Weekly Roundup, 7th March 2022

We begin today’s Weekly Roundup with the terrible situation in Ukraine.

Contents

Higher inflation, not rates

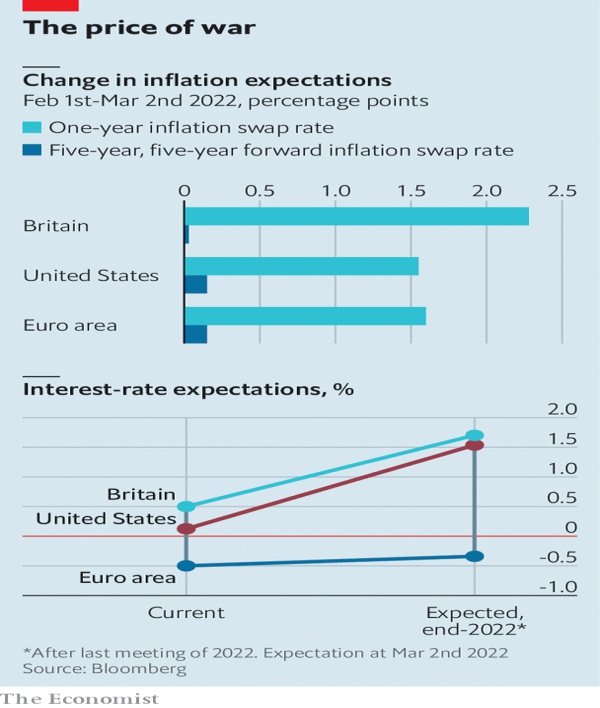

The Economist felt that war and sanctions would lead to higher inflation, but not necessarily higher interest rates.

Russia’s economic importance vastly outweighs its GDP or financial clout owing to its energy exports. It produces nearly a fifth of the world’s natural gas, and more than a tenth of the world’s oil, the price of which drives much of the short-term variation in global inflation.

We can all see the impact on energy prices, and this will feed through into inflation.

A sustained shut-off of the Russian oil supply might cause prices to rise to $150 per barrel, a level sufficient to knock 1.6% off global gdp while raising consumer prices by another 2%.

There are similarities with the 1973 oil shock from the Yom Kippur war.

- The existing inflation problem from the collapse of the Bretton Woods FX system is replaced by the current inflation from the pandemic stimulus.

Inflation expectations have risen sharply or a 1-year outlook, but not much over five to ten years.

- And interest-rate expectations have barely budged, with the forecast rate for the UK and UK at around 1.5% at the end of 2022.

Longer-term rate expectations have fallen, which means that markets are betting that inflation will be temporary.

Defence stocks

Merryn Somerset Webb wondered whether defence stocks are now ESG since supplying weapons to an invaded underdog must count as a social good.

I think it’s fair to describe Merryn as a cynic on ESG: (( I am one myself ))

I’ve written before about the idiocy of exclusionary investment — refusing to invest in fossil fuels and mining because they are dirty but also relying on both to drive the global economy and the energy transition.

Structural under-investment in oil and gas means that we are all now facing energy bills of £3K+ pa. (( Mine looks like it will hit £5K ))

This week Merryn has been invited to a seminar on the evolution of ESG:

It will continue to evolve until one way or another it encompasses everything. Then, like everything that has tried to be all things to all men before, it will mean nothing.

Merryn thinks there is too much emphasis on the E in ESG, and not enough on S, which she takes to mean community well-being and the maintenance of living standards.

- I think most ESG diehards would be happy for living standards to deteriorate.

Back to defence:

Jets and tanks have something of a significant carbon footprint — and anything designed to frighten and kill is surely impossible to classify as a good thing.

But isn’t supplying the underdog – and national defence in general – ok?

- The problem is that defence companies sell to dictators as well as underdogs.

Despite this, the buzz is that the EU is planning to add defence as an ESG sector in its social taxonomy.

The idea that anyone can provide a static ESG framework that both excludes some sectors or companies and works is dead. If you want to invest sustainably for the long term in companies that offer something to society

you don’t actually need an ESG fund manager.

Merryn is also in favour of dumping passive funds (who would have had a forced allocation to Russia) in favour of unconstrained active funds, and

An unconstrained, active, focused, and thoughtful fund manager — possibly one who recognises that his clients want to be good to the planet, but who also

remembers the 1970s and buys you a hefty position in real assets.

Credit Suisse Yearbook

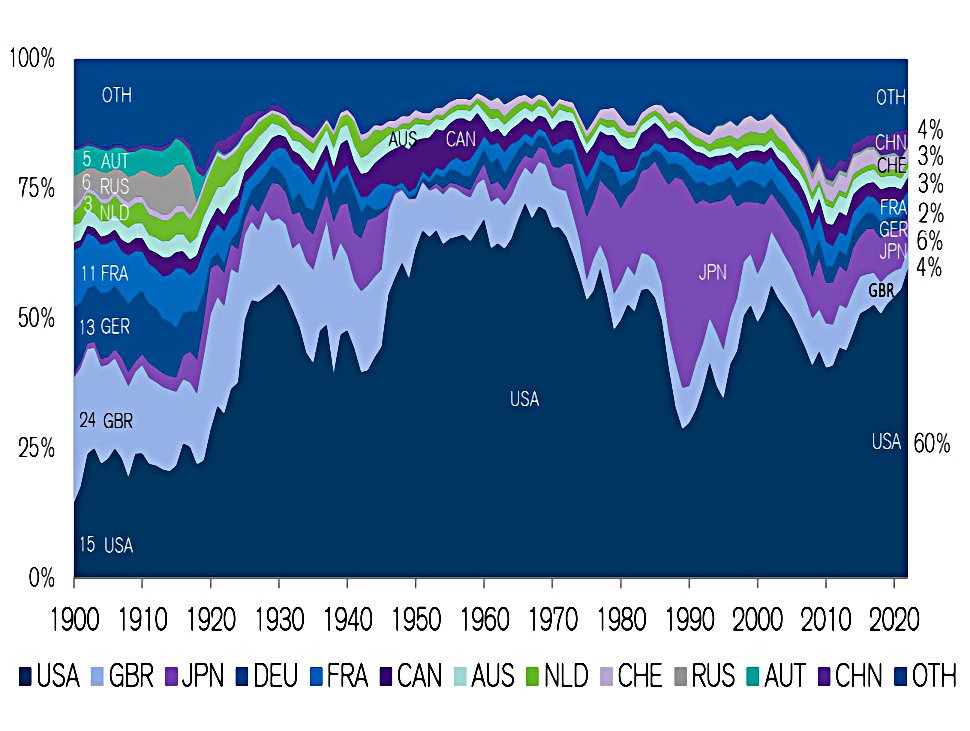

David Stevenson helpfully summarised the annual Credit Suisse Global Investment Returns Yearbook from Elroy Dimson, Paul Marsh, and Mike Staunton.

He called it a 10-point summary, but for me, there are three core topics:

- US dominance

- Returns

- Diversification and correlations

Although (some) investors are worried about the current US dominance of listed markets, things have been worse, notably in the 50s and 60s (before even my time).

- The other things to note from the chart are the size of the Japanese market in the 1980s and 1990s, and the dominance of Europe before the first world war.

The long-term (real) return of stocks over bonds has been 3.2% pa (and 4.6% pa vs bills/cash).

- Returns have been steadily declining, however, and future stock returns are expected to be 3.5% vs cash, with almost zero return on bonds.

A blended portfolio should return in the order of 2.5% real pa.

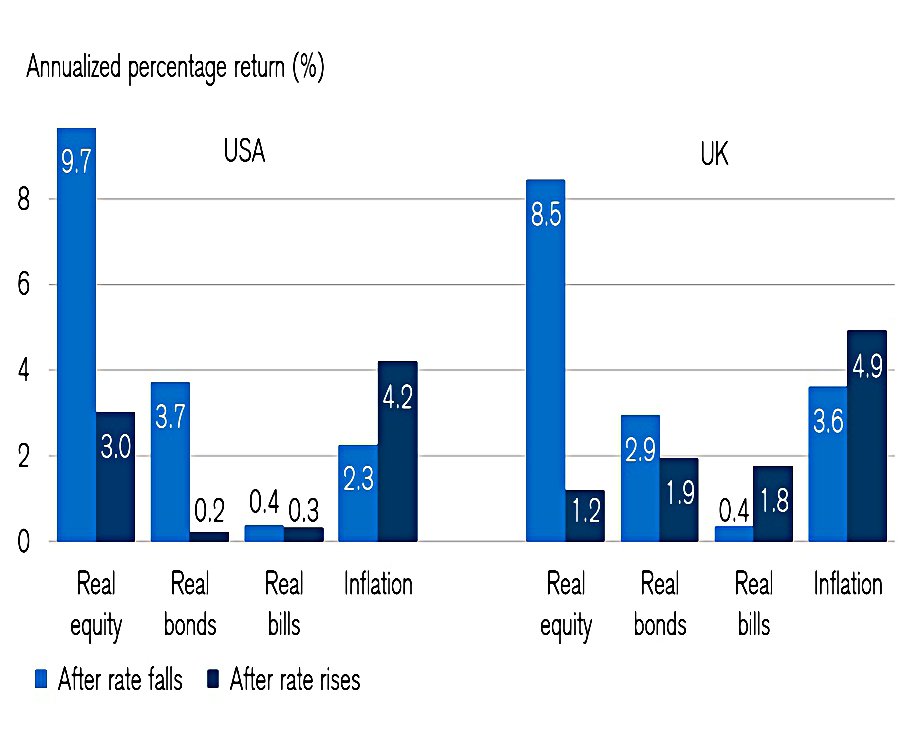

After a series of interest rate rises, returns are much lower than after rate falls.

- US returns after rises are 3.0% pa, whilst in the UK they fall to 1.2% pa.

Diversification works – you can have the same return at lower risk or a higher return for your original level of risk.

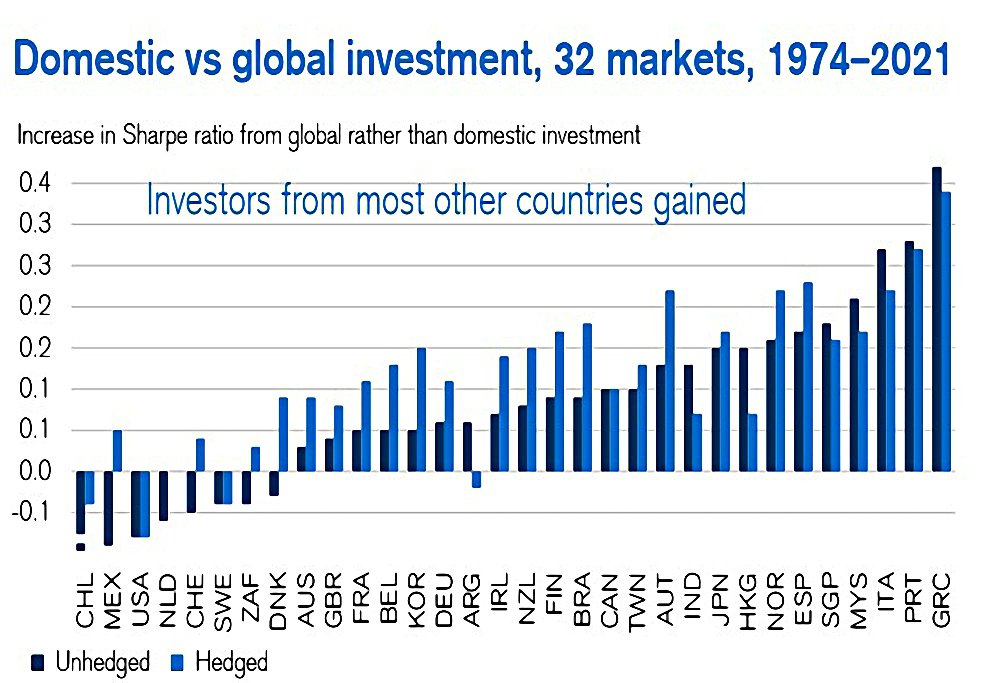

- Interestingly, the high returns in the US mean that international diversification hasn’t worked for US investors since 1974

It has for most countries, though – including the UK.

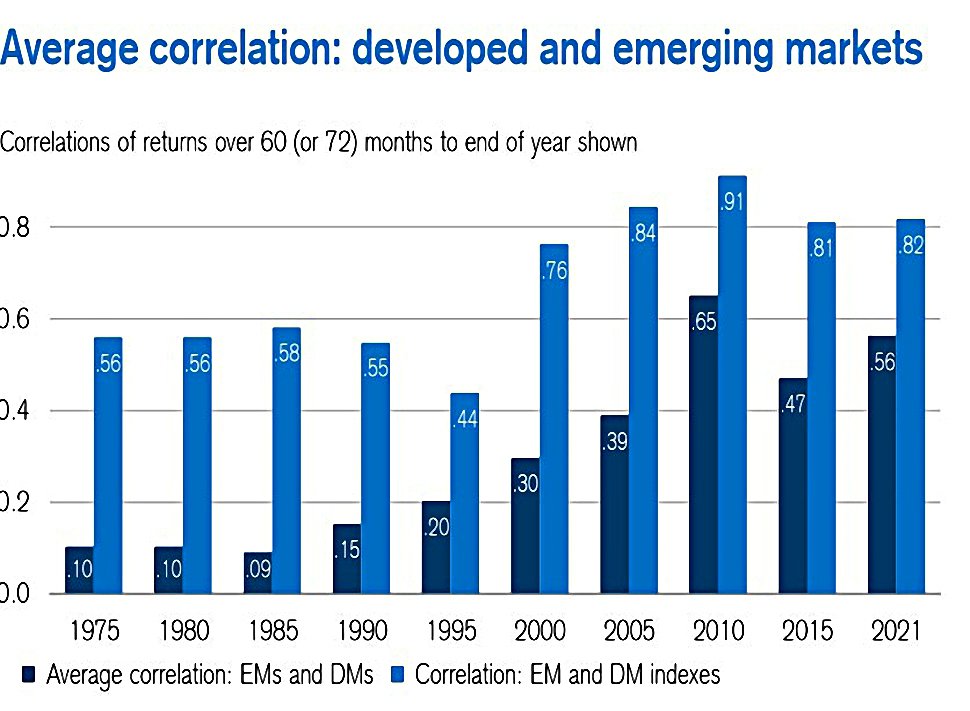

With the rise of globalisation and the internet, correlations between stocks in developed countries have increased significantly in recent decades.

But EM stocks are still useful diversifiers.

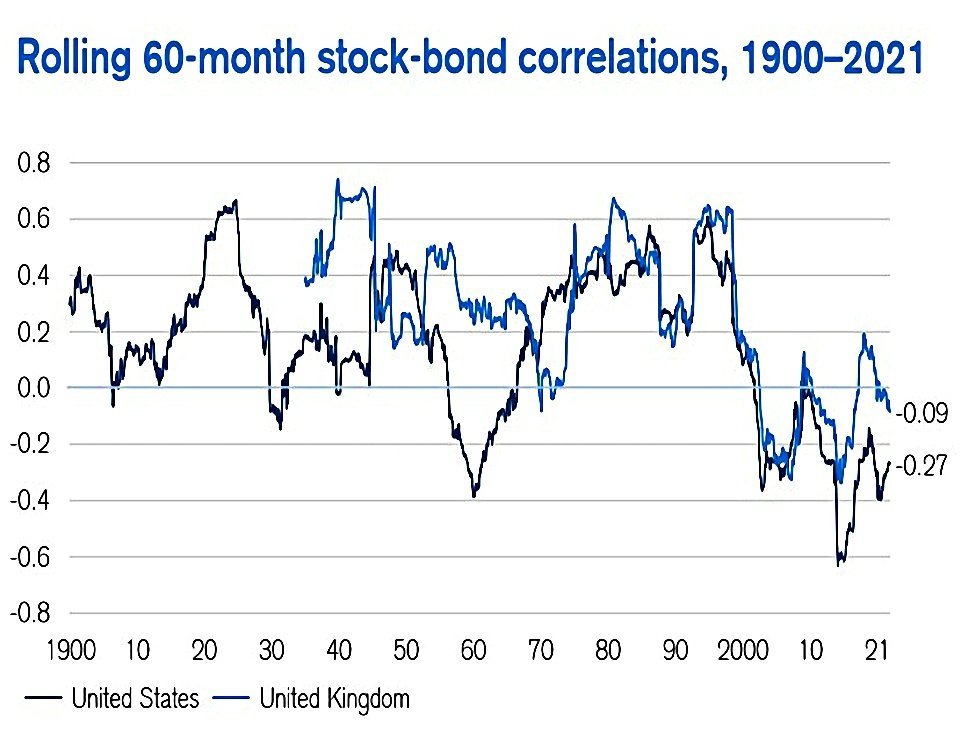

And bonds still work for now, though less well in the UK than in the US.

interactive investor

The interactive investor platform has launched a new “low-cost” SIPP called Pension Builder.

- The custody fee is £12.99 per month, regardless of pot size.

- Transaction fees are £7.99 for UK shares and ETFs.

This is still more than AJ Bell (£10 per month) and FIdelity (just £45 per year for exchange-traded instruments). (( Note that Fidelity has a restricted range of ETFs and ITs, so you will probably need another SIPP alongside it ))

- So I won’t be switching over, though if I needed a third SIPP provider I would definitely consider it.

I think ii are trying to poach clients from Vanguard, which is more expensive than ii above £100K in pot size.

- I don’t use Vanguard because they only offer their own funds and their annual fee tops out at £375, more than 3x the AJ Bell fee and 8.3x the Fidelity fee.

The new ii scheme also looks attractive for those who use mutual funds rather than ETFs and ITs (which I don’t).

Freetrade

Freetrade has launched in Sweden, its second foreign office after Australia.

- It plans to open to the Swedish public after a beta test of several months.

Freetrade also has plans to launch in Germany and the Netherlands and has been adding international stocks for some time.

CEO Adam Dodds said:

This news marks a significant milestone in our mission to get everyone investing. We’ve always considered Freetrade to be a European company at heart, and I am thrilled for us to be able to [open in Sweden].

It’s good news for the Swedes, but the focus on Europe – and on the paid tiers of the app – does nothing for me as a user of the UK free tier.

- I’ve stopped trading on Freetrade, and use Trading 212 in the UK, and Stake and LightYear for US stocks.

Freetrade has also asked users to agree to new Ts&Cs which include securities lending (for non-ISA accounts only, as the practice is not allowed by HMRC in ISAs).

- Securities lending is pretty common, but the move will go down badly with the Reddit meme stock traders who are still mad at platforms like RobinHood and eToro for employing “sharp practices” like this.

- Revolut and Trading 212 also lend stocks.

Securities lending – used by hedge funds and other short sellers – will earn Freetrade money and help them to keep costs down.

A Freetrade spokesman said:

We’re asking all Freetrade customers to provide their consent to allow us to lend the securities they hold. It’s an important evolution in our business.

Securities lending isn’t the wild west, it’s an established process, with risk controls taken throughout. Securities lending and its participants are part of the regulated UK financial market which means any lending in the UK must be reported to regulators.

In line with our goal to build a sustainable business, securities lending will provide Freetrade with a new and stable revenue stream, allowing us to keep our fees low, continue to improve our product and services as we scale and help get everyone investing.

Users have until 1st June to agree or to move off the platform. (( Specifically, they will no longer be able to buy stocks after that date ))

PayPal

Crypto trading has finally turned up on PayPal in the UK, but it looks too expensive to use.

- You can now “Buy, sell, and hold Bitcoin, Ethereum, Litecoin and Bitcoin Cash” directly in your PayPal wallet, in sizes right down to £1.

The crypto is bought in dollars, so if you hold sterling on PayPal, there will be an FX fee as well as the crypto fees. (( I used to have a medium-sized balance in dollars with PayPal but this has arrived too late for me ))

- You can’t send the crypto outside of PayPal (to another wallet or exchange) – or even to another PayPal user.

Here are the fees, ignoring the buy/sell spread:

- For £1 to £25 is 50p (min 2%)

- £25 to £100 = 2.3%

- £100 to £200 = 2%

- £200 to £1K = 1.8%

- £1K+ = 1.5%

Quick Links

I have seven for you this week, the first five from The Economist:

- The newspaper said that Sea Group faces choppier waters

- And wrote about two new ways of extracting lithium from brine

- The Economist also said South Korea’s economy threatens to become like Japan’s

- And that Russia’s attack on Ukraine means more military spending

- And asked whether Elon Musk will change Germany.

- Alpha Architect wondered whether culture affects equity analysts

- And asked whether internally generated intangibles are worthless.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.