Weekly Roundup, 23rd November 2020

We begin today’s Weekly Roundup with John Redwood in the FT.

Biden’s win

John Redwood’s ETF portfolio is overweight the US at the expense of the UK, Europe and Emerging markets.

- Because of this, he’s up 6% YTD.

In this month’s FT article he looked at the likely impact of President Biden on the markets.

Mr Biden wants the US to rejoin the world orthodoxies, be a good member of global bodies, embrace the green revolution and follow the mantra of lock downs.

As a Biden win became more likely, lockdown tech stocks rallied, despite the threat of regulation.

- Then when the vaccines were announced, the anti-lockdown stocks (travel, entertainment and even oil).

John expects a tougher Biden response to the virus, but an ongoing challenge in getting the two Americas (his and Trump’s) to coexist happily.

- Added to this will be more support for the green and digital revolutions, and more monetary stimulus.

I have switched some of the technology investment into more general world shares, and trimmed the successful US-led digital revolution investments. The fund also has a position in index-linked bonds in case in due course the world decides to inflate its way out of debt.

John also has theme fund exposures to clean energy, battery technology, robotics and cyber technology.

Currency trading

Joachim Klement reported on a new study which shows that central banks have effectively killed currency trading.

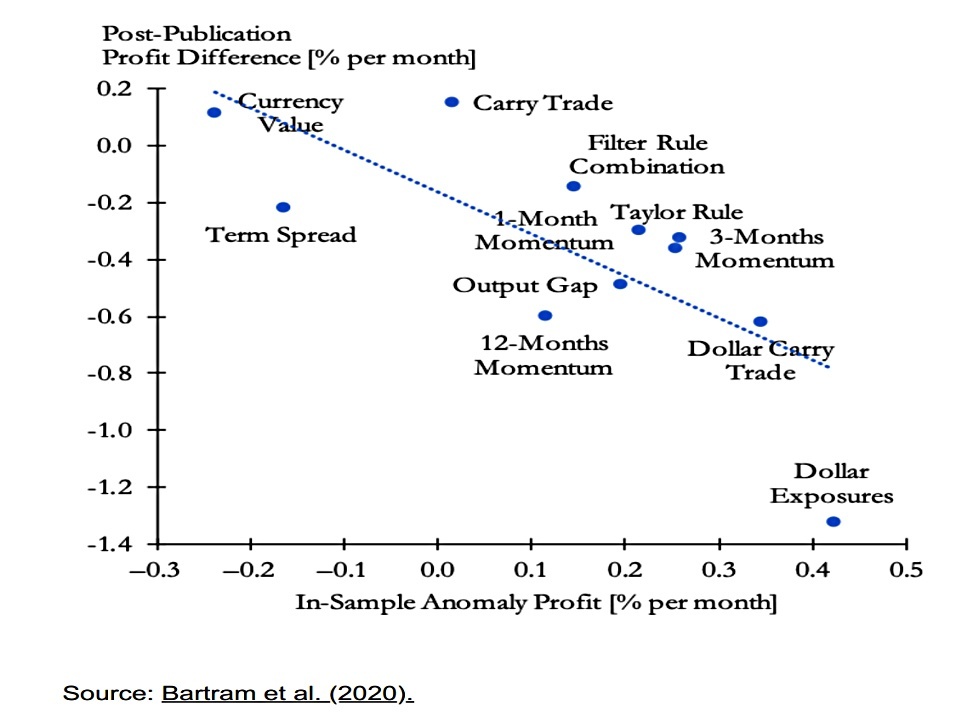

The most popular anomalies (aka factors) that are traded in the currency markets are the carry trade (buying currencies with high interest rates and selling currencies with low interest rates), momentum trades, and the valuation trade (based on purchasing power parity).

Unfortunately, the profitability of each of these factors – and many more – has declined significantly since they were first reported in the academic literature.

Most factors became loss-makers, and loss-makers became profitable:

Value strategies were losing money in sample (i.e. you should have bet against them according to the academic research), but once that fact was known, so many people started betting against value that the strategy started to work better after publication.

The only factor that continued to work was the carry trade – so long as your pairs didn’t include the dollar.

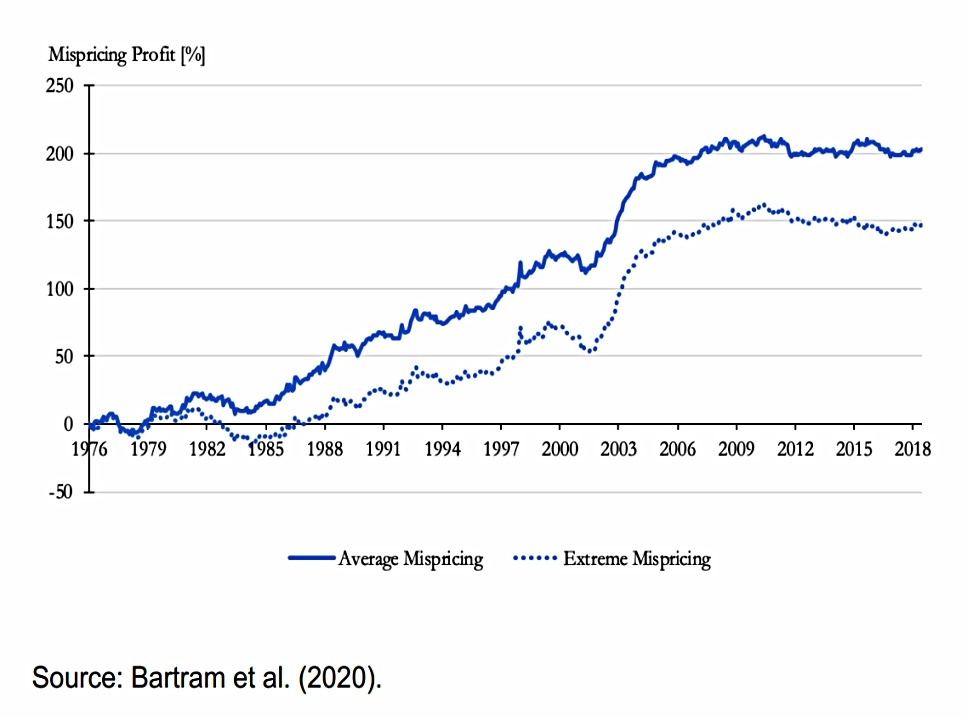

Looking at the factors through time, they were profitable until 2008.

- Which is when central banks lowered interest rates and started QE.

The new policy regime after the financial crisis has made it impossible to make money in currencies in any systematic way.

Joachim speculates that the new regime is also a contributor to the decline in equity factor performance over the last decade.

Investment trusts

Elsewhere in the FT, Madison Derbyshire plugged a few investment trusts for the way they have handled the pandemic.

- But it’s been a turbulent year, as evidenced by the fluctuating average discount to net asset values.

After a decade of contraction to a historic low of 1.3%, the gap jumped to 12% in April (flirting briefly with more than 20% in March), before shrinking back to 7% by October.

- That sounds bad, but in 2008 many trusts went to a 30% discount, and the average hit 18%

Madison stressed the use of reserves by ITs in order to support dividends:

The capacity of trusts to maintain or even increase payouts to investors when many listed companies were cutting or axing them has shone a spotlight on the trust business model, and driven a resurgence in popularity with investors.

Some 58 per cent of the 124 trusts that have reported so far this year have increased payouts, according to the AIC, and a further 23 per cent have held them.

We’ve covered the many advantages of ITs on several occasions, but with the rise in popularity of low-cost ETFs, two stand out today:

- Suitability of the closed-end structure for illiquid assets (eg. property, VC, private equity)

- Usefulness in accessing esoteric and/or poorly priced markets and asset classes.

I no longer buy ITs in major developed markets, but I still use them for themes and alternatives.

The three trusts showcased by Madison were:

- Baillie Gifford China Growth

- Hipgnosis song royalties fund

- City of London (an income fund)

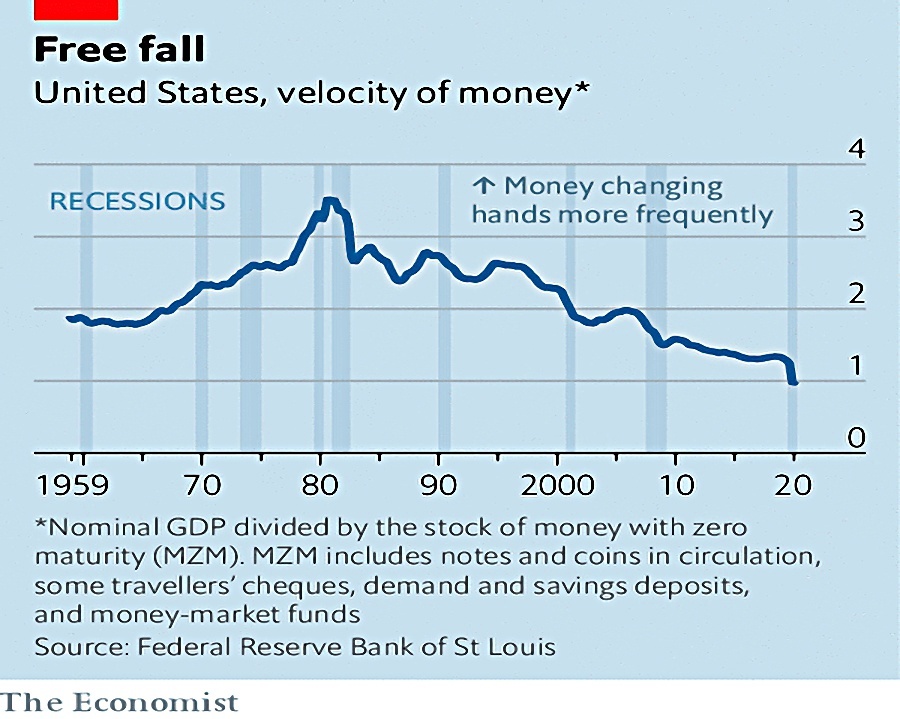

Velocity of money

The Economist explains that the velocity of money has fallen sharply because of economic uncertainty and government handouts.

Money’s “velocity” is calculated by dividing a country’s quarterly GDP by its money stock that quarter.

There are several versions of this number, based on different definitions of money.

Most popular with economists is “money of zero maturity” (MZM), which includes assets redeemable on demand at face value—such as bank deposits and money-market funds.

In 2Q20, MZM went below one – the average dollar was used less than once from April through June.

- In June, the Fed had to ration supplies of coins when they remained stuck in wallets and purses.

In a weakening economy, consumers prefer to save rather than shop; investors cling to the safe assets that make up MZM. Both the Depression and the Great Recession began with sharp declines in velocity.

During the Depression, velocity recovered but after the 2008 crisis, the Dood-Frank act moved money from the shadow-banking system to the regular banking system, and velocity continued to fall.

Personal savings rates are at record levels this year, and the money supply is up by more than 20%.

- Once the pandemic is over, this savings glut could turn into a spending spree, perhaps triggering a repeat of the Roaring Twenties.

It could also lead to inflation, which in turn might finally trigger a rise in interest rates.

Bad year for quants

Last week, we looked at why 2020 has been a bad year for quants, and this week Buttonwood has covered the same topic.

- Vaccine day two weeks ago was the worst day ever for long-short momentum.

Quants rely on history. If something happens that is without precedent, such as a

vaccine in a pandemic, they have a problem.

As in chess, the human strategy differs from that used by algorithms:

Humans retain an edge. They are able to winnow down endless possibilities using mental shortcuts. They can imagine scenarios that the past has not thrown up—scenarios such as “a vaccine may become available soon, given the amount of money and effort being thrown at it”; and “news of such a vaccine might spark a sell-off in ‘stay-at-home’ shares and a rally in ‘get-out-of-the-house’ shares”.

Liquidity is probably to blame:

A speedy trading strategy, such as momentum, relies on liquid markets to keep turnover costs in check. The strategy can become crowded. And when the quants suffer losses, they may be forced by risk-management rules to close their positions. As everyone rushes to get out at the same time, it makes for extreme price movements.

Of course, quant strategies like trend-following are not designed to predict the future – they are designed to react to price.

- And no quant would pretend that the factors work all of the time.

The quant game is all about capturing equity-like returns without the massive drawdowns that equity markets are prone to.

- And trend-following is a long game.

I won’t be abandoning my quant allocation just yet.

- Combining a long-only passive core with active satellites (including quant) leads to lower volatility and a higher Sharpe Ratio.

Quick Links

I have five for you this week, the first three from The Economist:

- They looked at the DoorDash IPO

- And the Airbnb IPO

- And at the stellar quarter enjoyed by Walmart.

- Alpha Architect looked at using Quality to separate good and bad value stocks

- And at an easy way to simplify and improve the predictions from the Shiller CAPE.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.