Modern Monetary Theory

Today’s post looks at Modern Monetary Theory.

Contents

Modern Monetary Theory

This post is the third in a series of four (previously three):

- In the first article, we looked at whether and why inflation has gone away

- Last time, we looked look at helicopter money

- In this article, we’ll examine Modern Monetary Theory (MMT)

- In the final article, we’ll look at other ways of dealing with the next recession

In the previous article, we defined helicopter money is a version of QE where instead of creating credit balances to fund bond purchases, money is directly transferred into the accounts of consumers for them to spend in the real economy.

For us, Helicopter Money is a temporary stimulus program that gets closer to the consumer than the traditional bond-buying of QE.

- Longer-term programs which credit the government to fund stimulus spending count as MMT, discussed today.

- The Job Guarantee is closely associated with MMT but will be discussed in a future post.

The issue of deficit spending, funded but the issuance of long-term bonds which currently attract historically low interest rates (and are therefore attractive to governments) is outside this debate.

- Similarly, permanent “state salaries” like Universal Basic Income have been dealt with in other articles already.

Both HM and MMT are intended to create some inflation, but not too much.

The distinction is largely to do with primary motivation:

- Helicopter money would be short-term and controlled by central banks using inflation and unemployment targets.

- MMT is (IMHO) a device to allow left-wing politicians to claim that there is a magic money tree.

Lineage

MMT has been all over the financial media over the last couple of years since left-wing politicians on both sides of the Atlantic (Corbyn, Bernie, AOC) began to name-check it in their speeches.

- It supports their ambitions to implement a large fiscal expansion to fund climate policies, universal healthcare (in the US), free college tuition and some kind of job guarantee / basic income for the unemployed.

On the other side of the argument, Robert Schiller, Ken Rogoff, Jay Powell, Larry Summers, John Tudor Jones, Larry Fink and Warren Buffett all think that it’s bunk – “voodoo economics”.

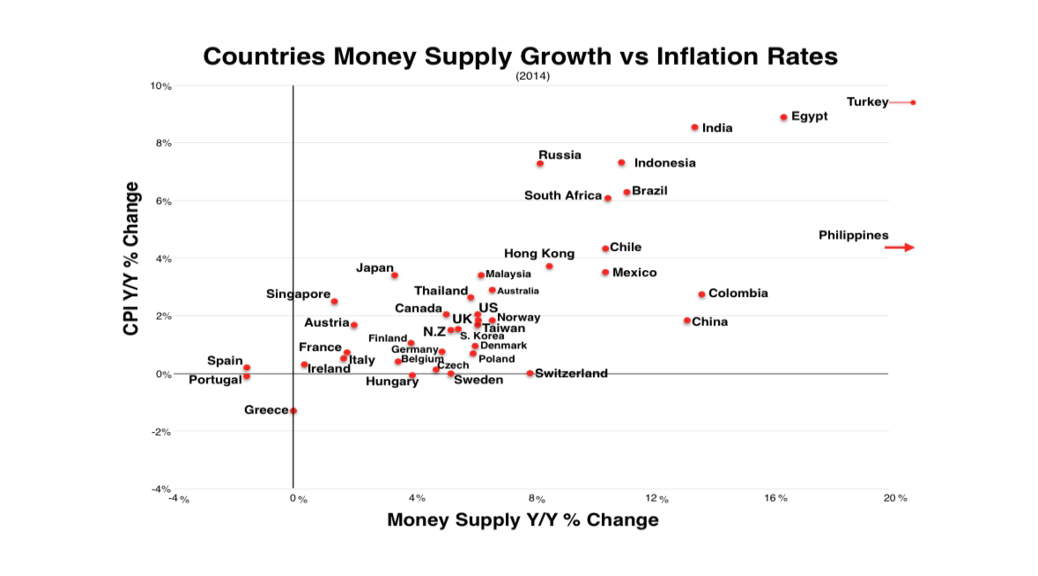

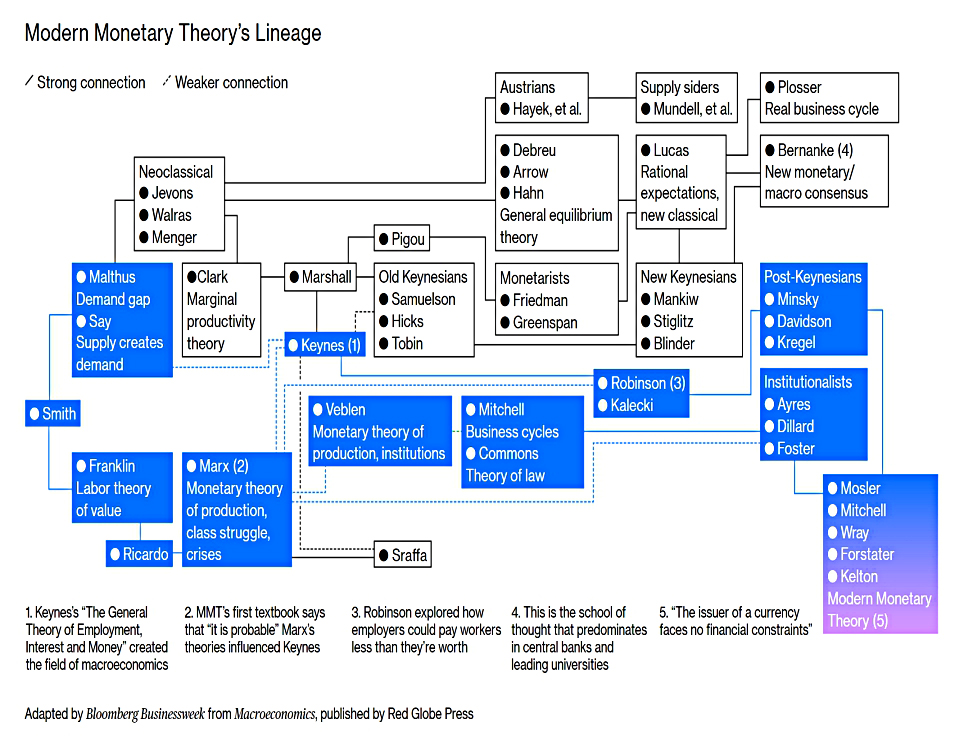

The theory (and its predecessors) date back decades:

This is not a history of economics lecture and I won’t attempt to explain that chart. (( Not that I could do a very good job in any case ))

- Similarly, the rest of this article will not be a deep dive into macroeconomic theory.

All I want to cover are:

- What do MMT fans think that non-fans don’t?

- What might go wrong?

- Is now a good time for MMT and how can we tell?

Central theory

The core belief of MMT is that a country with a sovereign currency (the US or the UK, say) need never default on its (sovereign) debt, no matter how much debt exists – or how large the budget deficit is.

- A true sovereign government has no foreign debt, is not resource-constrained, has a diverse output base, and so on.

- This is a small club of rich countries and not one that a country can choose to join.

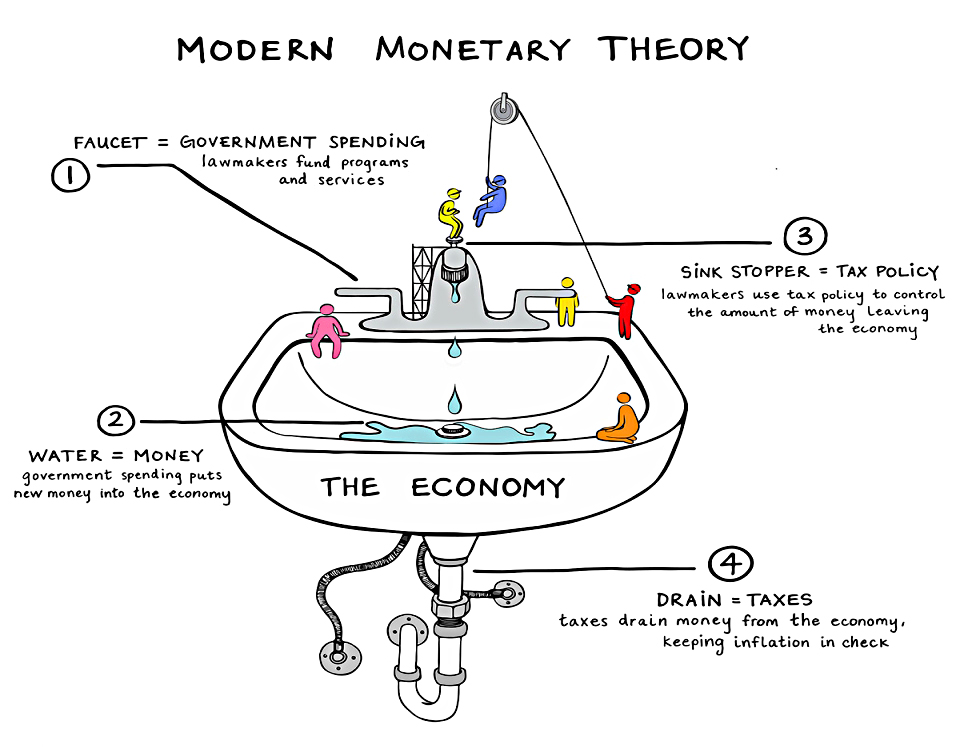

A sovereign government can always print more money to pay the interest on the debt, or to redeem it entirely.

- This money can also pay for any other government spending, so tax revenues become optional.

Another way of looking at this is that since the government has to issue money before the private sector can use it, the government spends first and taxes second.

- Yet another way of looking at it is that governments have economic credibility because of their ability to enforce (literally, if necessary) the raising of taxation.

- So a government that prioritises printing over raising enough taxes becomes less credible.

In practice, taxation would be used as a brake against inflation (see below).

Interestingly, taxes in a sense become the cause of unemployment because only government assets (money) can be used to pay taxes.

- Without the tax, no-one needs to work because they don’t need government money.

Banknotes (more generally, money) are/is not a public sector liability because the private sector can’t enforce a swap for another asset (traditionally gold).

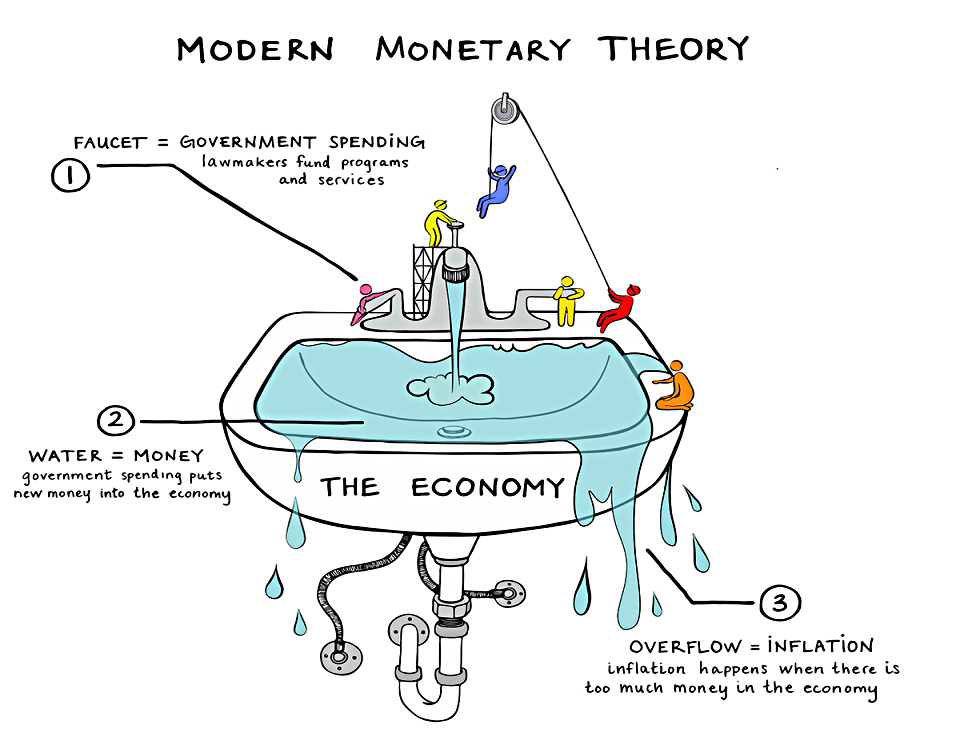

The downside of this money printing is that it could lead to inflation, and possibly hyperinflation and the collapse of the currency.

- It’s also likely that at some point, no-one would want the bonds of such a government.

Once long-term interest rates move above the growth rate of the economy, debt becomes unsustainable.

- Unless the government runs a budget surplus – which is not something you would expect from a government which has used MMT.

Philosophy

A letter in response to Gavyn Davies’ MMT primer in the FT highlights a philosophical difference between advocates and opponents of MMT:

- Anti-MMT types believe in the delivery of monetary policy by an independent central bank to ensure financial stability (low inflation) – so that asset prices are protected.

- MMT-types want full employment at a living wage with long-term environmental sustainability.

This distinction hints at the politics that comes bundles with MMT – supporters want to break up monopolies and introduce fossil fuel taxes.

- They want to break up and shrink the real estate, defence, and financial industries, too.

- Many want to see price controls, too.

In short, they think the government can make a better job of allocating resources than the market.

- If this sounds familiar, it’s because the last few attempts to implement socialism/communism (in South America) have looked a lot like this.

Even when the options are couched in the loaded language from the letter, I prefer option one.

- For one thing, I think the second option is unattainable (if environmental stability is to be achieved, it will have to be through the traditional tools of capitalism).

More importantly, without financial stability, we’ll be back in the stone age.

- And very few people know how to cope with those conditions anymore.

Formality

Noah Smith notes that MMT is guru- rather than model-based.

Most economic theories are collections of mathematical models. A good formal model can be compared with quantitative data, to see whether it works or whether it fails.

Formal models can make testable predictions. If you have to run to the gurus to ask them what the theory says any time you think you’ve found a flaw, it becomes almost impossible for to skeptics to evaluate the theory objectively.

I’m not saying that formal models would help private investors to get a grip on MMT (they usually involve hard maths) but they might have led to more criticism of the theory in the financial press.

- Then again, macroeconomics, in general, is pretty non-testable – it’s not a science.

But as John H Cochrane points out:

[MMT] is almost entirely a creature of tweets, blog posts, youtube videos, and so on.

When is an idea ready for widespread implementation in public policy? How much of the sociology of science should we wait for before spending trillions of dollars?

There are so many bad ideas out there, that I think the answer is, a bit longer.

Three kinds of money

As we all remember from the many recent critiques of cryptocurrencies, money has three functions:

- Means of exchange,

- Unit of account, and

- Store of value.

MMT focuses only on the first, which can be set by the state.

- But the most important is number three, which is set by the market.

Where are we now?

Because of the inflation risk, the weaker form of MMT is that is can only be used in a deep recession, with interest rates at the lower bound of zero.

- We don’t have a deep recession, but much of the world is pushing against the lower bound.

Note that another likely consequence of MMT is that the exchange rate would collapse, which would both bring inflation and likely lead to higher interest rates, moving the economy away from the lower bound.

- Hardcore MMT fans would argue the opposite – that the success of the “full employment” policies would lead to a strengthening of the FX rate.

But the key argument against using MMT at the moment is that the UK and the US are each close to full employment (if not full capacity, and in the absence of major wage inflation).

- Which means that MMT is likely to be inflationary (and financially destabilising).

So whether you are a fan or not of implementing MMT in the short-term probably revolves around whether or not you think we are close to full capacity.

- If you believe that there is equipment, people and resources that could be put to work to better society, and the main obstacle to this happening is a lack of government funding, then MMT could be for you.

So long as you also believe that the kind of government who would use MMT would then step back from it as the economy overheats.

Conclusions

MMT is based on the idea that control of the printing presses (and later on, of the men with guns) is everything.

But people have to want the money you are printing – they have to be willing to exchange it for real-world goods and services.

- When a company issues more shares, the price of each one will fall – unless the underlying activities of the company become more valuable.

This isn’t Field of Dreams – if you print it, they might not come.

- See Venezuela for more on this.

And even if MTT worked for a while when inflation inevitably emerged, and it was time to cut spending and increase taxes:

- Would politicians (who had been happy to use MMT) be prepared to make these changes?

- And would the electorate vote for policies that would make them worse off?

I’d rather not find out.

All of the “solutions” we’ve looked at so far (QE, HM, MMT) remind me of a series of pain-killers of increasing strength.

- We start with aspirin and ibuprofen.

- When that no longer works, we move on to codeine.

- And after that, we call for the morphine.

All along, the problem remains – how do we fix the underlying cause of the pain, and kick the drugs altogether?

I think that’s enough for today.

- But in researching this post I uncovered so much material that I think we might come back for at least one more look at MMT.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.