Weekly Roundup, 14th March 2017

We begin today’s Weekly Roundup in the FT, where John Authers was writing about bias in financial reporting.

Financial reporting bias

It’s a thin Weekly Roundup today, because the media last week was still full of the Budget, which we’ve already covered here.

John Authers looked at a study by Diego Garcia of Colorado University called “The Kinks of Financial Journalism“.

- Garcia looked at articles in the New York Times and Wall Street Journal from 1905 to 2005

- He marked their choice of words against a positivity / negativity scale.

- And he correlated this mood against the previous day’s move in the Dow Jones Industrial average.

Not that surprisingly, journalists were more negative about market falls than they were positive about market rises.

- The key difference was that after a rise of around 1%, larger increases in the index made little difference to the language.

- But after a 1% loss, bigger losses led to even more negative language being used.

There was also a difference over time:

- The positive effects of an up day lasted only for a single day

- The negative effects of a down day lasted for four days

There were no differences between individual journalists – they all showed the same bias.

Following Robert Shiller’s lead, John thinks that the dot com boom of the late 1990s may have been an exception to this rule, a time when “irrational exuberance” was really present.

Garcia offers two explanations for what he calls the “kink”:

- journalists are demand-led, telling investors what they want to hear, or

- they are supply led, using “hype” to sell papers

John focuses on loss aversion – our greater emotional reaction to a loss than to an equal profit.

- I think this could be used to support either of Garcia’s explanations

But John is really talking about “loss aversion by proxy” – journalists are more worried about encouraging readers to buy (with the risk of future loss) than of urging readers to be overly cautious (losing out on gains, but protecting against losses).

- From his own experience, he feels that his excessive bearishness of the last eight years is less important than his correct bearishness before 2008.

- He also feels that journalists have a role as watchdogs, and must remain sceptical.

I think John’s theory may hold some truth, but that doesn’t mean that the behaviour of journalists is correct.

- Since buy and hold (time in the markets) beats market timing, we would be better served by journalists reminding us to stay in the markets than scaring us out of them. (( I would add that many brokers do send reassuring letters to clients after market falls, but mainstream media tends not to reassure ))

- And scepticism is justified in the context of scams, but not of the stock market.

Forestry

In the property section, Tory Kingdon had an article about forestry.

- It’s been the top-performing asset class in the UK over the past three years with returns of 14.7%

- Apparently this beats commercial and residential property, as well as equities and bonds. (( I suspect that this is a somewhat cherry-picked date, since total equity returns over the past three to five years have averaged more than 5% pa ))

Woodland is a real asset that “you can actually enjoy”.

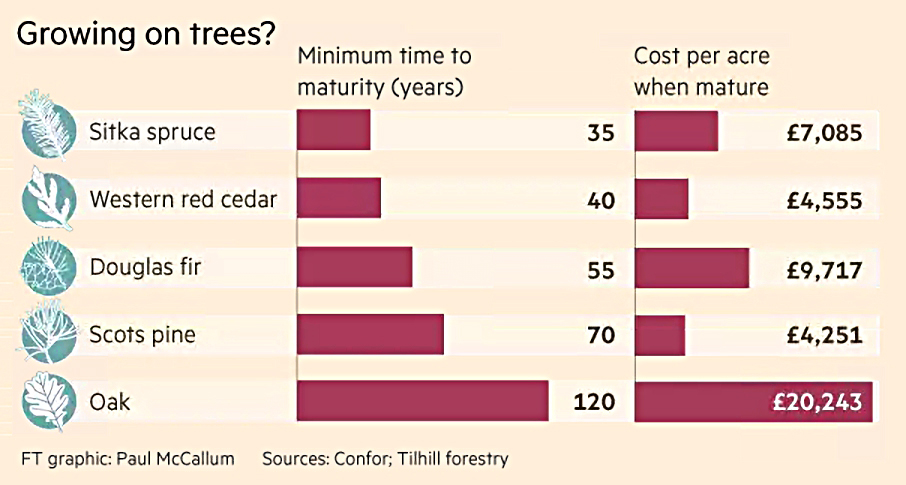

- Most commercial woodland is in Scotland, and is dominated by Sitka spruce, a US conifer.

- This takes 35 to 55 years to mature, compared to 70 years for Scots pine.

- Many owners also hunt on their land.

Location – or rather, distance to the nearest sawmill – is important, since haulage costs can reduce proceeds from £30 per tonne to £18.

- From the deals quoted in the article, forest seems to cost in the region of £1,500 to £3,500 per acre.

- But when mature, it’s worth £7,000 upwards per acre

- Taking the lowest purchase price, that’s a 366% gain over 35 years, or about 4.5% pa compounded.

Woodlands have the same tax benefits as farms (and AIM shares) – after two years they qualify for business property relief, which means no capital gains tax and no IHT.

- For IHT planning, experts recommend young trees, since once they are felled, the sales create taxable cash.

Bubble spotting

The Economist looked at the fragility of booming markets, reasoning that it will be difficult for governments (and Trump in particular) to please both businesses and populists.

- They believe that the recent floatation of loss-making Snap is reminiscent of the dot com boom.

The Shiller CAPE is now close to 30.

- It has only been higher twice – during the internet boom and in 1929.

The paper gives several reasons why investors are ignoring the alarm bells:

- low recent returns – less than 10% from the S&P 500 in 2016, and a loss in 2015

- low holdings of shares – February saw the first net inflows to equity funds for a year

- equities look attractive compared to bonds

- the global economy looks like it might pick up

- Trump has promised tax cuts and infrastructure spending in the US

Of course, Trump’s proposals could get watered down or delayed in congress, and his immigration and trade plans could harm growth.

- And the bull market is now eight years old.

- And the Fed is likely to raise rates again this month.

More importantly, elections in Holland, France and Germany could see large populist votes.

- Workers want a bigger slice of the pie, but it’s hard for both profits and wages to rise faster than GDP.

- And the populists are anti-globalisation, and hence anti-free trade.

Something has to give.

In MoneyWeek, Andrew Van Sickle looked at the same topic.

- The S&P 500 bull market is the second-longest already, with gains of 250%.

- A few mega stocks are now driving the market.

He quotes John Authers saying that it feels like we’ve reached the final phase of the market, but not the end of it.

- More 1997 or 1998 than 1999.

There could still be “a final euphoric phase as the last doubters are sucked in”.

But long-term investors should avoid the market since the high valuations imply dismal returns from here.

Secular stagnation

The Economist also had an article about secular stagnation – the idea that growth will never return.

- With a third consecutive year of growth in prospect, is it time to retire the theory?

Secular stagnation breaks the normal relationship between savings and investment.

- Savings need to be reinvested to avoid recession.

- Central banks control this process by setting interest rates to make sure savings are used up.

Under secular stagnation, the gap between savings and investment becomes too big to control with interest rates.

- Interest rates fall to zero, or even go negative.

- This leads to low growth, low inflation and continued low interest rates.

Though there are now signs of growth, the newspaper worries over negative trends like an ageing population and the concentration of wealth in those groups least likely to spend (the old and rich).

This can lead to temporary punctures of the stagnation by bubbles of financial excess, driven by borrowing.

- A good example was the dot com boom in the late 1990s.

After the 2000 crash, the economy slumped until the property boom – again built on credit.

Reduced borrowing capacity and credit reforms mean that things are a bit different this time, but the Economist fears this might delay rather than prevent a repeat.

- US debt is rising, driven by student and car loans.

- Across the developed world, debt is higher than in 2007, and still rising.

Ways out of stagnation include breakthroughs in technology, or possibly wealth redistribution.

- Public investment (infrastructure spending) would also help.

We await with interest the reaction of the US economy to likely interest rate rises from the Fed.

- If recovery is choked, government action will be required.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.