Weekly Roundup, 9th April 2019

We begin today’s Weekly Roundup in the FT, with the Chart That Tells A Story. This week it was about equity release.

Contents

Equity release

It’s a thin roundup this week, with Brexit back in the headlines and the financial pages taken up with the end of the tax year (and last-minute ISA contributions in particular).

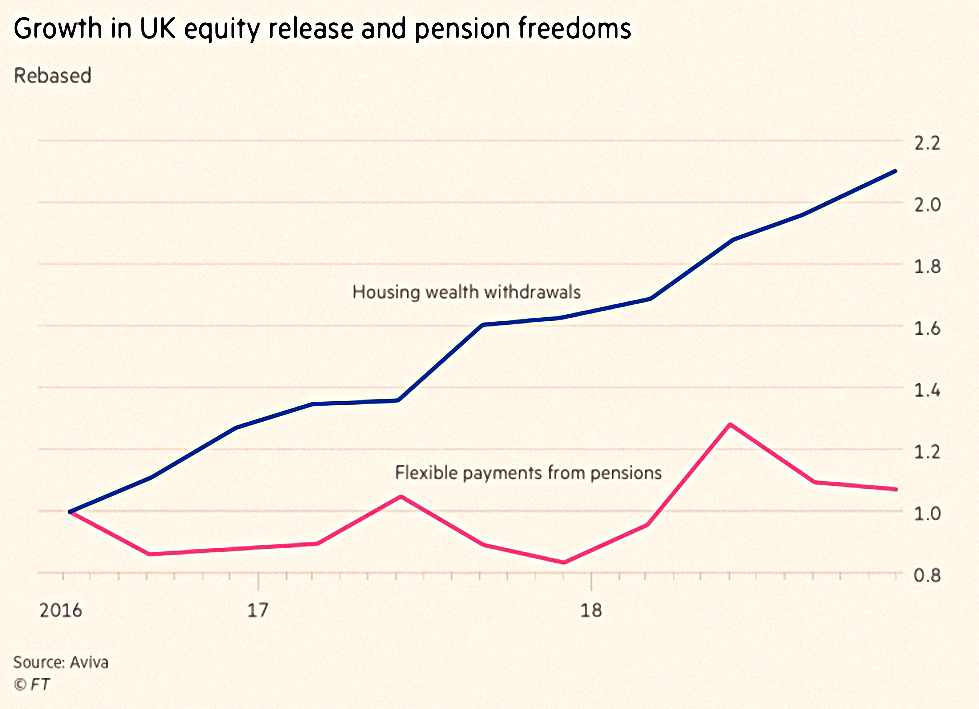

Lucy Warwick-Ching compared the recent growth in equity release to the flexible payments taken from pensions since the recent “freedoms” were introduced.

- It’s an interesting comparison – equity release is growing at twice the rate of pension withdrawals.

But the chart is misleading, as more money is withdrawn from pensions.

- More than £1bn of home equity was withdrawn during 4Q18, and close to £4 bn over the whole year.

- But close to £8 bn was withdrawn from pensions.

I’m not a fan of equity release, because the interest roll up on top of the initial loan, to be repaid on death (or when both of the owners move into long-term care).

- This snowball effect makes it easy to burn through all of the equity.

But there are products available with a “no negative equity” guarantee.

Aviva (who carried out the research) say that property and pensions together represent close to 80% of UK private wealth.

- That’s another interesting number – it’s closer to 60% for me.

Pensions and houses

Merryn Somerset Webb also wrote about pensions and houses.

- According to the OECD, the UK has pension assets worth 105% of GDP.

This puts us near the top of the global pension savings league.

For comparison, France and Italy are at 6% and Germany at 7%.

The UK’s pensions have also grown strongly from 73% of GDP in 2007.

- This growth will slow as DB pensions are closed down, but workplace auto-enrolment will mean that it doesn’t stop completely (see below for details on the contribution levels for the new tax year).

Merryn is worried by regularly recurring proposals that pension money should be able to be used as house deposits.

- This week it was the turn of the Centre of Policy Studies to suggest it.

But the whole point of a pension is that you can’t access it until you are old (-ish).

- The other problem is that it would push up property prices even further.

Tax relief for elderly downsizers (as we discussed last month) would be a much better idea.

New tax year

Emma Agyemang ran through the key tax changes for the new year:

- The tax-free personal allowance goes up to £12.5K, and the higher rate threshold to £50K.

- NI contributions will be synchronised to this £50K threshold, at 12% below and 2% above this line.

- The nil-rate residence band (an IHT allowance) rises from £125K to £150K (on top of the basic allowance of £325K).

- The state pension increases by 2,6%, with the new pension now worth £8.8K pa.

- Auto-enrolment workplace contributions rise to 3% for the employer and 5% for the employee.

- The LTA for pension withdrawals rises to £1.055M, but the annual allowance remains at £40K.

- The ISA allowance remains at £20K pa.

- The CGT allowance rises to £12K pa, with CGT rates unchanged.

John Lee

John Lee’s regular update on his small cap portfolio started with a look at insurance services group Charles Taylor.

- The share price had dropped from £3 to £2 without an announcement on likely earnings (which must be made if they will differ from market expectations).

In the event the results were reassuring, but the price didn’t bounce.

- Dinner with the chief executive didn’t make things any clearer.

But with a single figure PE and a dividend yield close to 6%, John made his 19th purchase of the stock nonetheless.

- I’m pretty sure I wouldn’t have been able to do that.

I also note that since John’s article was published, the price is up by close to 10% in less than a week.

Interactive investor

Interactive investor announced than from June they will be moving to “Netflix-like monthly flat fee pricing”. (( It’s news to me that Netflix invented this pricing model, and I can’t really see the connection between investing and streaming video ))

There are three new plans, priced at £10, £14 and £20 a month.

- The more expensive plans come with cheaper trades, from £8 on the basic plan to £4 on the most expensive.

This Super Investor plan also comes with two free trades per month (compared to one for the basic plan).

- So it becomes competitive at 5 trades per month (total cost 20 + 3*4 = £32, or £6.40 per trade).

Unfortunately that’s still more than iWeb and X-O for ISAs.

- But if you are sure you will make even more trades than that every month, then it could be the one for you.

The basic plan looks attractive for SIPPs – £120 pa plus £8 per trade.

- This compares favourably with YouInvest (£100 pa plus £10 per trade).

But unfortunately there’s a £10 per month surcharge for a SIPP.

- So YouInvest is still the cheapest SIPP.

Doctors’ pension tax

In FT Adviser, Maria Espadinha reported that the government has ruled out a pension tax exemption for NHS scheme members.

Health minister Jackie Doyle-Price said:

The annual allowance provides a disincentive to take on additional work or responsibilities, [but there is not] a case for exempting high earning NHS staff from a tax measure that is intended to apply to high earning individuals.

And I don’t think that clinicians expect to be treated differently from other taxpayers.

That’s good news, as it would have been an unfortunate precedent.

Peer to peer lending

Kate Beioley reported that the FCA has warned on holding P2P loans inside an IF ISA

The Financial Conduct Authority said it had seen evidence that Innovative Finance Isas were being marketed alongside cash Isas despite the fact they offer far less protection to consumers.

The article linked the warning to the mini-binds marketed by failed introducer London Capital & Finance.

- But although the marketing of minibonds is similar to IF ISAs, and they share the lack of FSCS protection, mini bonds are not IS ISAs.

And the FCS warning is really designed to ensure that investors know that P2P loans are not protected like cash ISAs are.

- Some investors may still be attracted by the higher returns, even if thy are aware of the risks.

Personally I would avoid both products at the moment – the returns aren’t high enough for the risks involved.

And there is no tax-efficient way to invest other than:

- Giving up my ISA allowance for the year, or

- Buying the P2P investment trusts, which have generally underperformed.

Kate also reported that the Funding Circle P2P investment trust – Funding Circle SME Income – is to be wound up.

During 2018 the board revised down its return expectations, saying it expected net asset value total returns of just 4% in 2019 — a way behind its original target of 6-7% — and revealing it did not expect to pay a covered dividend until 2020.

Funding Circle itself said that it had moved away from the trust for funding, with only 3.5% of its origination volume in 2019 coming from the fund.

The company said it intended to raise £200m from UK institutional investors over the next few years and announced two new institutional funds to back loans on its platform — a UK private direct lending fund and a UK bond product.

Funding Circle lost £51M in 2018, a 40% increase despite a 55% jump in revenues.

Quick links

I only have three for you this week:

- Flirting with Models revisited The Weird Portfolio

- Alpha Architect said that Short Selling + Insider Selling = Bad News,

- And also wrote about The Momentum of News.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

Interactive Investor will only charge 99p per regular investment trade. This will be taken from the £7.99 “free” trading credit awarded each month. So for £9.99/month you can get about 8 purchase trades, so long as you are happy with autopilot investing (occurs around middle of each month).

Yes, I ignore “regular” investing as I don’t do it. Passive investors with small pots are the target market for that, I imagine. I trade pretty much every day, so the cost of standard trades is important to me.

What I’m most surprised by is that AJ Bell’s £100 a year SIPP hasn’t been challenged by anyone in many years. Vanguard are taking forever to get their SIPP platform going.

“Merryn is worried by regularly recurring proposals that pension money should be able to be used as house deposits.”

I believe it is an idea from Singapore where one can borrow from pension pot for house deposit, but have to pay back in timely fashion.