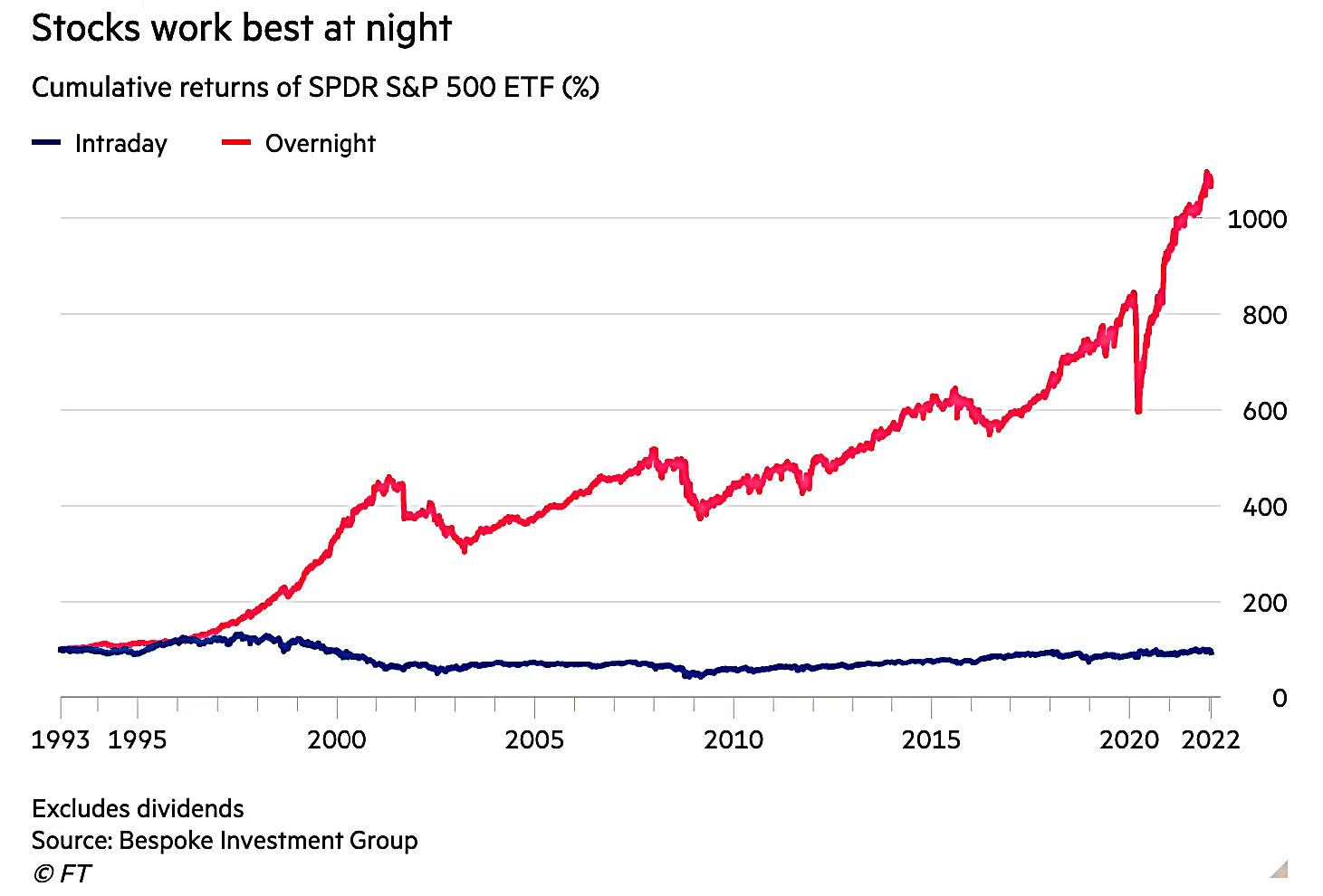

The Overnight Effect

Today’s post is about a well-known feature of the markets that has proven difficult to exploit.

The Overnight Effect

I came across the overnight effect a few years ago from a couple of articles by Robin Wigglesworth in the FT.

- Most of the gains in the US market occur after hours, when the market is closed.

- During the official opening hours, the market is largely flat, and in the morning returns tend to be negative.

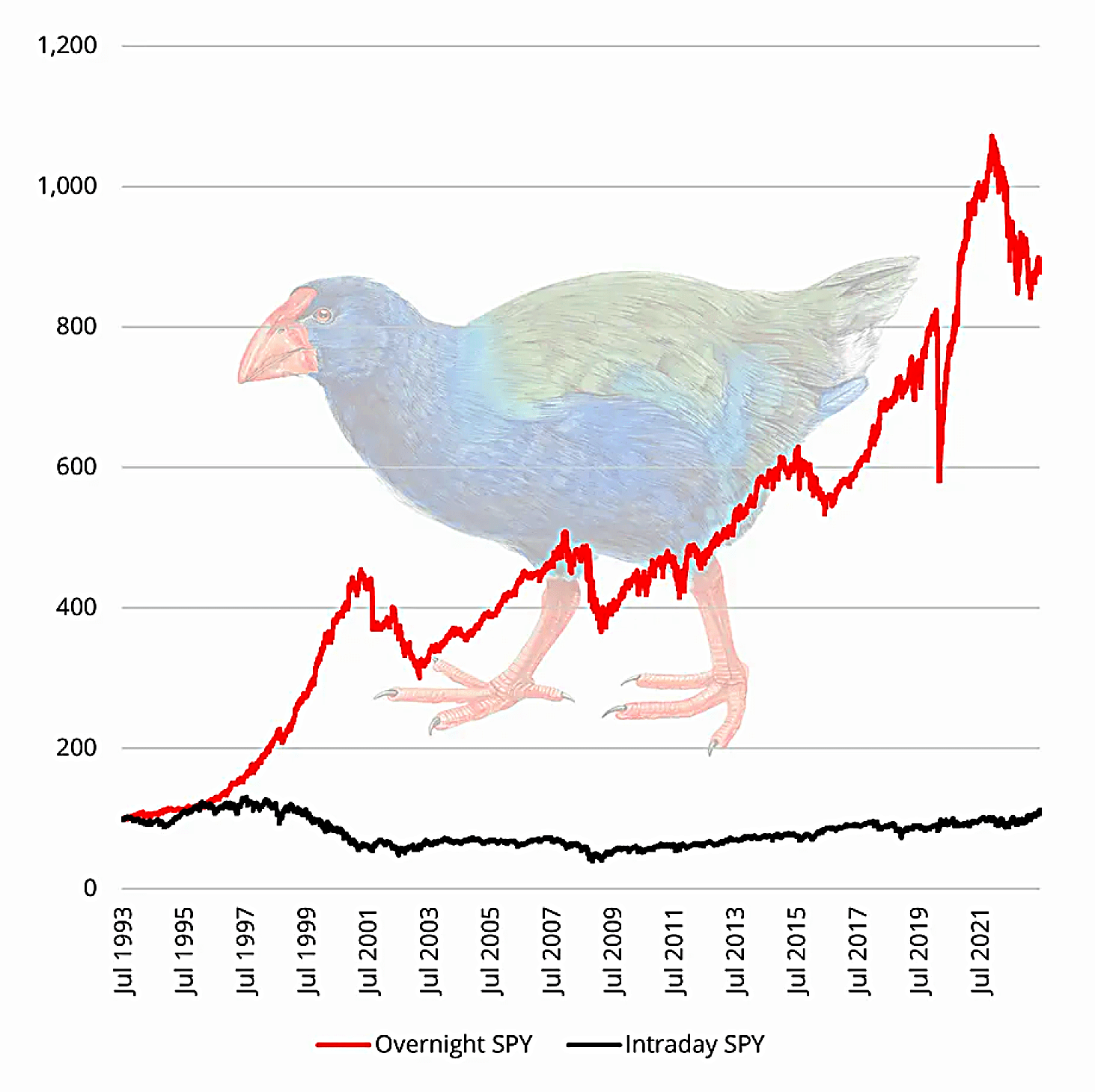

In fact, between 1993 and 2018 (when the New York Times mentioned the effect), all of the 571% gains in the SPY came outside regular trading hours.

- Daytime trading during this period lost 4%.

The effect has since been noticed in other markets, but not every market shows the effect to the same extent.

Why?

Robin’s first article (in 2022) covered a theory from researcher Bruce Knuteson that systematic market manipulation by quant hedge funds was responsible.

Quant funds take advantage of the bigger impact that trades can have when markets are closed and liquidity is thinner. They aggressively buy shares they already own, driving their price higher.

Since Knuteson used to be a quant analyst at DE Shaw, many found this conspiracy theory plausible. But perhaps something else is to blame:

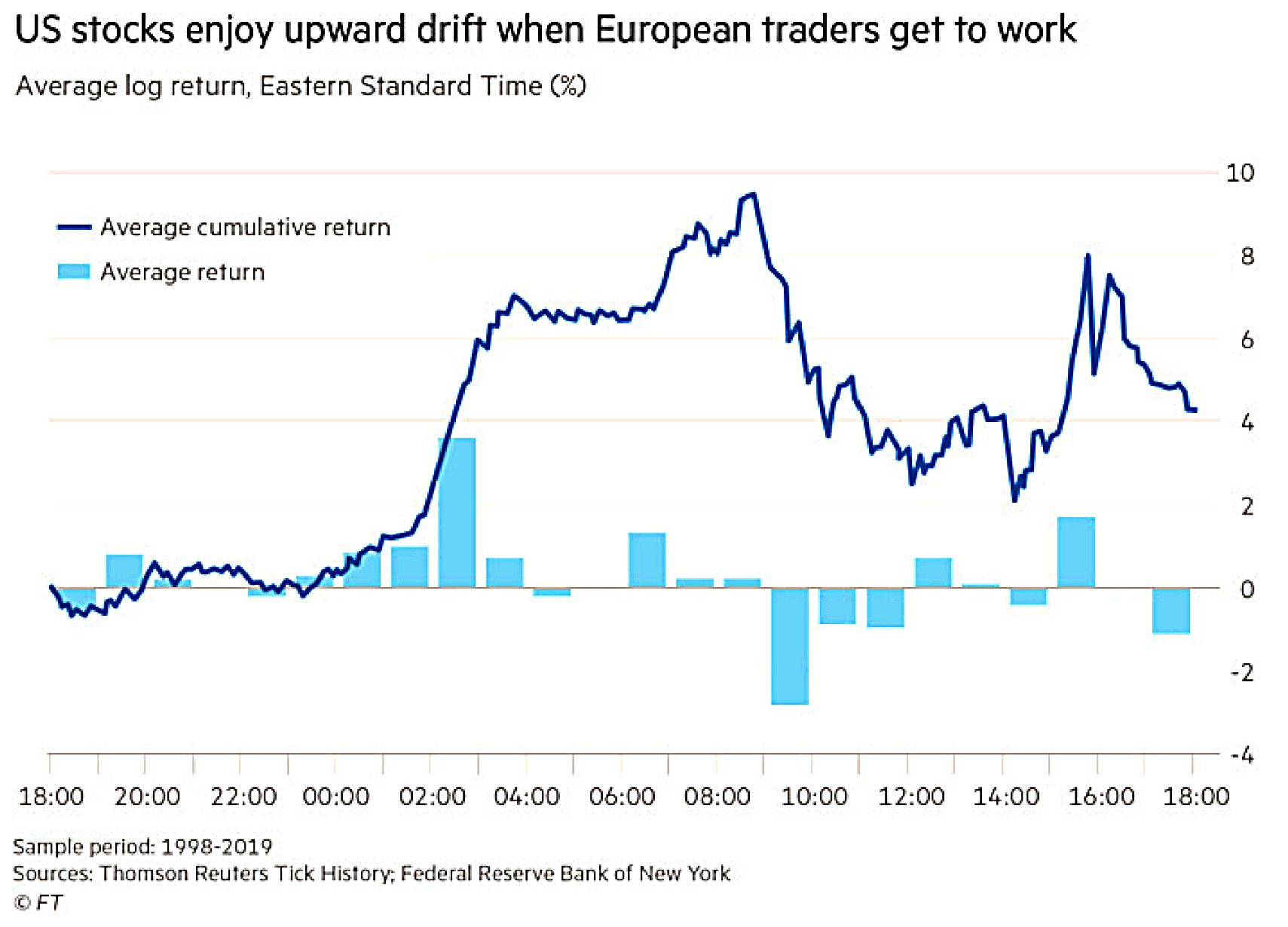

A New York Federal Reserve study of S&P 500 futures patterns showed that returns actually spike most notably between 2 am and 3 am in New York. This is roughly when European traders get to work.

Earning releases may also be a factor:

A quarter of US corporate earnings releases are published right after the market closes, and another 60 per cent before trading starts in the morning. Most companies tend to beat estimates and therefore enjoy subsequent price spikes in the overnight trading session.

Exploitation

Robin’s second article (in 2023) looked at how best to exploit the phenomenon. By then, there was an ETF employing the strategy.

In practice, the anomaly is impossible to easily exploit because of trading costs (liquidity is much lower overnight, and one-day holding periods would make it a high-turnover strategy). The NightShares ETF has actually lost almost 6 per cent over the past year, compared to the US stock market’s 18 per cent gain over the same period.

JP Morgan dug into the Fed paper and found one potential strategy:

The strategy takes a long position in the hours around European open if there is a negative order flow at market close. Results of this last variant are strong with a Sharpe ratio of 1.1.

But more interestingly:

Returns that are realised in the overnight period can be used to predict both the subsequent intraday and overnight returns. Specifically, high (low) overnight returns are followed by strong (weak) returns in the next day’s trading session, which are then followed by a reversal in the next overnight session. This overnight signal is sufficiently strong to overcome the high turnover and the associated transaction costs.

The daytime returns can also be used as a reversal signal for the following night and daytime returns.

Combining both signals looks good, and the system thrives in turbulent periods. JPM’s conclusion was:

Traders who are active during the time when the cash equity market is closed can be viewed as trend setters and demonstrate better skills.

Robin was dubious about the skill part:

A lot of investors probably look at what is up overnight and just jump on the bandwagon, irrespective of how sensible any nighttime moves are.

I would argue that it is still a skill.

JPM found that the strategy also worked for the Nasdaq and to a lesser extent, the Nikkei, but not in Europe (where only the overnight reversal works):

Given the leading role the US plays, some of the returns that are realised in the European daytime session are actually more akin to overnight returns.

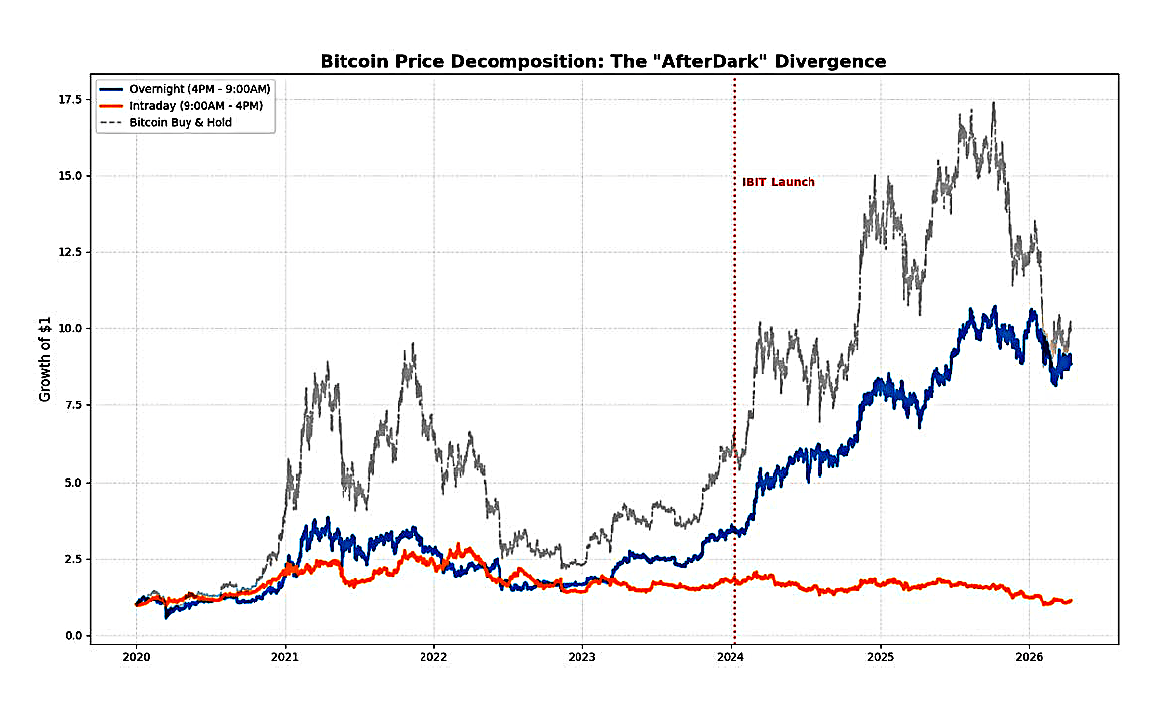

Bitcoin

Matt Levine reminded me of the overnight effect when he wrote about bitcoin in April 2026. He noted the failure of previous funds to make money from the effect:

In 2022, two exchange-traded funds (“NightShares 500” and “NightShares 2000”) were launched to profit from the anomaly, but they lost money and closed after a year.

Now a new fund has launched:

The Nicholas Bitcoin and Treasuries After Dark ETF (NGHT) made its debut on Wednesday. Since BlackRock Inc.’s iShares Bitcoin Trust ETF (ticker IBIT) launched in January 2024, overnight price gaps have generated a roughly 200% gain, a figure that outpaces a buy-and-hold strategy that rose more than 40%. Buying at the open and selling at the close [lost] more than 50%.

The fund will take long Bitcoin exposure via swaps at 4 p.m. Eastern time and exit by 9:30 a.m. the following morning. During US trading hours, capital rotates into short-termTreasuries.

Matt finds it funny that attempts to explain the effect in Bitcoin use different reasons:

Analysts have pointed to several explanations: global crypto-native capital trading during Asian and European hours; thinner overnight liquidity amplifying moves; and US-session selling pressure tied to ETF hedging, rebalancing and derivatives positioning.

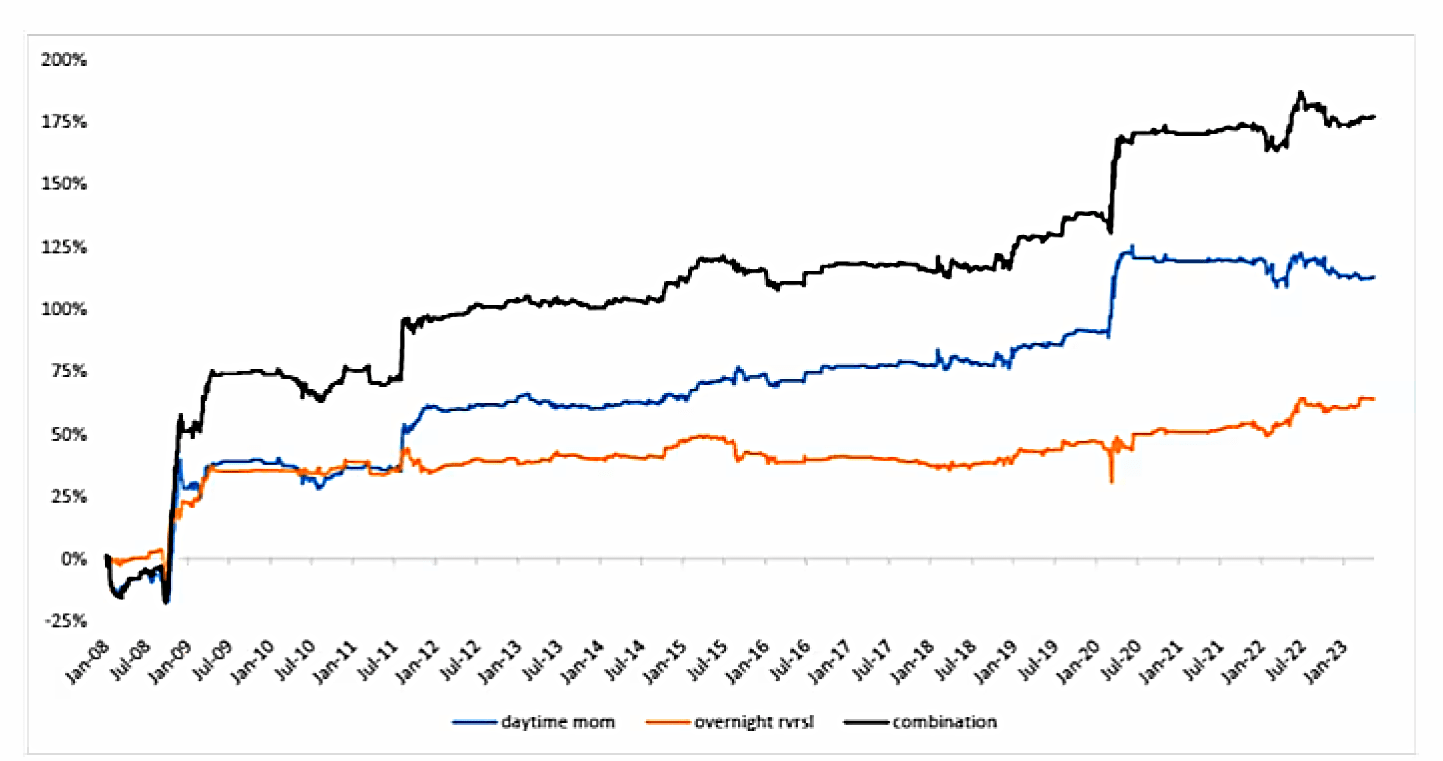

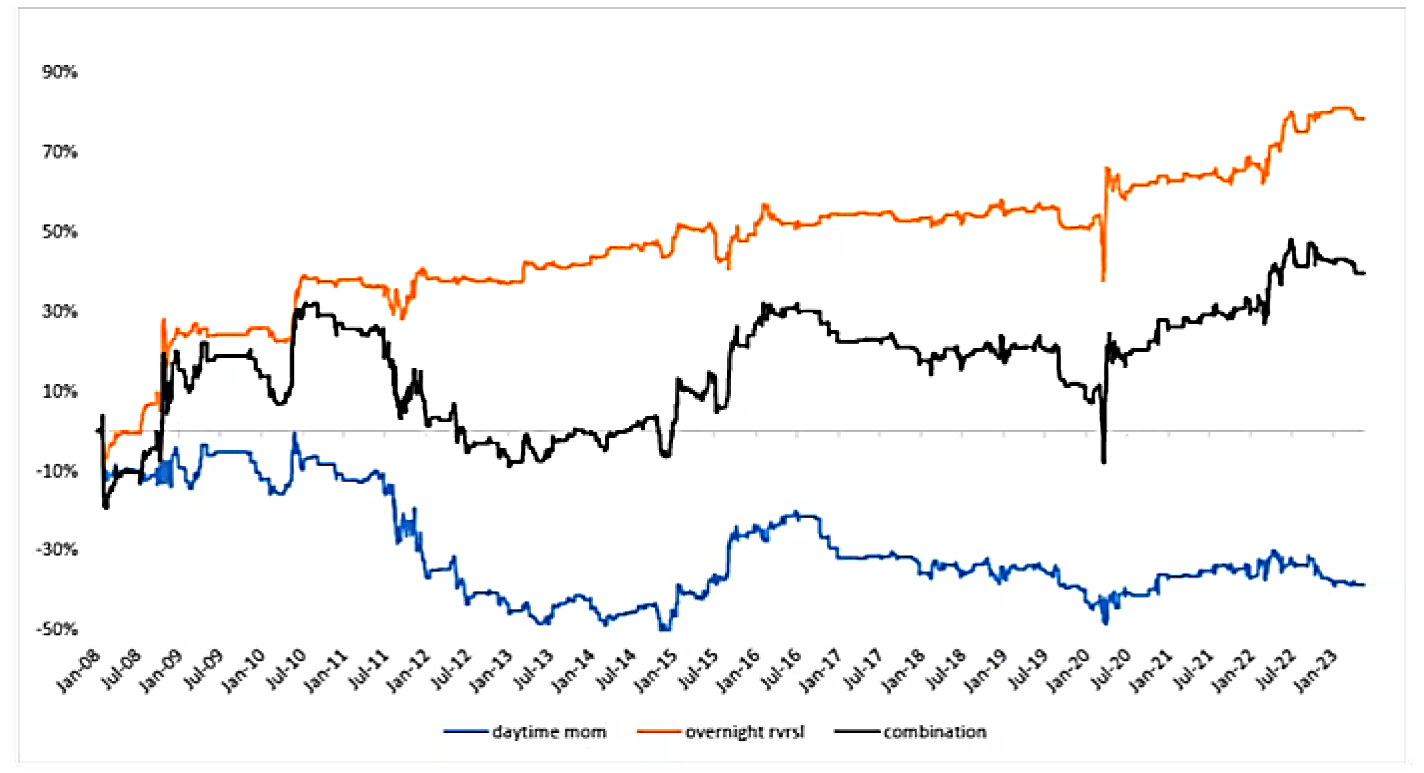

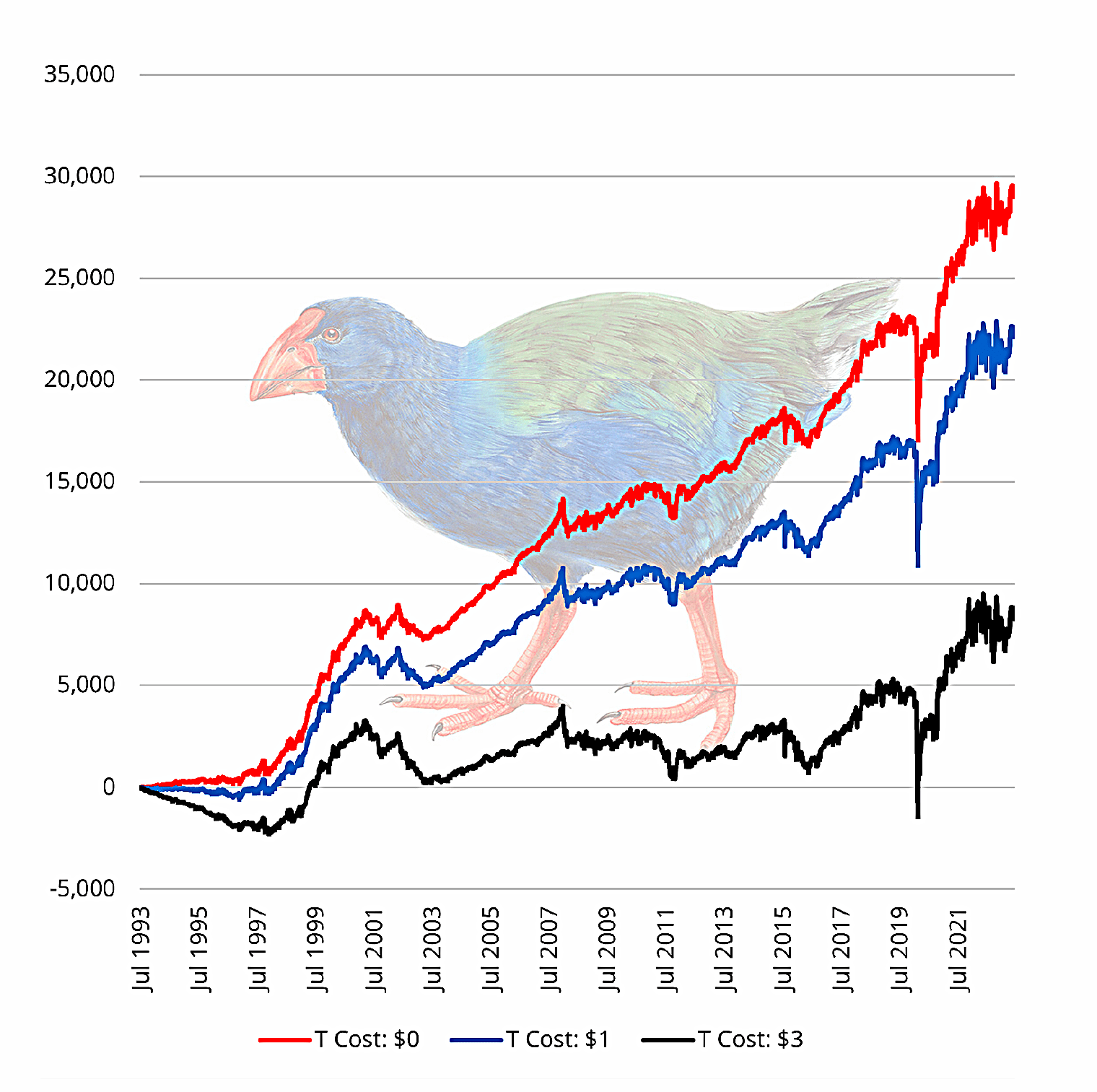

Trading the Night Effect

Back in 2023, the Two Quants (Moritz Seibert and Moritz Heiden) wrote an article in response to the first FT note, which discussed a couple of overnight trading systems.

More than 88% of the SPY’s overall return is due to overnight returns! However, the overnight performance is not a straight line, and the Night Effect wouldn’t have worked well during crises (see Covid, GFC, tech bubble). The overnight performance peaked in January 2022 and has deteriorated since then, maybe because the effect is now widely known and exploited.

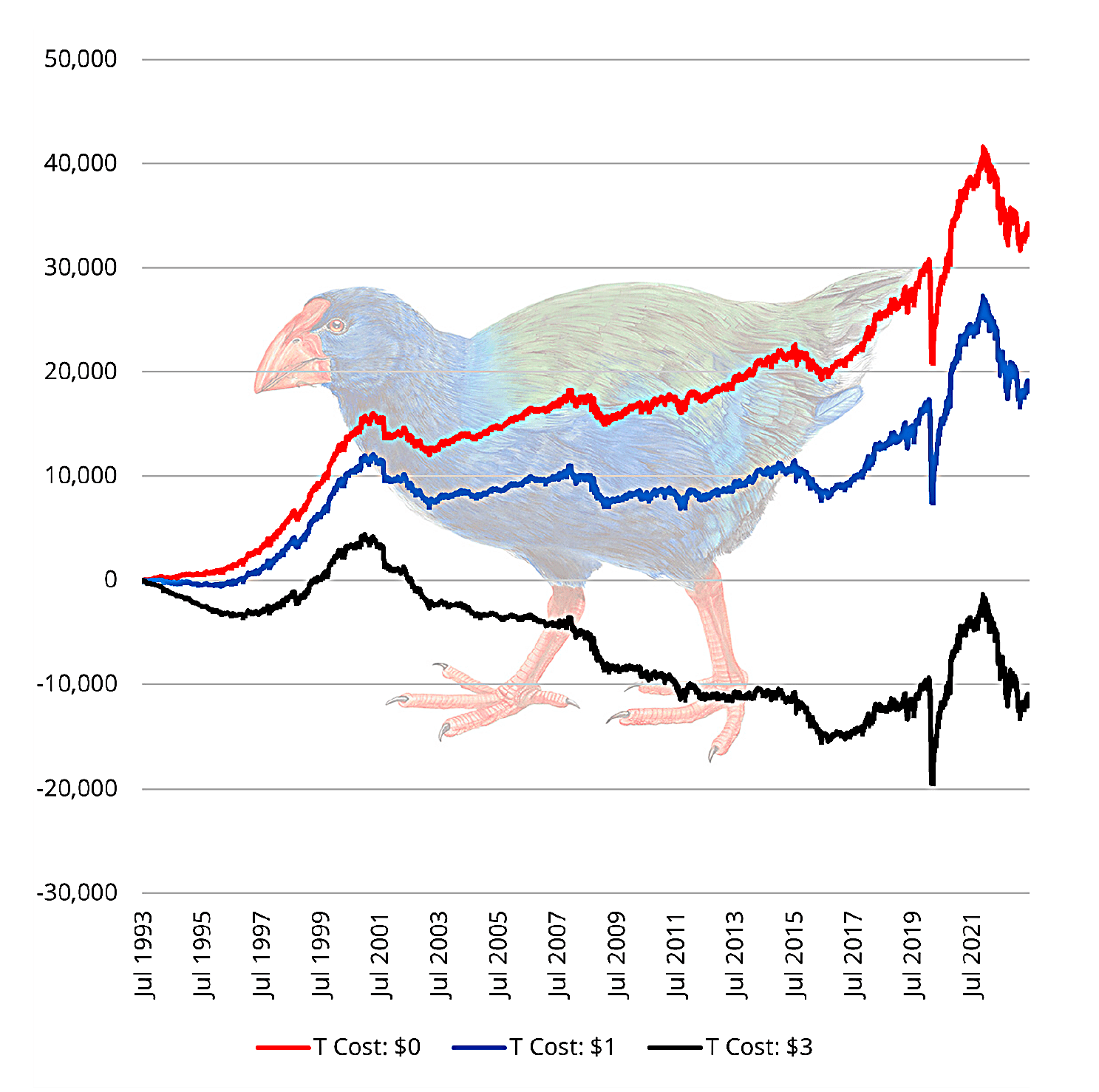

System one simply buys 100 shares of SPY (worth around $30K?) at the close and sells on the open.

This is profitable with transaction costs of zero or $1, but makes a loss if transaction costs are $3. (There’s no comparison with buy-and-hold returns).

System 2 uses a limit order to buy on the close, but only if today is a down day for the market. Sell on the open as normal.

- The limit price is yesterday’s close, to ensure we have a down day, but you could use a bigger “margin of safety” (eg. 1% below yesterday’s close)

This impacts profits where trades are free, but makes the $3 trades profitable.

Unfortunately, Two Quants (now Takahe Capital) didn’t take this system forward:

Historically, the Night Effect has produced a negatively skewed return distribution as it exposes the trader to the left-tailed equity risks. We aim to do the exact opposite at Takahē Capital, i.e., take advantage of outlier moves and thrive in the tails, which is why we are not interested in trading strategies such as [this].

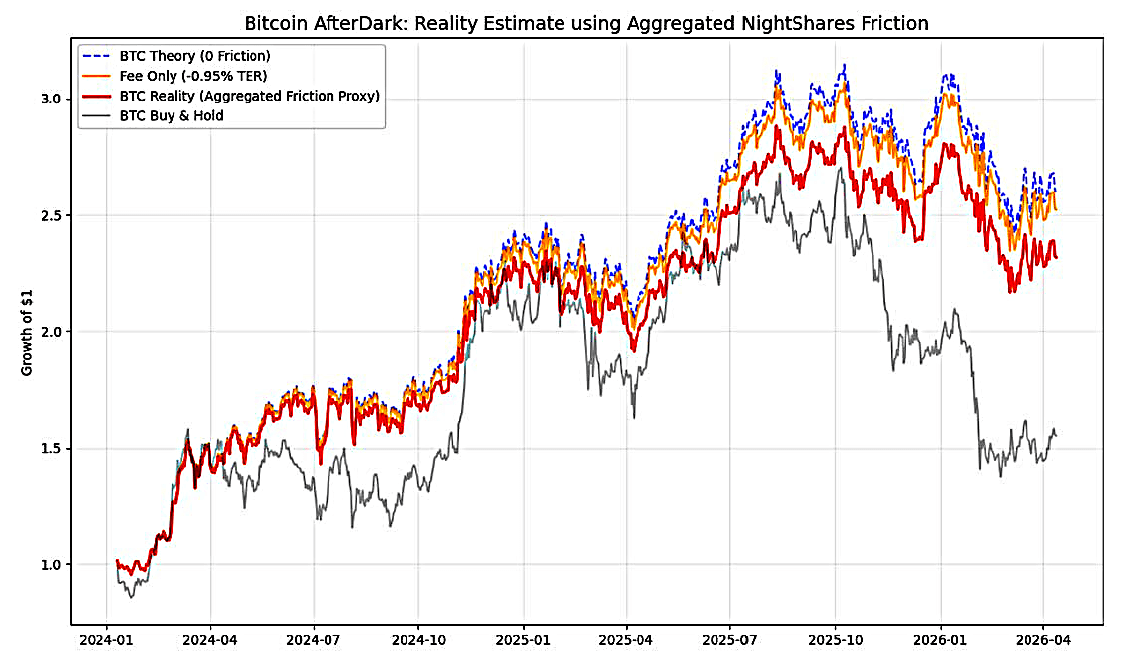

Good night, sweet IBIT

Two Quants returned to the overnight effect this year, after Matt’s article on Bitcoin.

They have run the numbers on the new ETF:

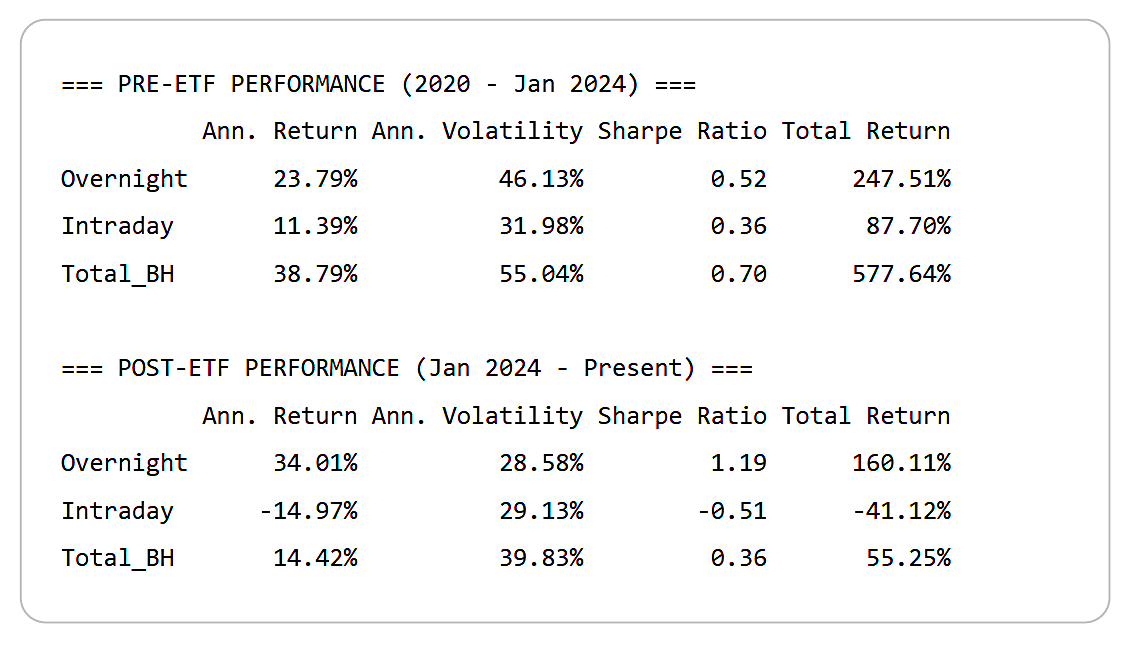

Overnight is more profitable than intraday, but intraday is positive, so buy and hold beats both.

- The overnight effect has been much stronger since the IBIT ETF was introduced.

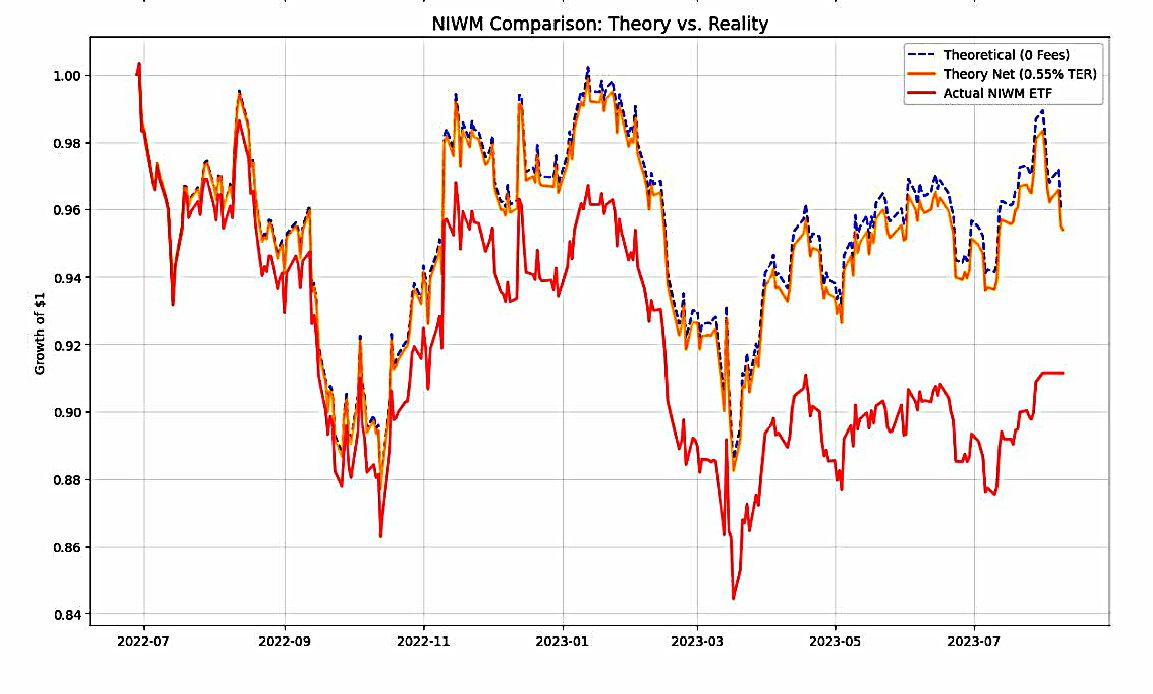

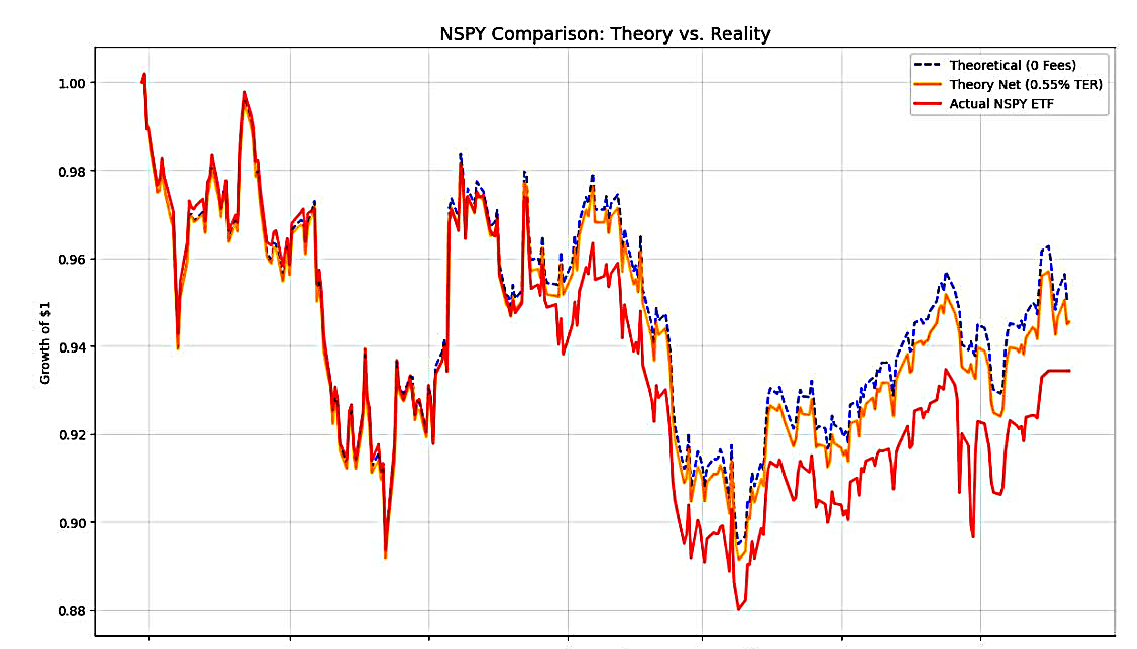

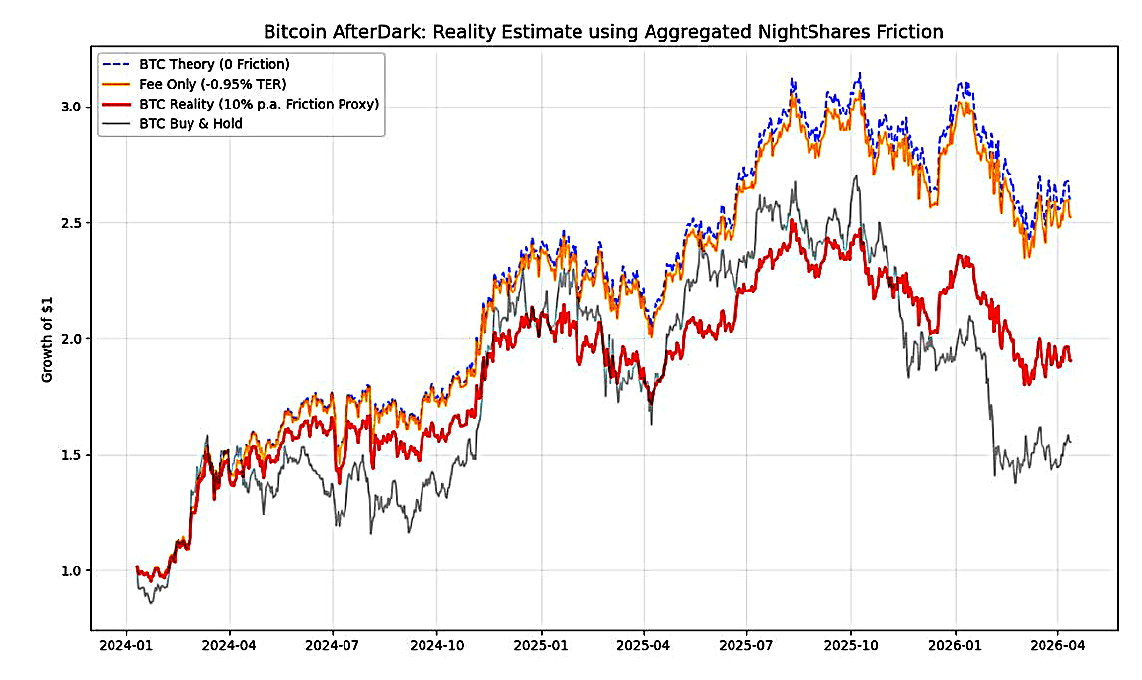

To look at the impact of costs, Two Quants used the old ETFs:

Both ETFs significantly underperformed the theoretical returns, even after allowing for their TERs.

- Two Quants note that the ETFs were alive during a bad period for the overnight effect (in SPY).

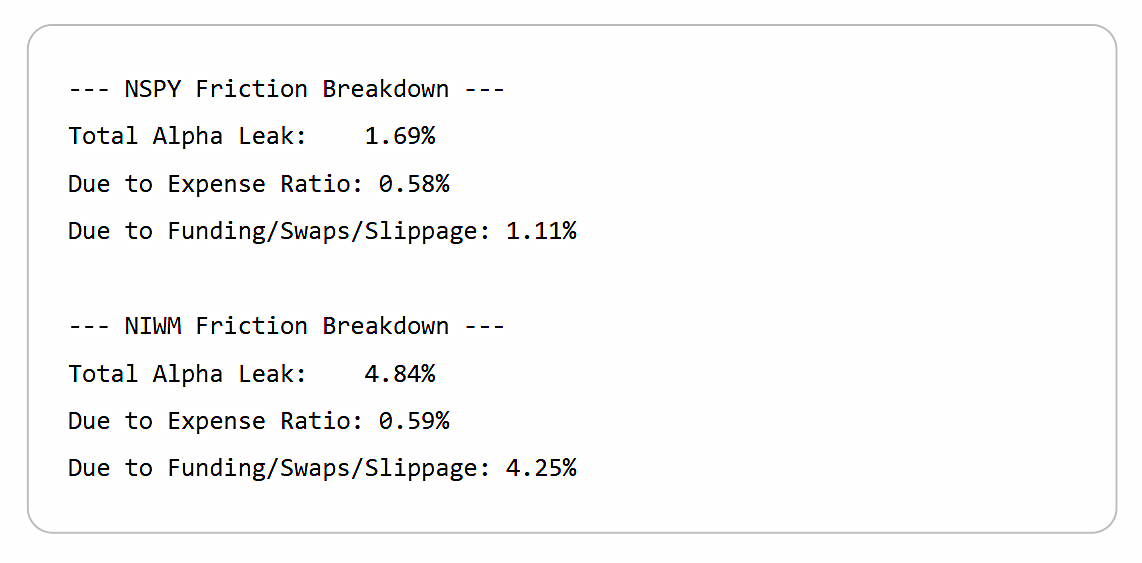

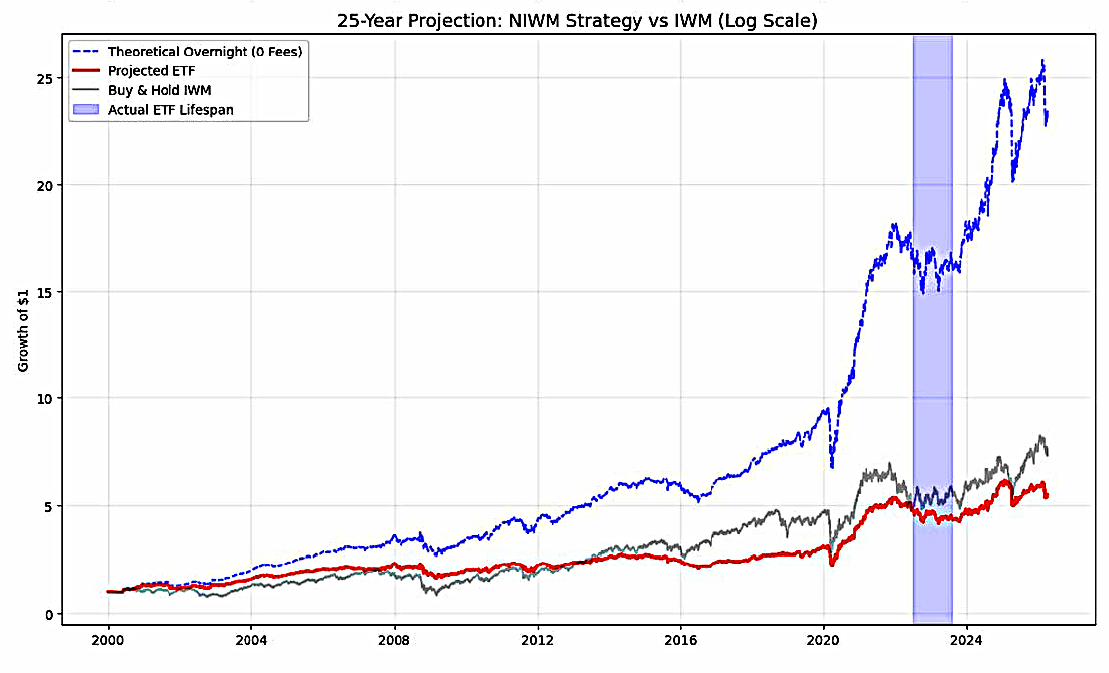

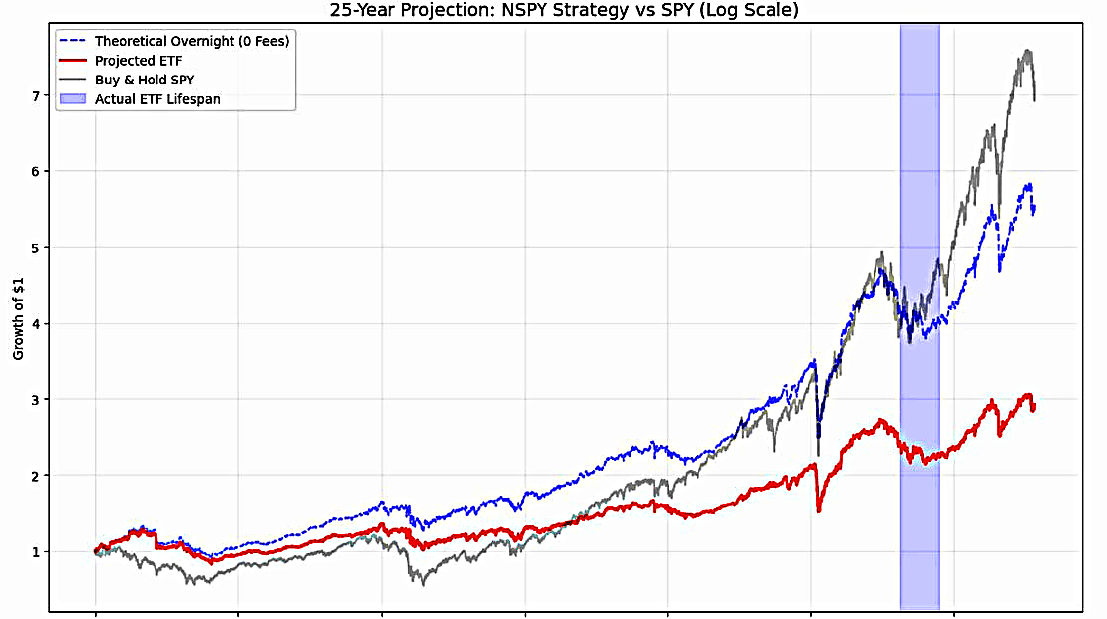

Using the alpha leakage from their live period, Two Quants projects how the ETFs might have performed over 25 years:

We see two things:

1 – Timing was really bad for both ETFs. The period itself was mixed for buy& hold in the underlying as well as the theoretical overnight return.

2 – Costs destroy even the best theoretical performance. Overnight IWM looks great on paper, much better than IWM buy & hold – but terrible if we account for costs.

But all is not lost for the Bitcoin ETF:

If we assume a conservative annual drag of 3.59% (based on a mean of the NightShares friction + the 0.95% fee), the strategy still looks attractive.

But in fact, costs for a volatile asset will be higher than for SPY. Yet even with a 10% drag (2x the NIWM friction + fees), the ETF still beats buy and hold.

That’s it for today.

- It’s been an interesting journey, but I’m not sure that I’m any closer to profiting from the overnight effect.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.