Weekly Roundup, 14th March 2022

We begin today’s Weekly Roundup with the oil shock.

Oil shock

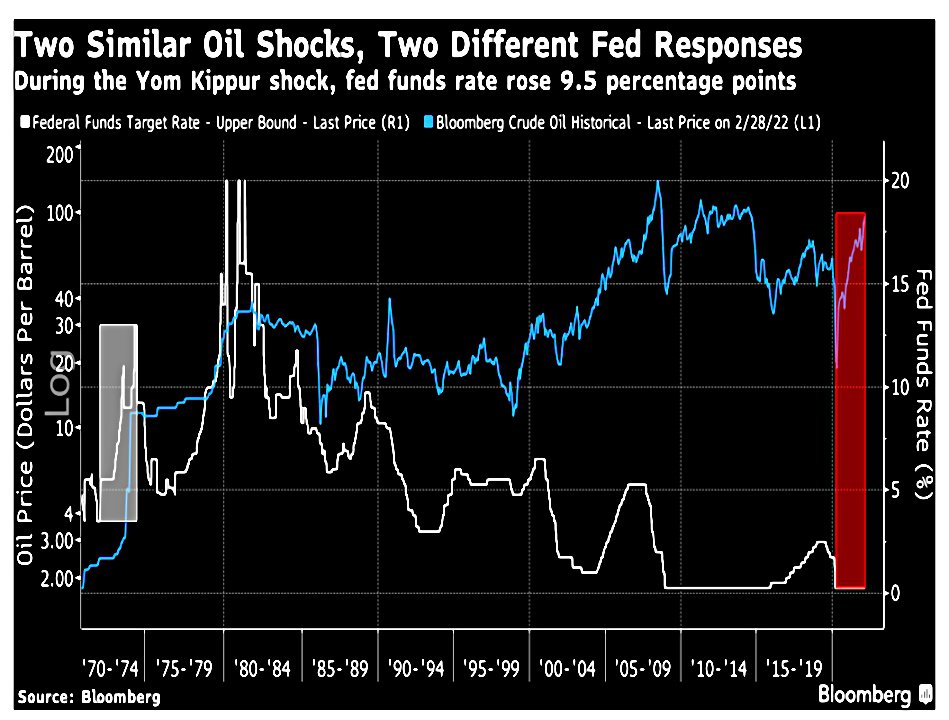

John Authers saw similarities between the current oil shock from Russia’s invasion of Ukraine and the 1973 oil shock following the Yom Kippur war when a group of Arab countries (unsuccessfully) invaded Israel.

- Supporters of Israel were then subjected to an oil embargo, but this time around, the embargo is voluntary.

Incredibly, in percentage terms, this shock to the oil price really is on the same scale as the one from Yom Kippur.

John sees three reasons for comparative optimism:

- Today’s economy is far less dependent on oil;

- This shock started from a freakish low point, not from a position of long-term price stability as in the early 1970s;

- The oil price never gave up its gains in the 1970s, and surged again toward the end of the decade — it’s way too soon to predict that will happen again.

Less happily, inflation is in a very similar situation to 1973.

In the 1970s, the Fed response was to raise rates by 9.5%, from 3% to 12.5%.

- This time we are starting at close to zero, and we’ll be “lucky” to see 2% in rises.

The Fed’s hiking cycle at the beginning of the 1970s has not gone down in history as an error. That title instead belongs to the decision to cut rates again thereafter as the era of stagflation took hold. The shock required a response, but the Fed shouldn’t have then tried to return to normal so quickly.

After Saddam’s invasion of Kuwait in 1990, the Fed paused its ongoing series of rate cuts, leading to a US region recession and Bush losing to Clinton the following year.

- John concludes that the Fed should try to look through big geopolitical events.

He still expects the Fed (and the ECB) to raise rates in March, but as with Isreal and its neighbours, the chances of a rapid solution to the Russia/Ukraine issue are low.

- And so are the chances that the embargo will quickly be lifted.

Global Returns Yearbook

In a second newsletter, John looked at the Global Investment Returns Yearbook from Dimson, Marsh and Staunton (via Credit Suisse) that we looked at last week.

- Luckily, John covered a few charts that David Stevenson didn’t.

![]()

He began by taking us back to the original book from 20 years ago – Triumph of the Optimists, published when the three authors were academics at London Business School.

- This looked at 100 years of returns to work out the equity risk premium (the extra return from stocks over bonds/cash).

Global investors really did get a juicy premium for buying stocks in the last century. The final 50 years worked out fantastically well compared to what was reasonable to fear in 1950. Japan and Germany rose from the ashes, the Iron Curtain fell without a fight, the emerging markets began to emerge.

The book predicted that the equity risk premium would be smaller in the future, and twenty years later, that looks correct.

Non-U.S. stocks have grown at slightly less than 1.2% per annum since 2000. The latest selloff leaves them comfortably below their pre-Global Financial Crisis peak.

That excludes dividends, but it’s still not a great result.

In the long run, stocks have paid off everywhere — although this was only just the case in Austria, a conspicuous loser from the First World War.

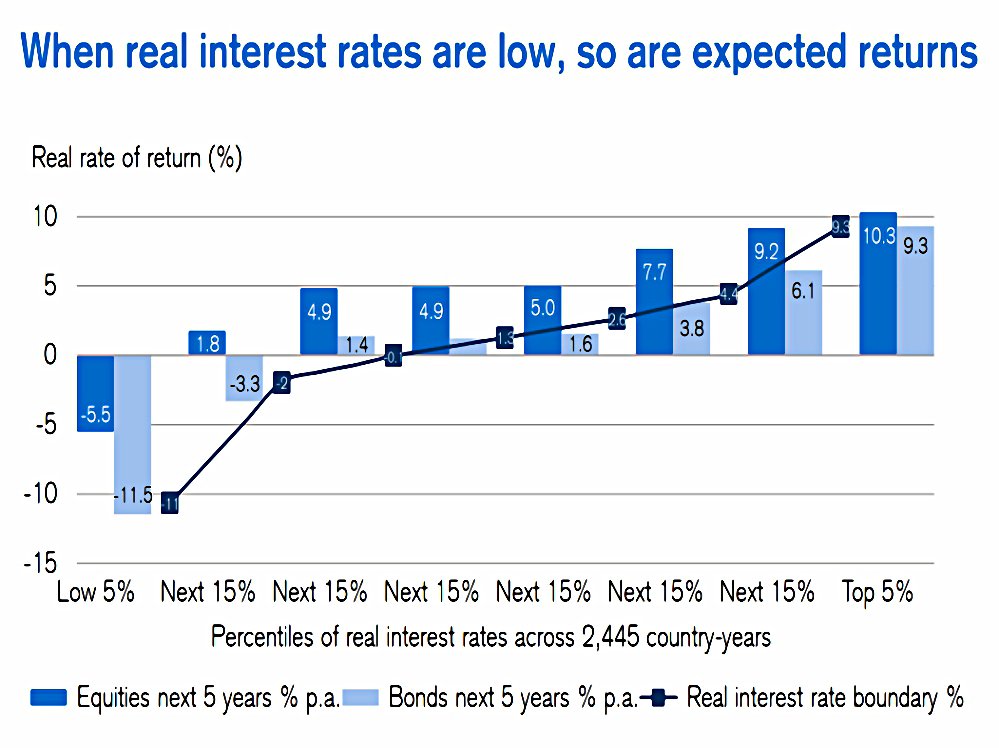

If there is any time not to buy stocks, it’s when real yields are very low. That is a shame, because the Ukrainian conflict has sent 10-year real yields back below -1% in the US.

Bonds should do worse than stocks, but neither looks great from here.

In the short term, equities are not a good inflation hedge. But they do perform better than bonds in all but the most intense periods of deflation, and they generally beat inflation in the long run.

Stocks also do far better in falling rate regimes than in rising ones, but we covered that last week.

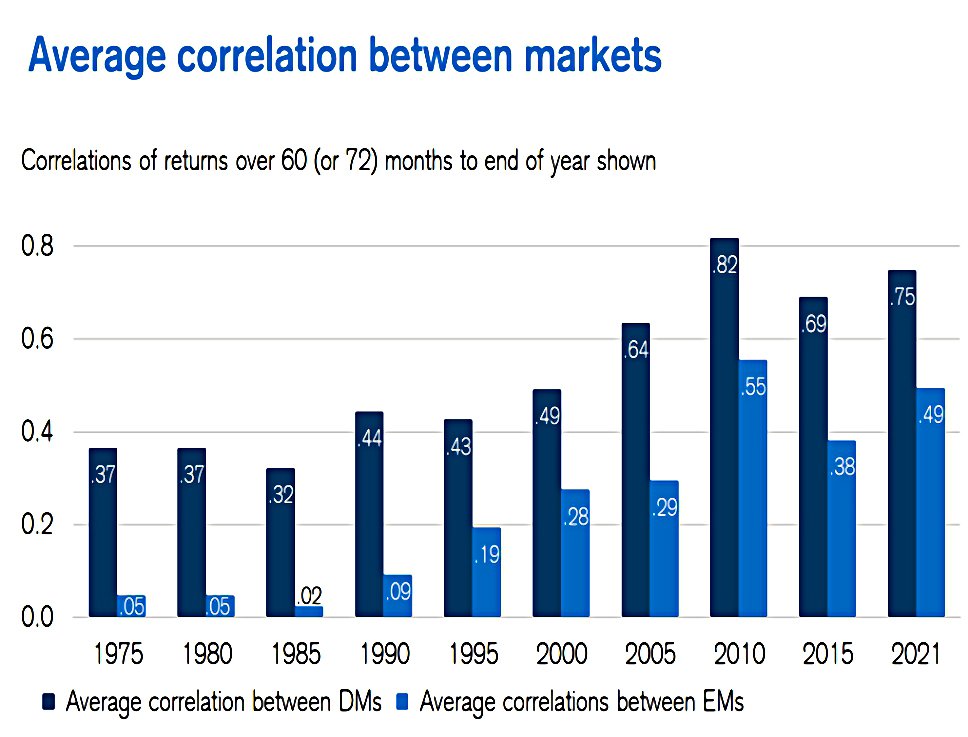

- We also covered the recent rise in correlations between stocks in different countries over the past few decades, as globalisation and the end of fixed FX rates have made nations more entwined.

EM stocks are still useful diversifiers, and correlations between EM countries are lower than those between DM nations.

As expected, correlations increase during a crisis, and in recent crises, they have been increasing from a higher base.

John’s conclusion is not positive:

A period of high inflation and rising rates, starting with negative real yields, is a time when we can expect returns for stocks to be about as bad as they ever are — while bonds should be even worse.

But in the end, stocks do well, and getting out of the market altogether is usually a bad idea.

It makes sense to go searching for opportunities in real assets, led by commodities. And cash makes sense, more for optionality than anything else.

Takeovers

In his regular column in the FT, John Lee said that takeovers had lifted the investment gloom for him.

I have been on the receiving end of more than 50 takeovers or moves to take companies private, including Pifco, Friedland Doggart, Breedon, Delcam, Trafford Park Estates, Wintrust, and more recently Tarsus and Charles Taylor.

In many ways I would have preferred continuing independence and growth, but takeovers, usually at significant premiums to prevailing prices, provide liquidity to reinvest and compound.

This year’s takeover is Air Partner, at a 50% premium.

- John has been on board since 1999, so it’s been a fair wait.

It will give John a 10% cash position in his ISA, so it’s a sizeable holding.

John’s new position is Facilities by ADF, which shot up after its recent IPO, though it has since fallen back a bit.

The company provides a rental range of the trucks and trailers used by actors, make-up artists, technicians on location and sets for the burgeoning content creation sector in the UK and Europe.

Few have appreciated the scale of investment in developing and upgrading studios — an estimated £1bn, according to the British Film Institute, in sites like Shepperton and the new Sky Studios Elstree, with total UK studio space planned to exceed that of Los Angeles.

This has also led John to increase his position in Videndum (formerly Vitec), a global video and photographic equipment company.

DB pension transfers

Also in the FT, Josephine Cumbo reported that the shrinking number of qualified financial advisers had led to a hike in fees for DB pension transfers.

- The FCA is not keen on DB transfers (( My own view is that it depends on the value of the transfer )) and advice is compulsory for anyone who wants to move more than £30K.

But a number of scandals (eg. British Steel) have led to an increase in the cost of professional indemnity insurance for these transfers.

- This in turn has led to IFAs dropping out of the market, with the number of firms providing specialist DB advice falling from about 3,000 in 2018 to 1,160 as of February this year.

John Glen, economic secretary to the Treasury, said:

The FCA and the government believe that it is vital consumers receive suitable advice in this market, considering the long-term financial implications of a pension transfer, and continue to monitor the situation closely.

Some firms are choosing not to offer pension transfer advice and others are charging more, due to the cost of the insurance premiums. The level and structure of advisory fees is a commercial decision for advisers and the FCA do not have a remit from Parliament to regulate the way in which financial advice firms price their services.

In October 2020, advisers were banned from using contingent charging (where the fee is less if the transfer doesn’t go ahead).

- This means that lots of people will end up paying a hefty fee only to be advised not to transfer (which means in most cases that they will be unable to transfer).

Aviva commissioned LCP to survey fees in 2021 and found that they were much higher than the £3K to £4K that the FCA predicted when it banned contingent charging.

- Fixed fees ranged from £3K to £10K, but many advisers used a hybrid model where customers paid £3 to £4K upfront and then 1% of any value transferred.

Former pensions minister Steve Webb, now at LCP, suggested that DB schemes should appoint an IFA to provide transfer advice.

This can be more efficient for the scheme, more cost-effective for the member and provides assurance that the advice is being provided by a firm which has been properly checked out and whose performance is monitored on an ongoing basis.

Quick Links

I have six for you this week, the first three from The Economist:

- The newspaper said that war in Ukraine will cripple global food markets

- And that oil shocks have become less shocking

- And reported what oil bosses are saying about the global energy crisis.

- UK Dividend Stocks said that the FTSE-250 is now in bear market territory.

- Alpha Architect looked at Factor Investing Premiums and the Economic Cycle

- and Klement on Investing warned us not to trust management forecasts.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.