Weekly Roundup, 28th March 2017

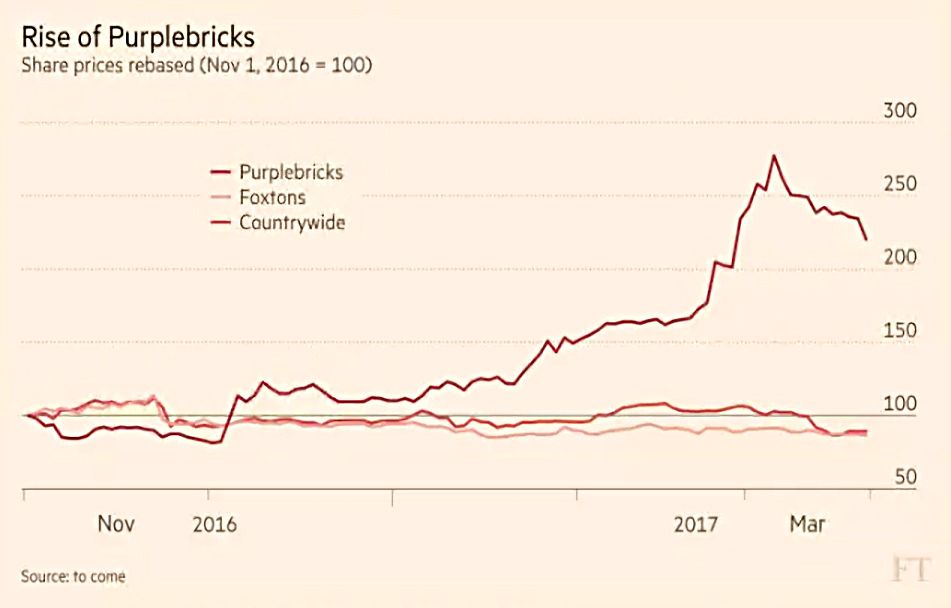

We begin today’s Weekly Roundup in the FT, with The Chart That Tells A Story. This week it was about Purplebricks, the online estate agent.

Contents

Purplebricks

One of the main events of last week was the publication of two government reports into the future of the State Pension.

- I’ll have a separate post on this topic later this week, so we’ll ignore it for today.

Judith Evans looked the Purplebricks‘ share price, which has more than doubled since last November (though they have fallen back recently).

- Traditional rivals Foxtons and Countrywide have fallen.

The catalyst for the shares increase in price – apart from its backing by Neil Woodward, who owns 26% – was its plans for international expansion, beginning in Australia, but moving onto the US.

- The latter rollout will be funded by the proceeds of a £50M share placing earlier this year.

Despite having double the market cap of Countrywide (£760M vs £380M), Purplebricks has only 3.3% of “sold listings”, compared to 4.5% for Countrywide.

- And some of the directors have been selling down their holdings.

Definitely a case of DYOR.

Market valuations (CAPE)

There were lots of articles on market valuations – whether the CAPE meant that stocks were overvalued, and whether this was the end of the Trump reflation trade. Let’s look at a few of them.

Let’s start with perennial optimist Ken Fisher, who says that stocks aren’t overvalued, and we should keep buying.

- According to Ken, people have been saying this since 2013, when the bull market was 4 years old.

- The bull market is now eight years old, and has seen 200 record highs.

Ken thinks that the doomsters are looking at things the wrong way round.

- Long-term growth investors need stocks to come out ahead.

- And bear markets won’t kill you if you sit through the bull markets as well.

Tot get out of stocks, you need to identify a huge problem that nobody else is aware of, and is therefore not already priced in.

Ken expects this bull to last longer than the 10 years of the one in the 1990s.

- We’re nowhere near peak euphoria yet.

Ken also thinks that we shouldn’t yet worry about PE ratios.

- The world PE of 18.6 is above average, but rising only slowly.

- It’s a sudden spike we need to watch out for.

- And 18.6 PE means 5.4% earnings yield, so its not the end of the world, especially as earnings will on average grow in the future.

He hands out particular stick to the 10-year smoothed CAPE ratio, which has been flashing red since 2013, when it passes the 2008 number.

- Now the US CAPE is at 29.1 – a figure beaten only in 1929 and 2000.

But Ken points out that the same thing happened in 1996.

- But it was another 39 months and a 116% gain before the market crashed.

Ken thinks the CAPE is useless up to 5 years ahead.

- The current calculations include the earnings numbers from 2008 and 2009.

- When these drop out over the next two years, things will look more respectable.

As well as this, changes in GAAP standards over time haven’t been accounted for.

- And comparing nominal stock prices to deflated (real) earnings is weird.

Even if CAPE works for 10-year return projections, if the next five years are good, and the following five are bad, would you want to skip the five good years?

- When the real peak comes, people will be explaining why PE numbers have further to go.

- Fear of heights is bullish, so keep buying.

Stocks are expensive

In contrast, Merryn does think that stocks are overpriced.

- The S&P 500 is up 80% over five years, while earnings per share are up only 8%.

- The trailing PE is 25 and the CAPE is 29.

- Over here, the FTSE-100 has a PE of 30 and the whole market’s PE is 21 (compared to a long-term average of 14)

- The UK CAPE is 18.

Merryn also likes to use investment trusts discounts as an indicator.

- They are as narrow as they have been for 15 years.

Most developed markets – with the exception of Merryn’s usual favourite, Japan – are are least 30% above their long-run PEs.

But markets need a trigger to crash. Options include:

- recessions

- political disasters

- interest rates rising quickly

- and the odd “black swan” event

Interest rates should be rising quickly (here in the UK they should be around 4% right now) but the actions of central banks over the last nine years suggest there’s not a great risk of this.

Political shocks – Trump no delivering his tax cuts, amnesties, deregulation and infrastructure spend – are more likely, but not yet probable.

- And Scotland and Europe look less likely to deliver shocks than a few months ago.

And global growth is picking up, so a recession looks unlikely.

Merryn recommends holding some cash and gold, and backing the cheap markets, like Japan, Korea and Vietnam.

In her MoneyWeek column, (( I couldn’t find it online )) Merryn took a different angle:

- Robin Angus, chairman of the Personal Assets Trust points out in his latest shareholder letter that the best question to ask 30 years ago would have been “what would the world look like if 10-Year US Treasuries yielded 2.5% pa?”

- Of course at the time, such a world would have seemed ridiculous.

So the question for today is “what would the world look like if 10-Year Treasuries yielded 14%?

Victims include:

- people with debts

- holders of long-term bonds (eg. almost every pension fund)

- bond proxy stocks (blue-chips with reliable yields)

Of course 14% is a long way off, but 4% is not so far. (( This appears to contradict what Merryn said in her FT column ))

- Actually, I think that in the UK at least, it is.

US market wobble

John Redwood focused on the US market wobble rather than valuations, but he was in the reassuring camp.

- The wobble reflects doubts about Trumps ability to deliver, plus the falling oil price.

John thinks that US reflation will continue, and will not be choked by interest rate rises.

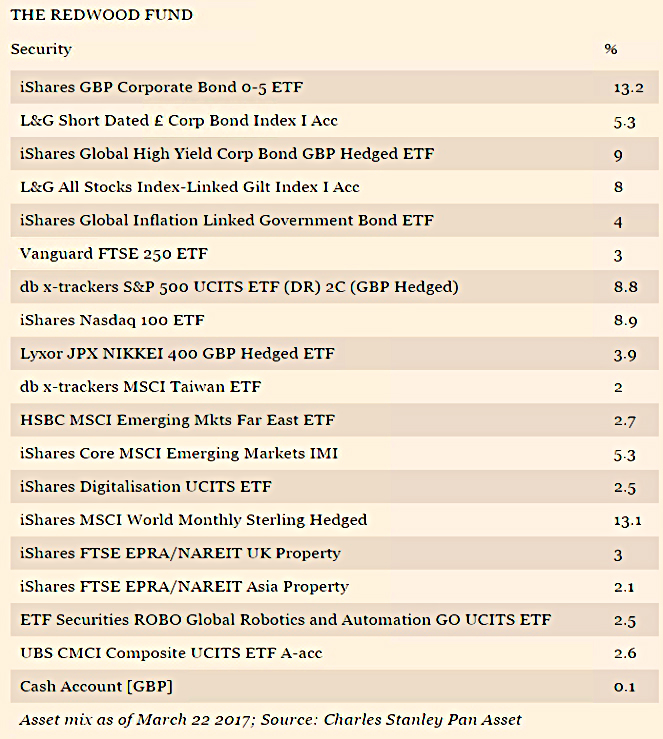

- So he’s keeping a large US position (around 18%) in his ETF portfolio.

It’s nice that John regularly updates us on the composition of his fund, but I’d also like to see a performance-tracking chart.

Elsewhere, John says it’s clear that fears of a Brexit recession were overdone, but he hopes that the UK and other European companies take action to remain competitive with the US once Trump’s reforms go through.

- In particular, he is looking for policies in the Autumn’s “Budget for Brexit” that “reward enterprise and growth”.

- If he finds them, he will increase his exposure to the UK.

Reflation trade

John Authers looked at the reflation trade.

- For John, this “Trump trade” was always overstated – the reflation move began before the election.

Since the election, it has morphed in two ways:

- Europe has caught up with the US – it’s no longer simply “America first”

- Inflation expectations (from bond spreads versus linkers) have fallen

John uses a framework by Atul Lee of Deltec to explain.

- World markets move on global growth momentum, and liquidity.

- If both are favourable, only politics can get in the way.

Trump helped growth momentum, as did Chinese stimulus and perception that fiscal stimulus would replace monetary policy.

- And liquidity is flowing back from the US to the emerging markets.

- China raised rates after the Fed, Europe looks closer to further tightening, and the Fed is now expected to be less aggressive.

- All of which has pushed down the dollar.

As for politics, Europe looks less of a risk, and Trump has done nothing so far on trade.

- The big question is whether the Trump defeat on healthcare will translate to defeats on tax cuts and infrastructure spending.

Bank stress tests

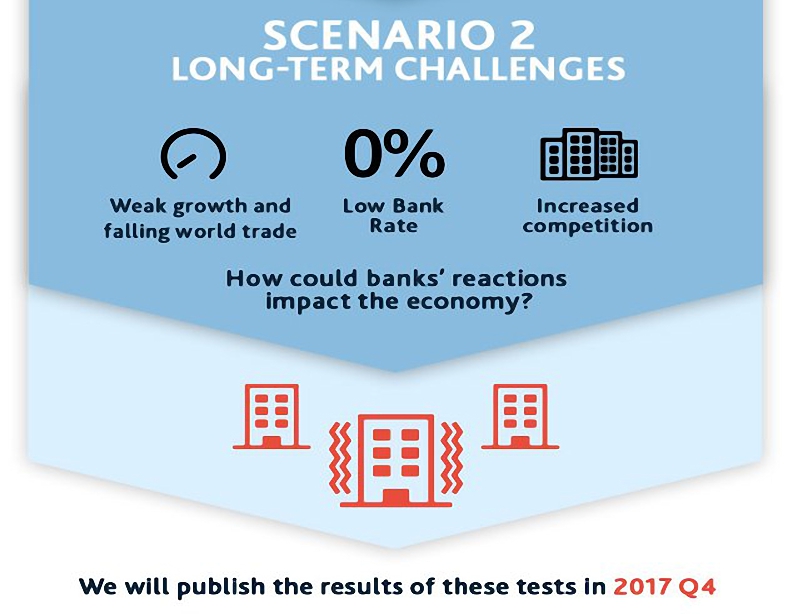

And finally on this topic, the Bank of England released details of its planned stress test for banks this year.

Highlights (lowlights?) of this worst-case scenario include:

- UK GDP shrinking by 4.7%

- house prices down by 33%

- interest rates up to 4%

Let’s hope this stays in the realm of the hypothetical.

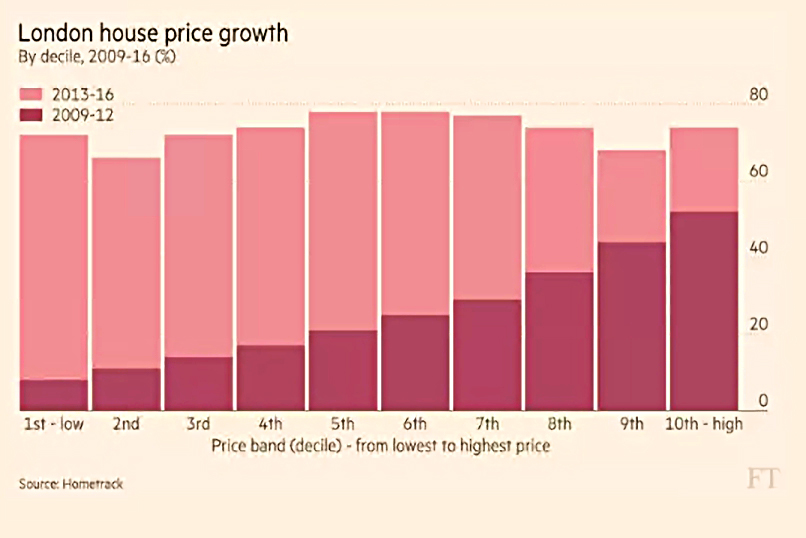

London house prices

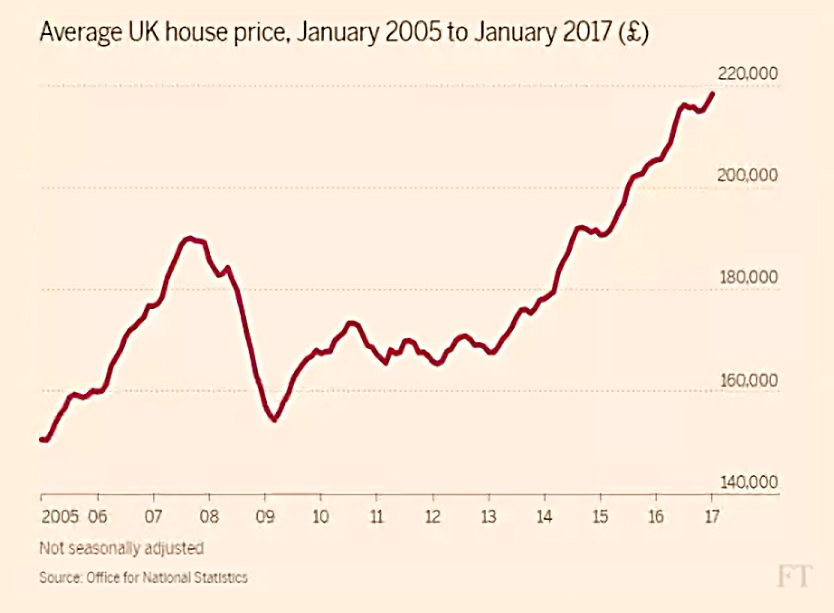

In our last piece from the FT, James Pickford reasoned that London house prices will not crash.

- A survey by Hometrack found that because the difficulty of mortgage finance at high loan to value ratios means that most owners have a lot of equity in their properties.

- The UK average loan to value is 53% but for mid-priced London homes it is 40%, and at the top end that drops to 23%.

Its clear however that there has been a slowdown in prices at the top end of the London market.

- The relative share of increases between 2009-12 and 2013-16 increases as you move up the property price deciles.

- Transaction levels in London have dropped by 35% in the year to November 2016, compared with 21% for England.

Measures of inflation

In the Times, Paul Johnson explained why the new measure of inflation is the best of a bad bunch. (( No link because the article is behind a paywall ))

We now have three main inflation measures:

- consumer prices index (CPI, the headline measure)

- retail prices index (RPI, much older)

- CPI including owner-occupiers’ housing costs (CPH-H, about to become the headline measure)

The first point that Paul makes is that inflation does not predict the annual increase in spending.

- That’s because if wine rises in price sharply, I may decide to drink less of it, or to substitute some with cheaper beer.

- So all the measures overstate inflation to some extent.

There are other problems with inflation as a time series:

- What should we do to accommodate new products (smartphones, say)?

- How do we account for dramatic increases in quality (laptops, or TVs – even cars)?

But these problems exist across all three UK measures so instead he focuses on the differences.

- RPI is the highest rate, because it has a problem in its maths

- if prices go up one month, then back down again the next, RPI reports an increase over the two months

- but the ONS has to produce it because it’s widely used (eg. in index-linked gilts)

- CPI has good maths, but leaves out the cost of housing for owner-occupiers

- it’s the UK version of an EU measure that ignores these costs

- CPI-H attempts to include these costs

But housing is problematic, because it’s partly an investment.

- And none of the inflation baskets include things like stocks

To avoid including house price increases, CPI-H uses “imputed rents” – what it would costs you to rent your home.

- This is not the same as an owner-occupier’s housing costs, but it’s the best measure we have.

So CPI-H is an improvement on CPI, even though the two numbers have been very close to each other in recent years.

- The only problem with this interpretation is the cynical historic use of CPI for things where a small inflation number is helpful to the government, and RPI where a big number helps.

For CPI-H to be a real improvement, the government needs to stick to it.

Bond spreads

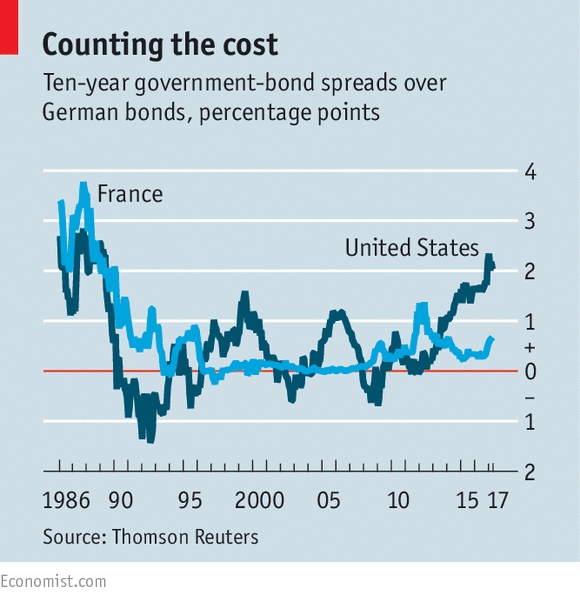

In the Economist, Buttonwood looked at bond spreads.

- 10-year US bond yields are now higher than those in Britain, France, Singapore and Italy.

- US yields are usually 1% above German yields but the gap is now 2%.

Normally, the country with higher yields has the weaker currency.

- But the dollar is stronger than the euro

- And its higher yield makes more people want to buy it

Today the gap partly reflects monetary and fiscal policy:

- the Fed has stopped buying bonds and has raised rates twice

- the ECB is still buying bonds and won’t raise rates

- plus the US plans tax cuts and infrastructure spending

But inflation rate expectations are 2.1% for the US and 1.7% for the euro zone (from 2022 to 2027)

- which means this is not like the US / Japanese divergence driven by the latter’s deflation

Politics could be a factor:

- there’s a small chance that Le Pen could win in France, and issue bonds in francs

- this would make investors buy German bonds, depressing their yield

And European pension funds / life assurers buy a greater share of european bonds than do US firms, which again depresses yields.

- Because the liabilities of the firms are longer than the bonds, when yields fall, they need to buy more bonds

- This pushes prices up and yields down – a vicious circle

If Le Pen doesn’t win, or the Trump stimulus is delayed or diluted, expect things to sort themselves out.

Shale oil

Schumpeter reported that America’s shale oil firms were about to go on an investment spree.

- It’s not immediately apparent why that should be so – the oil price is $48 a barrel, half the level of three years ago

- And the industry has burned cash for 34 of the last 40 quarters

- $11bn was used up in the last quarter

When the oil price crashed in late 2014, 68% of US rigs were shut down.

- 100 firms went bust, defaulting on $70 bn of debt

- production fell by 15% to 1M barrels per day (1% of global output)

Apart from the stabilisation of the oil price, another new positive is the realisation that the Permian basin in Texas holds a lot more oil than previously thought.

- Production could exceed that of Saudi Arabia in time.

- And productivity is up.

But debt remains high, at $200 bn in total.

The Economist puts the level of investment down to incentives for both executives and lenders to use more capital.

- Return on capital is rarely used in pay schemes, and low interest rates and loan startup fees mean that everyone wants to use more money.

The only way this will end well is if the oil price rises sharply (unlikely) or the small firms are bought out by the big boys (also unlikely).

- They could also dramatically increase production, but that would cap the oil price, and thus be somewhat self-defeating.

Until next time.

Hi Mike,

Great round up as ever, thanks! In terms of Ken Fishers comments – it just shows why you shouldnt try and time the market (I know I dont practice what I preach..) – pound cost averaging each month is the best way to remove the stress. My personal view is with Merryn’s – things are over priced, however this is not stopping my monthly pension and ISA contributions ticking in and buying at whatever price it happened to be on that day!

As for interest rates, I never thought they would stay this low for this long, but as you say can we imagine a world with interest rates at 14%? Right now no as so many people would go bust (I can honestly say I would struggle with our mortgage at that rate!), but that doesn’t mean it can’t or won’t happen – anyone else remember interest rates of 15%? Fortunately back then I was a kid and saving without any debt, but it hit my parents….

Cheers,

FiL

Hi FiL,

You’re right about stress, but pound cost averaging lowers your returns in the end. I just put the money in the market as soon as I have it (which is what you seem to be doing as well).

I can certainly imagine 14% interest rates because I lived through them back in the early 1990s. I had what was then thought of as a big mortgage (3 x earnings) so I was quite keen to pay it off.

At the moment I can’t see a rate rise in the UK, but the one certainty in life is change.

Mike

Hi Mike,

I will be putting it in as soon as I have it on the Go T’ Pub portfolio, but on my active managed one I am not – in fact I am sitting on a larger cash balance than I have for years waiting for a timing!

I am with you – can’t see much of a change (I doubt it will get above 1%) for another couple of years, but with uncertainties ahead, who knows 🙂 Like you – I would want to clear my mortgage as fast as possible – but also as efficiently, so I have to have some sleepless nights as money goes into ISAs rather than off the mortgage!

Cheers,

FiL

I would say that paying down debt is the same as investing it. Sitting on cash is the bad habit you don’t want to develop.

I am with you I count it as part of my savings rates.

Yes, cash is not a good store, so I know I should have just thrown it into the market months ago (I’ve now lost out on the quarterly dividends), but I can’t help myself on that one….!