Autumn Statement 2016

Today was new Chancellor Philip Hammond’s first Budget (technically the Autumn Statement 2016) and the first major UK fiscal event since Brexit.

Contents

Scene setting (before the statement)

What has he said to date?

Before the statement, all we knew was that he was planning a “fiscal reset” and that there would be a new plan for the new circumstances Britain faces”.

- This obviously means Brexit (which got him his job) but now also presumably means President Trump.

Most people also thought that he would want to make a point of distancing himself from George Osborne.

- Hammond has already abandoned the target of balancing the budget by 2020 and a few weeks ago he abolished the planned secondary annuity market.

He has said that he intends to bring the public finances “back to balance” eventually, but in the near-term he has talked about providing the government with “headroom” to deal with any Brexit fallout.

- He may also be instructed by PM Theresa May to take action to help families who are “just about managing” – now known as the JAMs.

Given that Hammond is the first Chancellor for a long time who is not auditioning for the role of PM, we could probably have expected fewer headline-grabbing gimmicks than usual.

What do the public finances look like?

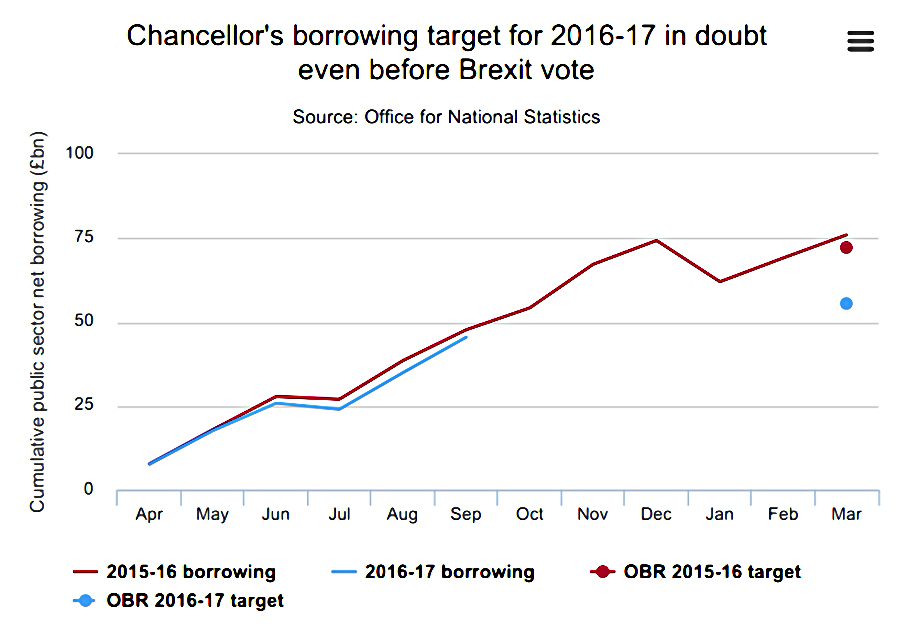

This week’s numbers were good.

- Borrowing fell on the back of higher receipts and higher spending.

- There was a big increase in Corporation Tax receipts.

But progress towards balancing the budget is slow (borrowing is down 10% YoY).

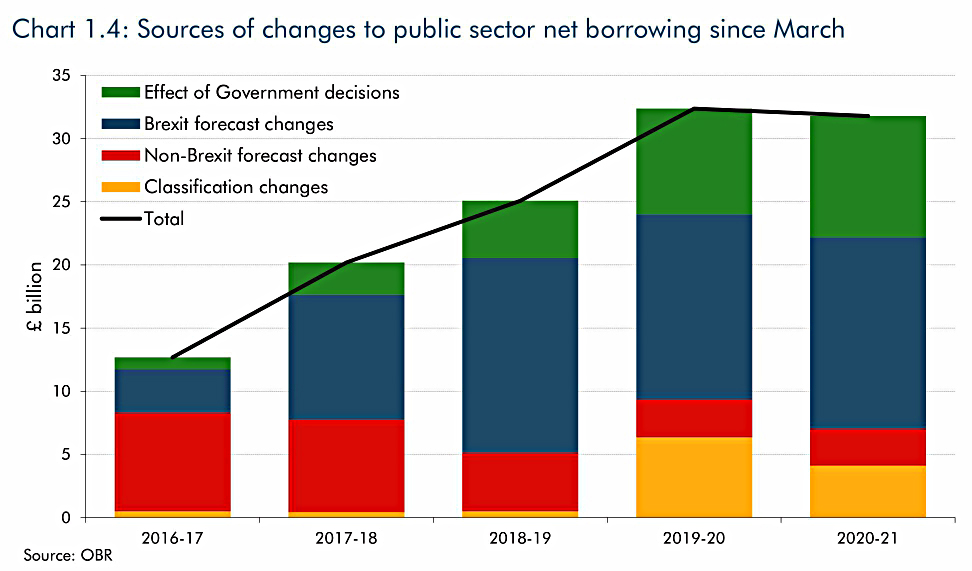

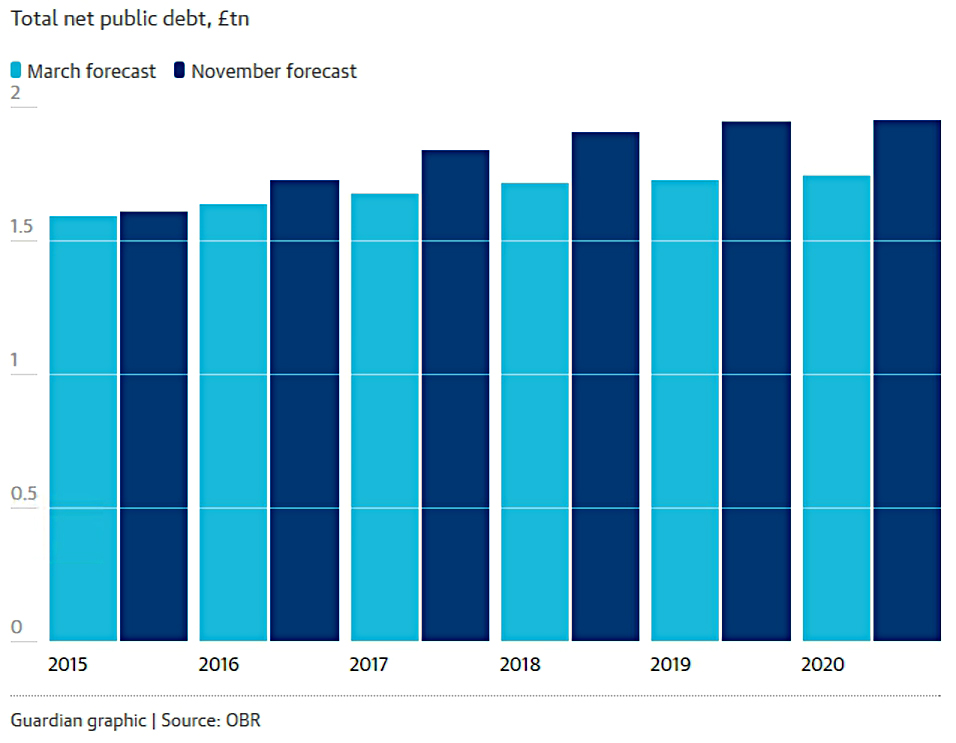

The OBR was thought likely to report a “deterioration” since the last Budget in the UK’s finances going forward.

- This has been reported by the hysterical mainstream media as a “£100 bn Brexit hole”.

Some of this is Brexit, some is changes to corporation tax calculations and the benefit system (rollout of universal credit, softer work capability tests for the disabled). (( Thanks to Notayesmaneconomics for a nice summary of the public finances ))

Here’s the chart from the budget document showing what’s changed since March:

But remember, all of this is a forecast – from the OBR.

- So it should be taken with a pinch of salt.

When looking at economics, data is useful, forecasts not so much (though as Buffett said, they reveal a lot about the forecaster).

We can predict higher inflation from the weaker pound, which is an obvious risk.

- But it will be counteracted by “fiscal drag” – the collection of taxes (eg. VAT) in nominal terms.

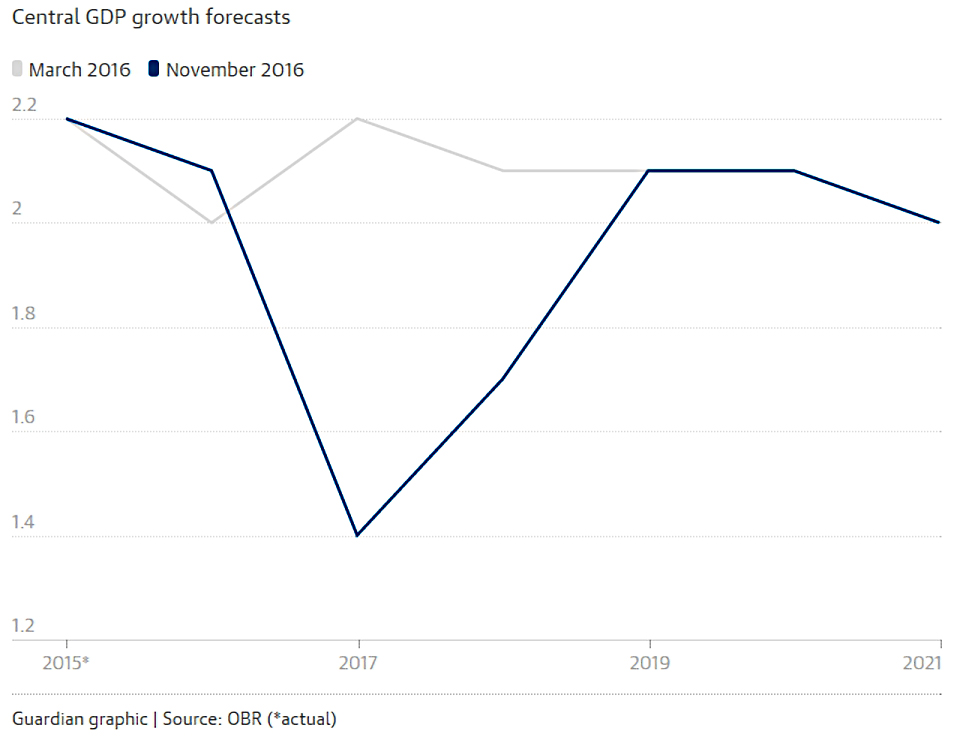

Hammond announced that growth would slow and inflation would rise over the next two years.

- But growth would continue to be positive, and employment would continue to rise over the next five years.

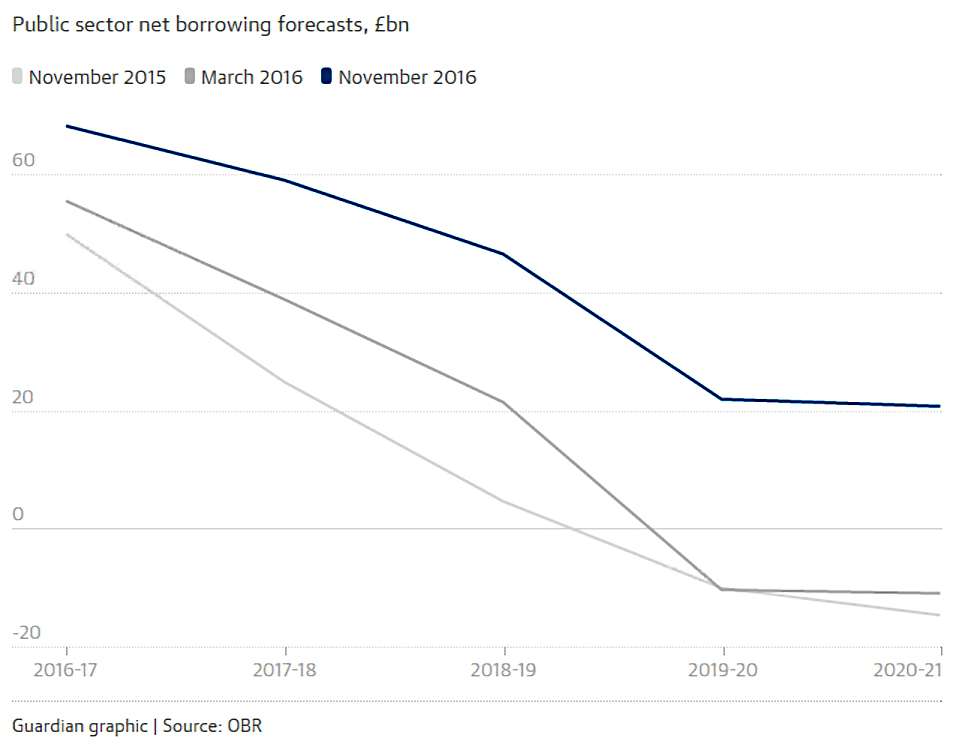

The deficit target was changed to 2% of GDP by 2020, with the national debt forecast to peak at 90% of GDP in 2017.

Public spending should come down to 40% of GDP in 2016 – still unsustainably high.

The Statement

Infrastructure

What we expected:

Everyone was banking on an increase in infrastructure – roads, railways and broadband.

- I would have liked to add energy provision to that list.

With interest rates still low (but possibly about to rise) now is a good time to borrow more over the long-term.

- That said, we probably shouldn’t have expected too much – Hammond has talked of “careful, considered and targeted investments”.

It was also possible that the Chancellor would announce changes to the way that these infrastructure projects are funded.

- Currently even some pensions often can’t invest because of rules about what proportion of their fund they can put into a single project.

Private investors can use infrastructure funds and investment trusts, but there had also been talk of infrastructure bonds to fund some of the projects.

- Unless these were underwritten by the government and yielded more than gilts, I can’t see the point.

- From the opposite direction, if those conditions were fulfilled, I can’t see the attraction to the government – the cost would be higher and the pool of potential investors smaller.

What we got:

Not quite what we expected:

- A National Productivity Investment Fund (£23 bn) that will spend on “transport, digital communications, research and development (R&D), and housing”

- This includes £27M for the Oxford to Cambridge expressway

- And £1.3 bn to reduce congestion and increase road safety

There’s also £390M on “future transport technology” – driverless cars, electric and hydrogen buses and taxis, plus more charging points for low-emission vehicles

- And £450M on digital signalling for railways, to improve capacity and reliability

- Plus £1 bn for more fibre broadband and trials of 5G mobile

There’s also a £2 bn R&D fund, and £1.5 bn for the Nations.

- The UK Export Finance capacity (( I’m not sure what this is )) will be doubled.

- And another £400M of Venture Capital will be injected via the British Business Bank – this could be unwelcome competition for VCTs.

Housing

What we expected:

Alongside traditional infrastructure, everyone expected a boost for housebuilding.

So far, a £3 bn fund had been announced to help smaller builders build 25,000 new homes (a drop in the ocean) by 2020.

- There’s also another £2 bn in loans to build another 15K homes on surplus public-sector land.

Many of these homes will be “affordable”, which the government defines as costing no more than 80% of the local market average to rent.

- For buying, mortgage payments should be between council house rents and market levels.

- This is an unsatisfactory definition, since it relies on interest rates and personal borrowing circumstances.

Some are starter homes reserved for first-time buyers under 40, with a discount of at least 20% to market value.

The Royal Institute of Chartered Surveyors (RICS) has called on the government to distinguish between developers (who need a land pipeline) and speculators “sitting on land only to sell on at a profit”.

- RICS would like to see brownfield (especially public-sector brownfield) and unused land freed up for building.

- Developers should only have two years to build after planning permission is granted.

Some simplification of the planning system for smaller builders has also been called for.

There’s also been the usual debate about the green belt surrounding London, and whether some of this should be freed up for housing.

- I’m not against this in principle, but the key is that the new houses should have good public transport links into London.

- If not, it’s just urban sprawl as seen in America.

What we got:

The main news is an extra £1.4 bn to build another 40K homes – far too few in my opinion.

- Plus £2.3 bn for a Housing Infrastructure Fund, to provide road and water connections to 100K homes.

- Plus £1.7 bn to speed up construction of new homes on public sector land.

Upfront letting fees have also been banned, which has hit estate agents shares.

Corporation tax

What we expected:

This was a tricky one.

- Hammond himself had dismissed Osborne’s plan to cut corporation tax to 15% as “just a suggestion”.

- He seemed more likely to stick to the previously announced target of 17% by 2020.

But in recent days, Trump has promised to cut US corporation tax to 15% (to match Ireland), and May has promised that the UK will have the lowest corporation in the G20. (( Hungary has announced a rate of 9%, but I doubt that we will match that ))

- So who knows where we are headed.

What we got:

Hammond pledged to stick to the cut to 17%, but didn’t promise to go any further.

VAT

What we expected:

There was speculation that Hammond might raise the rate of VAT.

- 20% is low for the EU (not that they are our natural comparator any longer)

- And if he did want to put it up, it would probably be best not to wait until too close to the 2020 general election.

Equally possible was a temporary cut in the VAT rate to boost the economy.

- And there was always the chance that some things would be added to the VAT regime, or exempted.

What we got:

There were no changes to VAT.

Stamp duty

What we expected:

Plenty of commentators were looking for a reversal to some of the recent changes to stamp duty:

- As well as the extra charge on second homes, the increases to rates at the top end of the market appear to be preventing a lot of over-60s in the south-east from downsizing.

- It could be that a specific relief would be introduced for those moving to a cheaper home.

The high rates at the top end (12% over £1.5M) are also causing that part of the market to lock up, with gradual implications for the layers below.

- But stamp duty receipts remain at record highs, so Hammond might wait for some evidence of market deterioration before he makes any cuts.

What we got:

There were no changes to stamp duty.

State Pension

What we expected:

Some people had called for the abolition of the triple lock (inflation, earnings or 2.5%, whichever is the largest) on the annual increase to the state pension.

- I think that the state pension remains too low in comparison with the living wage and the benefits cap (£8K, vs £15K and £20K respectively) for this to be fair.

The recent Cridland review of the state pension found that there would be no funding problem for many years to come.

- But that didn’t mean that there wouldn’t be a review of whether the triple lock should be extended beyond 2020.

What we got:

There were no changes to the state pension.

Personal pensions (SIPPs)

What we expected:

Tax relief on pension contributions “costs” the UK £34 bn a year, and most of that goes to high earners or those with DB plans.

- As usual, there was speculation that pension tax relief at your marginal rate of tax will be replaced by a flat rate relief for all, at perhaps 30% (mid-way between the most common marginal rates of 20% and 40%).

Hargreaves Lansdown (HL) had called for an age related relief (100 – your age, as a percentage), but this would have surprised me.

- The trouble with these age-related things (like the LISA) is that in reality they just help wealthy families who can pass money down to their children.

Others suspected that annual allowances would be trimmed once more.

- The annual allowance peaked at £255K in 2010/11 (hard to believe, isn’t it), but has been just £40K for the last two tax years.

There had also been calls for the Lifetime Allowance (LTA) to be abolished.

- The LTA has been cut from £1.8M to £1M in recent years, and with annuity rates at all-time lows, no longer provides an adequate pension for those wanting to retire early (before 55).

- £1M produces only around £20K of inflation-linked income.

One thing that was not expected to change was the 25% tax-free lump sum on retirement, at least not for those within 10 years of reaching 55.

Much more likely was the implementation of some of the recommendations from the recent review of salary sacrifice arrangements.

- Note that pension contributions were explicitly excluded from the review.

Some see this as a precursor to the merging of national insurance and income tax, but until we work out how to exempt those of state pension age from the NIC part of the combined tax, I can’t see this happening.

Another expected change was the pre-announced ban on cold-calling about pensions.

- Around 250 million scam calls are made each year (eight per second), costing £19M in losses to pensioners.

- Now callers will face fines of up to £500K.

What we got:

The ban on cold calling was announced, as were the restrictions on salary sacrifice.

The surprise was a cut in the Money Purchase Annual Allowance (MPAA).

- This is the amount of money that someone already drawing from their pension can pay back in each year.

- It’s been cut from £10K to £4K to clamp down on “pensions recycling”.

ISAs

What we expected:

ISAs were originally introduced (as PEPs, in 1989) as something simpler than pensions.

- You have an annual allowance that is lost if you don’t use it.

- You put money in after paying tax on it.

- You can take money out at any time without paying any more tax on it.

That was then.

- Now there are six flavours of ISA.

The latest – the Lifetime ISA, or LISA, which goes live in April 2017 – is the worst of the bunch.

- It mixes retirement objectives (age restrictions with penalties for early withdrawal) with housing objectives (it can be used as a deposit).

- It replaces tax relief with bonuses, and

- It introduces age restrictions (you must be under 40 to open a LISA, and must stop contributing at age 50).

- It also runs the risk of diverting investment from superior workplace pensions.

- It’s so unlike an ISA as to be one only in name.

HL has called for all the ISAs to be merged into a single “Super ISA”.

- It’s got to be better than what we have, though I would prefer that everything except the Cash ISA and the Stocks ISA were abolished.

What we got:

There were no changes to the ISA regime.

- The standard ISA limit will rise as planned to £20K in April 2017.

- The Junior ISA limit rises from £4,080 to £4,12.

We did get the announcement of a new NS&I 3-yr investment bond from “Spring 2017”

- But it only pays 2.2% gross pa, and each person is limited to investing £3K, so it won’t make much difference to anything.

- It works out at £66 of interest per person per year.

Allowances and other duties

Osborne had previously announced his intention to raise the tax-free personal allowance to £12.5K, and the higher-rate threshold to £50K, by 2020.

- Hammond was likely to stick with both of these pledges.

Fuel duty might be frozen, since the post-Brexit sterling crash has increased petrol prices significantly.

What we got:

Hammond confirmed the increase to the tax-free allowance and the higher rate threshold.

- The £12.5K personal allowance will be linked to inflation from 2020.

He also kept fuel duty frozen for the seventh year in a row.

- But he increased Insurance Premium Tax (IPT) from 10% to 122% from 1st June 2017

An increase in the living wage – from £7.20 to £7.50 an hour – was announced for April 2017.

- And the Universal Credit taper (the rate at which benefits are withdrawn as someone’s income increases – otherwise know as the poverty trap) will be reduced from 65% to 63% from April 2017.

Employee and employer National Insurance thresholds will be equalised (at £157 per week).

Hammond also confirmed that there would be no further welfare savings during this parliament.

And finally, he announced a swap between the Spring Budget and the Autumn Statement:

- In future the Autumn Budget will be the big dog, and the Spring Statement merely a response to OBR forecasts, with no major fiscal changes.

Impacts

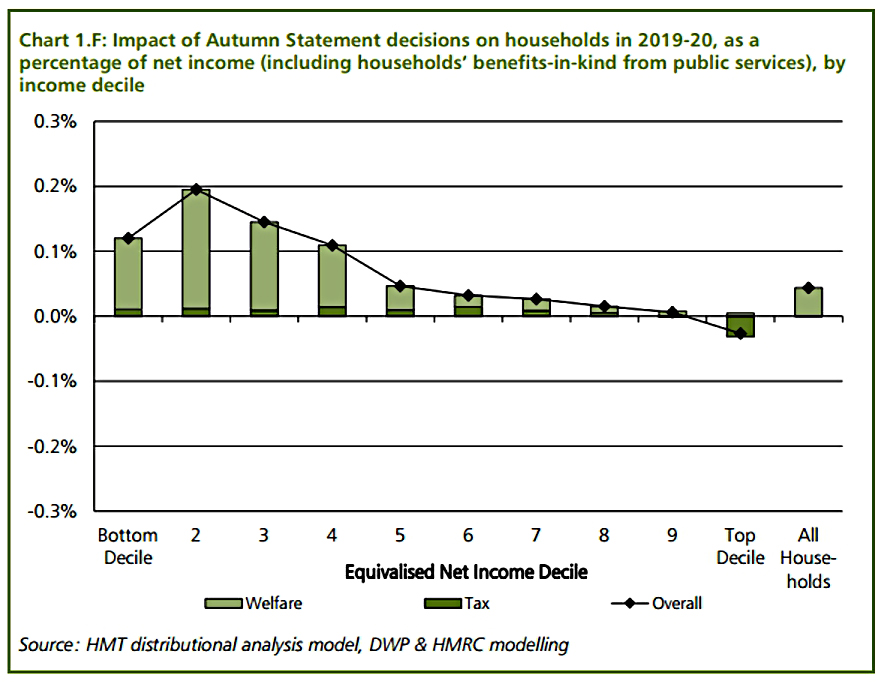

Alongside the budget document itself, the government also produces an impact statement on how UK households will be affected by the changes in the budget.

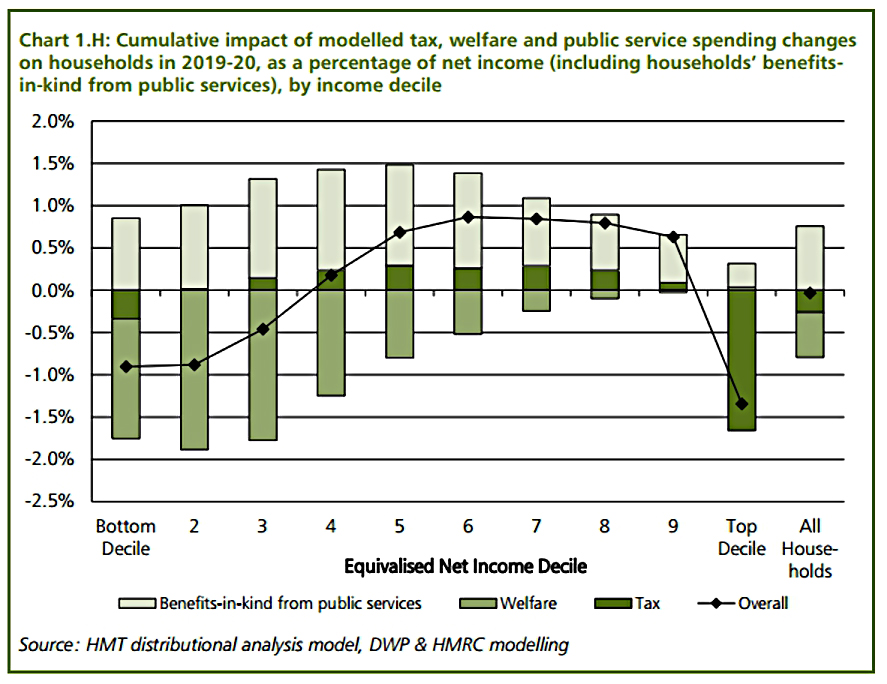

Here’s the impact in percentage terms in 2019/20:

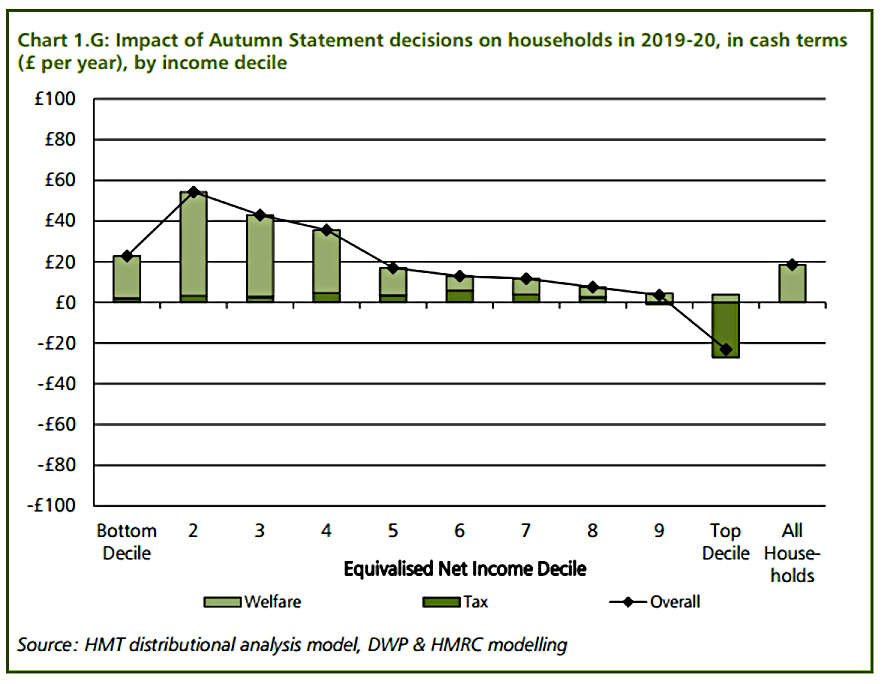

And here’s the same thing in cash terms:

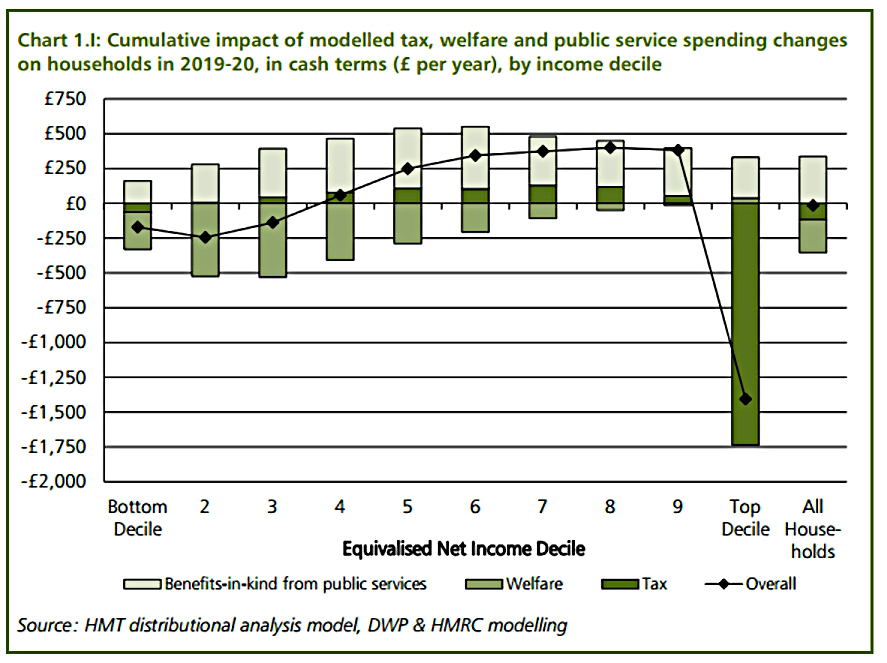

Here’s the cumulative impact over the life of the parliament:

And here’s the cumulative impact in cash terms:

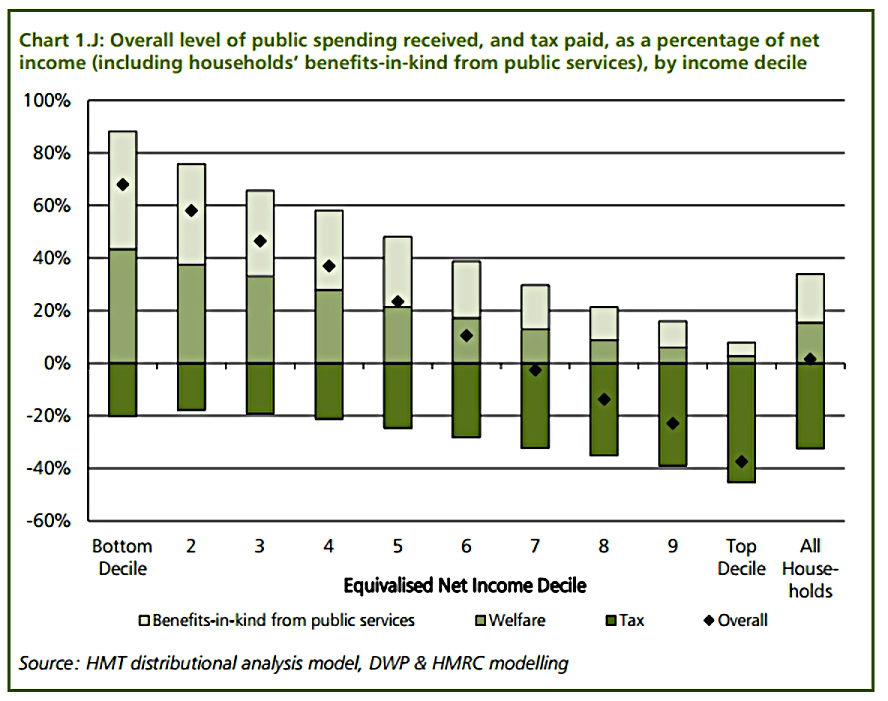

The final chart is the net contribution of households by decile:

- sixty percent of households are net beneficiaries

- the seventh decile contribute just 1% of income

- the top 30% are paying for everybody else

Conclusions

This was a very quiet Budget, with few big changes, and no surprises – in keeping with the reported personality of the new Chancellor.

- The infrastructure spending was underwhelming – no sign of HS3 for the Northern Powerhouse, for example, or more transport links into London.

- I’d also have to put it down as a missed opportunity to simplify our ridiculous tax system.

But at least he doesn’t appear to have made things much worse.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.