Weekly Roundup, 7th March 2017

We begin today’s Weekly Roundup in the FT, with the Chart That Tells A Story. This week it was about the entry costs for first-time buyers.

Contents

Entry level property prices

James Pickford looked at what the ONS calls “entry-level property prices“.

- This appears to be simply the 25th percentile of all property sales.

The chart below compares the average price paid by first-timer buyers in the various regions of the UK with the price of an entry-level property in this locations.

- First-time buyers are paying a bit more than they need to get on the property ladder (though they could hardly pay less).

- In London, first-timers spent £423K against the entry-level price of £315K.

I’m not sure what to make of the chart, since the people for whom property is a big issue won’t appear in the data.

- These are the wannabe first-time buyers who can’t save a big enough deposit or borrow enough from a mortgage lender.

The ONS has also released a property affordability tool.

- This shows the property data at postcode level, the local average income, and the income and (15%) deposit needed to buy an entry-level home.

- London comes out worst, as you might expect, particularly the up-and-coming areas where the average income hasn’t yet caught up with the average selling price.

You can tweak the inputs on the model, but the somewhat depressing defaults are “not untypical”.

Probate fee increases

Hugo Greenhalgh reported on massive increases to probate fees:

- Above £500K in estate value, the fee will increase from £215 to £4,000.

- For estates above £2M, the fee rises to £20,000.

- That’s not a typo, it’s an increase by a factor of 100.

The fees were proposed back in February 2015, but despite a 98% negative response to the consultation, the government has decided to proceed.

- Fees of this level bear no relation to the work involved and are simply naked revenue raising.

Taxes are supposed to encourage good behaviour and discourage bad behaviour.

- Are we saying that getting rich is a bad thing, or simply that dying is?

LISA vs pensions

Josephine Cumbo looked at the arrival of the Lifetime ISA (LISA) in April, and at the implications for pensions.

- The LISA is available only to the under-40s, and can be used as the deposit on a property, or withdrawn tax-free after age 60.

- Like an ISA it is funded from post-tax income (up to £4K pa) but like a pension the government adds a 25% bonus (equivalent to the rebate of 20% income tax).

- This bonus is clawed back if money is withdrawn (other than for a property purchase) before age 60.

So unless you are buying a house, the LISA is worse than a pension for higher-rate taxpayers, and the same (but with a much lower annual contribution limit, and a higher age qualification of 60 vs 55) for basic rate taxpayers.

Millennials clearly aren’t keen on pensions, and the LISA is likely to appeal to them more (since you can get your money out for a house purchase, or via the penalty route).

Unfortunately, lots of millennials have just taken out a workplace pension under the auto-enrolment scheme.

- The worry is that LISAs will be funded with money that should go into more attractive workplace pensions (which attract matching contributions from employers).

- Workplace pensions also have fee caps of 0.75% pa.

Added to this, the under-pensioned self-employed will be largely excluded from LISAs as they are mostly over 40 years of age.

Josephine also worries that the LISA is a stalking horse for the abolition of higher-rate tax relief on pension contributions.

- Extending the qualification age to 50 and the contribution age to 60 (as well as increasing the annual contribution limit) would make the LISA a clear challenger to pensions, but with only 20% tax-relief available.

Overvalued dollar

John Authers began with the new record levels in the S&P 500 and the Dow Industrials indices (2,400 and 21,000 respectively), but cautioned that 10-year Treasury yields were only 2.5%.

- This is below the 3% level they hit three years ago, suggesting a lack of optimism over growth.

But for John, the biggest obstacle is the overvalued dollar.

- A strong dollar makes US exports expensive, and imports cheap.

In the FX markets, money tends to flow to the highest yields.

- The carry trade involves selling low-yield currencies (or borrowing in them) to buy high-yield currencies.

- This pushes down the value of the low-yield currency, and pushes up the value of the high-yield currency, so for a while the carry trade is self-supporting.

The carry trade was traditionally between the flat-lining Yen and the booming commodities currencies (Brazil and Australia at the time).

- But now there are large gaps between US yields and European ones.

- 1.95% against Bunds, and a record 1.25% more than Gilts

The Fed is positioning for another rise in March (next week) which will only make the gaps bigger.

- And Trump plans extra spending on defence and infrastructure, plus tax cuts and tariffs against imports.

The chart shows the trade-weighted dollar index after accounting for inflation.

- It’s clear that there is room for the dollar to rise further, perhaps by 25%, but more likely by 10%.

This should help European and Japanese exports, and hence their stock markets.

- It will hurt emerging markets, which have dollar-denominated debts.

- And it should cap US growth and end the stock-market rally.

If the Fed raises rates another three or four times, and 10-year yields hit 3% or even 4%, this could happen too quickly for comfort.

In a second article, John looked at whether Trump’s well-received speech to Congress last week was helping to fuel the stock market rally.

- He concluded that it was not.

Instead, he put it down to the increasing likelihood that the Fed will raise rates in March, and to positive monthly survey data from supply managers on inventories and orders.

- Inflation is now close to the Fed target of 2% pa, and Europe, Japan and China are recovering.

The general consensus is that the deflation scare of 2016 is now over.

- This “reflation trade” should drive stocks, metals and bond yields higher.

- John sees the “Trump trade” as a subset of this reflation trade.

The cynical take on US politics is that either Trump delivers tax cuts (good for the markets) or there is gridlock (historically good for markets).

- It’s a “win-win”, of sorts – unless bond yields go up too much.

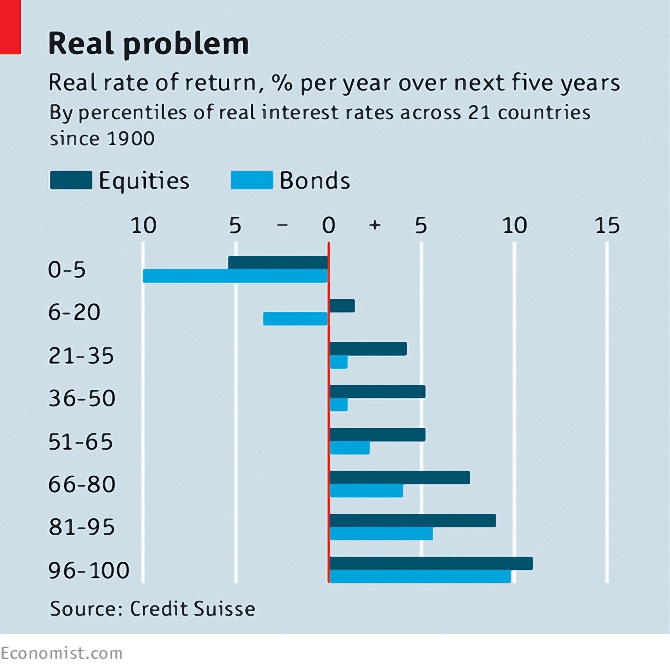

Investment returns

In the Economist, Buttonwood looked at the fall in prospective investment returns.

Dimson, Marsh and Staunton (Cambridge / LBS) looked at how real interest rates affect future real investment returns.

- Low real (after-inflation) interest rates generally lead to low returns.

- So the current buoyancy of markets is something of a puzzle.

Low real interest rates are associated with bad economic times, and therefore low corporate profits.

- But they also lower the cost of capital

- This should boost investment, and therefore profits.

in fact, since the 2008 crisis, investment growth has only averaged 1.5% pa, compared to 3% pa in the 40 years before the crisis.

Although there are problems is borrowing from banks keen to rebuild their balance sheets, a bigger factor could be the 12% pa return that companies still use as a “hurdle rate” for proposed projects.

- Since their cost of investment has fallen by around 5% pa, so should have their required returns

Another cause for concern is US pension funds, which (as we have discussed previously) are allowed to choose their own future rate of return.

- Buttonwood finds their continued prediction of 7+% pa returns surprising.

- I think they’re just choosing a rate that allows them to balance their books.

Currency manipulation

The Economist also looked at whether China is a currency cheat.

- The answer is yes, but not in the direction that the US means.

The US Treasury uses three indicators of manipulation:

- a big trade surplus with the US

- a current account surplus of more than 3% of GDP

- spending more than 2% of GDP to buy foreign assets (and thus suppress its own currency)

China has only the trade surplus (and indeed, no country currently meets all three criteria).

The newspaper came up with a scoring system from the criteria:

- one point for each 3% of current account surplus

- one for each 2% of foreign asset purchases

Trade surplus against the US was ignored because countries like Mexico have large surpluses with the US, but deficits with the rest of the world.

South Korea and Taiwan outscore China, and Switzerland scores highest of all.

- Yet the Swiss franc is one of the world’s most overvalued currencies (in PPP terms).

- This means that the scoring system is not that good.

China’s score is currently negative, implying that it is trying to push its currency higher.

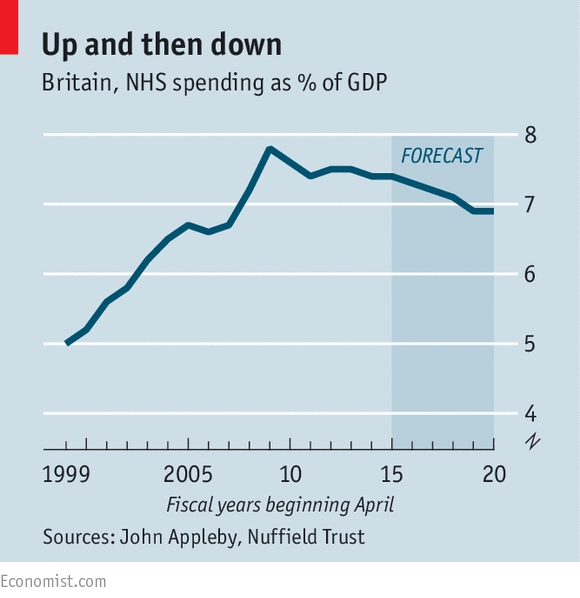

NHS spending

The Economist also looked at NHS spending.

- The newspapers are full of stories about a crisis in NHS funding and in social care (for the elderly, mostly).

Demand is rising, partly due to unfavourable demographics.

- Occupancy rates in many hospitals are close to 100%.

- Only 86% of emergency patients are seen within the four hour target for A&E.

Labour pushed NHS spending up from 5% of GDP to 8%.

- Seven years of “austerity” have knocked only half a percent off that, though 7% is forecast by 2020.

Deficits at NHS trusts now total £2.5 bn.

There’s been a lot of speculation in the run-up to this week’s Budget.

- Some say there will be a social insurance levy (similar to NICs).

- Others expect a new tax on inherited wealth (which would be strange when the primary residence exemption – admittedly George Osborne’s idea, not Philip Hammond’s – is due to come into force in April)

Alternatives to more cash include the integration of health and social care at a local level, and more emphasis on prevention.

I guess we’ll find out tomorrow.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

Hi Mike,

“Are we saying that getting rich is a bad thing, or simply that dying is?”

The probate ‘tax’ rate is about 1%, so I don’t think that’s going to have much impact on most people’s aspirations. However, I do agree that it’s an underhand stealth tax. Personally I’d much rather see IHT cancelled and all inheritance taxed as income, but that’s unlikely to happen.

1% too much for me – the money has already been taxed on the way in. IHT is an abomination.

Probate fees should match the worked involved – the existing system (£200) was fine.

You ducked the question about whether getting rich is now a bad thing. We need to fix society from the bottom up, not the top down.