Trend and Macro – AQR

Today’s post looks at a recent paper from AQR on the impact of the macro environment on trend-following returns.

Contents

AQR – Trend and Macro

The paper came out in the Fourth Quarter of 2022 and had no credited authors.

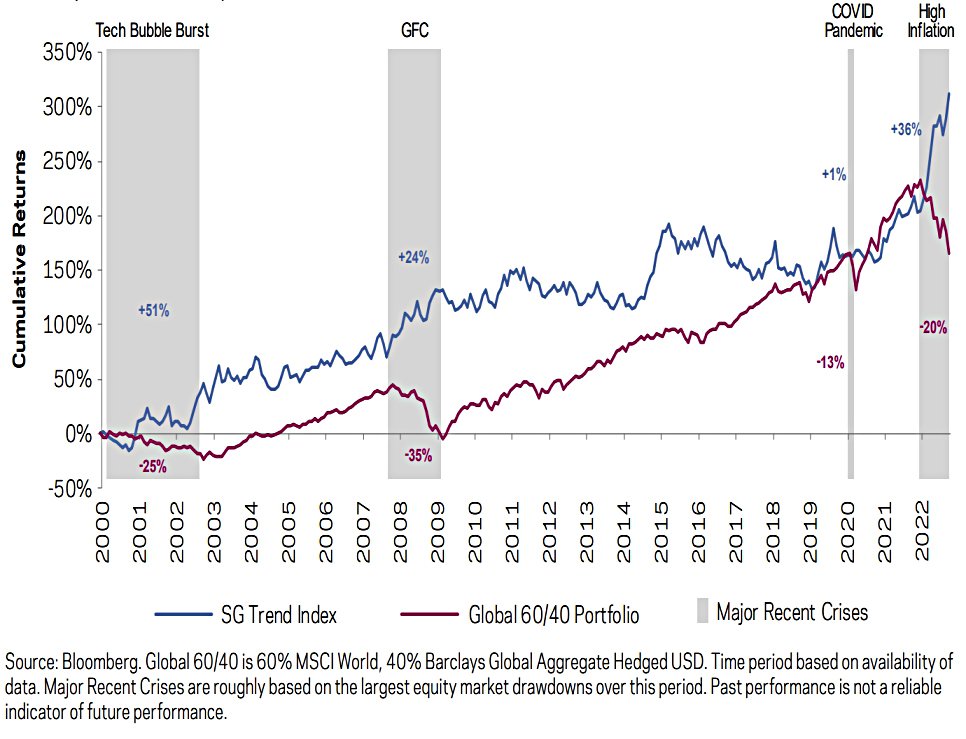

- When the paper was written, trend was having a great year, whilst the more traditional 60/40 portfolios had one of their worst years for decades.

Through September 2022, trend was up 36% and 60/40 was down 20%.

The paper discusses whether it was too late to get on board the trend “trade”, and compares the macroeconomic environment of 2022 to that of the 2010s when trend underperformed.

- The paper also looks at trend’s track record through other downturns for mainstream portfolios.

The conclusion is that trend might continue to outperform and could act as a valuable diversifier to traditional portfolios.

Trend’s track record

Since 2000 (when it was created) the SG Trend Index has delivered higher returns and slightly higher risk-adjusted returns than 60/40.

- It also performs well when 60/40 is doing badly – it has a low correlation to 60/40, making it a useful diversifier.

But trend significantly underperformed during the 2010s.

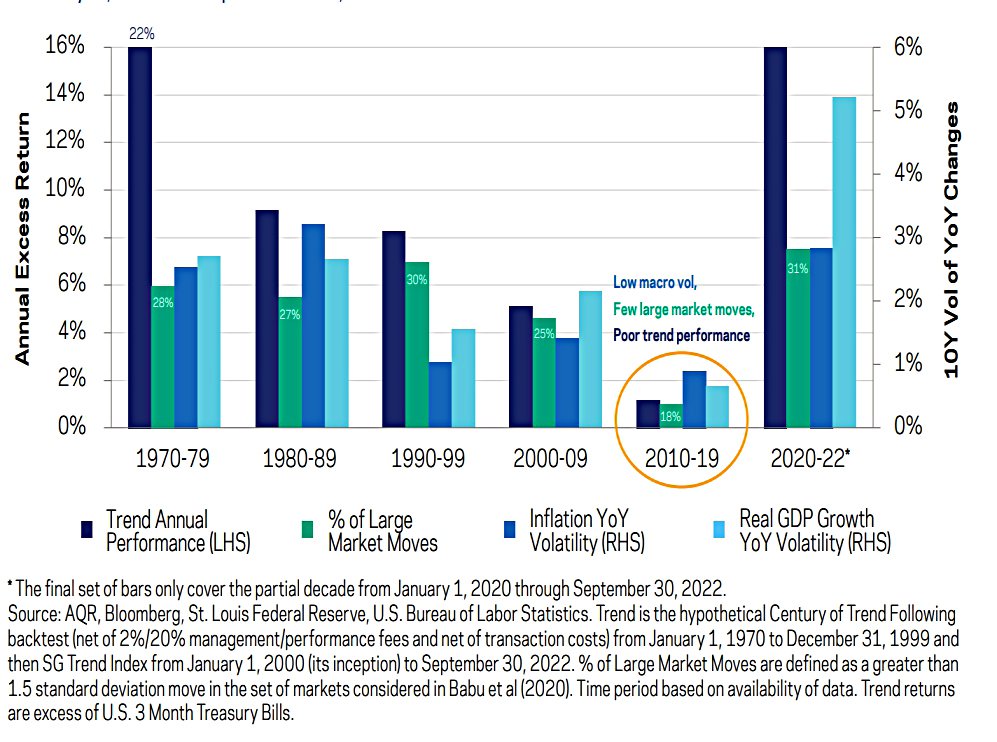

Macro Forces in the 2010s

AQR found that the 2010s were unusual compared to the last century.

Markets displayed unusually small moves, which coincided with a global economic backdrop that was relatively stable and featured few (if any) major crises.

They note that the US markets showed a strong uptrend, but trend followers use dozens to hundreds of markets, and would not have a large allocation to US stocks.

- Equity drawdowns (the taper tantrum in 2013, or one in 2018) were short-lived.

AQR wanted to know why there were no strong trends, and came up with three reasons:

- benign macroeconomic shocks

- soft growth and stubbornly low inflation, and

- central bank policy constrained by an effective lower bound on long-maturity bond yields

These conditions kept asset prices high.

Trend-following strategies capture the tendency of markets to gradually incorporate new information. In the 2010s, new information tended to be smaller in size and less persistent in duration than in other periods.

There was no GFC or Covid – or inflation.

With tepid growth and below-target inflation, central banks were able to respond to macro events – usually with stimulus – thereby stabilising prices (and dampening trends).

- The lower bound on bond yields made things even more unusual.

Typically, nominal bond yields in the range of 0 to 3 percent (real yields between -2 and 1 percent), would be highly stimulative, spurring spending and leading to stronger economic growth and higher inflation.

Post-GFC, this didn’t happen.

Central banks were able to drive yields to very low levels (primarily via forward guidance and asset purchases) in response to deteriorating economic conditions, without fear of stoking inflation.

The Return of Macro Volatility

Now, given the backdrop of persistently high inflation, a rapid and resolute shift in central banks’ policies, and the unexpected war in Ukraine, macroeconomic volatility is on the rise.

This means that the good times are back for trend following.

- The SG Trend Index is having its best year ever – will this continue?

AQR notes that periods of significant macro volatility tend to be followed by more elevated volatility (momentum everywhere).

- It also looks like a stretch that conditions return to their pre-pandemic “normal” in the near future.

A return to such a quiet state of the world would likely require a substantial moderation of global inflation, and history suggests this is unlikely to occur abruptly.

AQR predict a recession and expects the return of difficult trade-offs (between inflation, growth and unemployment) for central banks.

It is less likely central banks will be able to suppress market moves to the extent they did in the prior decade.

Enhanced Trend Following

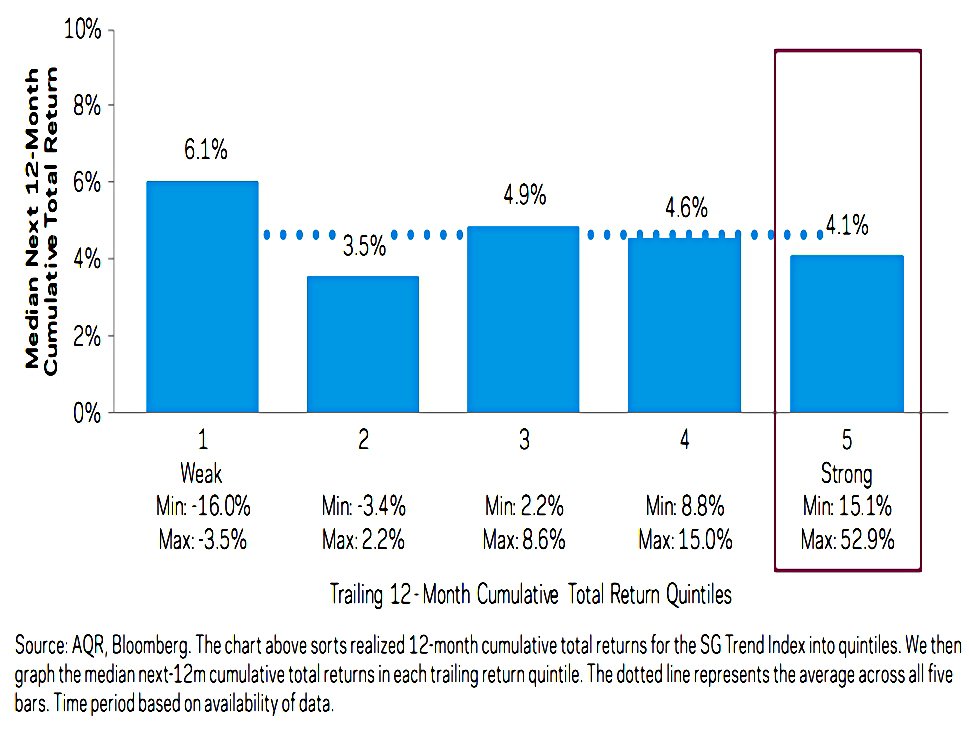

The next section of the paper provides more evidence for the idea that trend following can continue to perform well after a period of strong performance.

- But the problem remains of sticking with trend through its inevitable periods of underperformance.

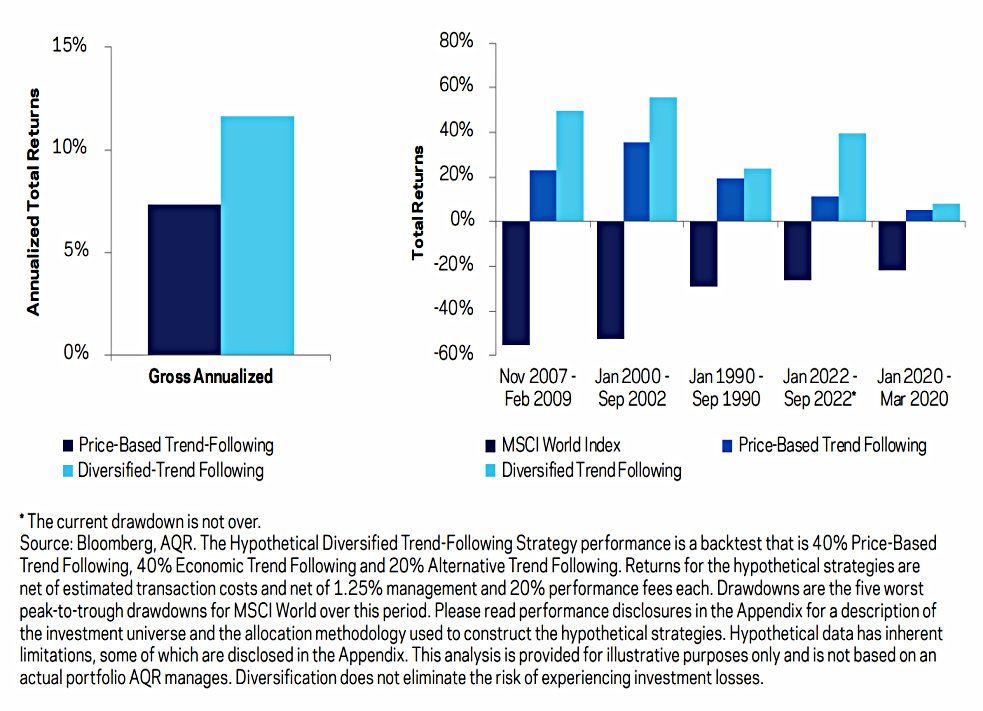

One approach may be to implement a more diversified approach to trend-following that may provide better average returns and even stronger protective properties.

AQR’s diversified trend-following adds economic trends and alternative markets (no details supplied) to traditional price trend following.

- They use a 40/40/20 mix of price, economics and alternative markets.

This leads to higher returns and better protection during equity drawdowns.

Digging into the appendices provided the following detail on the enhancements:

The Hypothetical Economic Trend-Following Strategy is based on trend following which for each theme (Growth, Inflation, International Trade, Monetary Policy, Risk Aversion) and within each asset class, takes a long position in assets in which economic trends are improving and a short position in assets in which economic trends are deteriorating.

The Hypothetical Alternative Trend-Following Strategy was constructed with an equal-weighted combination of 1-month, 3-month, and 12-month trend-following strategies for markets across 6 major asset groups – equity factor portfolios, credit indices, interest rate swaps, emerging currencies, alternative commodities, and volatility futures.

Conclusions

That’s it for today.

- It’s a short paper, but it makes it pretty clear that the underperformance of trend in the 2010s was down to unusual macro conditions.

These conditions are over and not likely to return.

- So we can look forward to trend performing in the future.

And AQR’s diversified trend approach should do even better.

- Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.