Weekly Roundup, 10th May 2021

We begin today’s Weekly Roundup with bitcoin.

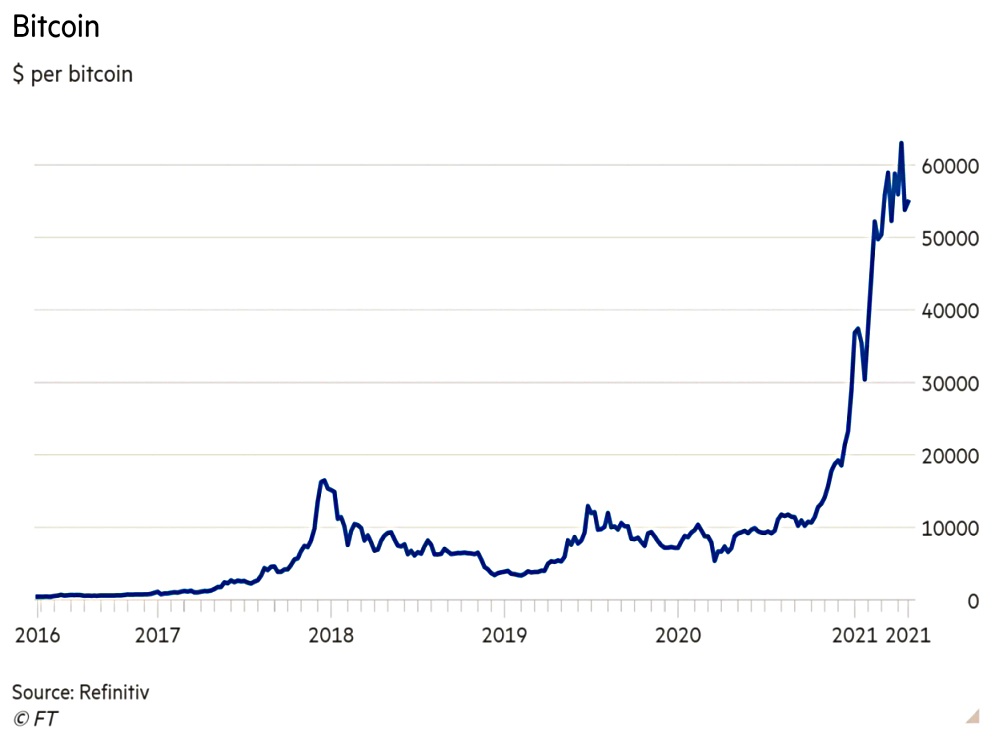

Bitcoin

In the FT, Eva Szalay wondered whether bitcoin was a bubble, or too good to miss.

- Or in other words, is it Too Good to be True?

BTC is up six times in a year (from $7K to $54K at the time the article was written).

As well as the price rise, we’ve seen more “mainstream” support than during the 2017 bubble, from Elon Musk, hedge fund managers and now – according to rumour – JP Morgan.

- And a couple of weeks ago, we had the IPO of Coinbase, at a market cap equal to that of BNP Paribas (founded in 1848).

Eva warns that the wider crypto space is still home to lots of scams.

- There is little protection (or tax-sheltering) available in the crypto space, so you need to be convinced by the potential for price appreciation, and to be prepared to diversify your holdings and counterparties.

Eva also notes an age gap:

In contrast with younger investors, those aged 55 or over remain resolutely on the

margins with just 8 per cent of survey respondents in this age group trading digital

currencies, [a] Charles Schwab study found.

And she mentions the environmental footprint of crypto:

The carbon emissions associated with bitcoin equal that of Greece, according to

research by Bank of America.

It’s a different country every week, but what I would like to see is the energy cost of other activities – computer gaming, say, or gold mining or the existing banking system.

- Everything costs (transforms) energy, and hence usually costs carbon too.

Eva says that the more sober BTC enthusiasts recommend an allocation of only 1% to 2% of your portfolio.

- And you should obviously avoid leverage on such volatile assets.

Crypto derivatives are banned for UK retail investors, though you can still buy blockchain ETFs.

Luno, a crypto exchange, found in 2020 that 55% of its clients had no other investments than crypto. Luno CEO Marcus Swanepoel, said:

Never spend more money than you can afford to lose. It’s very risky, there is no doubt about it.

In terms of exposure, Eva mentioned Coinbase and Revolut, which are both too expensive for me (particularly Revolut).

- Luno looks a better bet (though they are the firm responsible for the infamous bitcoin ad on the side of a London bus).

Crypto derivatives are banned for UK retail investors, though you can still buy blockchain ETFs.

Berkshire

Last weekend was the Berkshire Hathaway annual shareholder’s meeting – “Woodstock for capitalists”.

- It was held online for the second year running, and you can watch it all on YouTube.

Despite the lack of crowd, there were a few interesting things said.

Buffett and Munger were asked about bitcoin and as usual, Warren sidestepped:

We probably got hundreds of thousands of people watching that own bitcoin, and we probably have two people that are short. So we got a choice of making 400,000 people mad at us and unhappy, and, or making two people happy, and that’s just a dumb equation.

But Munger gave it both barrels:

I hate the bitcoin success and I don’t welcome a currency that’s useful to kidnappers and extortionists, and so forth. Nor do I like just shuffling out of extra billions and billions and billions of dollars to somebody who just invented a new financial product out of thin air.

So, I think I should say modestly that I think the whole damn development is disgusting and contrary to the interests of civilization.

As usual, bitcoin maximalist declared that Berkshire’s opposition was “good for bitcoin”. (( They say this whatever happens ))

- Perhaps they are right.

Like everything else in the world right now, bitcoin is dividing the investment community into two entrenched camps.

- Stock-picking value investors – who are usually old guys – won’t touch it.

- Lots of newer “investors” – who are usually young guys – think that everything else is doomed.

At the moment, I don’t meet many people in my middle camp of thinking this might be another store-of-value asset class that is worth allocating 1% or 2% of your portfolio to. (( Note that I have not made this allocation to date ))

- I think there will be many more like me in a couple of years, as institutional penetration continues, and easier and safer ways to hold bitcoin are introduced.

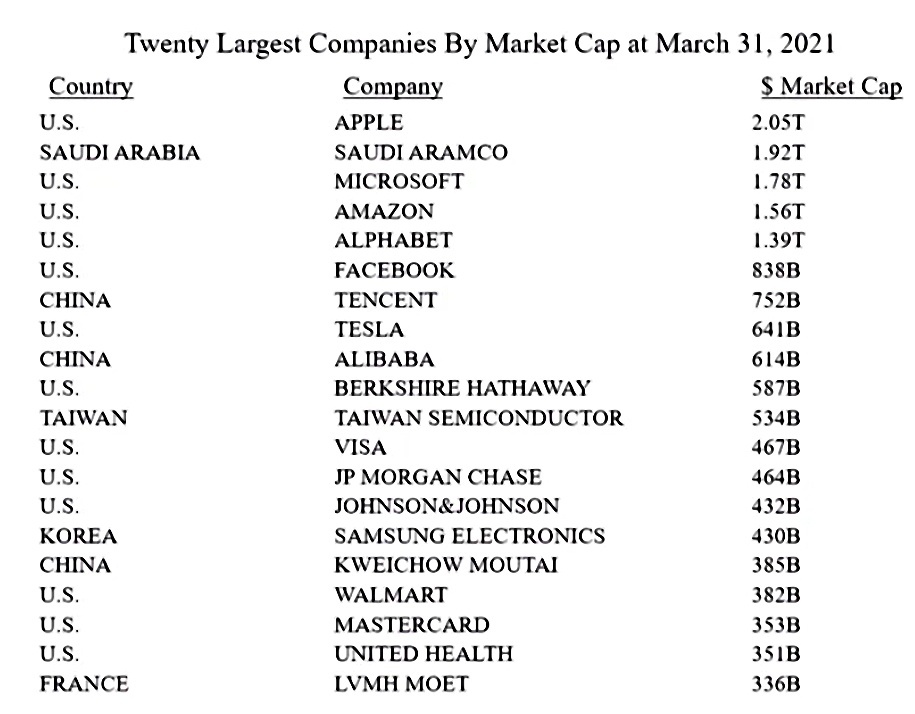

A second interesting topic was the changing nature of success.

- A slide showing the largest firms of 2021 features a lot of US companies at the top.

The same list from 1989 was dominated by Japanese firms.

- And none of the 2021 US firms was present.

Buffett pointed out that the best ideas of 1989 did not turn out so well.

We were just as sure of ourselves, and Wall Street was, in 1989 as we are today. But the world can change in very, very dramatic ways.

It’s a great argument for index funds. The main thing to do is be aboard the ship.

He also talked about the automobile craze from his father’ youth:

Everybody started car companies just like everybody’s starting something now that can be where you can get money from people. There were at least 2,000 companies

that entered the auto business, because it clearly had this incredible future.In 2009, there were three left, two of which went bankrupt. So, there is a lot more to picking stocks than figuring out what’s going to be a wonderful industry in the future.

The tension between value investing (( In its broadest sense, since Buffett isn’t really a value investor anymore )) and crypto leads into the question of whether Buffett and Munger – arguably the greatest investors of all time – still have relevance.

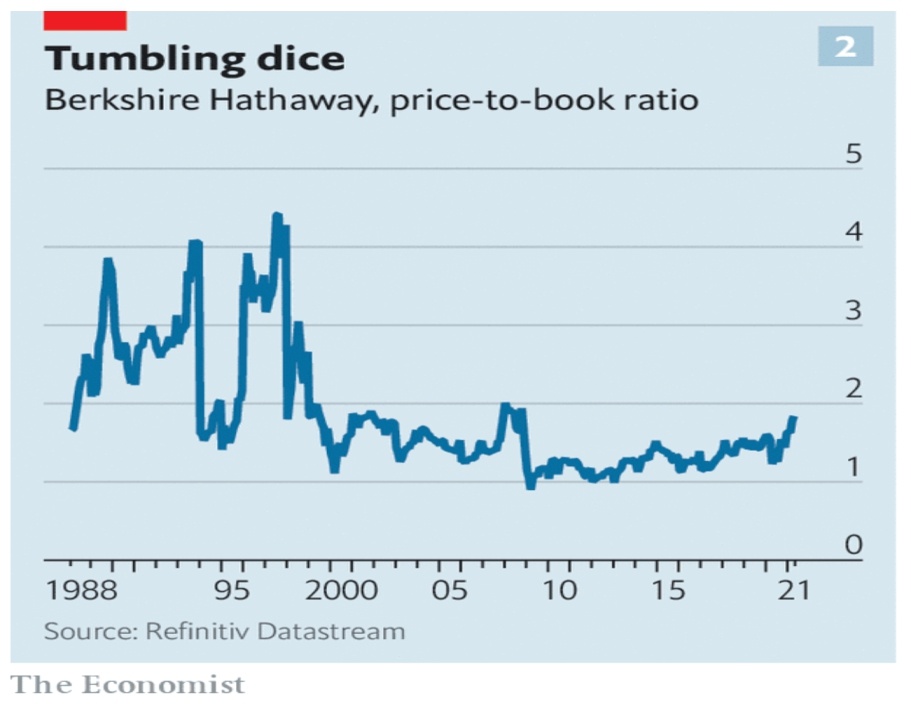

- They are very old, and Berkshire has underperformed the S&P 500 for more than a decade.

They were very late to tech, and growth investing has never been their thing.

- They are also long-time gold bears (calling the metal a “pet rock”), so bitcoin was never likely to appeal.

And the enormous scale of their conglomerate acts against them (hence the massive cash pile for which they can find no use).

- With inflation on the way (as they admit themselves), finding a home for this cash is more urgent.

Berkshire groupies will also have been excited to hear that Greg Abel – head of Berkshire’s noninsurance operation – will be Warren’s successor.

- Abel is widely regarded as a safe pair of hands, but the Economist thought that BRK will struggle to outlast its founder.

Berkshire has long enjoyed a sort of corporate exceptionalism, thanks to the halo over Mr Buffett. With disquiet growing over so-so returns, poor disclosure and more, that benefit of the doubt looks threatened.

The newspaper notes that apart from the disadvantages of large scale, one of BRK’s long-term advantages has evaporated:

Berkshire has long used the float (premiums not paid out as claims) from its giant insurer, Geico, to funnel low-cost capital to its other operations. But these days capital is cheap for everyone.

There have also been bad bets on Occidental Petroleum, Kraft Heinz and airlines, and over-paying for Precision Castparts.

- In acquisitions, BRK faces greater competition from PE and SPACs.

Berkshire is also starting to attract woke flak:

Mr Buffett has little time for ESG metrics, diversity targets and the like. He has said he doesn’t want his managers to have to spend their time “responding to questionnaires or trying to score better with somebody that is working on that”.

A lot of what is considered good governance today doesn’t fit with Berkshire’s heavily decentralised approach.

At the conference, Warren said:

Chevron is not an evil company in the least and I have no compunction about

owning Chevron. I think Chevron has benefitted societies in all kinds of ways, and I think it will continue to.I don’t like making the moral judgments on stocks. There’s something about every business that [if] you knew what, you wouldn’t like. If you expect perfection in your spouse or your friends or in companies, you’re not going to find it.

When Warren is gone, his role will split into three:

- Abel will be CEO

- Buffett’s son Howard will be Chairman, and

- The investment chief will be either Todd Combs or Ted Weschler.

And there will be pressure to similarly split BRK in three:

- insurance

- industrial firms

- consumer businesses

BRK’s conglomerate discount is around 5% and might rise to 10% post-Warren. But he points out the advantages of not being tied to the status quo in a single industry:

If horses had controlled investment decisions, there would have been no auto industry.

There are also tax advantages over the movement of capital between businesses.

Ultimately the shareholders will decide, and 70% of BRK is owned by Buffett and one million other loyal individuals.

- Which makes a break-up unlikely in the near future.

Buffett’s share will be sold into the market by charitable foundations over a decade, and many of the other shareholders will eventually pass them on.

- So BRK will change, but perhaps not until the 2030s.

Investing exam

In the wake of its report on self-directed investors – which we covered last week – the FCA has launched a discussion paper that proposes that people should be forced to take an online test before they can invest in “high risk” assets.

- They might also be forced to watch “educational” videos.

And the FCA floated the idea that investors might have to declare their salary, net assets, previous investing history and other personal information as part of the sign-up for certain products.

- They are also considering the introduction of “frictions” such as requiring a text message confirmation before an investment is made.

Responses to the paper are due by 1st July.

FCA director Sheldon Mills said:

We want to deliver a consumer investment market that works well for the millions of people who stand to benefit from it. We are concerned that too often consumers are investing in high-risk investments they don’t understand and can lead to significant and unexpected losses.

We have already taken action by banning the mass-marketing of speculative minibonds. We continue to address harm in this market through our ongoing supervisory and enforcement action but recognise more needs to be done. Our latest proposals would further reduce the risk of people taking on inappropriate, high-risk investments that don’t meet their needs.

The discussion paper also asks whether more types of investments should be subject to marketing restrictions.

- Oh, goody – more red tape for those of us who know what we are doing – driven by red faces at the regulator from their mishandling of the “mini-bond” scandal.

Negative rates

Den Danske Bank has announced that the threshold for charging negative interest rates will come down from DKK 250,000 to DKK 100,000 on 1st July 2021.

- The existing limit equates to a surprising low £29K, but the new limit is just £11.7K

The official negative rate spread is -0.75% to -1% pa, but personal accounts will be charged -0.6% pa.

- The Netherlands has similar plans, but only on accounts holding more than €100K.

The Bank of England recently gave UK banks six months notice to get ready for negative rates, but there has been no suggestion as yet that negative rates will apply to personal balances.

Quick links

I have five for you this week, with four from The Economist:

- The magazine looked at Apple’s court battle

- And at the digital yuan

- And at central bank digital currencies in general

- And at how B&M has quietly become one of Britain’s most successful retailers.

- UK Value Investor said that the FTSE-100 CAPE signals close to fair value, despite near-record prices.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.