Weekly Roundup, 5th July 2021

We begin today’s Weekly Roundup with a look at smart beta in bonds.

Bond Factors

John Authers looked at a new report from Robeco looking at outperformance factors (smart beta) in bonds.

As John points out, bond investing has two problems:

- Market-cap weighting puts you into the biggest (riskiest?) issues

- The bond market has been in a one-way trend for 40 years, but the regime might be about to change

I would add a third – yields are very low, or even negative at the moment.

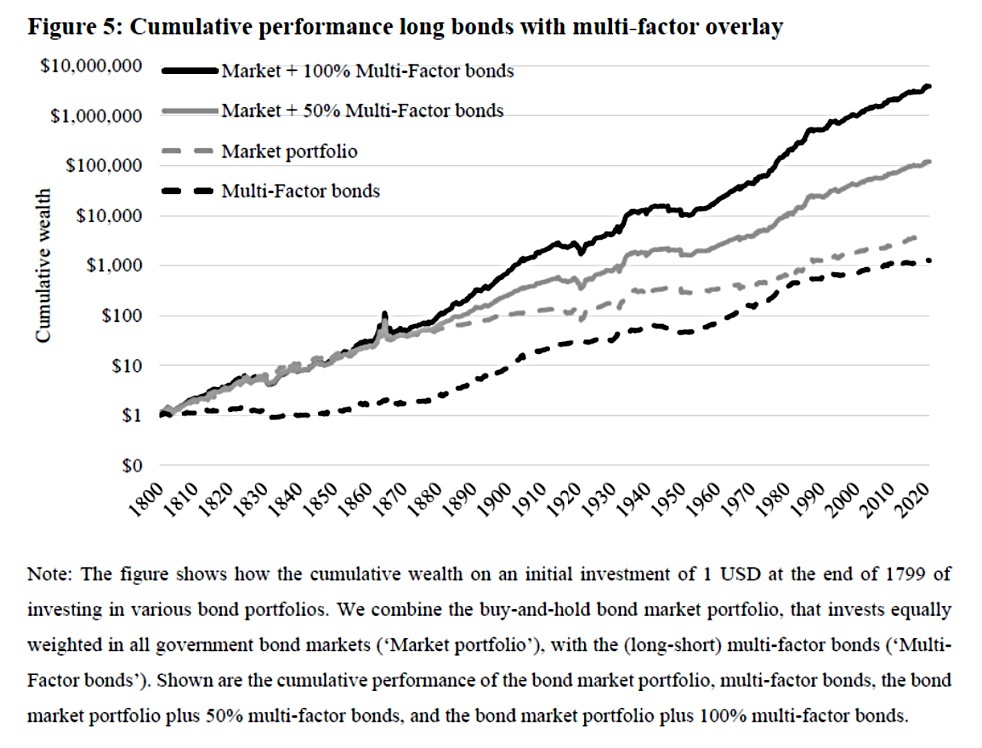

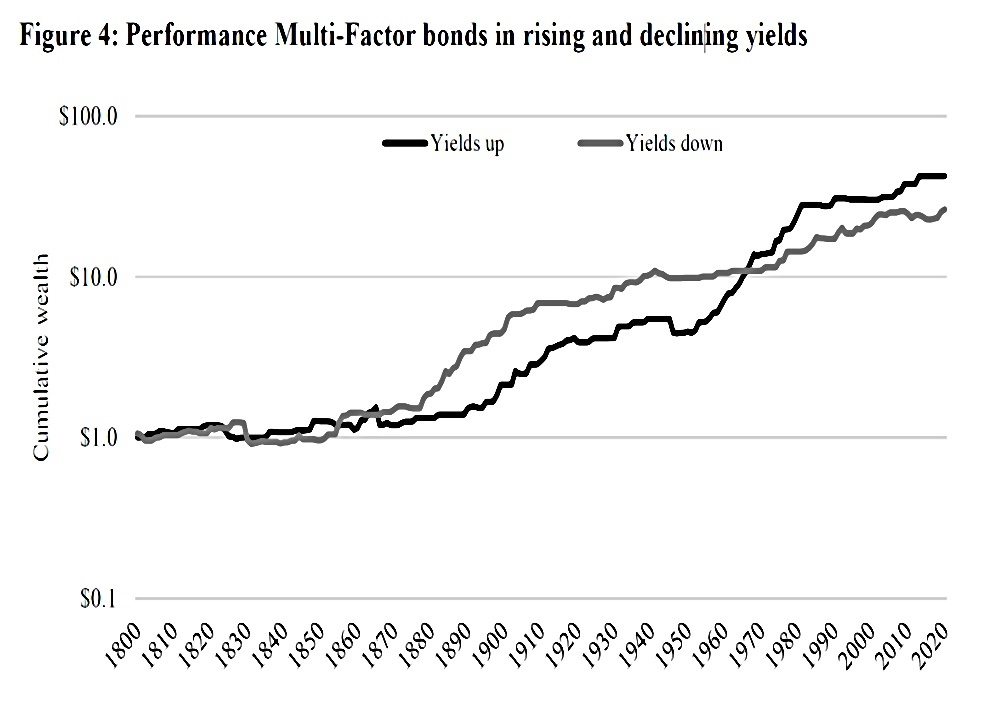

The new paper looks at data from France, Germany, Japan, the UK and the US over 220 years.

Robeco looked at three factors familiar from stocks:

- Momentum

- The study used 12 months minus 1 month

- Value

- They used yield relative to inflation, and yield relative to short-term T-bills

- This is a carry trade

- Low Vol

- As with low beta stocks, the study preferred bonds with low sensitivity to market moves

The factors don’t outperform the market, but they are uncorrelated, so adding them to a market-cap portfolio improves returns.

And it works whether bond yields are rising or declining.

So it looks as though they’ve found a way to improve on the market returns on bonds, year in and year out.

The authors of the paper explain the factors in behavioural terms.

The momentum effect, for example, is based in our behavior and our tendency to overreact, and it is visible in equities, commodities and currencies. Bond markets are strongly driven by sentiment around central banks and core macroeconomic indicators. But then we have seen over the past week that emotion on these matters is prone to overshooting and exaggeration.

The real danger is that now that these effects are known, they will stop working.

- In the meantime, let’s hope that some ETFs turn up so that we can take advantage.

Pension consolidation

In the FT, Josephine Cumbo had a couple of articles (1 and 2) on the proposed consolidation of company pension schemes.

- The rollout of workplace auto-enrolment means that there are now 1500 DC company schemes in the UK. (( I assume that small companies like mine – who mostly use schemes like Nest, NOW: and The People’s Pension – are excluded from both these statistics and the consolidation proposals ))

Last year, the government said that schemes with assets below £100M would need to pass “value-for-member” tests in order to “justify their continued existence”.

- Trustees of schemes that fail the tests would need to wind up the plan and transfer the members and assets into a larger scheme.

This makes some sense, but it’s not immediately clear how the larger scheme would be chosen or what incentive they would have to take on members from other companies.

- Nor is it clear who would pay for the costs of mergers.

Pensions minister Guy Opperman said last month that he might extend the tests to schemes with less than £5 bn in assets (fifty times more).

There is no doubt in my mind that there must be further consolidation in the occupational defined contribution pensions market. We know from other countries such as Australia that scale is the biggest driver in achieving value for money for savers and ultimately better retirement outcomes.

Further consolidation will drive better outcomes for members through better governance and greater investment in illiquid assets.

The illiquid assets the government has in mind include property, venture capital, private equity and infrastructure, including renewable energy plants like wind farms.

- In order to allow access to PE, the cap on payments to fund managers will be relaxed from October 2021.

Performance fees will be smoother over five years to avoid breaching the 0.75% pa cap, though PE and real estate industry feedback has suggested that ten years might be better.

- And of course, larger DC schemes should be able to negotiate better discounts from the traditional “two and twenty”.

Opperman said:

By not consolidating quickly enough schemes will not have the capability to grasp these opportunities with both hands. It is important that they move more quickly. This will ensure savers do not miss out but this will also help the UK build back better.

Fed tone

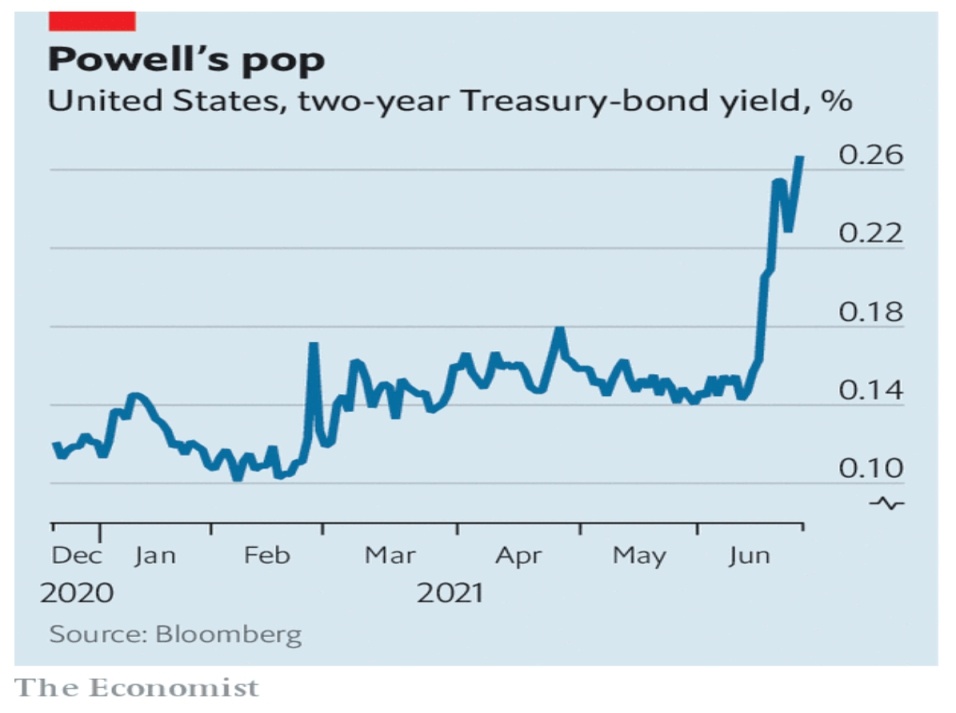

The Economist had a couple of articles (1 and 2) on the new tone from the Federal Reserve.

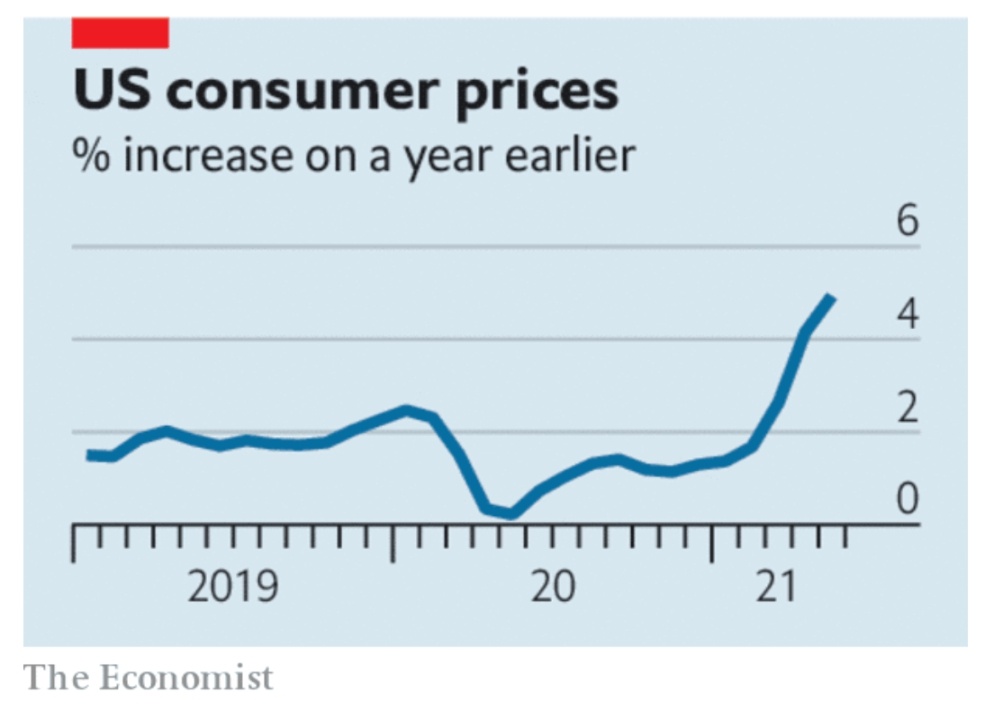

At the Federal Reserve’s meeting in June policymakers signalled that they may raise interest rates in 2023, sooner than they previously thought, and upgraded their inflation forecasts for this year.

The market reaction was mixed: bond yields rose (bond prices fell) and then fell back (recovered).

- Stocks fell and recovered, and commodities fell.

- Emerging market currencies fell against the dollar (and didn’t recover).

The central bank expects its preferred measure of prices to be 3.4% higher at the end of 2021 than a year earlier—or 0.6% higher than it would have been had inflation been on target since the end of 2019. Count from August 2020, when average-inflation targeting was introduced, and the price overshoot will be 1.2%

The Economist welcomes the change of tone but notes that the Fed is generally bad at forecasting.

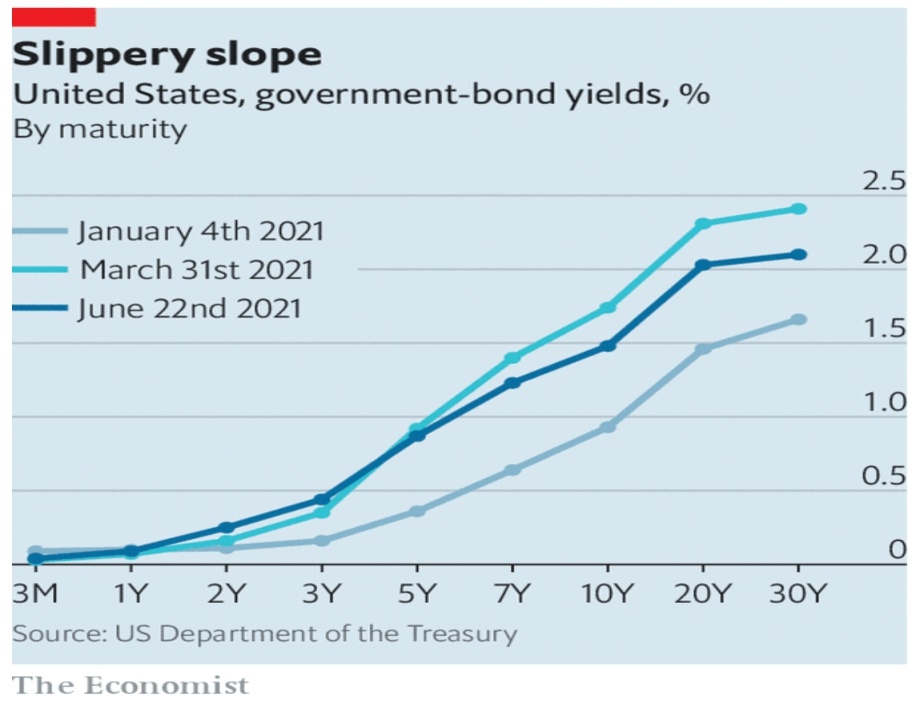

Buttonwood wrote about a new phase in the financial cycle.

- He notes that the slope of the Treasury yield curve is an indicator of where we are in the cycle.

In the first quarter, a steepening in its slope—a rise in long-term yields relative to short-term yields—said the economy was accelerating and inflation was coming. A lot of that steepening has since been reversed, to the surprise of many.

The two-year to 10-year gap rose from 0.82% to 1.58%, before falling back to around 1.1%.

The bond market is hinting that the early-cycle phase in which risk assets are embraced almost without discrimination has come to a close. The peak in economic growth may have passed.

Binance

The FCA has ordered Binance to stop all regulated activity in the UK.

Binance Markets Limited is not permitted to undertake any regulated activity in the UK. No other entity in the Binance Group holds any form of UK authorisation, registration or licence to conduct regulated activity in the UK.

The company has to display a notice to this effect on its website and social media channels.

The FCA also issued another general crypto warning:

Be wary of adverts online and on social media promising high returns on investments in cryptoasset or cryptoasset-related products.

While we don’t regulate cryptoassets like Bitcoin or Ether, we do regulate certain cryptoasset derivatives (such as futures contracts, contracts for difference and options), as well as those cryptoassets we would consider ‘securities,’.

A firm must be authorised by us to advertise or sell these products in the UK.

Binance is a Caymans Islands holding company founded in 2017 by Chinese-Canadian software developer Changpeng Zhao (known as CZ), though to be worth $1.9 bn.

There was no explanation from the FCA as to why this action had been taken, but there is speculation that Binance has been unable to comply with anti-money-laundering rules.

- Binance had applied to become a registered cryptocurrency company in the UK, but withdrew the application in May, “following intensive engagement from the FCA”.

Binance said that the FCA action would have no practical impact because Binance Markets Limited is a separate legal entity from Binance.com.

The FCA notice has no direct impact on the services provided on Binance.com. Our relationship with our users has not changed. We take a collaborative approach in working with regulators and we take our compliance obligations very seriously. We are actively keeping abreast of changing policies, rules and laws in this new space.

Last month, Japan’s Financial Services Agency noted that Binance was operating in the country illegally, and the US Justice Department and IRS have also been investigating possible money laundering and tax offences by Binance.

- The German regulator BaFin has also warned that Binance could be fined for offering digital tokens without an investor prospectus.

It’s not clear to me how this new FCA action exceeds the previous ban on retail access to cryptocurrency derivatives.

- As far as I can tell, buying and selling “actual” bitcoin and ether (can we call this spot BTC?) is an unregulated activity, and as such can continue.

The more paranoid amongst investors are likely to see the singling out of Binance as a red flag, and they are likely to prefer to use other exchanges.

Quick Links

I have just four for you this week:

- The Economist wondered whether Facebook is a monopolist

- HL reported that private equity firm Bridgepoint is planning a London IPO

- Alpha Architect looked at how investment horizon affects the results from the low volatility factor

- And also asked whether investors can beat active funds by using cheap ETFs.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

Call me cynical, but reducing the number of employer DC schemes might just make it easier for the government to ‘target’ them for future initiatives!

No need to be cynical – they want schemes to invest in (green) infrastructure. I think auto-enrolment shows the government is keen on employer DC schemes.