Econ 101 – Ten Principles of Economics

It’s back to basics today, with Econ 101 – an Economics primer that paves the way for a discussion of whether Economics works as it should do, and indeed, whether it is any use at all.

Contents

Textbook

I am often accused by my friends of sounding like a textbook. Well, today at least it’s true.

I had intended to write about a spat last year between Noah Smith (who writes a blog called NoahOpinion) and Don Boudreaux of Cafe Hayek (the clue is in the name).

- Noah wrote a piece for Bloomberg entitled Most of What You Learned in Econ 101 is Wrong.

- And Don replied with a piece called Most of What You Learned in Econ 101 is Right.

Econ 101

But before we decide whose side we are on, we need to know a bit about Economics.

I took Economics classes twenty-five years ago as part of my MBA, but it struck me that some of my readers might never have come across the dismal science at all. ((And to be honest, I’ve also forgotten most of what I learned ))

- So today is a refresher course.

Luckily, Noah named the Econ 101 textbook that he was thinking of.

- It’s called Principles of Economics and it’s by a professor from Harvard called Greg Mankiw.

[amazon template=thumbnail&asin=0538453427]

The copy I have is 848 pages long, but luckily the first chapter is a summary of the ten key economic principles. ((I’m also grateful to a presentation by Mark Karscig of Central Missouri State University, which summarises Chapter One very well ))

That’s what we’re going to look at today.

- And then next week we’ll examine the debate between Noah and Don, and everyone else who joined in.

Definition of Economics

The word Economics comes from Greek, and means someone who manages a household (older UK readers will be familiar with the vintage school subject of Home Economics).

Some of the decisions faced by an ancient household included:

- who will work?

- what goods will be produced and by who?

- what resources are needed to make these goods?

- what price should the goods be sold at?

- how much should we work, save and spend?

As you can see, these questions carry over well to the management of a country’s economy.

More fundamentally, resources (time, money, natural resources, things like food and shelter) are scarce – or at least, finite.

- Not everyone can have everything, all of the time – apart from in science fiction’s utopian futures (eg. Star Trek’s replicator).

Economics is about the management of – and the allocation of – these scarce resources.

- As we saw a few weeks ago, Economics is ultimately about “who gets what, and why” – a subject we shall return to in a later post.

Ten Principles of Economics

Economics looks at three areas in particular:

- how decisions are made

- how people interact with each other

- the forces and trends that affect the economy as a whole

We can group the ten basic principles under the three areas listed above:

- how decisions are made

- people face trade-offs

- the cost of something is what you give up to get it

- rational people think about marginal costs and benefits

- people respond to incentives

- how people interact

- trade can make everyone better off

- markets are usually a good way to organise things

- in some situations markets fail, and government can help

- the economy as a whole

- the standard of living depends on production

- printing too much money leads to price rises

- there is a (short-term) trade-off between inflation and unemployment

Trade-offs

There is no such thing as a free lunch

Or as I like to put it, you can only spend money once.

- You have to choose what you spend your money (and your time) on.

You can have more leisure time (and less work) but a lower income.

- Or you can work as hard as possible to earn the most you can.

You can eat in fancy restaurants but not have enough money for nice clothes.

- Or you can have Saville Row suits and eat in McDonalds.

In practice, some people can do both and some can do neither, but even these people face their own choices between what to do with their money.

This applies to governments as well as people.

For example, defence spending and overseas aid both use up money that could be spent at home.

- And protecting the environment takes resources that could be used to make people’s lives better right now.

Two principles involved with the allocation of resources are efficiency and equity.

Efficiency is avoiding waste and getting the most we can from resources.

- People find it fairly easy to agree on this one.

Equity is sharing out the benefits of these resources fairly across society.

- The problem here comes with the word “fair”, which means different things to different people.

Often there will be a trade-off between efficiency and equity.

- So you have to decide which is more important.

A good example is tax.

- Taking money from the rich (or, more realistically, from the middle classes) and giving it to the poor will improve equity (depending on exactly how and to whom the money is given).

- But it will impact efficiency since the return on hard work is reduced and the middle classes are de-incentivised to work.

- This in turn means that output from resources will go down.

The cost is what you give up

Every decision you take needs to involve an examination of the alternatives.

- If you want to go to college, not only do you have to take on a massive student loan, you also need to give up three years of earnings from the job you would have taken instead.

- If you want to live in London and be at the centre of things, you have to give up living close to your family. ((Unless of course your family lives in London ))

This is known as the opportunity cost – what you give up in order to have something.

- You need to know which things matter the most to come to the right conclusion.

The margins

People make decisions by comparing the costs and benefits of the available choices at the margin.

- They look at the small, incremental changes to their existing lives that the various options will make.

You can’t make a good decision by looking at one thing in isolation.

Incentives

When the marginal benefits of an option exceed the marginal costs, a person has an incentive to choose that option.

- This just means that their life will get better – as they see it – if they choose that option.

So a rational person – which is definitely not everyone – would make that choice.

- Looked at this way, improving your life is just a question of making a series of choices that lead to marginal – incremental – gains.

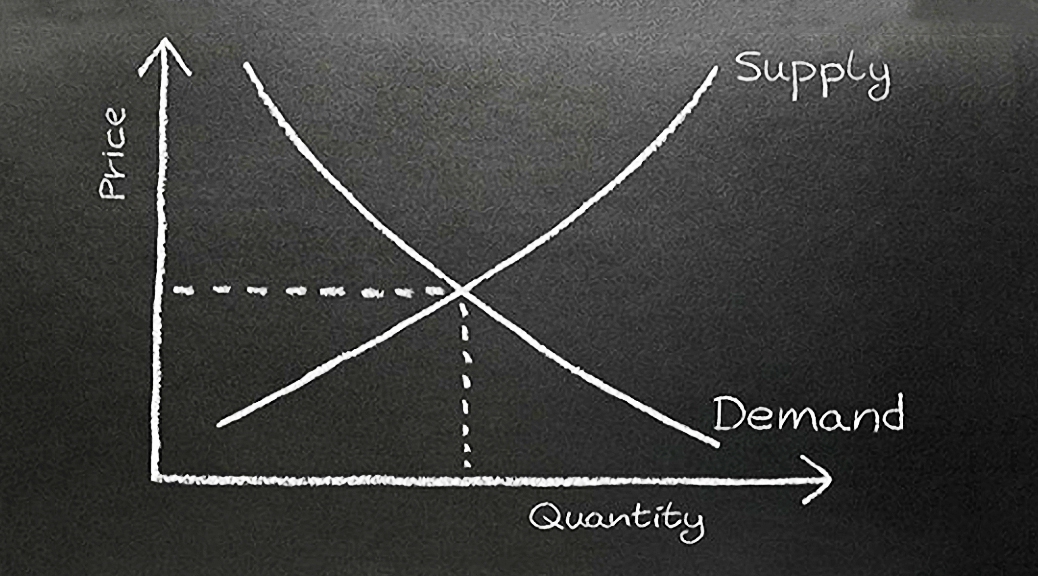

In economics, this leads things to like supply and demand, and the price curve.

When the cost of something goes up, people buy less of it.

- But producers will make more of it, since it its more profitable.

- Eventually the excess supply will lead to prices coming back down.

When the cost of something comes down, people buy more.

- But producers are making less profit, so they will make less of it.

- Eventually the shortage of supply will drive prices back up.

Things can also include unintended incentives.

For example, vehicle safely laws (seat belts, motorcycle helmets) can reduce the incentive to drive safely (since the consequences of an accident are reduced).

- This leads to increased risks for pedestrians.

Trade

For some people, self-sufficiency is the ideal to aim for.

- But in modern society, it’s an increasingly unattainable goal.

That’s where trade comes in.

The odd thing about trade is that both sides can gain.

- It is not a zero-sum game.

People tend to have a surplus of the things they are good at, and a shortage of the things they are bad at.

- This can mean that they value the thing they have a lot of lower than the thing they are short of.

- When they meet a person with the opposite perspective, they can both do well by swapping – trading – their extra stuff.

Marriage and relationships can work this way too.

Trade lets people and countries specialise in what they are good at.

- Where more than one person or company or country is good at something, competition between them leads to gains (lower costs, greater quality and innovation).

Markets

Markets are usually the best way to organise things – you only need to look at North Korea to see that.

In market economies, people (known in economics as households) decide what to buy and who to work for.

- Companies decide what to make and who to hire.

Both make decisions based on prices, and if things are priced correctly, they should reflect the social consequences of their actions.

- This would mean that the outcomes benefit society as a whole.

Adam Smith called this the “invisible hand” that guides self-interest into something that promote society’s economic well-being.

A corollary of this is that in general, government intervention in markets leads to decisions that are not based on proper price information, and hence to inefficiency.

- That’s why centrally planned communist societies don’t work so well.

Government intervention

But sometimes, things go wrong with markets.

- When a market doesn’t work properly (when resources aren’t allocated properly – known as market failure), the government can intervene to ensure efficiency and equity.

There are two kinds of market failure.

The first is that resources aren’t allocated correctly because of externalities (the effects on people or things outside the transaction)

- good examples of this are insufficient taxes to pay for pollution and climate change aspects of some activities,

- or the incorrect allocation of capital caused by the historically low interest rates that we currently operate under

The second kind of failure is driven by market power

- this is essentially a monopoly where a single person or company (or a small group of them) can influence prices (eg. keep them higher than they should be)

- this means that certain things (railway tracks, or a Land Registry) might be better off under government ownership

A second role for government is security and property rights.

- People are less incentivised to work, produce and invest if they risk their property being taken away from them.

Standard of living

The standard of living in a country is usually measured in terms of GDP (national, or per capita) or of household incomes (before and after tax).

- We’ve discussed the limitations of GDP before, and will so again in future, but for now let’s go with it.

This means that the standard of living in a country depends on its ability to produce goods and services.

Variation in standard of living between countries is largely down to productivity.

- This is the amount of goods / services produced by a worker in a given time (say an hour, or a year).

Money printing and inflation

Inflation is the increase in prices in the economy (usually year on year).

- If the government creates large amounts of money (through printing, or via a mechanism like QE) then the value of each unit of money falls.

The way to look at this is that there is more money chasing the same amount of stuff, so each unit of money is equivalent to less stuff.

- This means that you need more money to buy a unit of stuff, which is the same as the price in pounds going up – inflation.

This is particularly interesting today, as despite large amounts of money printing, no governments around the world seem to be able to generate inflation.

- Is this one of the ways in which Noah thinks that economics is wrong?

Inflation and unemployment

To get inflation down – should we ever need to in the future – usually involves measures that will increase unemployment in the short-term.

- But only in the short-term (normally one to two years).

I won’t go into the mechanics here. If you want more information, Google the Phillips Curve.

Conclusions

That’s it. You’ve competed your ten-minute economics course.

- Congratulations to any of you who are still with me.

Now you’re ready to get into the nitty-gritty.

- Next week we’ll look at what Noah said, how Don answered him, and what all the other commentators said.

I don’t find any of the above controversial, so it will be interesting to see what Noah thinks is wrong with it.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.