Weekly Roundup, 10th September 2015

We begin today’s weekly roundup in the FT, with the Chart That Tells a Story.

Contents

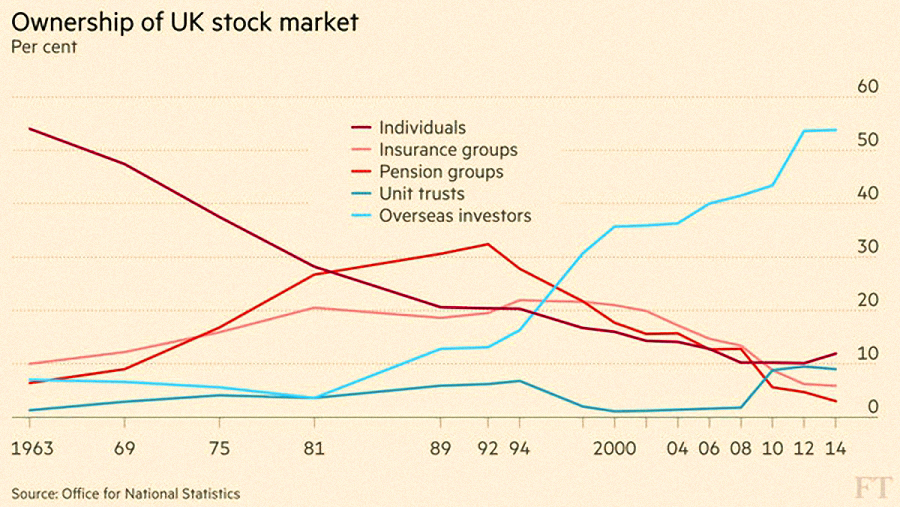

Adam Palin took a look at share ownership in the UK, using data from the ONS (Office for National Statistics).

By 2014 more than 50% of shares were owned by foreigners, compared with only 4% in 1981. This higher than the US market (16%) and Japan (32%).

The London figure partly reflects the composition of the UK market – much of the FTSE-100 market cap is made up of international mining and resources companies.

Many former third-world economies are now rich enough for their citizens to own foreign shares, and electronic trading has made access to these more straightforward.

The other key trend has been in the opposite direction: UK private investors now own 12% of UK stocks. This is up from the 8% low between 2008 and 2012, but a big drop from the 54% holding in 1963.

Some of this will be down to the ease with which overseas markets can be accessed – both directly and through ETFs and funds within ISAs and SIPPs – but changing attitudes to the “riskiness” of shares and the ease of tax-sheltering cash (in an ISA) are also factors.

UK insurance and pension groups now hold less than 10% of the market, down from 52% in 1992. After the 2000 and 2008 crashes, they replaced equities with bonds.

Unit trusts hold 9% of the UK market, up from 2% in 2008.

Value investing

Merryn wrote about value investing and its relationship to behavioural economics.

Richard Thaler, who invented behavioural finance 40 years ago, is now the president of the American Economic Association.

Until then, economic actors – people – were assumed to be rational and always acting in their own best interests. ((I try to stick to this methodology for myself, but a quick look around tells me I am in the minority here ))

Now we know better – people are irrational (often predictably so) and biased and make bad decisions.

[amazon text=Amazon&asin=1846144035&template=thumbnail]

Thaler has a memoir out – called Misbehaving, The Making of Behavioural Economics. Merryn recommends the book and recently interviewed Thaler on the subject of value investing.

Value investing – buying cheap stocks, since they will do better than expensive ones – dates back to Ben Graham and The Intelligent Investor in 1949.

[amazon text=Amazon&asin=0060555661&template=thumbnail]

He demonstrated that low PE stocks in the Dow Jones outperformed by more than a factor of 2 from 1937 to 1969.

Follow-up work by James P. O’Shaughnessy in What Works on Wall Street showed outperformance by a factor of 10 over the 52 years to 2003.

[amazon text=Amazon&asin=0071625763&template=thumbnail]

Even better measures than PE include price to book, which outperformed by a factor of 27.

According to the efficient markets hypothesis, the outperformance is because cheap stocks are riskier and might go bust. People want more reward from taking on this risk.

This is not true. Thaler demonstrates that value investing is no more risky than growth investing. Nor is investing in small companies, which also out-perform.

It’s all to do with most people being irrational and refusing to buy stocks they have stereotyped as “bad”.

Inflation risk

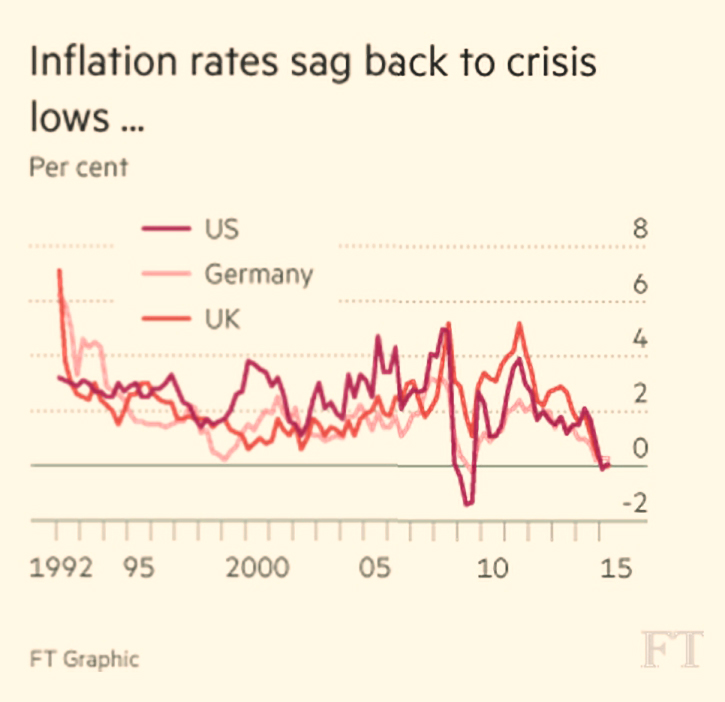

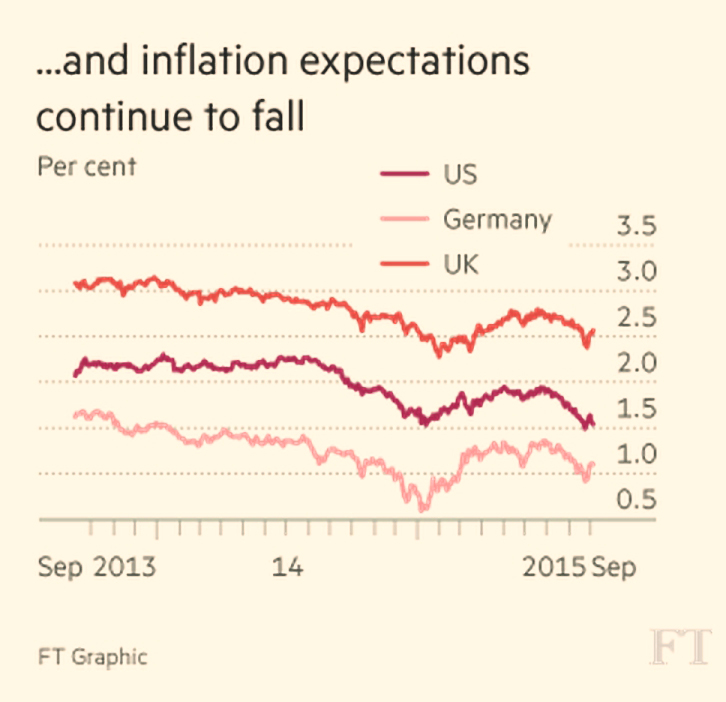

Robin Wigglesworth looked at whether reports of the death of inflation were premature.

The slide in commodity prices and the devaluation of the renminbi have the effect of exporting deflation to western economies, adding to the effects of the 2008 crisis and the Euro woes.

“Breakeven” rates, which measure inflation expectations by comparing normal and inflation-linked government debt are back where they were in 2008.

The German 2-yr breakeven is negative, and the US 2-yr breakeven is close to zero. Ten-year breakevens are 1.5% for the US, 2.4% for the UK and 0.9% for Germany.

More complicated “five year, five year inflation forwards” – the 5-year average rate starting in 5-yrs time, as implied by derivatives – have fallen to 2% for the US and 1.6% for Europe.

Inflation has been falling for decades. The US average for the 70s was 7.1%. This fell to 5.6% in the 80s and 3% in the 90s. It was 2.6% in the noughties and has been just 1.8% over the past five years.

The consensus is that we have this inflation thing licked. People think that it won’t reappear, and even if it does we know how to handle it. That makes me a little nervous. – Michael Arone, chief strategist at State Street Global Advisors

Money can buy you happiness

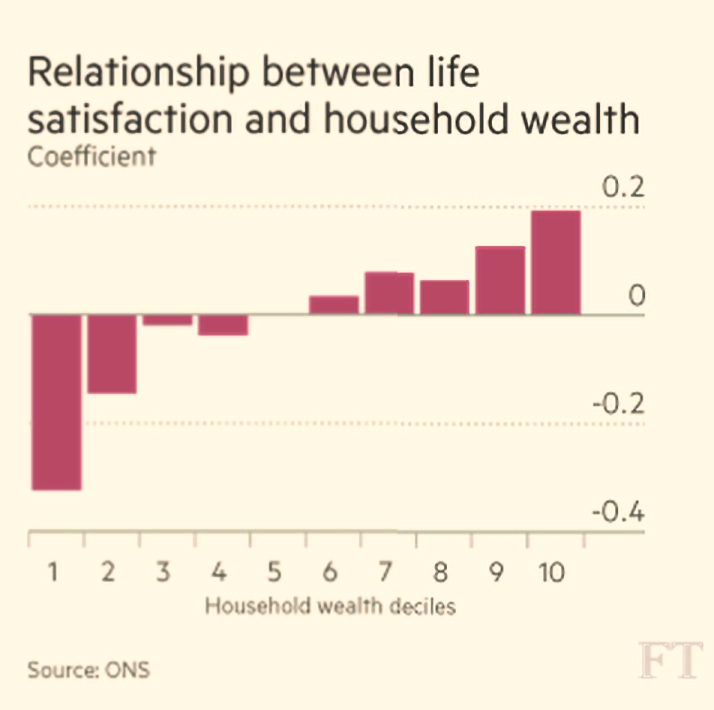

The ONS has also decided that money can buy you happiness, Emily Cadman reported.

“Life satisfaction, sense of worth and happiness are higher, and anxiety less, as the level of household wealth increases,” they said in a paper last week.

- Financial net worth was the number which had the effect.

- There was no correlation with property or pensions, just with the bottom line.

- SWAG (cars, stamps, antiques, yachts) also had no impact.

- The effect of income was much weaker than that of wealth.

The ONS asked people to score themselves from 1 to 10 on a range of questions. The analysis controlled for gender and ethnicity.

The FT also noted that economists Betsey Stevenson and Justin Wolfers had failed to find evidence for the idea comparisons with those around you were what matters for well-being.

There is no “keeping up with the Joneses” effect, and no “satiation point”, at which income and well being are no longer related.

Previous studies ((US-based if I remember correctly )) had found evidence that the first £50K of income was crucial, as was the wealth of those around you (we hate to have richer neighbours or friends).

They did however find that countries which grew quickly became happy more quickly.

Will the Fed raise rates?

John Authers looked at the chances of a first interest rate hike in nine years from the Fed in September.

The Fed has historically been data-driven, and it now has all the data it needs to make a decision.

But that doesn’t mean it will be easy. Employment data is encouraging, but market fragility is not.

The US has added 8M jobs in three years, and 5.1% unemployment is the lowest since before Lehmans went bust.

But the employment ratio – the proportion of the population in work – is below 60%, as in the “dark days” of the Carter presidency in the late 70s. It was 5% higher in the 1990s.

The futures market still sees a rate rise as a 1 in 3 shot, which means the good employment data has made no difference.

The market turmoil of the past few weeks means that the Fed is now also market dependent. The importance of the monthly payroll figures has reduced.

John believes that the Fed should “remove the punch bowl before the party gets too wild”. It’s not their job to make sure people make money in the stock market.

It’s true that markets have already recovered significantly, with the US down less than 10% and still looking over-valued.

John suggests that the significance derives from 1998, when Russia defaulted and LongTerm Capital Management went bust.

Credit markets froze and stocks fell 20%. Alan Greenspan cut rates, inflating the dotcom bubble. Perhaps a mistake, but revealing of the Fed’s thought process.

China and the commodities bust won’t affect the US much, but a crisis elsewhere – Brazil, South Africa, emerging markets generally – might have more impact.

There’s also the highly leveraged US shale oil companies to consider.

In the end, John feels that averting a financial crisis would be the only reason worth delaying the rate rise. Which would require another volatile week in the markets.

Emerging markets outlook

The Economist has turned bearish on emerging markets.

When I was a young investor, the main thing about emerging markets (EMs) was that they were growing very quickly, driven by favourable demographics (lots of young people).

During the noughties, the four BRIC markets returned between 294% and 884%, while the S&P 500 and Europe were flat.

But nobody is a fan these days. The Economist begins with Manoj Pradhan of Morgan Stanley, who warned two years ago (in “The Great EM Unwind”) of three headwinds:

- US QE is being unwound by generating higher real rates and a stronger dollar, which hurts EM capital accounts

- China’s leverage is being unwound, taking growth lower, which hurts EM current accounts

- Credit is being unwound, with EM demand likely to suffer

Add to this the plunge in commodity prices.

A new note reassures that this is not 1997, as there are fewer currency pegs and less hot money (the exit of which triggered the crisis).

Mr Pradhan still worries about EM current account deficits. If exchange rates fall, international money may dump local bonds.

And China’s slowdown hurts Asian exporters and EM commodity producers.

Even worse, the growth has gone. An increase in state-directed capitalism has undermined the moves towards Anglo-Saxon governance which made EM stocks such an attractive asset class.

EM return on equity is also falling, so the stocks are currently cheap for a reason.

Non-performing loans are on the way and the some countries have better governance than others. Back Mexico, India and the Philipines over China, Brazil and South Korea.

In lots of ways, the EMs have ceased to be emerging. But will they stall, or go backwards?

Deutsche Bank has a different analysis, based on FX reserves.

After the 1998 crisis, the EMs moved away from hot money and built up FX reserves. China is the best example, but the total increase was $10 trn.

This meant running current account surpluses.

These reserves were used to buy developed country bonds, driving down real bond yields in the west and helping to inflate the subprime boom.

Deutsche thinks reserves are starting to decline. China still has a (smaller) current account surplus, but the oil producers are in trouble.

The euro area surplus won’t offset the EM decline, and demand for government bonds will reduce, which may mean higher yields.

Deutsche have decided to call this “quantitative tightening”.

The US has shale oil, so doesn’t need as much foreign money to fund its deficit. So yields may not rise quickly.

And there is still QE (bond-buying) in Europe and Japan.

But the flows are in the opposite direction now – EM investors have supplied capital to the west and could withdraw it.

Let’s call it anti-globalisation.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.