Weekly Roundup, 15th August 2022

We begin today’s Weekly Roundup with jobs and inflation.

Jobs and Inflation

The Economist reported on two US data points – the 530K jobs created in July, and then the lower inflation figure (down to 8.5% from 9.1%) the following week.

- There was no month-on-month inflation for the first time since early 2020.

Falling oil prices were the main drive, with core inflation still at 5.9%.

Meanwhile, the unemployment rate fell to 3.5%, the same as just before the pandemic (a 50-year low).

This labour market tightness is what has encouraged Jerome Powell to believe that lowering demand for new workers might not lead to mass unemployment.

- This is linked to the NAIRU – the non-accelerating inflation rate of unemployment. which is the lowest rate that doesn’t produce higher inflation.

The NAIRU used to be estimated in the 4% to 5.5% range but when it fell below this (pre-pandemic) without producing inflation, the Fed stopped looking at it.

- The NAIRU appeared to jump higher during the pandemic when high rates of unemployment didn’t lead to deflation.

It may have reached 8% in 2020, before falling back to 6% in 2021.

Now, the economy may be experiencing the flipside of an elevated NAIRU: higher-than-expected inflation as unemployment falls. A gap between the measured unemployment rate of 3.5% and the estimated natural rate of 6% implies that wage growth is likely to remain strong in the coming months.

That will feed through into core inflation. A pessimistic interpretation is that the Fed may have to keep raising rates until measured unemployment approaches the NAIRU.

Which would mean millions of lost jobs – so a preferable solution would be for the NAIRU to fall as the pandemic-driven disorder in labour markets settle down.

John Authers also looked at the inflation number.

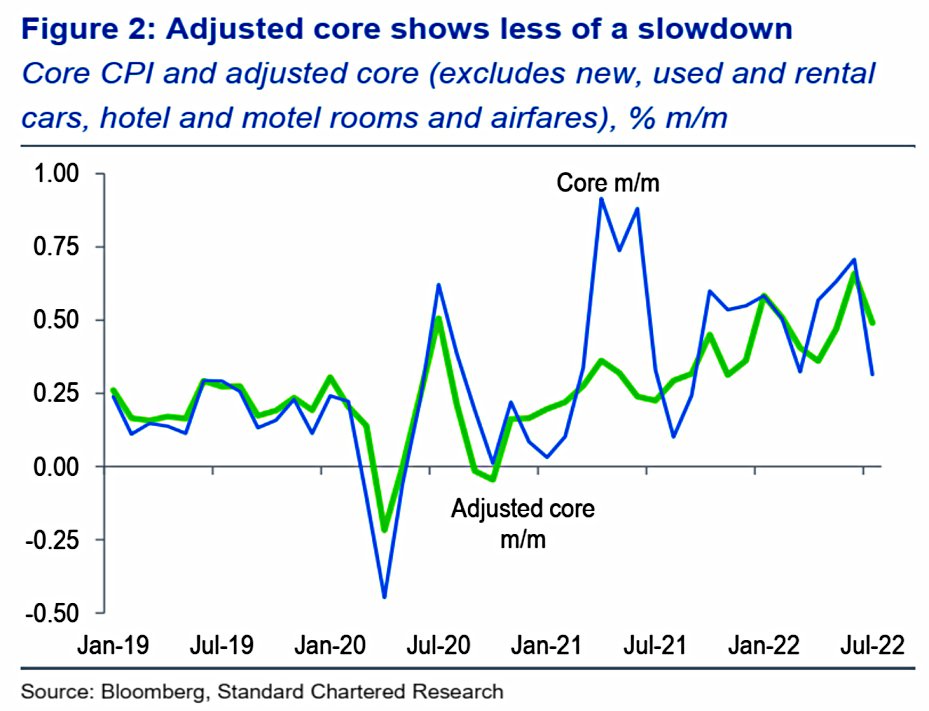

The surge in pandemic-affected products and services is now more than 12 months ago, and so the transitory elements of inflation have disappeared.

The transitory effects are also flattering the core inflation numbers, which look better but not because of monetary policy.

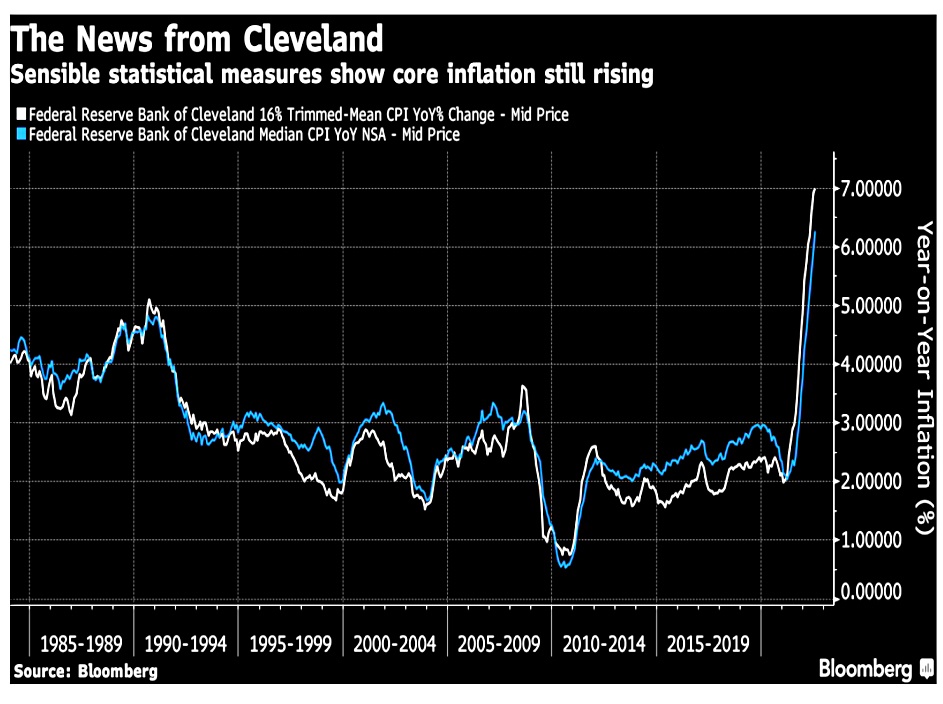

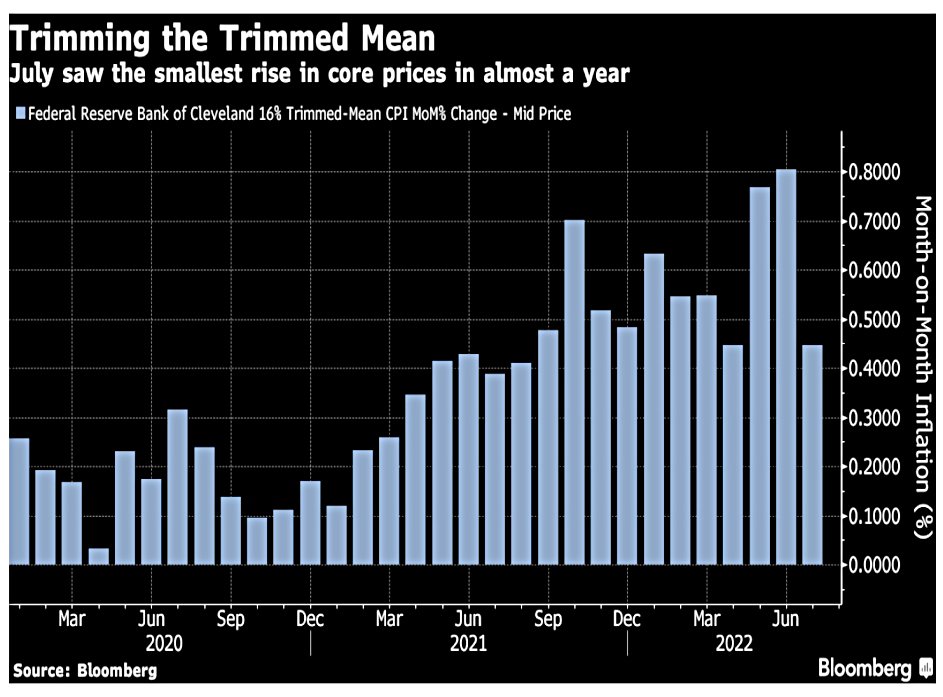

The trimmed mean is still rising.

But not as quickly as before.

The same goes for sticky prices. Then there are housing costs to consider:

Year-on-year inflation in owner-equivalent rent, rose again last month to set a new high since 1990. This number tends to come through with a lag; the number is likely to keep rising — and take core inflation up with it.

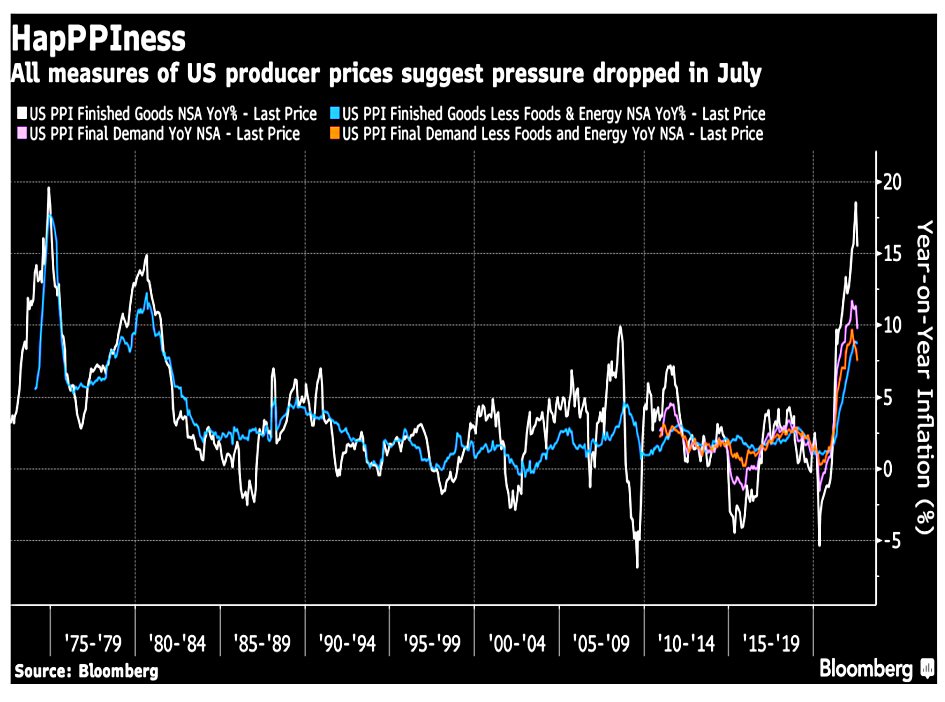

More good news is that producer price inflation dropped in July.

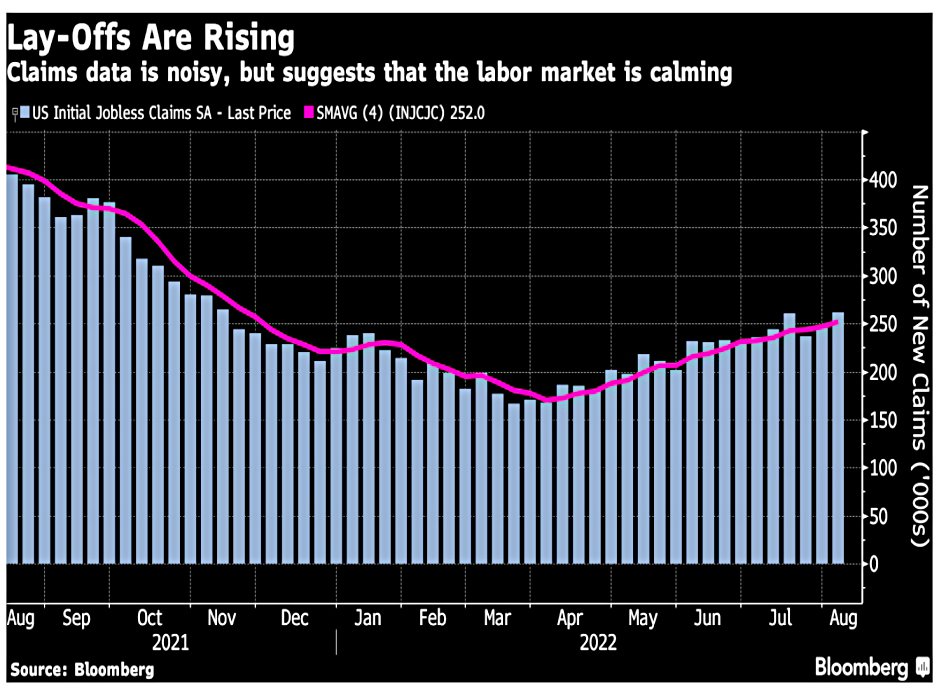

Lay-off are also starting to rise.

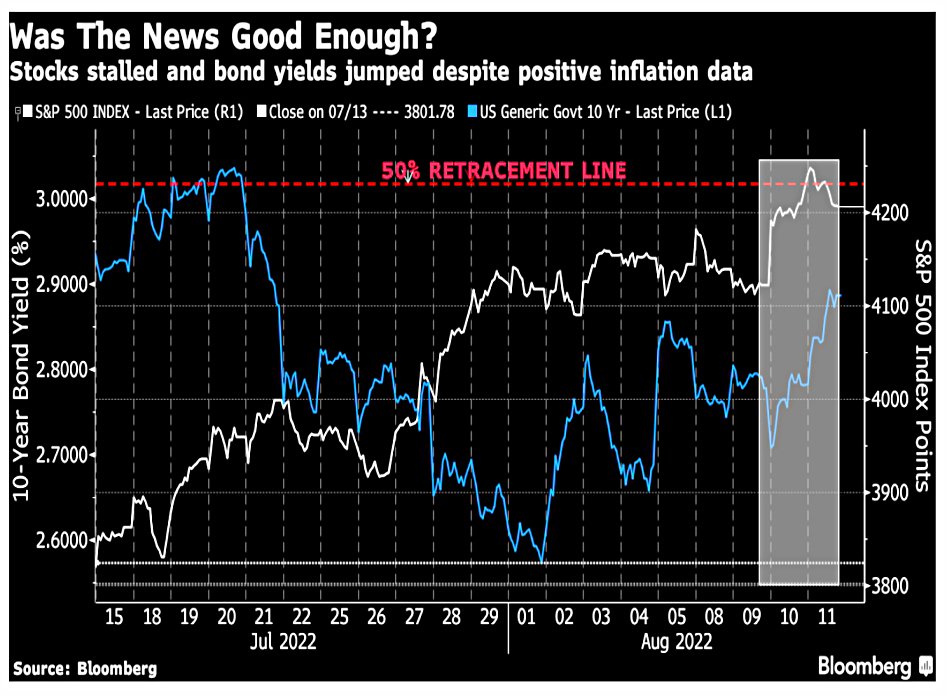

Market reaction was muted.

The S&P 500 started the day very close to retracing 50% of its decline since January. To close above that 50% retracement level would have been taken as a positive signal that the low was in. The S&P crossed the retracement line twice, and then fell back to end down for the day — a classic failed breakout.

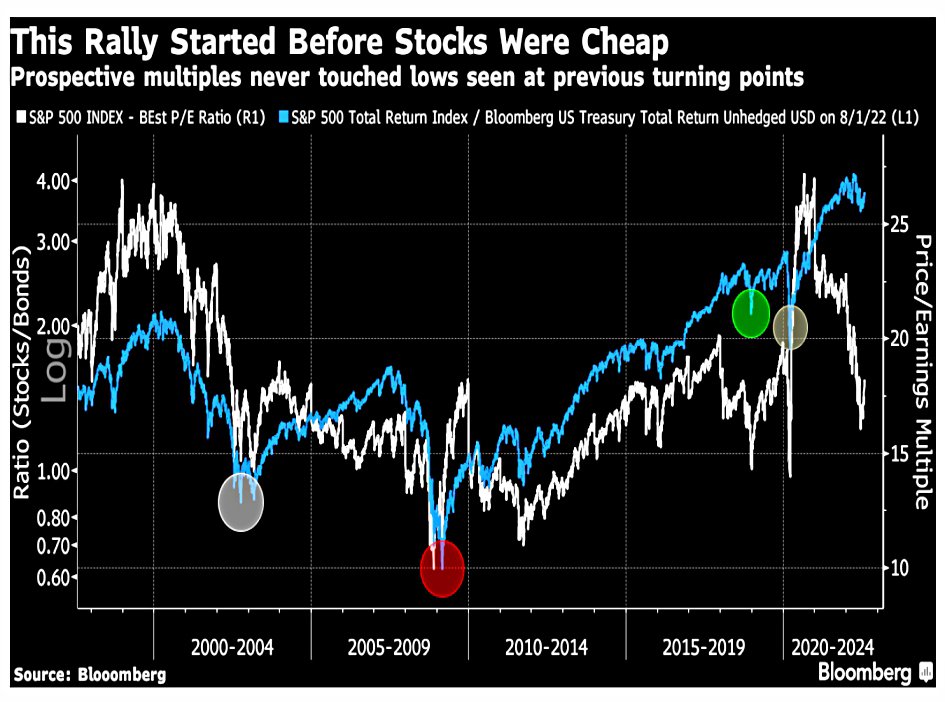

Despite the recovery in July, this sell-off is larger (so far) than the ones in 2000 and 2007.

The recovery (a 7.5% fall in one month, then an equal or larger gain in the next) has only happened six times since WW2.

The others came in October 1974, October 2002, March 2009, January 2019 and April 2020. Regular readers will recognize those as famous buying opportunities when the market was at or near a major bottom. The S&P 500’s average return 12 months after these turnarounds: 30%.

There were also five such signals during the Great Depression of the 1930s, and most were bad times to buy.

John also notes that the recent good signals all came sfter the Fed had slashed interest rates, which hasn’t happened this time.

- But it seems that the market expects a Fed pivot.

It’s also the case that previous bauying opportunities have teded to occur when stocks were cheaper than today:

In all previous cases, the buying opportunity came with the p/e ratio below 15; this time it stopped at 16 and rallied, even though the prospective earnings on which that p/e is based look too high to many people.

On the other hand:

No previous stock market selloff of the last 100 years was preceded by a global pandemic, or the desperate fiscal and monetary measures that accompanied it. But on balance, it’s best to work on the assumption that the bottom is not yet in.

That has been my feeling for many weeks, but the longer this rally continues, the harder it is to maintain that feeling.

NHS pensions

NHS leaders have written to the acting chancellor Nadhim Zahawi to ask for special treatment on pensions for doctors.

- They are worried that high inflation will mean that annual adjustments to the health service’s generous DB pensions will result in doctors breaching the £40K yearly allowance.

The calculation of the annual increase in value of the pot uses CPI.

- Doctors receive a tax bill if this increase is higher than the annual tax-free allowance.

The implication is that doctors will stop working overtime (or even quit or retire), worsening the perceived NHS workforce crisis.

The lifetime allowance (LTA) is also an issue for senior doctors.

Danny Mortimer, CEO of NHS Employers wrote:

We must bring to your attention the very real risk that rapidly rising inflation will deter even more senior doctors from working additional hours — that is, unless urgent changes to pension tax calculations are brought in this year.

The issue of rapidly increasing inflation causing a spike in pension growth is preventing senior medical staff from carrying out the additional work that the NHS desperately needs them to undertake.

The NHS currently has a waiting list of more than 6M people, which would require a lot of overtime to shift.

The BMA has asked for a tax unregistered top-up scheme – this would not attract tax relief, but it would also mean that extra contributions did not trigger tax bills.

- A similar scheme was introduced for judges in April of this year.

This seems fine to me, but the government is not keen because it would not help the vast majority of NHS scheme members (whereas all judges are well-paid).

- It’s a fair point, but the government appears to be treating the issue as an either/or problem.

A top-up scheme would mean that NHS members could have both.

In FT Adviser, James Coney makes a good point:

The annual allowance works well for DC schemes but poorly for DB schemes and vice versa for the lifetime allowance. Having an annual allowance only for DC, and a lifetime allowance only for DB would be practically impossible to administer though.

I’m not so sure, but I doubt that any government would be keen to find out.

Redwood

In his regular FT column, John Redwood said that we a paying a heavy price for the central banks’ money creation.

The leading western central banks — the Federal Reserve, the European Central Bank and the Bank of England — did not target or worry about money and credit, while actively promoting a major expansion to offset the impact of lockdowns and supply chain interruptions on general activity. Each of them continued the money creation drive well into the recovery and have ended up with inflation nudging double figures.

John sees the ECB as the worst of the bunch, and Europe as uninvestable:

The EU economy is suffering from an energy shortage, made far worse by the violent invasion of Ukraine by Russia and the need to take Russian energy out of Europe’s supply sources. It has been damaged more directly by the war and sanctions than the US. On climate change, it has embarked on a vigorous net zero path which means closing or adapting a lot of its more traditional industries.

More generally, he is becoming optimistic:

Much of the damage to bond and share prices we expected this year has been done. Markets are adjusting rapidly to a new world of higher inflation in most advanced countries. I continue to look for ways to earn a better return on the substantial cash the fund has been running, now that markets recognise more of the stresses ahead.

Capital Gearing

The FT interviewed Peter Spiller, the manager of the Capital Gearing investment trust since 1982 (during which time the trust has had only one losing year). (( Pretty much the same as my record, as it happens ))

- CGT is a wealth preservation trust, a category which has come back into fashion as markets have become choppier; others include Ruffer and Personal Assets.

These trusts focus on avoiding losses and beating long-term inflation rather than shooting for the moon.

Peter thinks that we should look to the 1960s rather than the 1970s for a guide to today’s markets.

- He says that inflation won’t get as high as in the 1970s, but could be very persistent:

What we are going back to is an era when inflation is a problem and the authorities will feel constrained to tighten policy whether monetary or fiscal . . . and we will have recessions. I would not expect hyperinflation but I would expect the 2 per cent target to be missed.

CGT has a third of its assets in index-linked government bonds:

The very good news is that the price you pay for that protection is very low because [the market] assumes inflation is going to go back to 2 per cent and stay there.

Other investments include oil stocks, green infrastructure, real estate and Japan as well as 20% in cash.

We think the world is very fragile and we might get quite a lot of opportunities going forward.

Quick Links

I have seven for you this week, the first three from The Economist:

- The Economist looked at which European countries are most vulnerable to surging energy prices

- And noted that after a Covid adrenaline rush, biotech is crashing

- And said that short-sellers are struggling despite a bad year for stocks.

- Alpha Architect looked at litigation finance as an alternative investment

- And compared Buy and Hold with Trend Following in Treasury bonds.

- UK Dividend Stocks explained why Telecom Plus has been sold after recent share price gains

- And Mauldin Economics said that we are curving towards stagflation.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.