Irregular Roundup, 19th February 2024

We begin today’s Weekly Roundup with ISAs.

British Isa

This week’s episode of Budget Watch focuses on the rumours of a British ISA.

- Current thinking is that this might be a separate £5K annual allowance on top of the regular ISA, with the BISA exempted from stamp duty (which is one of the things that puts me off investing in UK shares).

This would tie in nicely with government plans to sell the 39% of NatWest that it still owns (since the 2008 bailout).

- There might also be a market cap limit to favour small- and mid-caps (which obviously wouldn’t help the NatWest sale).

It would be interesting to see whether UK-listed investment trusts (which would allow you to invest pretty much anywhere and/or in anything) would be included.

- Although it adds yet more complexity to the UK investment landscape, I would like to see the BISA happen if only because it’s a more palatable way to raise the annual ISA allowance (which is what I really want).

What I really don’t want to see is a forced allocation to UK stocks within existing ISAs, or at least not a large allocation.

- We have 19% of our net worth in ISAs and say a 50% UK allocation would be an uncomfortably large lump of UK stocks (given the UK’s share of global stocks is around 4%).

I think a lot of people probably already have a large allocation to the UK within their ISAs, but I would very much prefer not to.

And with the CGT annual allowance coming down to £3K, investing internationally outside of a tax shelter is also unattractive.

UK Stock Market

The BISA would be expected to help counteract the flow of capital way from the UK stock market, but there are bigger obstacles to overcome:

- the economic outlook is not favourable in comparison to say the US

- our mix of industry sectors is less favourable (particularly the absence of tech)

- we have no successful recent IPOs to point to (there was a Kazakh airline float last week, but you know what I mean)

- PE ratios are lower here (which puts off potential IPOs), as is liquidity

- stamp duty on non-AIM stocks (at 0.5%, the second highest in the world) is a headwind

- As mentioned above, the CGT allowance is miserly

- UK pension schemes used to allocate 50% of their pots to UK stocks back in the 1990s, but it’s more like 5% these days

Other than the abolition of stamp duty, I can’t see these issues being resolved, and I think the best days of the UK market are behind it.

- We need a pan-European exchange to provide a meaningful alternative to the US.

Active vs Passive

For Bloomberg, John Authers noted that passive investing is under attack again.

The current debate was kicked off by David Einhorn of Greenlight Capital:

Passive investors have no opinion about value. They’re going to assume everybody else has done the work.

Charles Gave ofGavekal Research says:

Indexation will destroy capitalism.

And way back in 2016, Alliance Bernstein’s Inigo Fraser Jenkins said:

Passive investing is worse for society than Marxism.

The debate has reignited for two reasons:

- The market share of passive continues to rise (it’s passed 50% in the US now), and

- The concentration (market share held by the leaders) of the US market also continues to rise, driven by inflows to passive funds.

As long as passives are growing, they will tend to push up the price of the leaders by taking the price available in the market,

- The global focus on the Mag Seven tech firms makes this effect more widely known.

Generally over history, it’s been a bad idea to buy the biggest stocks by market cap. Almost by definition, all the good news is in their price, and there is nowhere to go but down.

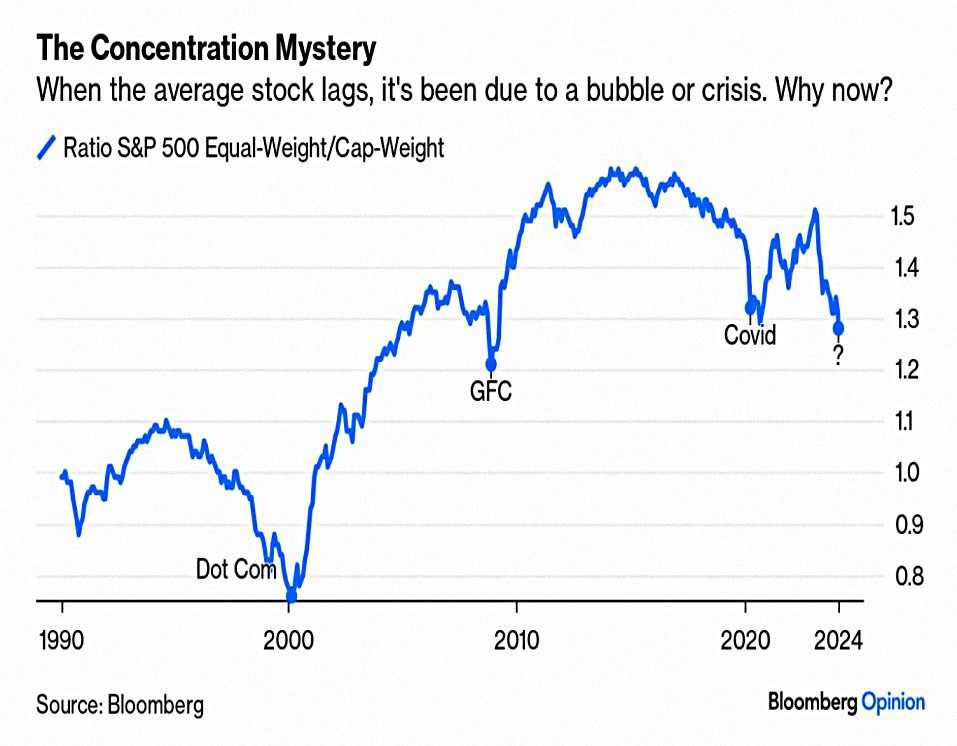

John’s chart compares the equal-weight S&P 500 to the market-cap weighted version.

Most of the time, the equal-weight does better, because it isn’t so heavily skewed to companies whose good news has already been priced in. Periods when the equal weight markedly underperforms are rare. They tend to come during periods of serious stress (the Global Financial Crisis or Covid ) or during a bubble (the dot-coms in 2000).

Since there is little stress at the moment, perhaps we have a bubble?

Gave points out that the US stockmarket is now about 70% of world market capitalization, even though its economy is only17.8% of global gross domestic product. Therefore, the markets are implying that “over the next 20 years, less than 20% of the world economy will earn three times more profits than the remainder” or that US tech firms will be“entrenched global monopolies stretching into perpetuity.”

But even if passive is helping (along with AI frenzy) to inflate a bubble, its lower costs mean that it will outperform, making it a sensible choice for most investors.

- At the same time, 100% passive would mean no price discovery and broken markets.

Whenever concentration peaks, there is a great opportunity for active investors to prosper.

The years following 2000 were banner ones for value managers, and in many ways established the power of the hedge fund sector. This was an era when good stock-picking was rewarded, and when there were lots of stocks out there that were undervalued and ready to outperform the market.

As well as a tech bubble, the Mag Seven’s dominance also leads to a massive US vs international dominance (since the Mag Seven are all in the US).

- But does the rise of passive mean that these bubbles will last longer than the Nifty Fifty or the dot coms?

Or is this a once-in-a-generation opportunity to bet against concentration?

- Even if this is a great moment for the best active managers, as a whole they will lose to the index, so there’s no reason for the rest of us to abandon passives.

Nor should we want this:

A big recovery for active funds will require the chaos of a burst bubble. And if thepublic really loses trust in index funds and starts taking out money, after decades of netinflows, they could speed the collapse just as they sped the ascent.

At the same time, we could look for some ways to bet against the current bubbles.

Index-linked bonds

The Economist defended inflation-linked bonds whilst admitting that they are a poor inflation hedge.

One hundred dollars put into inflation-protected Treasuries in December 2021, when investors first saw American core inflation reach 5%, would have been worth just $88 a year later. Even cash under the mattress would have done better.

Investors have been pulling funds from their ETFs, and Canada and Germany plan to stop issuing them.

The lack of inflation protection does not come from the protected coupon but from changes in the bond’s price, which in turn reflects the current value of those future coupons.

- When real interest rates rise, prices fall.

As was made painfully clear during 2022 and 2023, few forces raise long-term real rates as sharply as a central bank ferociously tightening monetary policy.

But linkers are still useful since regular bonds are affected by both inflation expectations and real interest rates.

Inflation-linked bonds disentangle them: their yield more cleanly expresses the market’s pricing of real interest rates. Likewise, the gap in yields between a nominal bond and an inflation-linked one gives the market’s pricing of expected inflation, known as “breakeven inflation”.

Useful yes, but why buy them? The newspaper points out that they offer some protection:

They can outperform if inflation rises and central banks fail to raise rates in response, as in 2021 when most central bankers valiantly insisted that inflation was transitory. Shorter-duration inflation-linked bonds can provide payouts with lower exposure to rising interest rates.

Pension funds can also hold them to maturity and ignore price fluctuations.

- Indeed, they will often pay fully for them, dissuading other investors.

But linkers aren’t much use to regular folks, who would be better off holding gold and commodities, or even betting on falls in bond prices when inflation and interest rates rise.

Woodford

The 300K investors in the failed Woodford Equity Income Fund have been awarded another £230M in compensation, with the first payments due by April this year (only five years after the fund collapsed).

- The FCA says the award equates to around 77p in the pound for investors.

£2.56 billion has already been paid out from sales of the fund’s investments.

- The new award is against Link Fund Solutions (LFS), the authorised corporate director of the fund (responsible for monitoring and supervising the investments executed by Woodford).

The FCA has previously said that Link made ‘critical errors and mistakes’ which ‘caused significant losses for those investors who remained in the fund when it was suspended’.

- Campaigners are considering an appeal against the ruling, even though 94% of investors voted in favour of the arrangements.

Hipgnosis

The shareholders of Hipgnosis Songs (SONG – I have a small position) have voted through the contribution of £20M to any bidder’s due diligence costs.

- 90.9.% of those who voted (around two-thirds of investors) were in favour.

The idea behind the offer is to counteract the impact of the right of the current fund manager (Hipgnosis Song Management – HSM, part of Blackstone) to buy the catalogue for “fair value” within si months of its contract being terminated.

- The shares remain at a 53% discount to NAV.

Quick Links

I have a bumper nineteen for you this week:

- The Wall Street Journal said A Fund With a 94.9% Yield? You Guessed It, There’s a Catch

- Moontower wrote about Getting Paid To Flip Million Dollar Coins

- GMO said that things are Magnificently Concentrated

- The Economist wrote that Investing in commodities has become nightmarishly difficult

- And explained How the world economy learned to love chaos

- And asked How worried should Amazon be about Shein and Temu?

- And said that China’s stockmarket nightmare is nowhere near over

- And that America’s economy is booming. So why are bosses worried?

- Alpha Architect wrote about the Persistence of Growth and Value Stocks

- Discipline Funds asked Is the June Rate Cut Off the Table?

- UK Dividend Stocks said The UK’s 20-year house price bubble may finally be ending

- AQR explained yet again Why Not 100% Equities

- And ERN also looked at 100% Stocks for the Long Run

- Of Dollars and Data wrote about The Holy Sale of Investing

- Aswath Damoradan explained How Big Tech Rescued the Market in 2023!

- The FT noted that Japan’s Nikkei hit a 34-year high on a weak yen

- A Wealth of Common Sense said that All-Time Highs in the Stock Market are Usually Followed by More All-Time Highs

- Morningstar asked What’s Unique About Private Equity?

- And Fortunes and Frictions said that How You Average Matters

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.