How I Invest 2

Today’s post is our second visit to How I Invest My Money by Joshua Brown and Brian Portnoy.

![]()

Contents

Tyrone Ross

Tyrone Ross is a financial consultant who hosts the Human Advisor Podcast.

- He grew up poor but made it to Wall Street, ending up at Merrill Lynch.

I left Merrill to go independent in 2017 after learning about Bitcoin in 2015 and working with startup founders in 2016.

The majority of my investments are tied up in cryptoassets and the equity of private companies. I do own a few stocks here and there, put money away in retirement accounts, and recently opened an HSA.

Well, that makes a change, though it’s not a mix that you could recommend to many people.

Dasarte Yarnway

Dasarte Yarnway is the Founder of Berknell Financial Group, an independent wealth management firm focused on “helping millennials and seasoned investors design their best lives”.

- He has a weekly podcast (The Young Money Podcast) and has written three books – Dating Benji (2016), Young Money (2018) and Pay Me In Equity (2019).

I am a first-generation Liberian-American man, born to parents who fled their homeland before a deadly civil war. I’ve experienced devastating loss, repeatedly, and these events have conditioned me to value time.

If I value a particular thing, person or place, I want to invest my money there. If I am also spending a significant amount of time on said thing, person or place, I also will consider investing there.

If something buys back time, I’ll certainly invest my money there, because then I can reinvest the free time on more of what I value.

After that preamble, where is Dasarte’s money?

Most of my net worth is tied to my business. I continue to invest my money in the creation of businesses that will offer [social] impacts.

I have a SEP IRA for retirement planning. I align my portfolio with the investments of my clients. Roughly 25% is in individual equities – particularly in companies that align with my values, or through fundamental analysis that I believe will withstand the test of time.

Some are speculative, some aggressive, and a good chunk are proven companies with dividends. I love individual stocks because I believe that here is where premium returns are made, if and only if, you have the stomach for the inevitable volatility.

The larger bulk of my investments are comprised of exchange traded funds. I rebalance two times per year on average.

Nina O’Neal

Nina O’Neal is a Partner with Archer Investment Management.

- She started out in fashion PR before moving to an institutional money manager and then becoming a financial advisor with Merrill Lynch.

Nina’s kids are in private school and her husband is a small business owner, so a lot of her time is spent i juggling cashflow, using multiple accounts.

- Excess cash goes into a joint brokerage account.

I prefer not to invest my own accounts and do not purchase securities for my own accounts. I utilize third-party money managers to manage my brokerage account. I tend to be pretty aggressive. I invest in mutual funds and exchange traded funds. My biggest investment is the business that I co-own.

None of us know how long we have in this world with those that we love. Whether it is too short or very long, we have to prepare to live well both in the present and in the future.

Yet another vanilla strategy, I’m afraid.

Debbie Freeman

Debbie Freeman is a Principal of Peak Financial Advisors in Denver, Colorado. Before that she was an accountant with Deloitte.

- Debbie has always used debt – car loans, student loans and now a mortgage.

I have a Roth IRA where I invest in individual equities. I typically buy companies I understand and use in my own life.

Debbie reasons that the potential upside of individual stocks will be tax-sheltered in this account.

I also have a simple IRA invested in the models we create for our clients. I contribute every month and my firm has a match. It is a mixture of ETFs and mutual funds, and we are active in adjusting the allocation.

The largest component of my savings (usually around 10% of my pay) goes into an online savings account. This funds my annual equity purchase with the firm.

The last component of my savings and investing habits is my absolute favorite. It is my monthly deposit into an online savings account exclusively for a dream vacation when I turn 40.

The suicide of her brother has convinced Debbie that it’s worth spending to “take time to grow through travel and adventure”.

- It’s another simple plan – funds, stocks, a house and equity in the business she works in.

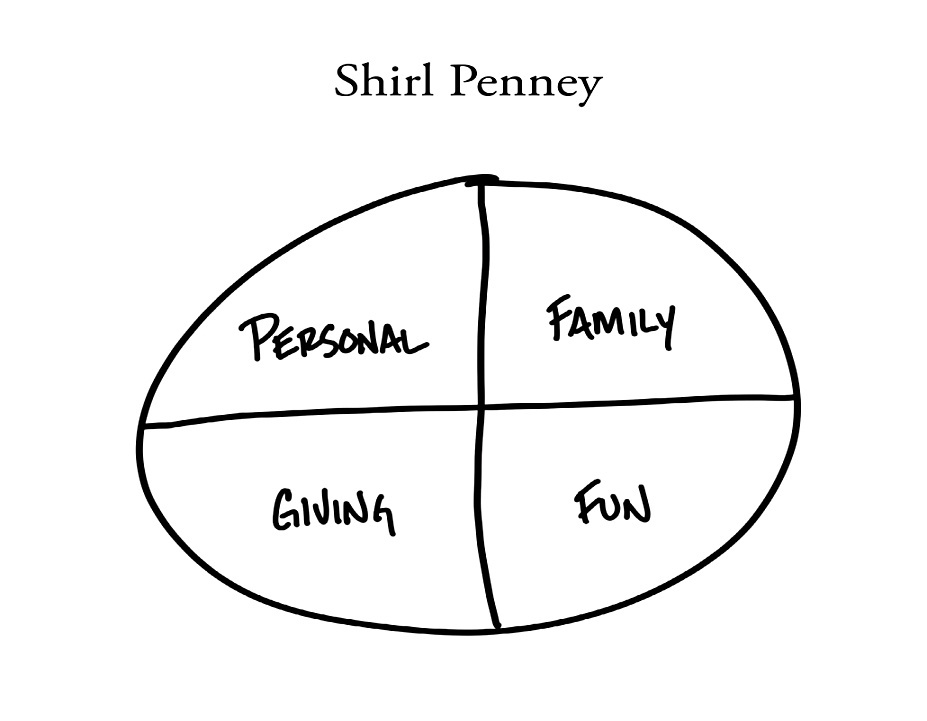

Shirl Penney

Shirl Penney is the founder of Dynasty Financial Partners. Before that he worked at Citi Smith Barney.

A substantial portion of my net worth is still riding alongside the other equity owners and partners at the firm.

As well as that, Shirl has four “pools of capital”:

Personal capital (Mary Ann and myself ), family capital (our two daughters and nieces and nephews, etc.), philanthropic Capital (we focus on education, ALS, and helping military families), and our “fun” capital bucket (assets we like to enjoy but where we are not fixated on financial return).

We invest in a diversified portfolio of index funds in the core portfolio, managed money for small cap and international, and currently have a 10% allocation to both fixed income and cash.

Of the 80% in growth investments, roughly 50% is in public markets and the other 30% is in alternative investments, split between a handful of funds in the private equity and real estate space, and direct investments in companies run by teams I believe in that are not in financial services.

The family pool is mostly Dynasty equity.

Our philanthropic capital is invested the most conservatively of our pools, with domestic equity indexing in core at roughly 30%, with a high dividend value manager at 20%, 25% taxable xed income, 15% international mutual funds, and 10% in cash.

The fun money is “H&H” – houses and thoroughbred racehorses.

- Shirl sounds rich, and can perhaps afford his overconcentration and his non-productive assets.

There’s not much here for the typical private investor, though.

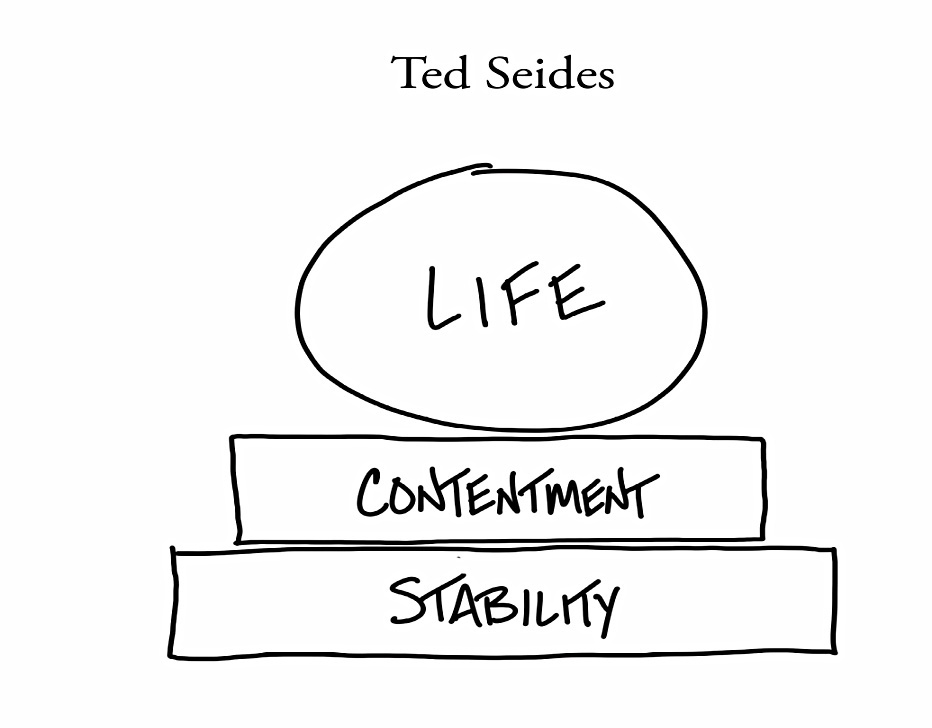

Ted Seides

Ted Seides is the Founder of Capital Allocators “created in 2016 to explore best practices in the asset management industry”.

- He hosts the Capital Allocators podcast.

Before that, he was a founder of Protégé Partners, an alternative investment firm that invested in and seeded hedge funds.

- And before that, he worked under David Swenson at the Yale University endowment.

He’s also famous for losing a 10-year bet with Warren Buffett that a bunch of hedge funds would beat the S&P 500.

During my time managing hedge fund portfolios, I was restricted in what I could own and invested most of my capital alongside my clients. Those investments were wildly suboptimal for me. Hedge funds are generally tax inefficient and assume less risk than I wanted.

So now Ted does things differently:

I leave a buffer in cash to protect against lean years. I’m comfortable with equity market volatility, and I don’t believe in marketing timing, so I stay fully invested.

I’m a good contrarian buyer, a mediocre short-term trader, a reluctant seller, and a serene owner through choppy markets. I also love investing in outstanding people pursuing value-added strategies.

Sadly, this sounds better than it is.

- Ted follows a buy and hold strategy with stocks, funds and ETFs.

I hold index or factor ETFs in absence of something better to do, but I much prefer active management. Most of the single names in my portfolio take the form of replicating an investment in a manager. I tend to have a value bias in my manager preferences, so I own a few growth stocks to balance out the exposure.

He mentions AMZN, GOOG and SHOP.

I fill out my stock portfolio with a small opportunistic bucket of fliers, partly for the lure of option-like upside in dynamic sectors like biotechnology. I certainly know my way around the hedge fund space, but I don’t invest in hedge funds. I see valuable merits for outstanding hedge funds in tax-exempt institutional portfolios.

But not so much in taxable accounts.

Outside of the public markets, I invest in a few private equity funds with managers pursuing unusually attractive strategies

Ted’s portfolio is a little closer to what I would regard as optimal, though he doesn’t really get down to the nitty-gritty, or completely explain his positions.

Ashby Daniels

Ashby Daniels is a Financial Advisor with Shorebridge Wealth Management. He works with people at or nearing retirement and has a blog called Retirement Field Guide.

- He writes a lot about lifestyle:

Few people discuss the impact lifestyle choices can have on their financial future, but I believe it will account for about 80% or more of our personal financial destiny. It’s not going to be the fund choices or any other tactical decision that will determine our success. It will be our ability to live well below our means.

Savings rate certainly counts, especially in the beginning.

- But if you stick with things, eventually asset allocation – along with costs and taxes – become more important.

Ashby doesn’t like debt.

The only debt we maintain is our mortgage due to the low interest rate.

He has a 100% stock portfolio for retirement and college fees, and even for his emergency fund. He has no fixed income because:

We have no short-term goals. Anything that reduces short-term volatility must also reduce long-term return.

Not quite true, but I see where he is coming from. Ashby doesn’t try to beat the market.

The quest for alpha is entirely out of my control and because it is entirely unnecessary for achieving our financial goals. Attempting to beat the market must also introduce the risk of underperforming the market.

We invest our portfolio into a diversified mix of index funds and other than rebalancing our accounts, we do not touch them.

He doesn’t believe in portfolio optimisation since it is necessarily based on historical data.

But he also believes in insurance, which is understandable when you are working and the sole provider:

I have enough life insurance to provide for my family in perpetuity and cover our education goals if something should happen to me. I have disability coverage to provide for my family if I am unable to work, and we have adequate liability insurance for the remaining what-ifs.

Conclusions

That’s it for today.

- We’ve looked at thirteen “investors” so far, and there are twelve more to come, which means that there will be another two articles in this series, plus a summary.

I don’t think that we’ve learned very much from the first half of the book, but who knows what the second half will bring.

- Sadly, more of the same, I expect.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.