Weekly Roundup, 21st June 2016

We begin today’s Weekly Roundup in the FT, with the Chart That Tells A Story. This week it was about house prices.

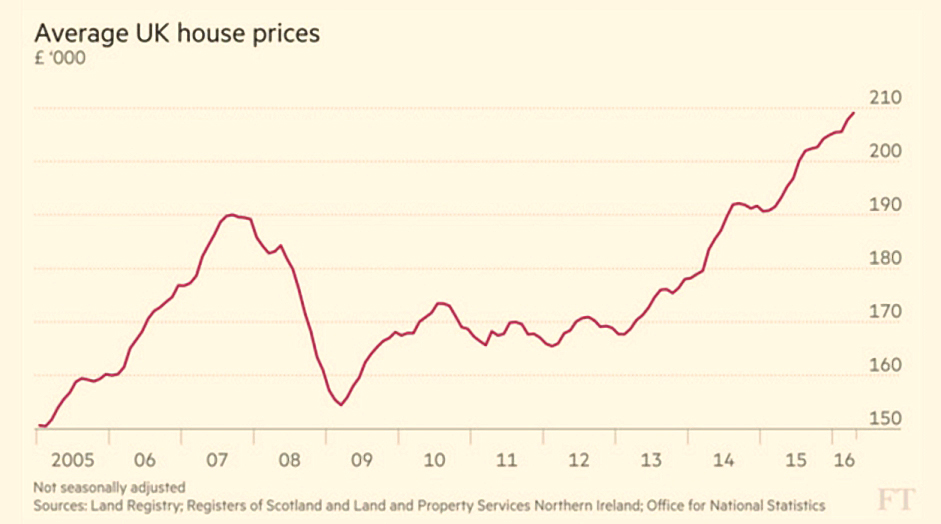

House Prices

Gemma Tetlow looked at a new measure from the ONS using Land Registry data.

- It shows that the average house in the UK is now worth £209K, up £16K or 8.2% over the past year.

- This is also a rise of £55K from the recent low of March 2009.

House prices matter in the UK because so much of the average person’s wealth is tied up in their home.

- When prices are rising, people feel more confident, and are more likely to spend money.

- This should show up in the wider economy (eg. GDP figures).

But house prices are difficult to measure, because they change hands infrequently, and each house is unique.

The new figure is very different to the ONS number for last month, which was £292K.

The ONS figures now uses all house sales, rather than just those bought with mortgages.

- The same problem exists with the indices from Halifax and Nationwide, which only use the houses that they lend against.

- I switched to the Land Registry data – which always used all sales – some time back.

- The drawback of this data is that it tends to lag, only being published about six week afters the month in question.

The new numbers also reduce the weighting of very high value properties (ie. it’s not a simple mean average price any more), and take into account measures like floor space.

- This is why it looks as though prices have dropped by £83K in a month.

Cash

Also in the FT, Paul Lewis – presenter of Radio 4’s MoneyBox was arguing that cash beats stocks, or rather that “active cash” can beat a FTSE-100 tracker.

- “Active cash” is Paul’s term for money moved once a year into the best-paying savings account.

I first heard this argument from Paul at the Master Investor show in April, but now that it’s hit the Weekend FT, it’s time to take a closer look.

Interest rates are at record lows, with a one-year savings “bond” yielding only 1.66%.

- Despite this, Paul is in favour of cash.

Paul has never liked the comparisons between stock returns and those on cash, since the former usually neglect commissions, spreads and holding fees.

- They also tend to compare stocks with government bonds, rather than an actual cash account.

- These will often be much lower than the “best-buy” accounts for cash.

Paul looked at 192 five-year periods from January 1995 to December 2015.

- Stocks returned 6% pa over the 21 years, while cash returned 5%.

- But cash beat “stocks” (an HSBC FTSE-100 tracker) in 57% of these five-year periods.

Paul also looked at 84 14-year periods (a very strange time-frame, if you ask me) and found that cash won in 96 per cent of these periods.

- Only after 18 years of investment did stocks start to pull ahead.

Some commentators have said that it’s not fair to compare the best buy in cash with the average return from stocks.

- But I think that it is fair, since you can know the best buy for cash in advance, whereas you won’t in general beat the stock average.

At the same time, a mythical investor who has the energy to switch cash accounts each year but is too lazy to re-balance his equity portfolio is a funny fish to follow.

I also think that it’s unfair comparing cash to the FTSE-100, an unrepresentative lumpy index.

- It would be much better to look at a diversified multi-asset portfolio.

And the vehicle used to represent the FTSE-100 is simply the longest standing tracker fund (from HSBC).

- This started in 1995.

- It would be better to look at the average return from stocks each year, and to go back further than the 21 years that the HSBC fund allows.

It’s also a mistake not to account for tax.

- The best buy rates for cash are usually not available within an ISA, and as your portfolio grows, this tax shelter becomes ever more important.

- Cash rates in SIPPs are usually zero.

It’s also possible that the period since 1995 is unrepresentative.

- Paul claims this is not the case by reference to the annual Barclays Equity Gilt Study (BEGS).

- The BEGS shows that cash returns 2.8% pa since 1899, while stocks return 7.3% pa.

- Paul puts the difference down to not accounting for charges, and not using “best buy” cash accounts.

But what is certain is that 18 years is only a fraction – I would argue less than a third – of the average person’s total investment horizon.

- And over fifty plus years, the difference between cash and stocks is likely to be very significant indeed.

- And not in favour of cash.

Merryn talked about Paul’s work, and made the same point about the lazy equity investor being compared to the energetic cash investor.

- She also thinks that trackers would do better going forward, since fees are much lower now than they were in 1995.

- And she points out that the Association of Investment Companies (the Investment Trust spokespeople) has stated that ITs beat the FTSE-100 and cash “by a substantial margin over 3, 5, 10 and 21 years.”

- That’s certainly been my personal experience.

To close, I’ll just repeat what I tweeted earlier in the week: everybody I know that stayed in cash is poor now.

- So stick with stocks, and keep your costs down.

Performance rewards

Tim Harford took a look at the world of performance rewards.

- These work best with jobs that are simple and easy to monitor – the “piece work” of factories, or the modern equivalent of flipping burgers – yet they tend to be applied to applied to C-suite jobs that are hard to measure.

Tim reports that money itself isn’t always the best incentive.

This finding has always puzzled me.

- I’ve worked in investment banks and consultancies with straightforward cash bonuses, and also in call centres where rewards ranged from voucher points towards “gifts” from an in-house Argos catalogue, to a weekly meat raffle.

- I always preferred the cash – I could turn that easily enough into Argos tat or meat if wanted to.

But other people seem to find extra cash grubby, and like other rewards as well or even instead.

Tim reported on the “Farmer Smith” experiments carried out on casual immigrant labour a British fruit farm.

- Piece work boosted output by 50%.

- Performance related pay for front-line managers increased output by another 20% (as managers no longer gave work to unproductive friends).

- Competition between self-selected teams of workers increased productivity by another 20%.

Some support for money here, but Tim also discussed a Zambian experiment where HIV prevention advice from hairdressers was better motivated by public acclaim for top performance than by cash.

A third experiment used airline pilots, with the objective of saving fuel on flights.

- 3% to 6% of savings were available, based around three things:

- calculating fuel needs carefully before take-off (so as to not carry too much heavy fuel)

- switching off engines while taxiing

- adjusting flap settings during flight for the most efficient altitude, speed and course

The captains were split into four groups, one of which was a control group that was simply told a fuel study was taking place:

- the “information” group got feedback on fuel consumption before, during and after flights

- the “target” group got the same information but were also given savings targets

- the “incentives” group could earn money for their favourite charity by hitting targets

Even simply telling that captains that fuel consumption was being monitored led to a reduction.

- Setting targets (with or without the charitable donation) lead to greater savings.

- The captains who hit their targets had greater job satisfaction.

So the best approach seems to be to tell people what good looks like, and to let them know that you’ve noticed they are achieving it.

The high street

After the recent collapse of BHS and Austin Reed, the Economist looked at the prospects for the UK high street.

- Non-food sales growth has been slowing since mid-2014, with sectors like clothing actually shrinking.

- Only the high end and the discount end are doing well.

In total, 14 chains have collapses in 2016, affecting 989 stores and 20K employees.

- This is despite median household income and GDP per person having recovered to their pre-recession levels.

Some of this is probably down to Brexit, but there are two other factors:

- People are now more interested in “experiences” (restaurants, holidays and the cinema) than in more stuff

- And young people in particular look for a “omni-channel” experience, where online and bricks and mortar stores work seamlessly together.

Last week also saw the start of Amazon Fresh, delivering mostly Morrisons’ food to parts of London.

- And the living wage which came into force in April hasn’t helped either.

There’s little prospect of things getting better.

Bond bubble

Buttonwood looked at the continuing bubble in bonds.

- Pessimists – myself included – have been calling the top of the bond market since 2011, but it keeps going up.

- In many countries, investors are now paying governments for the privilege of lending money to them.

- The yield on ten-year Gilts has fallen from 1.96% to 1.24% during 2016.

This was supposed to the year that the US led the world to economic normality.

- But no further rate hikes have followed the one in December 2015, and the ECB and the BoJ are sill buying bonds with QE.

With a Remain vote in the Brexit referendum, a win for Clinton in the US presidency, and a soft landing in China, things might just turn around.

- But don’t hold your breath – we might need sustained inflation or increased productivity figures.

- And neither of those looks very likely at the moment.

$50 oil

The newspaper also wondered whether $50 a barrel would be a high enough price to revive oil production.

- West Texas has just had its first monthly increase in rig count for a year.

- Not only have spot prices returned to $50 a barrel, so have one-year futures prices.

- This lets producers lock in profits and offset the risk of reopening wells.

The ease with which shale-oil production can be ramped up or shut down had a moderating effect on prices on the way down, and appears to be having the same effect on the way up.

- There’s still a production surplus of 1m barrels a day over consumption, so perhaps the $50 price won’t stick in any case.

- And if rigs and workers are in short supply, shale-producers’ costs may rise in line with the oil price.

The real story might be as much as a year away, when demand increases and recent under-investment in conventional oil sources starts to show up.

- Then the bulls think we might see oil at $80 a barrel.

- Or perhaps Saudi Arabia will increase production, and $50 a barrel will be the ceiling.

Micro-investing

And finally, Aime Williams looked at the trend for milennials to use apps that nudge them into saving small amounts.

- I’m all for anything that helps with saving, but the scenarios involved are faintly comical.

Tony Stenning, “Head of Retirement for Europe” at BlackRock is quoted as saying “you can go to Starbucks, buy your coffee for £1.80 and then add an extra 20p to your savings.

At the risk of stating the obvious, you could also not go to Starbucks, and add the whole £2 to your savings.

- No app required.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

One reason that some companies favour rewarding their staff with vouchers is that vouchers attract no tax, plus you can often buy them in commercial bulk at a discount. I bought a Dyson vacuum cleaner and a dehumidifier with my last lot of Argos vouchers!

Are you sure about that? Looks like they are taxable:

https://www.gov.uk/guidance/employee-incentive-awards

And wouldn’t you rather have the cash instead?