Weekly Roundup, 16th May 2017

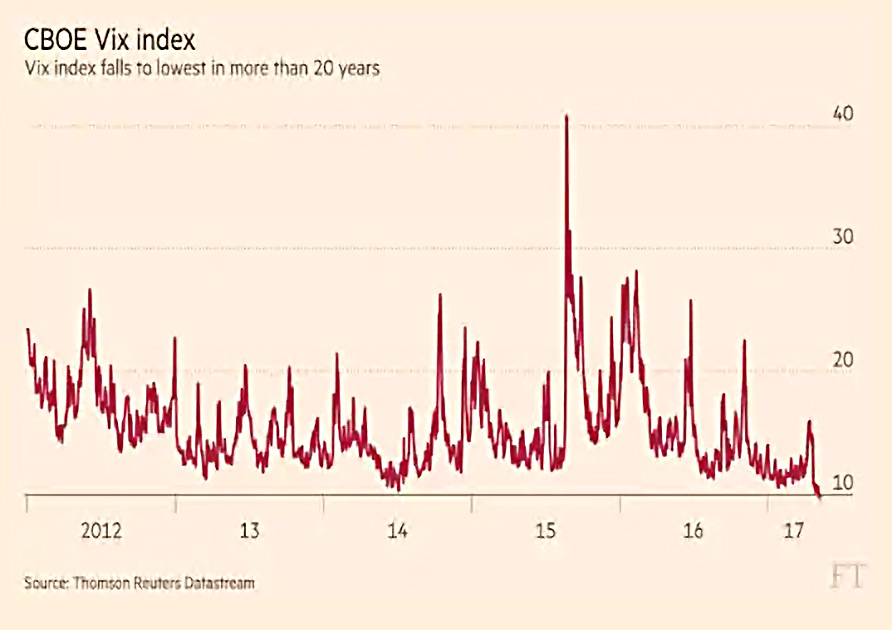

We begin today’s Weekly Roundup in the FT, with the Chart That Tells A Story. This week it was about the Vix.

Contents

Fear gauge

Robin Wrigglesworth asked whether investors should be worried that the “fear gauge” – the Vix, a measure of volatility on the CBOE (Chicago Board Option Exchange) – is so low?

- It’s a reasonable question, given that the Vix has been hitting 20-year lows.

The Vix is calculated from the prices of options that mature in the next month.

- A score of 20 (the long-run average) implies stock price fluctuations to average 1% a day (that’s 74 points on the FTSE-100 as I write).

This week the Vix fell below 10, it’s lowest level since 1993.

- Observers put this down to Macron’s victory in the French election.

- The low Vix level is also yet more evidence that markets have adjusted to a Trump White House.

Europe’s equivalent index (Vstoxx) is also low, though not so low as the Vix.

- Real volatility in the European market is near its lows since 1990, however.

Robin says that the implied volatility from the Vix is not particularly useful.

- It’s a lagging indicator rather than a leading one, and not great at picking up very short-term market worries.

Robin also mentions that a trader with the nickname “50 Cent” (since outed as the Ruffer Investment trust) has been buying Vix derivatives that cost 50 cents (hence the nickname).

- These insure against a market downturn (or to be precise, increased volatility).

Robin also highlights the alternative trade of buying Vix futures at the bottom of a crash, betting that volatility will subside.

- Futures bought in March 2009 would be up 4000% (40 times) by now, albeit via a wild ride.

Rich

Also in the FT, Merryn went back to the discussion triggered by Labour’s tax proposals about how much money you need to be rich.

- She remembers from her City days that £10M was the number people used.

- Accounting for house prices and pay rises that’s probably £25M now.

I think most people would say that’s too much.

- £1M to live off and £1M for a London flat is probably as much as anyone can justify.

Merryn walks through the many changes to income tax, pension allowances and IHT thresholds to demonstrate that every chancellor has his own definition of where rich kicks in.

- And that for most of them, the line moves during their tenure.

So we currently have £110K for income, £1M for wealth, and £425K for inheritance.

- Merryn thinks you can stretch the wealth line to £2M, but it’s not clear to me from the tax rules.

On Labour’s proposal, her point is that although only 5% of earners are above the proposed £80K threshold for new taxes, that 5% is in a single year.

- Many workers aspire to be in that band for at least part of their career.

Of course, this is academic, since Labour won’t win the election.

- With a Tory government returned, Merryn expects more taxes on wealth rather than income.

What Merryn would like to see is:

- an end to tapers

- abolition of the LTA

- flat tax relief on pension contributions (in the form of a capped bonus of 25% to 30%)

- replacement of IHT with a gift tax on all capital exchanges

I wonder if any of these will happen.

- They are sensible ideas, but how will they play on social media?

Pensions

Over in the Spectator, Jeff Prestridge had his own wish list for pensions:

- 25% bonus on contributions to £10K pa

- no bonus on further contributions to £40K pa limit

- Axe the LTA

- Close a DB schemes and replace with DC, to put the whole country on the same footing

- Make auto-enrolment compulsory

Another sensible list, though I would not cap the government bonus at such as low level.

Property

Merryn’s column in MoneyWeek covered a survey by Fidelity which found that UK adults still much prefer Buy-to-Let to the stock market.

- And let’s not forget the data from last week showing that 80% of ISAs are in cash.

It seems an impossible task to get Brits to think clearly about money.

Merryn thinks we’ve reached the point where property buyers won’t (or can’t) pay the asking price any more.

- But sellers probably won’t cut their prices, leading to a stand-off, and flat prices for the next few years.

Definitions

Back in the FT, Tim Harford’s column was nominally about how to mislead with statistics, but in practice was mostly concerned with definitions.

He began with the 21% increase in homicides in England and Wales in 2016, which Labour called “worrying”.

- It turns out that 96 of the 100 extra deaths actually happened in 1989, at the Hillsborough disaster.

- When these deaths were re-classified as homicides in 2016, the annual number leapt up.

The crimes database has long been seen as dodgy because of more mundane changes in reporting standards.

The next topic is immigration, and the Tory target to reduce annual net migration to below 100K.

- Since more than 100K people arrive from outside the EU, Brexit won’t solve this problem.

The current approach is to restrict unskilled migration.

- A wage floor of £35K pa has been suggested, but Tim points out that many people who would generally be regarded as skilled currently earn less than this in the UK.

A designated professions list – of jobs where we have shortages – might be a better approach.

Tim’s next target is Labour’s description of NHS funding shortfalls (as defined by the NHS itself) as “Conservative cuts”.

- Since the NHS budget is increasing by £8 bn, they can’t be cuts.

And then we come back to the definition of rich:

- is it £35K, as per the immigration visa salary floor?

- or household net worth of £2.9M (“the 1%”)?

Tim concludes that at least John McDonnell’s definition of rich as earning more than £70K pa – since revised to £80K pa – is clear.

- That doesn’t mean that you have to agree with it.

Crowdfunding secondary market

Aime Williams reported that crowdfunding website Seedrs is to open up a secondary market in the shares of companies on its platform.

- This is a nice idea in theory, in that it provides liquidity and the prospect of an early exit for initial investors.

But without any tax relief in the secondary market, will this really work?

It’s a similar story with VCT shares.

- They are fully listed, but because there’s no tax advantage to buying shares second-hand liquidity is poor (though you can usually trade a few £K at a reasonable price).

Seedrs will begin with a beta market that opens for one week a month, and only allows existing shareholders in a company to trade.

- And the price will be fixed at the valuation from the last funding round, rather than being set by supply and demand.

So not much of a secondary market, really.

Sports fund predictions

Aime’s second article of the week was about the launch of a sports betting fund.

- The fund, from tech startup Stratagem, will launch this summer and will focus on football, basketball and tennis.

- There will be restrictions on who can invest initially (presumably those who self-certify as high net worth or as sophisticated investors).

Aime says that this will be the second betting fund in the UK.

- The other is run by Priomha out of Guernsey.

- It has a £285K minimum investment, with annual fees of 2.5% and a performance fee of 25%.

Stratagem predictions are made by the company’s software tracking players and balls in real-time.

- If it works – and it’s a big if – we could be looking at the birth of a new asset class.

Crowdsourcing hedge funds

Staying with this territory, the Economist had an article on hedge funds that use a crowdsourcing approach.

- Quant funds use mathematicians and physicists to write algorithms.

- Quantopian (founded in 2011) crowdsources its algorithms.

Few quant firms have more than a few hundred researchers.

- Quantopian has 120K members.

Anyone can learn to build an algorithm on its platform, and the most successful are given money to manage.

- Authors receive a licensing fee of 10% of net profits.

The first allocation of funds (between $100K and $3M each) to a batch of 15 algorithms has just taken place.

- The remaining 120K authors (minus 15) are free to trade their own money on the platform.

A fund open to outside investors is expected later this year.

Fund managers

Elsewhere in the newspaper, Buttonwood expects further consolidation in the fund management industry.

PWC have identified four threats to asset managers:

- returns from investment are low

- revenues are being squeezed

- regulations are being tightened, and

- robots are coming.

As well as robots, passive funds are rapidly taking off.

- Commissions used to encourage active fund recommendations, but these have since been banned.

- The switch from DB to DC pensions has also helped.

Vanguard received more than 50% of global net fund inflows during 2016.

- Fees are as low as 0.04% pa for a Vanguard US tracker, but 20 times more (0.80% pa) for an actively managed fund.

- Average fees (weighted by assets) have fallen from 0.99% in 2000 to 0.68% in2015.

And for those who believe in active out-performance, there are smart beta funds.

So more consolidation seems inevitable.

Good Selfies

In the letters section, Robert Merton and Arun Muralidhar argued for the creation of a safe, low-cost, liquid instrument tailored to retirees.

- They called these SeLFIES (Standard of Living Indexed, Forward-starting, Income-only Securities).

These payout from the retirement age and only until the average life expectancy.

- So UK bonds might pay out for 20 years from age 66, say.

They would be indexed to per-capita consumption consumption rather than inflation.

As the coupons are spent, the government would receive income from VAT, which could be used to fund infrastructure.

It’s an interesting idea, but I want to know more about how such instruments would be priced and traded.

- And how people should fund retirement should they live beyond the national average life expectancy.

Marx

John McDonnell said last week that there was a lot to be learned from reading Marx, and Bagehot agreed with him.

- The bit Bagehot liked was the section on rent-seeking.

To Marx, capitalists “expropriate” other peoples’ work as their own.

- Even I agree with this to a certain extent.

I see nothing wrong with being rewarded for supplying capital.

- So literal rent from property, or returns from investments seem fair to me.

The modern day rent-seekers are managers and executives, who risk little and earn hundreds of times the wages of their workers.

- The average wage ratio in the UK has increased from 25 in 1980 to 130 in 2016.

The private sector earnings of former public sector workers (notably politicians and senior civil servants) is another example.

Marx also predicted the increasing concentration of capitalism, and the rise of reckless finance, even though the technological mechanisms that have driven this would have seemed strange to him.

The real issue is with Marx’s solutions.

- McDonnell is not just a fan of Marx, but also of Lenin, Trotsky, Castro and Chavez.

Cost Disease

The economist William Baumol died last week, and the Economist had an article that summarised his work.

His early work was on entrepreneurs, and how they (and their use of technology) lead to the differences between rich and poor countries.

- Thus the incentives faced by these “crafty strivers” would determine whether they became career bureaucrats or founded Microsoft.

His second area of expertise was contestable markets, which work well despite having fewer entrants than might be expected.

- This helped to distinguish when oligopoly was efficient, and when it was not.

His key contribution was cost disease, which originated from the study of arts organisations.

- As manufacturing productivity increases, so arts organisations must pay more to retain their staff. (( I have some issues with this myself – many arts workers here in the UK have private means, or would work for subsistence wages ))

- Since arts productivity is difficult to increase, either ticket prices or donations must increase (or less art must be produced).

The same analysis often applies to health care, education and government.

- So the cost of public services will generally increase as GDP and productivity grow.

Of course, technology can improve productivity in these areas too, and indeed there are promising signs in healthcare and education.

- The key point is the reverse.

Artificial percentage caps on the share of the economy devoted to say healthcare – a hot topic in the UK today – are likely to be counter-productive.

- Of course, healthcare is a special case, since the majority of the costs are likely to come from the less productive members of society.

- It’s easier to make the case for a larger spend on education.

At the limit, all productivity growth could come from automation, with “stagnant” industries providing full human employment.

Fully costed

On his Stumbling and Mumbling blog, Chris Dillow argues that “fully costed” spending plans from the parties in the election are nonsense.

- Government borrowing is the counterpart of private sector saving, and not directly in the government’s control.

But alternatives exist – higher taxes or reduced spending (each of which seems a valid option to me).

Chris points out that the Tories have overspent by £107 bn (compared to forecasts) in the last five years, yet bond yields have fallen.

Chris wants to see more Keynesian spending to boost the economy before we try to balance the books.

- But we aren’t in a recession, inflation is increasing and we might be near full employment.

- On the other hand, interest rates remain at record lows (and therefore borrowing is cheap).

I suppose it all really depends what we spend it on (infrastructure and education possibly good, bureaucracy and higher welfare rates likely not so good).

On his blog Mainly Macro, Simon Wren-Lewis disagreed with Chris about plans in aggregate, but agreed that individual proposals that cost money need not be matched with a corresponding cost-saving measure.

- We don’t have hypothecation in the UK, apart from during elections.

Simon suggests that budgets should be balanced at departmental level, rather than proposal level.

- This would leave the Chancellor to explain the allocations to each department, and to defend the planned level of borrowing.

- They should also be asked what they will do if / when the deficit turns out to be different.

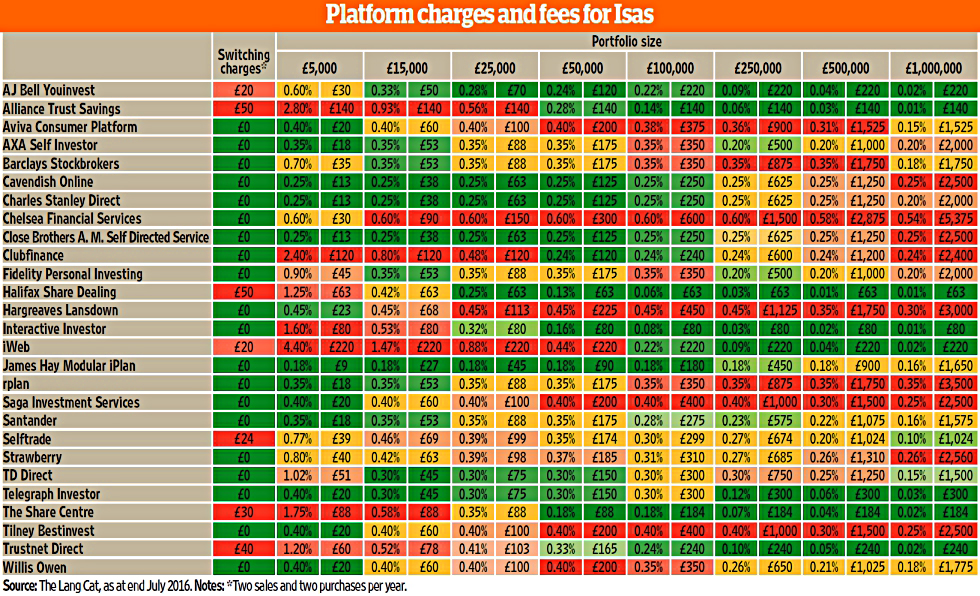

ISA charges

And finally, here’s a chart I came across this week on Reddit.

- I think I’ve posted it before, but it’s worth looking at again.

It’s from the team at the LangCat, and shows ISA charges from many providers and across a range of portfolio sizes.

- It’s not perfect, since it assumes a fixed level of annual account activity, but that’s really a limitation of 2D charts.

What I like about it is the colour coding.

- Whatever size of ISA you have, you can run your eye down a column to work out which providers are worth investigating.

- Over on the right side of the table, I can see that firms I use like iWeb an AJ Bell are competitive.

Most UK investors look at the Monevator charges page, which is pretty comprehensive.

- And of course, the Monevator team are doing heroic work collating the data – it’s not a task I envy.

- But the chart is a lot easier to digest.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

Hi Mike,

Thanks as always for sharing, couple of things that stand out to me (ignoring tax changes of course!)

1. What is Rich. Such an emotive subject! £1M in assets would generate between £30k and £40k a year – I personally wouldn’t call that rich, even with a paid off mortgage, however I know some who are only earning £25k per year would see it that way. I won’t declare my number 😉

2. ISA Charges. Thanks for sharing the simple graph, an interesting read. One thing I have found is it is such a difficult one given individual circumstances are so varied – with TD Direct with my mix of investments and trading levels I am paying less than 0.1% a year in fees, but I am enjoying seeing all the costs coming down over time

Cheers,

FiL

I think £1M and a house / flat is comfortable, but not rich. People tend to focus on income, though.

I’ve just done a comparison of platform costs as part of a post on Robo Advisors (in the wake of the Vanguard announcement this week). You can find it here: Vanguard and comparators

It’s “easy” to keep your costs low if you are totally passive and never trade, but few people can do that for 50 years.

Hi Mike,

I am with you – comfortable, very much so, but not rich.

Yes, I haven’t had a chance to read through the comparisons yet, its on my weekend reading list, but I know I can keep my fees very low as I try not to trade too often, even in my actively managed portfolio.

I find the biggest challenge is around the %age charges that get applied

Cheers