Weekly Roundup, 9th May 2018

We begin today’s Weekly Roundup in the FT, with the Chart That Tells A Story. This week it was about the widening gap between growth and value stocks.

Contents

Growth vs value

Kate Beioley reported that growth stocks are now almost as far ahead of value stocks as they were at the height of the dot com boom.

- Perceived wisdom is that value stocks outperform in the long run, but growth stocks are well ahead even over 30 years.

Of course, such a wide gap still means that the immediate prospects for value stocks are likely to be better than those for growth stocks.

- The kind of relationship is often seen at the end of bull markets.

- And rising interest rates (if they can be delivered) are good for value stocks like banks.

Of course, the past is not the same as the future.

- Unlike 2000, today’s tech stocks are highly profitable and cash rich.

Perhaps the leading growth stocks (the FAANGS) have developed monopoly powers that allow them to generate superior profits.

- Or perhaps these profits will be whittled away by regulation rather than by direct competition.

Help to sell

Norma Cohen argued that what the UK housing market needs is not more Help to Buy, but Help to Sell – assistance for older homeowners with too much space.

- I fill my own space very nicely thank you, but I can see where Norma is coming from.

The first problem is a lack of suitable homes for these people to move into.

- They want smaller properties, but often in the same area in which they already live.

- And they might need specialist facilities, support and assistance.

Retirement housing is slowly increasing as a proportion of the UK housing stock, but it’s only up from 1% to 2.6% today.

And many of these are in “Care Villages”.

- Properties are often expensive, since communal facilities impact densities.

This type of property usually comes with an onerous service contract and suffers from the same poor resale values as properties in purpose-built holiday villages.

- There can also be an “event fee” of 20% to 30% when ownership is transferred.

- Sometimes an annual fee of 1% to 2% is charged instead.

McCarthy & Stone is the market leader in this area, but does not charge event fees.

Norma thinks that land hoarding is the big problem, and wants to see a new tax.

- At the same time, a reduction in stamp duty would also help people to leave their existing homes.

Beach huts

In his Rich People’s Problems column, James Max looked at beach huts.

- They are a potentially interesting niche asset class, but I wasn’t sure that the numbers stacked up.

James’ hut cost £28K (plus £4K of renovations) and is in Frinton-on-Sea, a resort I’m not familiar with.

- In more fashionable locations you can pay upwards of £100K.

As a non-resident, James pays almost £1K a year for a licence, £300 in insurance and a few hundred a year in maintenance.

- There’s no water or electricity or toilet, and you can’t sleep there overnight.

Despite this, he says he could rent the hut out for £130 a week.

Assuming an optimistic 30 weeks of rentals, that’s £3.9K a year.

- Net of expenses, it’s more like £2.4K.

On a base cost of £32K, that’s a tidy yield of 7.5%.

- Perhaps I should investigate further.

UK not cheap

Ken Fisher was trying to decide whether UK stocks were Dr Jekyll or Mr Hyde.

- Global investors are bearish on the UK, so the market is trading on more than its usual discount to the world index.

- The pound is also near 30-year lows on a trade-weighted basis.

- Consumer confidence is low and business confidence is not high.

But the yield spread is positive and there have been 21 quarters of GDP growth (though recent growth was weak).

- Ken also sees the UK’s gridlocked politics and weak government as a positive:

Gridlock keeps legislative risk low, which markets like, since it reduces the risk of new laws disrupting property rights and regulation.

It also raises the likelihood of a “middle of the road” Brexit deal.

Coming back to the markets, UK stocks are skewed to commodities and defensives, with little tech.

- This is not a good mix at the end of a bull market (it’s better suited to the middle third of a bull).

Ken likes UK healthcare stocks but thinks the tech firms of the USA and Asia are a better bet.

- European banks and consumer giants will follow, with the UK’s time yet to come.

Profit warnings and Beaufort

John Lee’s column was about what to do after a profit warning.

- John was recently a speaker at the Mello private investors’ conference (which I will cover in a moment).

There he attended the Stockopedia session on what to do after a profit warning.

- We covered this last year – spoiler alert: you have to sell.

John has a large and concentrated portfolio, so selling is not so easy for him.

- He has recently hung on to PZ Cussons after a warning, as well as Air Partner.

The rest of us remain well-advised to sell.

John also commented on the Beaufort Securities issue, where administrators PWC propose to take their fee (of £100M!) from supposedly ring-fenced client funds.

- Although I had never heard of Beaufort until their collapse, this is clearly ridiculous.

- Anyone who had more than £50K with the firm would be impacted.

ShareSoc are threatening to sue PWC on behalf of private investors.

- You can support their campaign here.

John Lee has himself asked a written question in the House of Lords about the basis on which PWC can access the ring-fenced funds.

Mello

Andy Bounds reported back from Mello, a two-day investor conference held in Derby.

Mello is the brainchild of David Stredder, a leading light in ShareSoc who we’ve met several times before.

The conference differs from most UK investor conferences in several ways:

- the quality of the presenting companies

- the seriousness of the attending investors (who have paid to attend) – this is in part explained by the scale (there are 500 attendees, rather than the thousands at the big London shows)

- the social aspects of the event – its tag line is “Invest in good company”

I didn’t go to Mello (although I had paid for a ticket) for several reasons:

- Derby is a long way from London and I prefer my investment conferences to take place in Zone 1

- I don’t like company director presentations as I don’t want to develop attachments to firms

- There had been a lot of investor events in London around the end of the tax year

But the main reason is that in common with most UK investor events, Mello over-emphasises stock-picking.

- Asset allocation, costs and taxes are much more important in terms of your investment results.

Stock-picking is a fun hobby, but few investors can justify more than a 20% to 25% exposure to actively -managed UK stocks (especially the AIM stocks that are the favourites of many attendees).

I’ve had a number of conversations in recent months (at shows and on Twitter) which suggest to me that this is a message that few UK investors want to hear.

- So I’ll be attending far fewer events in the future, unless I can find some with a broader scope.

Groups that don’t focus on stock-picking tend to focus on another small aspect of investing (crypto, oil and gas, gold and miners, AIM minnows, Vanguard index trackers, Buy-to-Let).

- All of these have their place, but I’d like to be a member of a group that discussed all of them (along with regulation, macro-economics and drawdown strategies).

I’m prepared to start such a group myself, but I suspect there is no demand.

- If you are interested, let me know in the comments (or drop me an email – the address is in the left sidebar).

Merger frenzy and old mortgages

Merryn’s FT column was about merger frenzy.

- A dozen large deals have been announced in recent days.

She worries that all this swapping of shares doesn’t get us anywhere.

- Stock markets are supposed to funnel cash into new productive activities.

- But cheap money (low interest rates) makes it easier to buy market share and cost savings.

US companies have returned an average of 60% of earnings to their shareholders over the last 50 years.

- Over the last three years that has increased to more than 100%.

Since most investors are getting old and seek a yield that bonds no longer deliver, they are happy with this short-term harvesting of cash flows today at the expense of growth tomorrow.

- But there could be long term problems, as well an increased inequality and oligopoly.

Merryn’s MoneyWeek column was about an old mortgage deed that she shared on Twitter.

- It was a £35K loan from 1990 at 14.75% pa.

Older Twitterati remembered the hell of such high interest rates, while young people envied being able to buy a house for so little.

- There’s no doubt that the house price to income ratio has gone up since then (from 3.5 times to 5.5 times) but because of low interest rates, affordability has come down.

Mortgage payments were more than 50% of income in 1990, but now they are around 30%.

- The problem has become borrowing enough money in the first place (though I can confirm that this was always the problem – house prices are largely driven by how much first-time buyers can borrow).

LTA tax

Josephine Cumbo reported that the tax generated from breaches of the pensions lifetime allowance (LTA) has almost tripled, from £40M in 2014-15 to £110M in 2016-17.

- The LTA is a stupid tax that punishes good investment performance – it’s charged on outputs rather than inputs.

- And the threshold is way too low – £1M can safely generate just £26K at age 55.

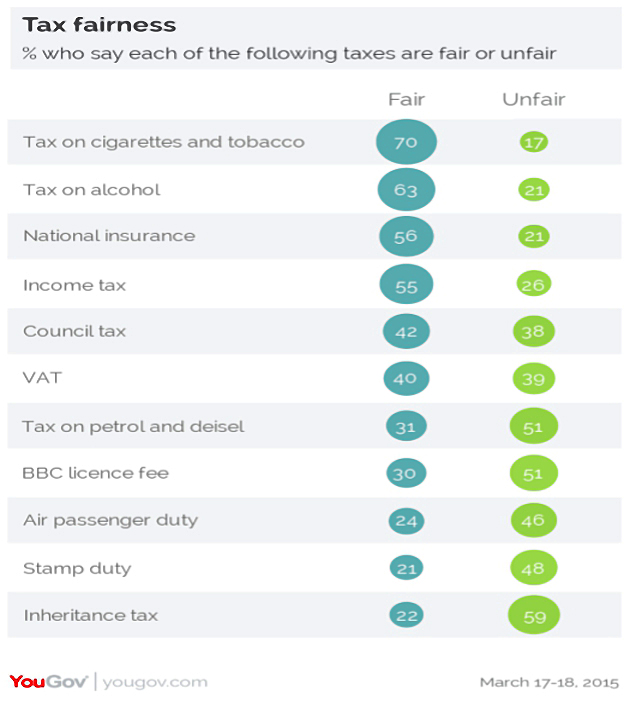

Inheritance tax

Andy Tilbrook collated FT reader responses to the government’s proposed review of IHT.

The FT claimed that its readership was split down the middle, though surveys regularly find that IHT is the least popular tax of all.

A lot of FT readers wanted to scrap IHT or raise the threshold to millions so that they could provide for their children.

- Others worried that the rich simply evade IHT or move assets out of the country, which is not desirable.

Yet others suggested taxing the recipient instead.

- This was also suggested by the Resolution Foundation as part of their paper call “A new generational contract”.

- I’ll return to this paper in a future article.

Less sophisticated readers tried to claim a moral difference between earned and “unearned” wealth (that produced by deferred income), or stated that they couldn’t be impacted by a tax that was collected after they were dead.

Emerging markets and the dollar

John Authers looked at the pressure on emerging markets from the strengthening dollar.

- Argentina has raised interest rates to 40% to defend the peso, whilst the Turkish lira is setting (bad) records.

John expects lots more emerging markets to have problems in the coming months.

The next crisis

In the Economist, Buttonwood looked at where the next financial crisis might occur.

There are three common causes:

- too much borrowing

- concentrated bets on a single outcome

- a mismatch between assets and liabilities

The 2008 crisis involved all three .

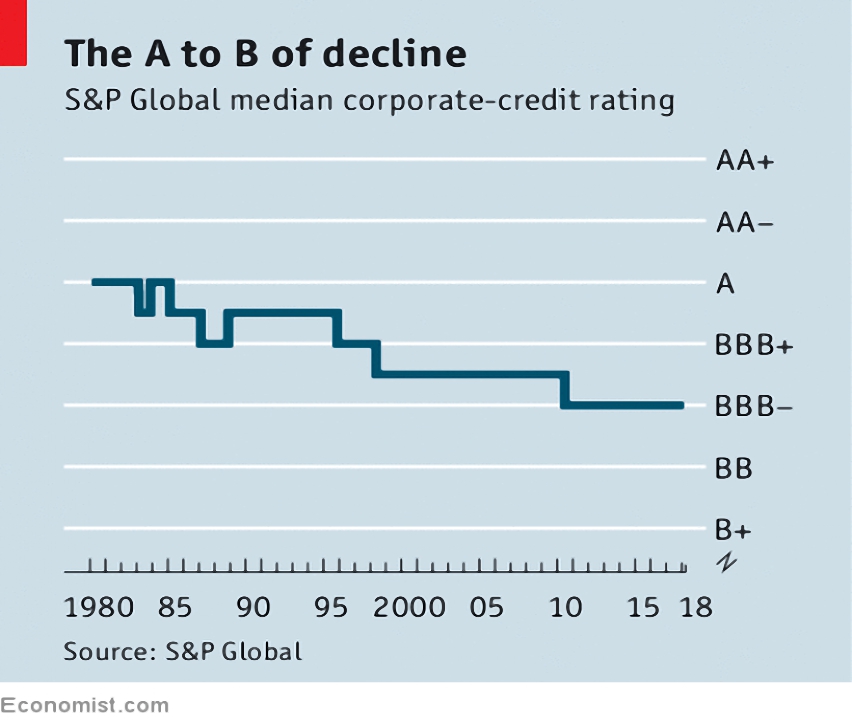

Buttonwood thinks that corporate debt could cause the next crisis.

- Spare cash is being used to bay back shares and balance sheets are being made more “efficient” (risky).

- 37% of global companies are now “highly indebted”, 5% more than in 2007.

And as the chart shows, the credit quality of the median bond has been dropping.

- It’s now one notch above junk (BB+), yet yields have not risen (since returns on cash are so low).

This lower risk-adjusted return, plus a lack of liquidity in the bond market (as banks have been discouraged from market-making by regulatory changes) means that a crisis is possible.

- And the withdrawal of monetary stimulus (reverse QE) could be the catalyst that is needed.

I don’t have any Twitter pics this week, so that’s it for today.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.