- Robinhood in the US is perhaps the most famous one, but over here we have Revolut (planned) and Freetrade (live).

- Trading 212 have commission-free trading on leveraged products and 600 UK shares, and social trading platform eToro is also planning to launch a service. in the summer.

I signed up to the waitlist for Freetrade a long time ago, and persuaded enough of my friends and colleagues to do the same with my referral code that I made it almost to the front of the queue.

- So I was looking forward to the beta test until I discovered that there was no desktop site, no android app and the iOS app needed a recent version to work.

- Even the waitlist app for android needed a recent version of that operating system.

Even if I were to own more modern devices (( You’ll rarely see me with a phone or tablet that isn’t at least two years old, since most of my equipment is handed down from someone who cares a lot more about having the latest gear )) I’m not a fan of trading from phones.

- So the lack of a website I can trade from is the biggest issue.

I’ll try not to hold this negative experience against them.

Trades on the main UK platforms run from £12 at Hargreaves Lansdown, down to £5 at iWeb and £6 at X-O.

- I tried out DeGiro, where most trades work out at less than £2, but their European insurance scheme meant that I never put more than £20K into the account.

Some platforms have discounts for frequent traders (usually cheap trades in the month following a busy month, which is not as useful as it sounds).

- Others allow cheap trades if you bundle your purchase with everyone else, in a large trade done once per day.

Which is essentially the approach that Freetrade use.

- Freetrade charge nothing for the 4pm bulk trade, and just £1 if you want your own instant trade.

- They also charge £3 per month for an ISA.

It’s not quite cheap enough to make me want to switch from iWeb, but I might give it a whirl the next time that I need a taxable trading account.

- Another drawback is that at the time or writing they only offer 335 securities (122 US stocks, 136 UK stocks plus 33 investment trusts and 44 ETFs).

I guess the attraction to novice investors is that you can get started with a lot less money.

- You could even put together a sensible diversified small portfolio if you wanted to.

Freetrade are planning a premium service (to be called “Alpha”) later this year.

- That will be £7 a month, which takes them up into SIPP territory (the AJ Bell SIPP is not much more than this).

So it will be interesting to see what’s on offer then.

Dot Residential

Andy Bounds wrote about Dot Residential, and new online platform for aspiring landlords.

- It provides rental properties mortgages and tenants in Manchester and Liverpool.

It will set up a company to own the home, allowing the casual investor more easily to build a property portfolio — and pay corporation tax at 20%, rather than income tax of 40%, on earnings. Dividends are taxed at 27.5%.

Buy to let (BTL) investors have been hit by tax changes in recent years, and larger players have responded by moving properties inside companies and becoming professional landlords.

- Dot Residential appears to allow the same solution for landlords of all sizes.

But there are a lot of fees:

- In addition to the taxes above, loans costs 5% pa and there is a £5K up-front cost for refurbing the property.

- That’s 3% on a typical £150K property.

Gross rents are apparently close to 10%, which I find surprising.

- Net yields are expected to be 4% (presumably before tax), or perhaps 6% if landlords arrange cheaper finance for themselves.

Dot plans to expand to US secondary cities (Austin and Denver were mentioned) later this year.

Redwood fund

John Redwood had another of his regular updates on the ETF portfolio he runs for the FT.

- It’s up 7.5% for the first quarter of 2019, with the US (particularly the Nasdaq) and China largely responsible.

This most unloved of all bull markets has enjoyed a new lease of life. The excessive pessimism of December was banished by the US Federal Reserve and the Chinese authorities pointing to changes of policy to relax the squeeze.

John expects interest rates and inflation to remain low.

- But there is a manufacturing downturn, affecting Germany and its car sector in particular.

Melt-up

Michael Mackenzie wrote that the possibility of a “melt-up” in markets in s back on after the impressive first quarter in the US and China.

- Larry Fink of BlackRock said last week that there is “too much global pessimism” and that money on the sidelines would go back into equities.

Michael notes that institutional investors who have favoured cash in recent months are now in a difficult spot.

- The same goes for private investors, too.

Tech IPOs

In MoneyWeek, Merryn Somerset Webb looked at tech IPOs, and Uber in particular.

It has never made a profit. It has little obvious prospect of ever making a profit. It isn’t considered remotely risqué to buy into loss-making firms when they list.

More than 80% of firms that listed in the US during 2018 were loss-making.

- The last time this happened was 2000.

For more on this topic, see the Quick Links section below, where we have a couple of articles from the Economist.

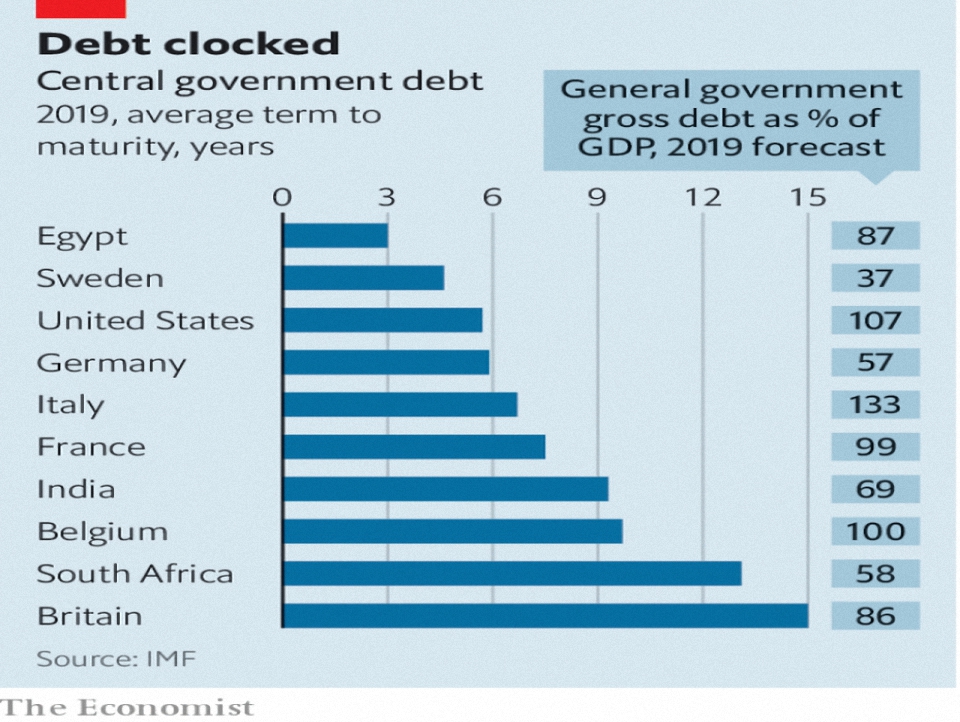

Bond maturities

In the Economist, Buttonwood looked at the tug-of-war between cost and uncertainty which determines bond maturities.

In public finance theory:

Debt is deferred taxation. A dollar of debt will cut today’s tax bill by a dollar, but at the cost of raising it by a dollar tomorrow. If the debt is a one-year bond, the tax bill will come sooner. If it is a ten-year bond, it will come later.

In practice, things are messier:

The government wants to keep today’s taxes low: that pulls it towards short-term bonds, the cheapest to issue. But it is wary of sudden increases in interest rates: that pushes it to issue long-term bonds, to limit “rollover” risk when bonds come due.

Certainty should matter more to high-debt countries, and cost to low-debt countries.

- The chart shows there is a tendency for high-debt countries to issue longer bonds.

Rollover risk is also a bigger issue for emerging markets.

- So despite their low debt-to-GDP ratios (53%, cf. 104% for rich countries) the average maturity is similar (around seven years).

The US is a special case, with shorter-tern debt than might be expected.

- Because a lot of trade financing and derivatives are priced in dollars, there is extra demand for short US debt (which is cheap to issue and safer for borrowers).

Britain, with moderat debt that is very long, is at the other end of the continuum.

- This is probably down to liability matching demand from pension funds.

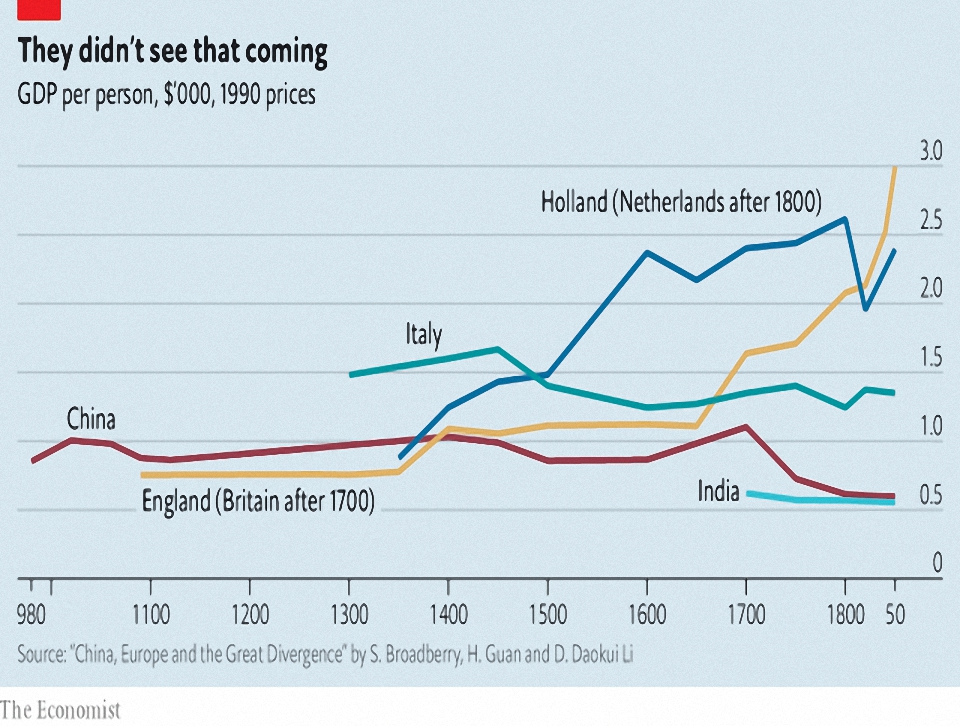

Population growth

The newspaper also looked at the link between population and growth.

- In theory – and in the very long run – size is a great benefit.

There are several related potential advantages:

- The more people you have, the more chance you have that one will be a genius inventor (the Economist cites Gutenberg and Watt, but I would have chosen from the Industrial Revolution in Northern England)

- The bigger your internal market, the you can boost output through (i) specialisation and (ii) trade with less blessed nations.

- The more people you have, the bigger the return is on a new invention, and hence the larger i the incentive for someone to produce something new.

A complicating force is migration.

- At the moment, the richest places are not the most populous, so in a free world there would be a brain drain from poor large countries to rich smaller ones.

- With limited migration (as is usually the case) the large poor countries should catch up and eventually overtake (note that this process should take upwards of 400 years).

The problem with this argument is that the large populations of China and India over the past 1,00 years have not protected them against the developments in (for example)Britain and Holland.

- The recent rise of emerging markets has been driven by globalisation and technology transfer, not population size.

I think there’s more to it than size.

- The US certainly benefited from its large internal market when playing catch-up with the UK (as China but not so much India is benefiting now).

- And the UK benefited from it’s exploitation of external trade networks.

But you have to come up with something great to sell in the first place.

- Size isn’t everything.

Quick links

I have six for you this week, the first four from the Economist:

- The wave of unicorn IPOs reveals the Silicon Valley groupthink.

- Tech’s new stars have no path to high profits.

- Big carmakers are betting on electric vehicles.

- Apple and Qualcomm have settled their patent feud.

- Musings on Markets looked at the Uber IPO.

- and Flirting with Models examined the Speed Limit of Trend.

Until next time.