Warren Buffett’s Annual Letters – 2013

Today we’re going to look at another of Warren Buffett’s Annual Letters, this time covering 2013.

Contents

Buffett’s Annual Letters

Last week we looked at Buffett’s 50th anniversary letter, for 2014. The naming convention on these reports is a little confusing, as the 2014 letter was published in 2015.

We’ll follow the system that Berkshire Hathaway (BH) uses, and so today’s letter is the one that covers 2013, and was published in 2014 – they call that the 2013 letter. ((Note that in the commentary below, I will use the same tenses as in the letter, so the present tense refers to 2013, the future begins in 2014, and the past ends in 2012))

I realised that last week I didn’t include the link to the page where you can download the letters in full, so here it is.

The good news is that after last week’s marathon 42 pages, this letter is only 23 pages. I won’t repeat anything that we’ve come across before (for example, the 6-point plan to increase BH’s per-share intrinsic value in the future).

Performance

I won’t repeat the table from last week listing the company’s performance year by year, but instead here’s a summary of the performance over the entire 1965 to 2013 period:

- Compounded annual gain:

- in BH book value per share: 19.7%

- in S&P 500 (dividends included): 9.8%

- difference in the two (BH excess gain): 9.9%

- Total gain for the period:

- in BH book value per share: 6,935 times

- in S&P 500 (dividends included): 98 times

Note that the BH share price isn’t being used as a performance measure at this point.

During 2013, BH made 18.2%, or $34.2bn. Warren notes that BH’s intrinsic value is far in excess of its book value, and that this gap has increased in recent years.

This led to share repurchases in 2012 at 120% of book value. There were no repurchases during 2013, as the stock price never reached 120% of book value.

Warren expects BH to outperform the S&P in normal years. BH will not outperform when the S&P has a good year.

BH has underperformed in 10 of 49 years, with all but one shortfall occurring in a year where the S&P gained more than 15%.

2013 events

- BH spent $18 bn on buying all of NV Energy and a major interest in Heinz

- Significantly, the Heinz purchase involved a partnership with 3G Capital, led by Jorge Paulo Lemann, a friend of Warren’s. More partnerships with 3G are expected for larger acquisitions

- There were 25 “bolt-on” acquisitions to existing subsidiaries, totalling $3.1bn

- $3.5bn was spent on purchasing the remaining shares in two existing subsidiaries (Marmon and Iscar). Warren complains that they have to be entered into the books at only $1.7bn, increasing the gap between book value and intrinsic value by $1.8bn

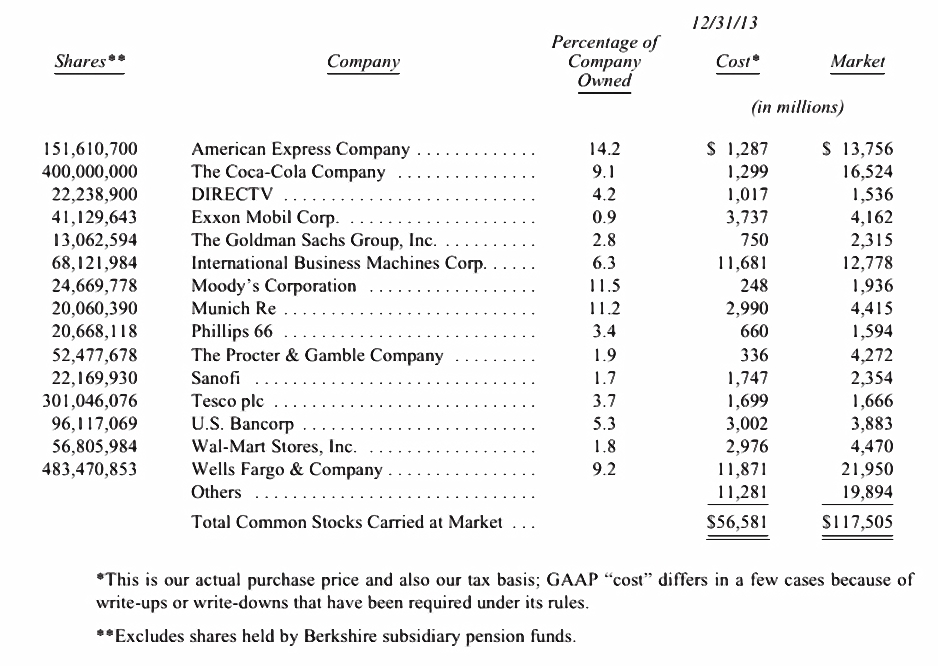

- More shares were bought in each of the “Big Four” non-subsidiary investments (American Express, Coca-Cola, IBM and Wells Fargo) – percentage ownership now ranges from 6.3% to 14.2%

With Heinz, Berkshire now owns 8 1⁄2 companies that, were they stand-alone businesses, would be in the Fortune 500. Only 491 1⁄2 to go.

Looking ahead

- Warren stressed the advantages of being willing to invest large sums passively in non-controlled businesses – BH needs to find sensible uses for the massive amounts of cash it generates

- Warren pledged to operate with at least $20 bn of spare cash and no material short-term obligations

Insurance

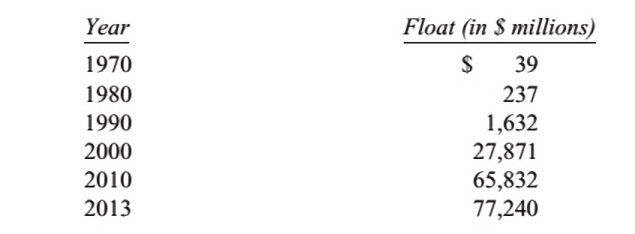

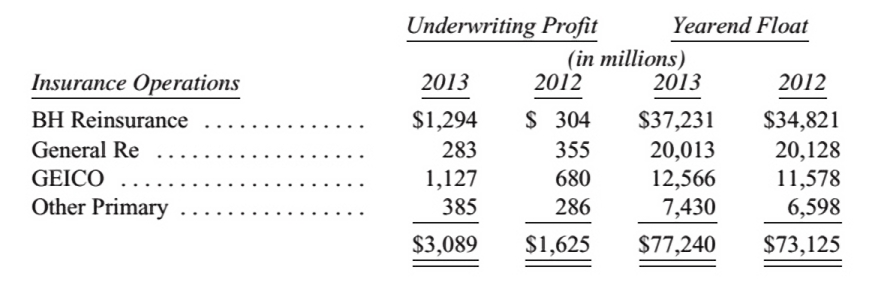

Warren began by stressing the importance of the insurance float (cash on hand from premiums received before payments are due). This can be invested in other operations.

BH’s float has grown impressively over the years (see above) but Warren doubts that the growth can continue, and an annual decline of up to 3% may be possible in the future.

BH managed to operate with an underwriting profit for the eleventh consecutive year, with earnings over the period now totalling $22 bn. Warren expects to continue to underwrite profitably in most years.

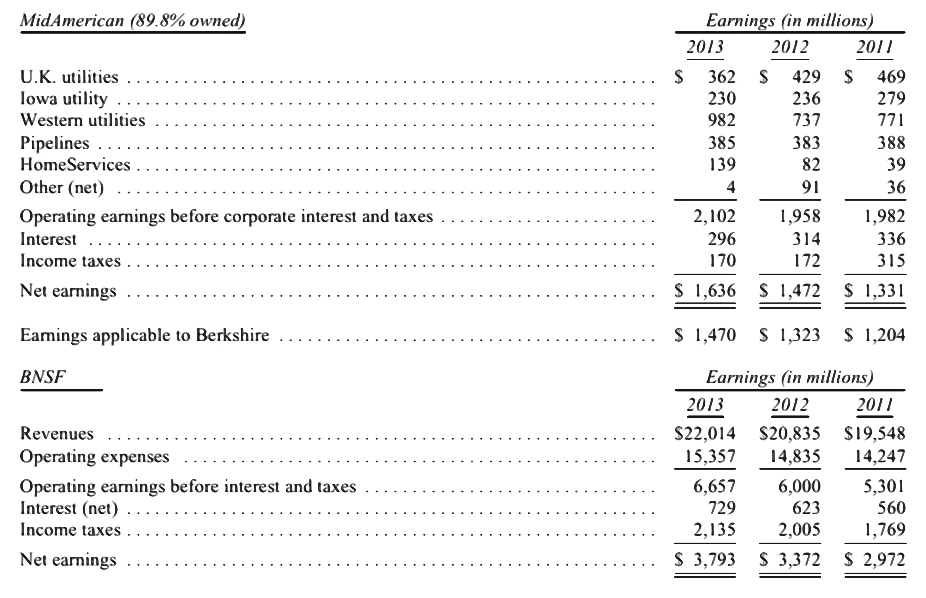

Regulated, Capital-Intensive businesses

As previously noted, ((In the notes to the 2014 letter)) BNSF (railroad) and Mid American Energy invest heavily in long-life, regulated assets and have large amounts of long-term debt which does not need to be guaranteed by BH.

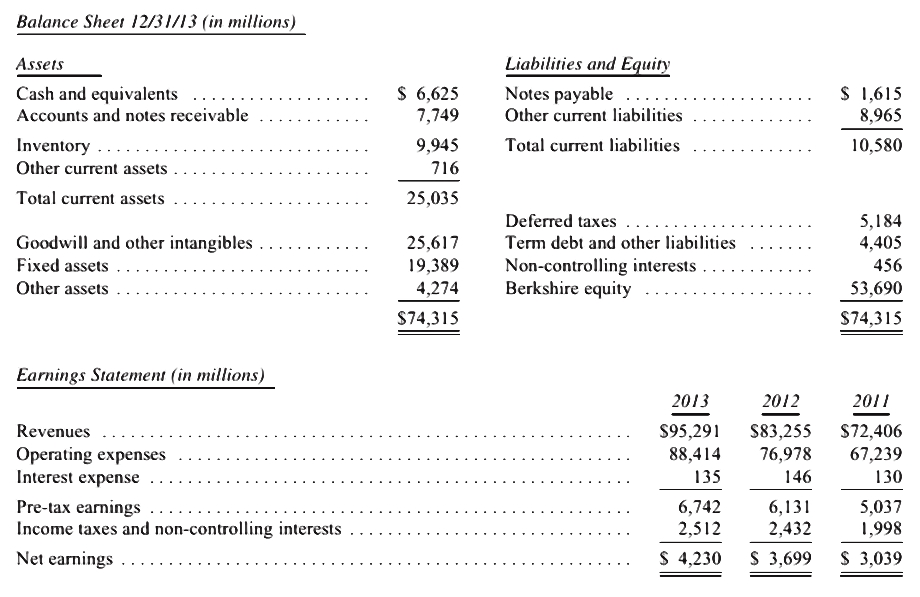

Manufacturing, Service and Retail

These figures are non-GAAP and exclude amortization of intangibles; Warren and Charlie believe this more accurately reflects the expenses and profits of the businesses.

The companies in this group earned 16.7% after tax on $25 bn of net tangible assets.

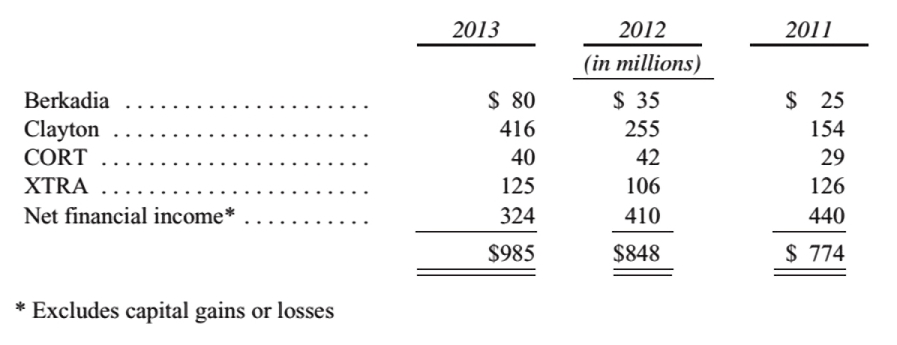

Financials

This is the smallest section of the BH breakdown, and includes rentals of trailers (XTRA) and furniture (CORT) plus Clayton Homes – the US’s largest home builder – and it’s $13.6bn mortgage portfolio.

Investments

This table excludes an option to buy 700M shares of Bank of America before September 2021 for $5 bn. At year-end 2013 these shares were worth $10.9bn. Warren plans to buy the shares just before the expiration of the option.

Warren also noted an unsuccessful investment in bonds from Energy Future Holdings (EFH). Bought for $2 bn, this was sold for $259M with EFH on the verge of bankruptcy. After allowing for $837M in interest, the pre-tax loss to BH was $873M.

Thoughts on investing

- You don’t need to be an expert in order to achieve satisfactory investment returns.

- But if you aren’t, you must recognize your limitations.

- Focus on the future productivity (earnings) of the asset you are considering.

- No one has the ability to evaluate every investment – you only need to understand the ones you buy

- The fact that an asset has appreciated in the recent past is never a reason to buy it.

- Forming macro opinions or listening to predictions of others is a waste of time and may blur your vision of the facts that are truly important.

- Tumbling markets can be helpful to the true investor if he has cash available when prices get far out of line with values.

For the non-professional, Warren has some other rules:

- use a low-cost S&P 500 index fund

- accumulate shares over a long-period

- never sell when the news is bad and stocks are well off their highs

- diversify

When Charlie and I buy stocks … we first have to decide whether we can sensibly estimate an earnings range for five years out, or more. If the answer is yes, we will buy the stock … if it sells at a reasonable price in relation to the bottom boundary of our estimate.

Cash will be delivered to a trustee for my wife’s benefit. My advice to the trustee could not be more simple: put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund.

Some more quotes to end with

It’s better to have a partial interest in the Hope diamond than to own all of a rhinestone.

The advantage of being bi-sexual is that it doubles your chances for a date on Saturday night. (Woody Allen)

When Wall Streeters tout EBITDA as a valuation guide, button your wallet.

Keep things simple and don’t swing for the fences.

When promised quick profits, respond with a quick “no.”

Games are won by players who focus on the playing field – not by those whose eyes are glued to the scoreboard.

If you can enjoy Saturdays and Sundays without looking at stock prices, give it a try on weekdays.

A climate of fear is your friend when investing; a euphoric world is your enemy.

A bull market is like sex. It feels best just before it ends. (Barton Biggs)

Price is what you pay, value is what you get. (Ben Graham)

Conclusions for BH

There isn’t too much to add to what Warren said in the 2014 letter:

- BH will make share repurchases whenever the BH stock price falls to 120% of book value

- BH will out-perform the S&P 500 in normal years, but not in good years for the S&P 500 (> 15% gains)

- BH will operate with at least $20 bn of spare cash and no material short-term obligations

Conclusions for the Private Investor

I was surprised by the amount of overlap between the 2014 and 2013 letters, but there are a few new suggestions:

- Recognise your limitations.

- Focus on the future productivity (earnings) of the asset you are considering.

- The fact that an asset has appreciated in the recent past is never a reason to buy it.

- Macro doesn’t matter and may distract you.

- Accumulate shares over a long-period.

- Never sell when stocks are well off their highs.

Until next time.

This post is one of a series on the Warren Buffet Annual Letters. To read the other summaries, go to the Warren Buffet Quotes and Annual Letters page.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.