Ratios and your finances

This week we will be using Ratios to look at the Income Statement and the Balance Sheet that we created last time, to see what they tell us about the state of our financial health.

Contents

Ratios

The main tool for analysing financial statements is ratio analysis, where we compare numbers in the statements to see if they match up properly to each other.

The kind of questions we will be asking include:

- do we have the liquidity to meet our pressing obligations?

- do we have too much debt (or too little)?

- are we using our money productively?

We also want to look at how things are changing over time:

- is our net worth increasing?

- have the ratios improved or worsened since the last time we checked?

So we need to hang on to the statements we produce each year (particularly the balance sheet), so that we can compare them to next year’s statement, and hopefully reassure ourselves that we are progressing.

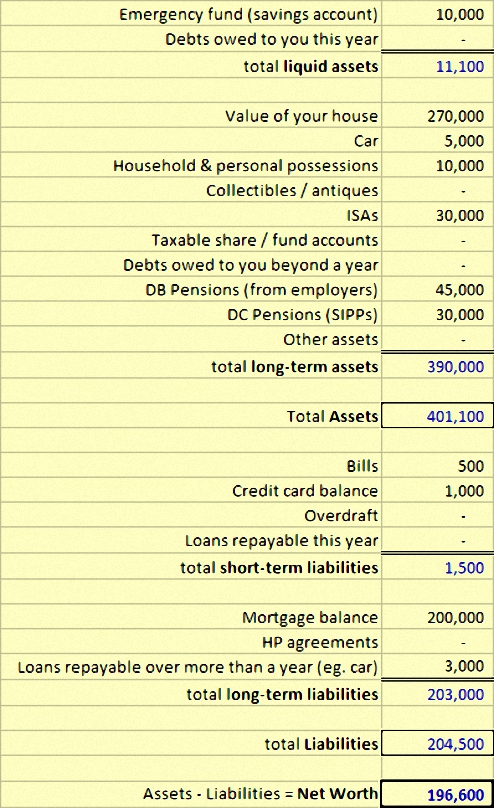

Our financial statements

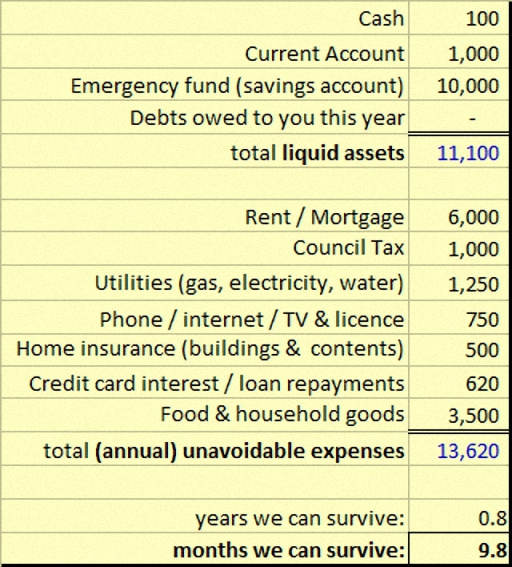

To refresh your memory, here is the income statement from last time. ((I’ve fixed a mistake here, where the car loan repayment wasn’t showing up in the income statement; I’ve also added the savings ratio to the bottom for later))

And here is the balance sheet:

They are very simple (and imaginary) but they will illustrate the principle of using ratios to investigate your financial health.

Which ratios?

There are lots of financial ratios to choose from, but we only need to consider a few. The main thing is that they answer an important question.

For some ratios there will be a “normal” value, a benchmark that we need to do better than. For others there will be a range of acceptable values. There’s no need to panic if you are the wrong side of the number, or outside of the range. You can always do better next time.

The point of the analysis is to find out where you are now, and in which direction you need to head. For those of you who can remember the days before satnav, it’s like reading a map: we’re looking for landmarks that we can aim for.

Here are the five ratios we will look at today:

- Emergency fund ratio (liquidity)

- Current ratio (liquidity)

- Total liabilities to total assets (debt)

- Debt payment to income (debt)

- Savings ratio (performance)

Emergency fund ratio

This ratio uses both the income statement and the balance sheet, and sets out to tell us how long our cash would last in an emergency.

We take the amount of liquid assets we have (from the balance sheet), and divide by the monthly unavoidable expenses (from the income statement). These are the things that we have to pay regardless of what happens (eg. even if we lost our job).

In the example I’ve used annual expenses to work out how many years our cash would last, and then multiplied this by 12 to work out how many months it would last.

Our answer is 9.8 months, which is very good. This is mostly because we have a £10K emergency fund on our balance sheet. The target for this ratio is six months, because in practice most people are able to rebuild their financial situation (eg. find a new job) in this time.

Don’t panic if your answer is three months, that still puts you in a much better situation than most people, and you can just work towards six months. If your answer is less than three months, you need to think about what steps you can take right now to get some liquid funds together.

It’s worth pointing out that you can also have too high a number. If you are a very cautious person, you might want your cash to last for a year. But any more than that and you could be working your money a bit harder. So in this example we’re getting close to that limit.

The current ratio

This is a balance sheet ratio and looks at whether we can meet our short-term obligations. We take our liquid assets and divide them by our current liabilities:

Our answer is 7.4, which again is very good. Normally the target for this ratio would be about 2, and certainly no less than one (this would mean that immediate steps should be taken to free up more cash).

A ratio as high as 7.4 is in one sense an indicator of inefficiency, since all this liquid money could be put to better use, but many long-term investors will find themselves in this situation. As short-term debts are eliminated, the cash needed to act as an emergency fund becomes large in comparison.

Total liabilities to total assets

This is a debt ratio from the balance sheet (in fact it’s just an upside-down balance sheet):

Our answer is 0.51 or 51%. We have almost twice as many assets as liabilities. The target here is generally held to be anything under 40%, so we have too much debt. We need to start to pay down our mortgage balance and look for progress towards 40% from year to year.

- Anything less than 1 is a positive net worth, while anything greater than 1 is a negative net worth.

- As we continue to invest and reduce our debts, this ratio will become smaller and smaller. ((I have almost no debt left, and my ratio is well under 1%))

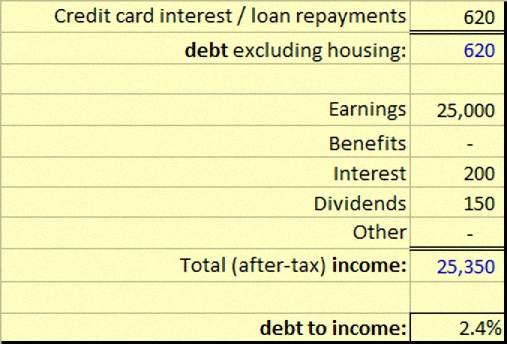

Debt payments to income (debt service)

This is a debt indicator from the income statement, and would normally exclude housing costs:

In our case, we have only a car loan to repay, and our ratio is 2.4% – that means that for every pound we earn, 2.4p is spent on debt repayments. This is a good number – we need to keep it under 10%, and definitely under 15%.

If it’s higher than 15%, then we probably need to look at paying off some debt, or reducing the interest rate or increasing the term of the debt.

Savings ratio

This one is pretty simple: it’s the amount left over at the bottom of the income statement which can be used for saving. It’s normally expressed as a percentage of annual income.

Looking at the income statement above, our answer is 11.8%, which is pretty good. The target is a minimum of 10%, but you may need to save more depending on your age.

Young people might want to add on any employer pension contributions here to make sure they get to 10%, but the real target is 10% from your own income. This is a good habit to get into – living within your means.

Young people will often find it harder to do better than 10% whereas people in their forties and fifties often find there is more money left over. Unfortunately, because of compounding it’s a lot more useful to save more when you are younger.

Now the 11.8% we have is good, but it’s not great. It doesn’t give much scope for increasing discretionary spending or taking on extra debt. We want to make sure that we have that minimum 10% left over every year.

From a point of view of financial security, we want to be increasing this ration to 20% or more (depending on our income). That means either earning more or spending less.

Next time we will look at making up a plan for the future from our statements and ratios.

Until then.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

I think you should include the current portion of long term debt on the current ratio calculation. Thus, the ratio will be lower and it is not going to signal inefficiency.

Hi Sena,

I think that’s fine. In the example above, the long-term debts are a mortgage and a car loan.

I suspect that only a small proportion of the principal is due in the next year, but given the size of the mortgage it might be a thousand or two. That would bring the current ratio down from 7.4 to something like 3.

The bigger point is that the current ratio is more useful to people with short-term debts (since it’s about your ability to pay them).

Long-term investors will have eliminated their debts but will still carry cash (an emergency fund, at least), so the current ratio will be misleadingly high.

Thanks,

Mike

Hi again,

This makes sense. By the way, I have just discovered your blog and loved it. It is way more beneficial than the blogs on how to save 60% of your salary by eating noodle only. Both the way you write things and the way your approach to the subjects are really good. I would say it is the most underrated early retirement blog I have seen so far.

Thanks,

Sena

Thanks Sena, you’re very kind.