Weekly Roundup, 4th January 2022

We begin today’s Weekly Roundup with inflation.

Inflation

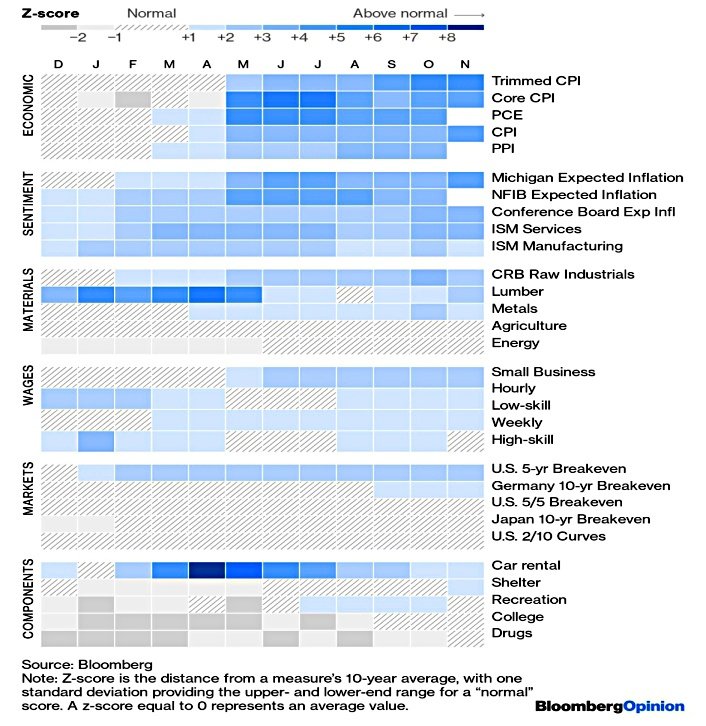

John Authers looked at whether we could have seen prolonged inflation coming.

- He’s been maintaining a week-by-week heatmap snapshot of thirty inflation indicators.

For several months, inflation could just as accurately be read as no more than a transitory phenomenon. Only in the last few months has it grown into a broad and persistent trend.

The squares in the heat map turn darker blue as their Z-scores increase.

In May, when alarm about inflation began to take hold, only a few indicators were extreme. Most had barely started to rise.

John drills down into the spread between core US CPI and the “trimmed mean” which excludes outliers.

While “core” CPI shot upwards, the trimmed mean barely moved. The gap between them hit a record. While May’s headline number was shocking, the huge gap between the core and the trimmed mean showed that it was driven to an unprecedented extent by a few outliers. And there was a clear explanation for those outliers: Covid-19.

Usually, a large gap like this closes by core CPI coming back to the trimmed mean.

- And the extreme readings in lumber and used cars did disappear – but core CPI never fell.

Instead, the trimmed mean rose.

Early signs of inflation — and the firestorm of commentary they provoked — helped to build expectations for future inflation. This encouraged many consumers to bring forward their purchases and drove workers to demand higher wages.

There were also monetary pressures from the Covid stimulus and the continued impact of the pandemic on supply chains.

- John’s newsletter goes into detail on each of his indicators.

The good news on inflation comes from the bond markets:

As far as the bond market is concerned, inflation may be elevated for the next five years. But the prices of longer-dated bonds show that dealers haven’t wavered in their belief that it will come back under control after that.

But the Fed’s task is not easy:

They will have to withdraw money from the system without prompting a downturn, convince consumers that rising inflation isn’t inevitable and, critically, persuade workers that they don’t need to raise their wage demands.

And the political interference from the looming mid-terms won’t help.

Interest rates

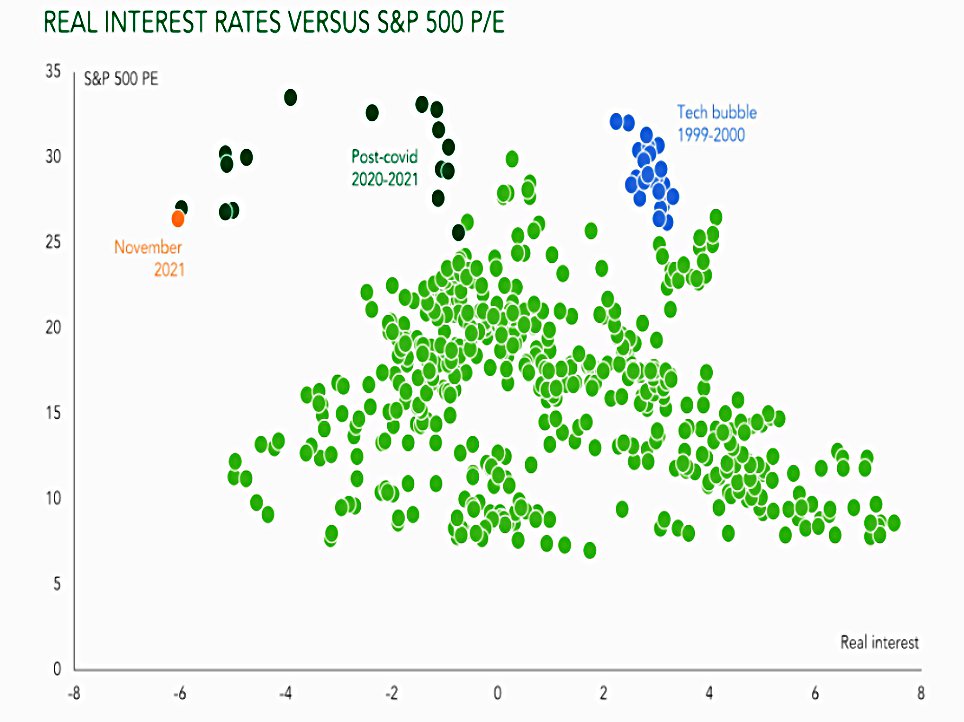

Steve Russell of Ruffer warned that negative real interest rates can be bad for equity valuations.

- Equities are commonly held to offer inflation protection (since their cashflows increase with inflation) but this only holds up to a point.

Whenever real interest rates have deviated from the ‘Goldilocks’ range of -2% to 2, stock market price-t0-earnings ratios (P/Es) have fallen.

There are a couple of exceptions:

The tech bubble in 1998-2000 and the recent post-covid period. The first ended badly, we must wait to see what happens this time.

Interest rates are the “speed” at which future profits/cash flows must be discounted to reach their present value.

- The lower the discount rate, the higher the P/E ratio that can be supported.

An increase in nominal interest rates would be bad news for all stocks, but particularly growth stocks.

Especially for those where most of the profits and cashflows are expected to be paid in the distant future. The growth stocks, profitless companies and concept stocks so popular today would clearly be the hardest hit.

With low interest rates and high inflation, we have negative real rates.

There will be more uncertainty on both future earnings and future interest rates. In contrast to the current market conceit this would demand a higher discount rate (and not a lower one). This implies a lower valuation for markets as a whole and potentially even worse news for those most highly rated growth stocks.

So negative real rates can potentially have the same effect as high nominal rates.

- And high inflation can hurt stocks even if central banks don’t raise rates too much.

Pensions

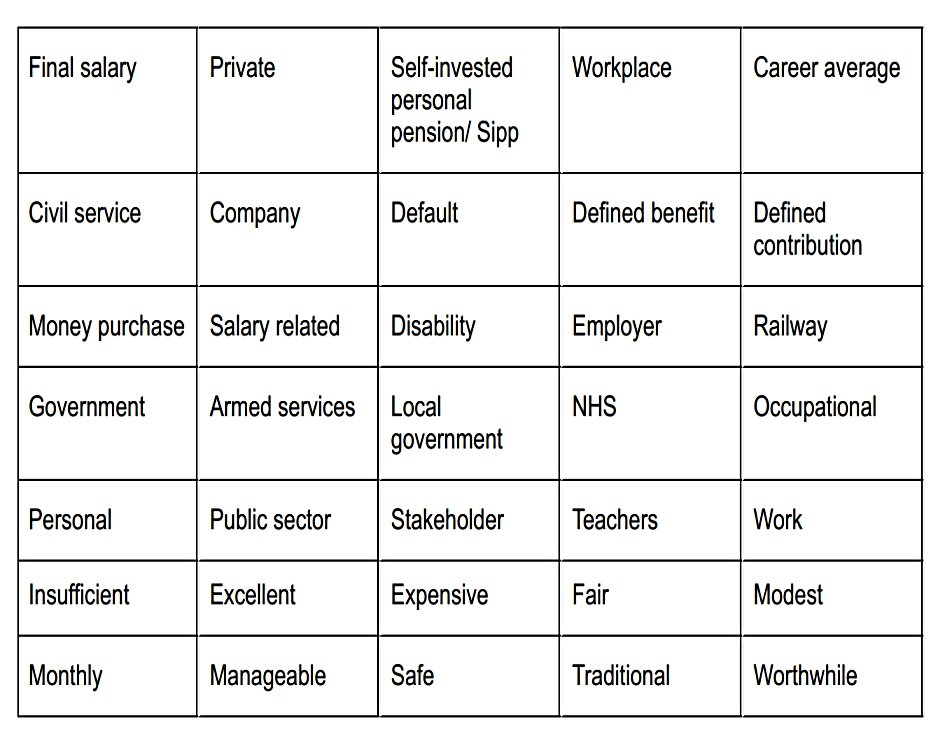

interactive investor carried out a survey to find out what the word pension means to people.

They came up with 35 common terms, plus a few fruity phrases:

- “defined contribution – pay and pray”

- “stock market Ponzi scheme”

- “I pay 5%, my employer pays 8%: it’s rubbish”#

Becky O’Connor of ii said:

For some, a pension is ‘excellent’; for others, it is ‘insufficient’. The type of pension someone has; the generosity of their employer or past employers and also, perhaps, their age, contribute to the different perceptions as well as eventual outcomes.

The classic ‘trump’ pension is a defined benefit, final-salary scheme. Sadly, few such schemes are open to new members anymore. But even this type has a disadvantage when it comes to inheritability, as these pensions might only be inherited at a reduced rate by a spouse, but not by surviving children.

The ability to move to different types of scheme can be limited by requirements to take advice, as well as employment status and how much you have in your pots. So there’s an element of ‘what you get is what you get’ about workplace schemes, while there is more freedom with personal pensions, including Sipps.

ii has a pack of “pensions trumps” cards to help people understand the options.

Crypto

In the FT, Robert McCauley from Boston University argued that bitcoin is worse than a Madoff-style Ponzi Scheme.

- His logic is that bitcoin is negative-sum rather than zero-sum and that there is no centralised operator that you can sue in the event of a collapse.

Here are some Ponzi characteristics:

- Investors buy in the expectation of profits.

- That expectation is sustained by the profits of those that cash out.

- But there is no external source for those profits; they come entirely from new investments.

- And the operators take away a large portion of the money.

The original Ponzi scheme lasted less than a year in 1920 after Charles Ponzi promised a 50% return over 45 days.

- Bernie Madoff’s scheme “only” returned 1% per month and lasted for many years until the 2008 financial crisis prompted a wave of redemptions. (( McCauley notes that 70% of the $20 bn invested in the scheme has been recovered, and those who put in less than $1.6M are being fully repaid ))

Bitcoin has already lasted a dozen years and is slightly different from those two schemes:

Bitcoin is bought not as an income-earning asset but rather as a zero-coupon perpetual. In other words, it promises nothing as a running yield and never matures with a required terminal payment. It follows that it cannot suffer a run. The only way a holder of bitcoin can cash out is by a sale to someone else.

The most likely trigger for a bitcoin collapse would be the failure of a stablecoin like Tether.

- McCauley draws a parallel with the value of a regulated money market fund holding Lehman Brothers’ paper “breaking the buck” in 2008.

A cynical view of Bitcoin holds that it is more like the traditional (and ongoing, in the UK’s AIM market) penny-stock pump-and-dump scheme than a Ponzi.

Traders acquire basically worthless stock, talk it up and perhaps trade it among themselves at rising prices before unloading it on to those drawn in by the chatter and the price action. Buyers cannot stand the sight of friends getting rich overnight: they suffer an acute fear of missing out (FOMO).

McCauley’s negative-sum argument rests on the use of real resources (electricity, computer hardware and internet fees) to maintain the network.

It is costly in a way that Madoff’s two- or three-man operation was not. About 900 new bitcoin a day require $45m a day in electricity. Thus, the negative sum in the bitcoin game is in tens of billions of dollars and rising at over a billion dollars per month.

This is true, but it will only become a factor when the bitcoin price falls such that miners cannot recover their costs.

- If at the same time, people no longer believe in BTC’s future as “sound money”, then it will collapse.

I’m worried by Tether too, and BTC (and crypto in general) is certainly risky.

- I wouldn’t advise anybody to focus on a crypto get-rich-quick plan, but a $1 trillion asset with a decade-long record of rapid price appreciation and a low correlation to stocks is worthy of a small allocation.

My personal target for end-2022 (assuming continued progress) is just 1% of net worth.

Another seven crypto adverts have been banned by the Advertising Standards Authority (the UK’s advertising watchdog).

- The ASA says that a lot of these ads don’t get across the risks of investing.

The banned ads were:

- Coinburp

- eToro

- Kraken

- Exmo

- Luno

- Coinbase

- Papa John’s pizza (“free Bitcoin worth £10”)

The Papa John scheme was a celebration of “Bitcoin pizza day” – in May 2020 a guy spend 10K BTC (now worth £350M) for two pizzas.

The ASA said this:

Trivialised what was a serious and potentially costly financial decision, especially in the context of the intended audience who were likely to have limited knowledge of cryptocurrency.

Mike Lockwood, ASA director of complaints, said:

Cryptoassets are a red-alert priority issue for us. Consumers need to know about the risks of investing in cryptoassets and companies should make sure that their ads aren’t misleading or socially irresponsible by taking advantage of consumers’ lack of awareness around these complex and volatile products.

Video game developer Ubisoft has announced that NFTs will feature in a new game (initially a Tom Clancy title, but later other games too).

- This has led to a backlash from gamers (through the crypto community appears to be in favour).

The tokens will trade on the “low-energy” Tezos blockchain (which uses proof of stake rather than proof of work), but energy consumption remains one of the chief objections from gamers.

- Crypto miners argue that they are mostly using “spare” energy, often from green sources like hydroelectric.

Ubisoft says that its NFTs (called Digits, and using unique serial numbers) will be fungible across games via an internal platform called Quartz.

- This sounds like they are not NFTs, but perhaps it means that the same object will be useful in more than one game.

Ubisoft is also not using the “royalties” aspect of NFTs, which gives creators a cut of future resales.

Ubisoft’s move is in contrast with platform Steam, which has banned all crypto and NFT-based games.

- Free-to-play games often depend on sales of in-game cosmetic items (“skins”) that change the look of characters or items – including on Steam since 2012.

Quick links

I have four for you this week, the first two from Alpha Architect:

- They looked at momentum investing

- And claimed that the illiquidity discount is an opportunity cost.

- The Economist asked how big Apple wants to be in media

- And UK Dividend Stocks looked at whether Ferrexpo is a good dividend investment.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.