Robo Advisors 16 – Exo Investing Interview

Today’s post is about robo advisor Exo Investing, and a chat I had with them a few months ago.

Exo Investing

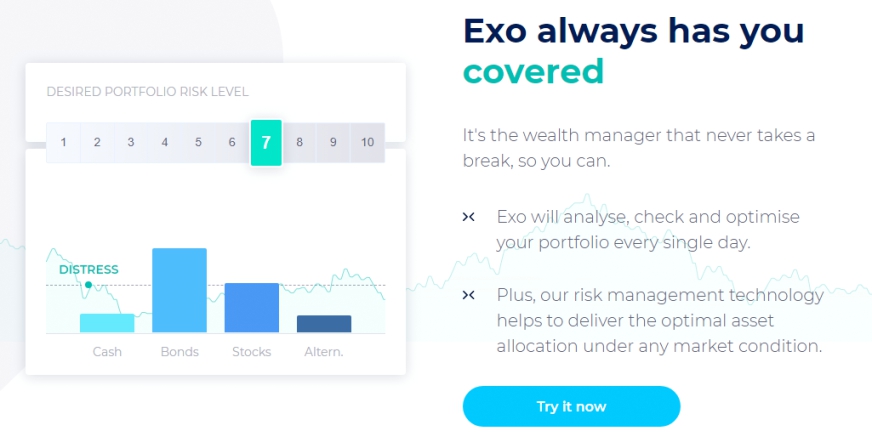

Our risk management technology helps to deliver the optimal asset allocation under any market condition.

Our algorithms have been used by institutions and UHNWIs for decades.

Exo Investing (( I need to use the full name because Google links Exo to a Korean boy band )) is a robo advisor which “does the hard work for you”.

- Their algorithms will use your preferences (sectors, regions, asset classes, plus risk appetite and investment objectives) to build a diversified portfolio of ETFs.

This is “tailored just for you” and “optimised each day” – Exo describe each portfolio as “unique”.

- More than 1,000 underlying ETFs could be used.

This level of individually tailored portfolio and risk management has never been available to the private investor before.

Exo is all about democratising access to sophisticated investment technology, using the latest advances in AI and risk management tools to break down the barriers to wealth and open the door to a new category of investing for as many people as possible.

To do all of this we’ve partnered with ETS Asset Management Factory, who launched back in 1987, and now has over €14bn under advice for large institutions.

Exo are backed by members of the Rothschild family and most of their staff are based in Madrid.

So far so similar to the rest, but Exo seem to trade on managing risk so that your path to your investment goals is a bit smoother than it might otherwise be.

- They also make a big deal of the AI / machine learning tech that underlies their portfolios.

The offer

Exo offer an ISA and a general (taxable) account (GIA).

- There’s a minimum investment of £10K.

- There’s no SIPP as yet.

Fees are 0.75% pa on the first £100K, plus a c. 0.25% pa for the underlying ETFs.

- That’s a pretty hefty 1% pa on the first £100K.

Above this the Exo fee drops to 0.5% pa (0.75% pa including the ETFs).

- So even at £500K the total fee is 0.8% pa.

Reweighting your portfolio (updating your preferences) is free.

At this stage, Exo sound like a (slightly) cheaper rival to Scalable Capital.

- They invited me in for a chat, so hopefully all will become clear below.

Interview

What do you see as your USP? The website mentions AI a lot, but this seems to be directed largely at reducing volatility. Is the pitch AI or low vol (aka “peace of mind” / “smooth”)?

That’s right. While we’re often testing the homepage messaging, the core principles are Peace of Mind, Time and Flexibility.

Outside of providing sophisticated tools that have never been accessible to this audience, Exo’s goal is to smooth your investment journey

Given that you have little track record, and the AI system functions somewhat as a black box, how will you get prospective investors to see the value of your proposition?

While we aren’t able to show a performance track record at this stage, we hope that showing (and providing access to) these sophisticated tools will bring across our value proposition.

We’ve now launched the portfolio evolution screen (your historic asset allocation), and we believe this will be a big draw as it’s something that simply doesn’t exist anywhere else on the market.

We also now have our first published user reviews which you can see via Finimize, and we now have some user case studies on the homepage to help you understand how the differences in current situation, outlook, preferences etc. will influence a portfolio over time.

Who is your target investor, in terms of: Age? Occupation / aspirations? Portfolio size?

Age 26-50 was our rough target, however we quickly found that clients and interest was coming from outside of this range. Our launch audience was professionals working in the city with a high interest in investing.

With the upcoming products and features we’re aiming to release through 2019, we’ll be targeting a much broader audience as we aim to help younger demographics become invested and also continue to build more complex features for the sophisticated investors already using Exo.

What is the average amount invested with you, per investor?

This is currently just under £20,000 however we expect it to push up towards £40,000.

Are you aiming at people who are DIY, “Do it for me” or “Do it with me”?

Exo is able to act in different ways for different clients as some like the control of adding in their investment preferences (and amending these preferences at any time) while others prefer Exo to simply create an optimal portfolio based on their profile.

We will soon (within the coming weeks) be releasing more variety across this as well. You’ll be able to work in three ways: let Exo’s AI create your portfolio, select an overall strategy (e.g. low risk, SRI, high returns etc), and finally you’d also have the ability to customise with your own individual preferences.

Why this segment of the market?

We believe there is a large gap where private banking is offering very sophisticated tools and experiences to institutions and UHNWs, some online platforms allow DIY investors to build their own portfolios but aren’t assisting them, and robo-advisers have done a great job opening up the retail end of the market to help people get invested – but with minimal sophistication.

While we may be getting great customer experience, interfaces, and branding, the underlying portfolios aren’t built for or managed for you as an individual, and that’s what we’ve brought to market.

How do you view your competitive position with regard to other robo-advisers?

Robo-advisers have done a great job opening up the market and making investing simple. However, they have their limitations.

Exo takes ‘robo’ to the next level by building unique portfolios, offering robust risk management by checking your portfolio daily and optimising as necessary

What about DIY investment platforms generally (eg. HL, YouInvest)?

These platforms act as great tools for DIY investors, however they require the individual to create a robust and diverse portfolio, and then have to monitor it themselves as often as they feel comfortable – daily/weekly/monthly.

This is both time-consuming and potentially risky if not checking often and rebalancing as necessary to stay optimal to your goals. They also open up the risk of human bias and emotion factoring into your decision-making, whether conscious or not.

And wealth managers (St. James Place etc)?

Wealth management and tailored financial advice will always be necessary for complex situations such as tax implications, inheritance, large-scale estate management etc.

However, for smaller investment portfolios, there can be a lesser need for advice given not only the high cost, but the issues that could arise with a human building your portfolio and not having the automated risk management in place.

How do you handle a client’s Risk Tolerance? Let’s start with how you measure it.

During the onboarding we look at a number of criteria to assess a client’s risk tolerance (e.g. net worth, monthly disposable income, cash reserves, etc), as well as their thoughts on different investor outcomes (e.g. variations on loss vs return and real market scenarios from 2008).

And what are the consequences (how does it affect asset allocation, do you use VAR etc)?

The risk assessment has a direct and indirect impact on the management of the portfolio. The direct impact is the allocation and distribution of assets between more volatile and less volatile as well as in riskier and less risky asset types.

The indirect impact is the extent to which the allocation is influenced by the client’s choices of preferences in choosing focus areas for their portfolio. This range is wider or narrower, think guard rails along a race track, depending on whether the client is more or less accepting of, knowledgeable of and capable to absorb risk.

Do you have a minimum investment amount?

Yes, this is currently £10,000.

What are your benchmarks?

We don’t operate off benchmarks as every person and therefore portfolio is unique.

You have tiered fees, which is very welcome, but don’t you think that platform fees should be capped rather than ad valorem? Have you any plans to bring your fees down further in the future?

We don’t envision reducing our fees for the current product as they sit very competitively across this market, especially when you factor in the service you’re receiving with Exo.

What we would like to do is build out our product offering and then see what we could do at different tiers for different products and features.

Do you have any plans to introduce “Networks” or “Circles” to allow groups of people (families) to club together to access the lower fees on larger pots? Would you consider paying introductory or ongoing fees to people who introduce such Networks / Circles?

We are currently building a generous referral programme, which will reward both parties.

This is now live, and offers £100 to a client who refers a new client, and six months of no fees to the new client. So it’s nothing like Networks or Circles (and there’s no reward for non-client referrers, such as bloggers like me).

We surveyed our current clients over the summer and asked what type of reward they’d prefer for referring a friend or family member to Exo. With that feedback taken into consideration,we believe we’ll have one of the best offers on the market.

At the moment you only really have one basic offer (albeit in GIA and ISA form). Are you planning to introduce any new offers in the future? What gaps will they cover? When will they appear? How much will they cost?

In time we plan to grow the platform to be able to take into account more of your overall portfolio, such as SIPP and individual stocks.

Both of these sit on our roadmap which looks at the next 18 months. As for price point, it’s hard to say at this stage.

How will the SIPP cope with decumulation (where smoothing is important) rather than the current “target date” approach? How will it deal with an investors other assets?

At its core the SIPP product would use the same daily rebalancing and fully automatic asset allocation engine.

The user journey into the product will look different to gather more data points that are relevant to pensions (total wealth situation, financial commitments, vulnerability, etc.) which in turn will influence the management of the portfolio.

Getting a cohesive picture of the client’s total wealth situation is the ideal scenario.

Can a saver split their pot across more than one plan (ie. have different preferences for separate pots of money)?

Yes for GIAs. Currently you can only have one ISA pot per year. It’s a mainly technical switch that we can implement if more users want that feature but not a priority to have this at the moment.

Can an investor phase / drip-feed their money into the market?

All money put into the account will be invested automatically – the client can easily achieve this by splitting their commits into regular monthly/quarterly deposits.

What are the underlying investments? Active / passive? Individual stocks chosen by a human? Index funds / ETFs?

Exo analyses every ETF on the London Stock Exchange.

Can an investor see the running cost / historic cost of their investments?

The fee is visible on the individual portfolio level scenario screens. All invoices are made available via the platform but we don’t add up the total cost and display this to the client.

You said these costs range between 0.19% pa and 0.25% pa.

Fund charges usually range from 0.07% to 0.75% per annum. At the moment, on average these funds have total expense ratios (TER) of 0.25% p.a..

These costs are deducted directly from the fund’s assets and are thus included in the price of the ETF. More details here.

Do you have asset allocation breakdowns available? I know you can access a list of the current day’s weightings, but are historical allocations available?

Yes. Within your portfolio you can see both your current asset allocation and your historic allocation to see how your portfolio has moved over time.

Do you have the average asset allocations across your entire platform available?

This is not currently available as every portfolio is completely different, however, similar to performance it may be something we are able to show when we have been going for a longer period of time and have more data.

What can you tell me about the AI algorithms? Does the testing use Monte carlo or real-world (sequential) returns? If the latter, from which markets and over which time periods?

Overall, we use different forms at different stages of the process, going from our universe definition, into building strategic portfolios, then building the tactical portfolios and using reinforcement learning to ensure the our models are continuously improving.

We don’t use Monte Carlo, this is a very classical method. For testing our methodologies, and to try and avoid overfitting, we have developed our Synthetic Financial Time Series generator, that is using real data to learn the patterns that drive financial time series. This is then able to create completely new and realistic scenarios that haven’t been presented before.

With this, we now have a bigger data set in which we can implement our methodology and test how we avoid overfitting. Because of this, our investment process is more robust and is designed to be better prepared for what is coming.

How does the GIA deal with CGT (since the investor cannot time his sales to implement tax-loss harvesting / keeping under the annual allowance etc)?

Currently there is no tax-loss harvesting functionality but it’s one of the more immediate items on the roadmap to take the tax situation into account.

At the moment you let investors choose assets and sectors that they want to include. Do you have any plans to add more options?

We’ll soon be adding ‘strategies’ (such as socially responsible investing, technology, value, etc). We’ll also be looking at adding ‘down-weighting’ as we know some investors may not have anything they have a preference to include by up-weighting.

Conclusions

I find the DIY management of a large portfolio time-consuming, and frequently tedious.

- When robo advisors appeared, I had visions of handing over a substantial portion of my money (a third to a half) over to a few of the better offerings.

I was particularly hopeful that “intelligent” algorithmic approaches – like Exo and Scalable Capital – would emerge.

- But they are too expensive for a DIY investor with a large portfolio to consider – Scalable Capital charges 1% pa, and Exo works out at 0.8% pa even on a £500K portfolio.

It’s relatively straightforward to put together a DIY solution for less than half that.

- It will be simpler and less intelligent than Exo but over the long run it is likely to outperform.

It seems to me that robos (in general, not just Exo) are still targeting relatively naive investors with not much money.

- Slick interfaces and references to AI play well with millennials, who will be less aware of the long-term impact of charges.

There are competitive options at the simpler, index-fund end of the market (PensionBee, evestor, Nest), but nothing cheap and clever has emerged.

Any attempt at differentiation in a crowded marketplace is welcome, but cost has to be part of the offer.

- Perhaps competition on price will only emerge after the market has consolidated into a handful of winners.

Or, perhaps – drawing from the market-leading and expensive example of Hargreaves Lansdown – only a tiny minority of investors care about costs.

- In which case we will get the robo advisors we deserve.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.