocks but with low correlations are the holy grail for diversifiers

- Treasuries, Gold and particularly Trend are the stand-out options,

- Luckily all three asset classes are available as ETFs within UK tax shelters (as are a few leveraged funds needed to make room for the overlays in the first place).

That’s it for today.

- Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.